Every now and then someone asks me to write a post about long-term care (LTC) insurance.

Every now and then someone asks me to write a post about long-term care (LTC) insurance.

In addition, the topic comes up now and then in a post I write.

I have been reluctant to get into it because many readers find insurance to be one of the least-interesting personal finance topics (I can tell in my site’s numbers every time I write about it).

That said, it’s an important subject as many of us face this issue not only for ourselves but for our parents as well.

So I thought it was time for me to tackle the subject.

Let me say that I am no where near being an expert on this subject. I do not currently have LTC insurance nor does anyone in my family. I am not an insurance agent nor do I play one on the internet.

In other words, take what you read with a grain of salt.

I’m hopeful that those of you who do know more about the subject will leave comments — especially those who have personal experience using LTC insurance for yourself, a family member, or a friend.

To educate myself on the subject I did what anyone does these days, I headed to Google. Ha! I typed in a few search terms and opened the top ten results.

These often led to even more posts. In the end I read almost 20 different articles and used their findings to write this post.

Today’s post will focus on the basics: what is LTC insurance, how likely is it that you’ll need it, and what are the costs on both sides (cost of care and cost of the insurance)?

Then next time I’ll get into who might need LTC insurance, the issues to consider, my thoughts, and what we’re doing.

Let’s get started…

What is LTC Insurance?

Unless you’ve been living under a rock, you probably have at least a vague idea of what long-term care insurance is.

But just to be sure we’re all on the same page, here are several definitions from a variety of sources:

From Nerd Wallet:

Long-term care refers to a host of services to help with “activities of daily living,” such as bathing, eating and remembering to take medication. Regular health insurance and Medicare pay for medical expenses. But they don’t pay for custodial care, which is the nonmedical help with routine activities. Medicaid, the federal and state health insurance program for low-income people, pays for nursing home care. But you have to spend most of your money first before you qualify.

From NPR:

This type of policy covers basic daily needs over an extended time. While health care insurance or Medicare helps pay for immediate medical expenses, say, a surgeon’s bill, long-term-care insurance helps people cope with the cost of chronic illnesses, such as Alzheimer’s disease, or various disabilities. The policies pay for assistance with everything from the basics — bathing and dressing — to skilled care from therapists and nurses for months or even years.

From Aging in Place:

Put simply, the term “long-term care” refers to the assistance offered to an individual with a chronic illness or disability over an extensive period. If you end up being diagnosed with a chronic disease, don’t expect your Medicare or Medigap Insurance policy to pick up the bill. Other programs such as Medicaid have stringent financial requirements, which you’re likely not to qualify for.

From AARP:

The phrase “long-term care” refers to the help that people with chronic illnesses, disabilities or other conditions need on a daily basis over an extended period of time. The type of help needed can range from assistance with simple activities (such as bathing, dressing and eating) to skilled care that’s provided by nurses, therapists or other professionals.

Employer-based health coverage will not pay for daily, extended care services. Medicare will cover a short stay in a nursing home, or a limited amount of at-home care, but only under very strict conditions. To help cover potential long-term care expenses, some people choose to buy long-term care insurance.

I think those cover the subject nicely. Quite simply we’re talking about insurance which covers the (generally very high) cost of caring for an (usually elderly) individual who can’t care for themself.

I think we’re all pretty familiar with long-term care facilities, and LTC insurance is meant to help pay for this sort of service. It could also be used to pay for home-based care.

Why Would Someone Need LTC Insurance?

Simply because a type of insurance exists doesn’t mean that any particular individual needs it. Otherwise we’d all be carrying about 1,000 policies for everything from alien abductions to bed bugs.

But in this case the answer to why someone might need LTC insurance is clear: long-term care can be VERY expensive.

Imagine paying a team of professionals to house, feed, oversee medication dispensing, offer social activities, and the like for a person. That’s going to cost a chunk of change.

However, before we get to how expensive it could be, let’s look at the chances anyone actually would use this insurance.

In other words, how likely is it that your LTC policy will actually pay anything out?

Here are some stats from various sources…

From Nerd Wallet:

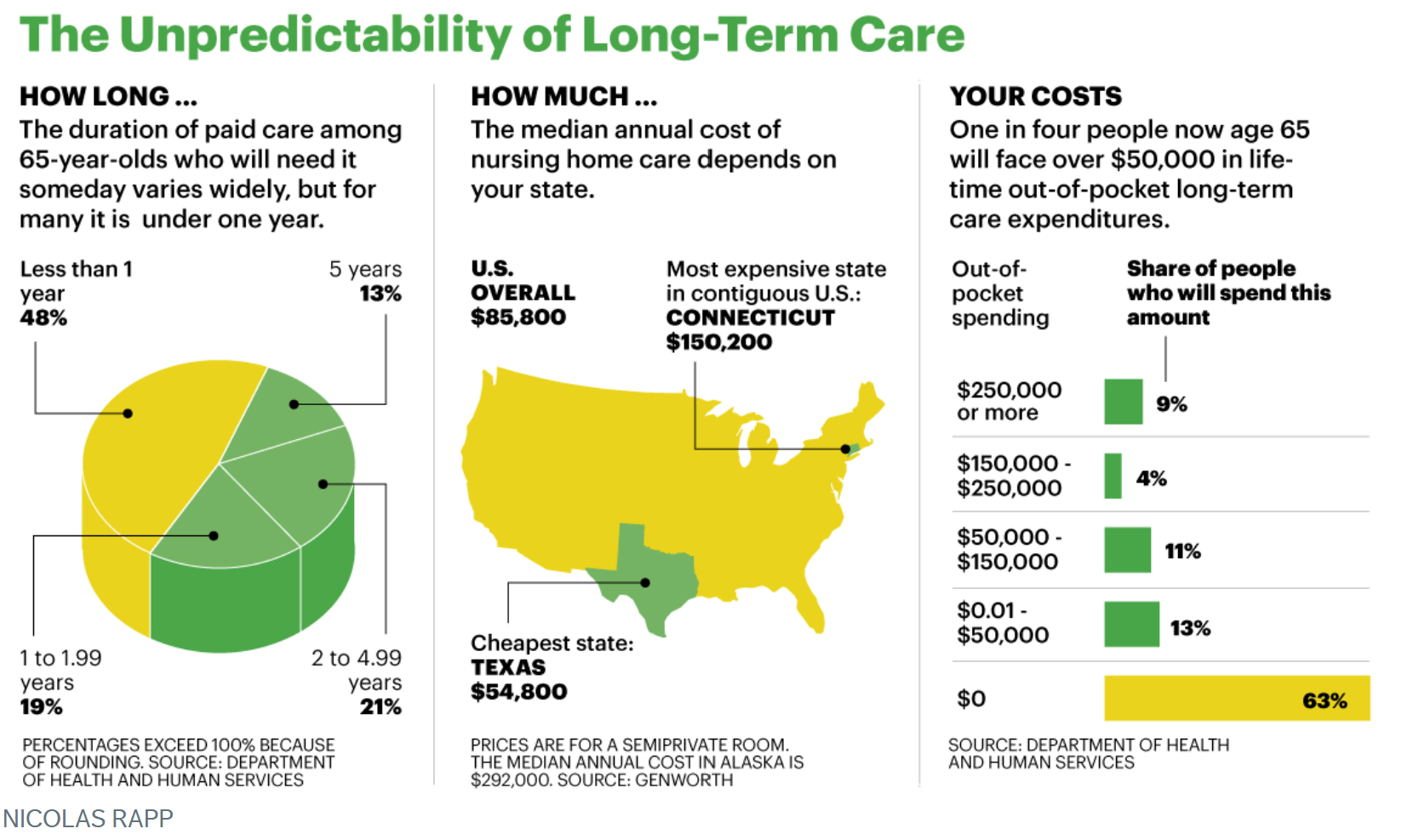

Among 65-year-olds, 52 percent will eventually develop a disability and require long-term care services, according to a study by the Urban Institute and the U.S. Department of Health and Human Services. Of those who require long-term care, men will need services for an average of 1.5 years, and women will need them for an average of 2.5 years.

From Dave Ramsey:

52% of people turning 65 today will need long-term care at some point.

From Forbes:

Only about 25% of people need long-term care for more than two years, and the probability of needing it for more than five years is only 2% for men and 7% for women.

Also from Nerd Wallet:

About half of 65-year-olds today will eventually develop a disability and require some long-term care services, according to a study revised in 2016 by the Urban Institute and the U.S. Department of Health & Human Services. Most will need services for less than two years, but about 14% will require care for more than five years.

From AARP — thoughts and a chart:

By the time you reach 65, chances are about 50-50 that you’ll require paid long-term care (LTC) someday.

From Kiplinger:

Half of men and nearly 40% of women who use nursing-home care never have a stay exceeding three months, according to a recent study by the Center for Retirement Research at Boston College.

From PBS:

If you do invest in such a long-term care policy, the probability of collecting on it is low. According to Prescott Cole in a recent article in the Wall Street Journal, about two-thirds of seniors stay in a nursing home for less than 90 days, which means that they get no compensation from their policies. Furthermore, fewer than 6 percent of those admitted will still be in the nursing home after two years. In fact, fewer than 4 percent of seniors currently reside in nursing homes.

What I get from the above is this:

- The chances are even (50/50) that you’ll need some care at some point.

- The care you’ll need will likely be for a relatively short period of time.

That said, we all probably know people (even if they are relatives of friends) who are 95 years old and have been in a nursing home for 20+ years. This is where the costs can really add up.

If you want more facts about LTC insurance in general, here’s a list of 75 Must-Know Statistics About Long-Term Care.

What are the Costs of Long-Term Care?

Ok, so there’s a decent chance that many will need some form of long-term care and it’s likely that care will last a year or two.

Now, how expensive is long-term care? What exactly is the cost we’re trying to protect ourselves from?

Like most other lifestyle decisions, the answer depends on a myriad of choices and situations — it’s difficult to offer specific guidance because there are so many variables.

That said, I looked for articles which gave a general feel for costs so we at least know the ballpark we’re dealing with.

We’ll start with Forbes:

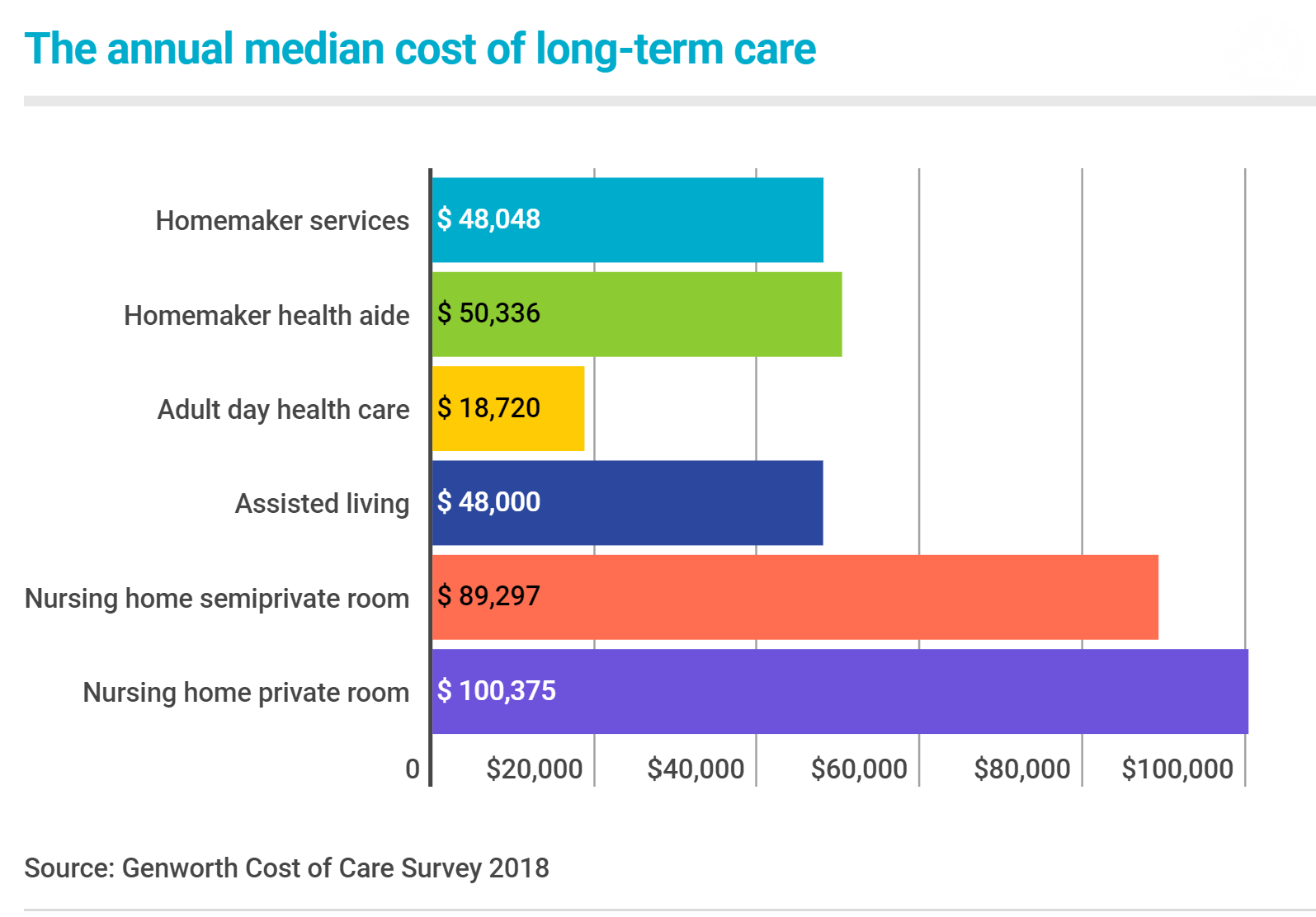

The median annual cost of a private room in a nursing home is now $92,378…The median annual cost of an in-home health aide is $46,332.

Also from Forbes:

How much will you spend for long-term care? That is going to depend a lot on the type of care you need and the area of the country in which you live. According to Morningstar, the average end-of-life cost in a patient’s last five years is $217,820 without dementia and $341,651 with dementia. This would indicate that a policy with a daily benefit of $125 to $200 for five years would have a high probability of being adequate.

From AARP:

If you pay out of pocket, you’ll spend $140,000 on average.

From Nerd Wallet:

Long-term care costs can deplete a retirement nest egg quickly. The median cost of care in a semi-private nursing home room is $89,297 a year, according to Genworth’s 2018 Cost of Care Survey.

And here’s a nice chart from Nerd Wallet:

From Dave Ramsey:

According to the Alzheimer’s Association, the estimated cost for end-of-life care in 2016 ranged between $217,820 and $341,651.

From NPR:

Such care can be crushingly expensive: Just one hour of home-health-aide care costs roughly $20, while the average private nursing home room costs $87,000 a year.

From PBS:

Over the past two years, the average cost for a private room in a U.S. nursing home has increased annually by 4.8 percent to $94,170 per year (semi-private rooms are about 12 percent cheaper), so the 5 percent inflation adjustment isn’t far off actual recent increases.

I know — lots of answers that don’t seem connected. Told you that costs depended on a lot of variables (which is why we probably have such a wide range of estimates).

That said, one consistent result is that they are all pretty high, especially for the average American.

And when you have a potentially high-cost event that you can’t afford, what do you do? You insure against it.

This is why LTC insurance is even a thing.

What Does LTC Insurance Cost?

Now that we know what LTC insurance is and why we might need it, the next question is usually, “How much does it cost?”

Costs of the insurance will vary just as the expenses above, but let’s hear what the top experts say.

Here’s a summary and a chart from NPR:

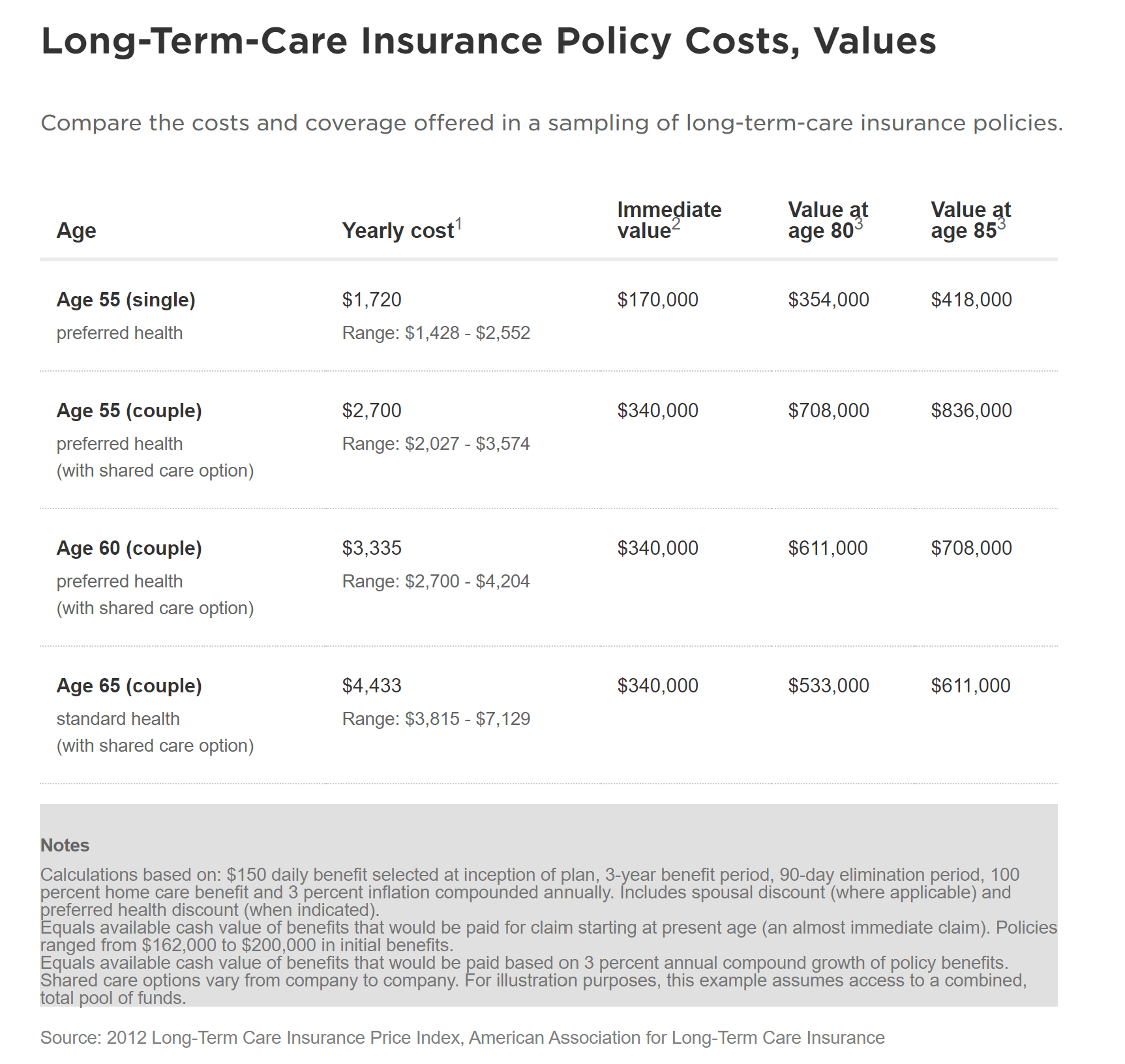

The American Association for Long-Term Care Insurance says people should expect to pay an average of $3,335 per year to cover a couple of healthy 60-year-olds on a plan that pays out a $150 daily benefit for up to three years. But prices can vary dramatically, depending upon factors such as the purchasers’ age, the level of inflation-adjustment protection and whether the daily benefit will be $100, or some larger amount, say, $150 or $200.

From The Motley Fool:

According to Genworth’s (NYSE: GNW) long term care insurance cost estimator, if a typical 60 year-old couple bought coverage that would cover $365,000 apiece worth of lifetime benefits, their premium cost would be around $2,758 each per year ($5,516 per year for the couple). For an individual 55-year-old looking for similar coverage, the price tag would range between $2,760 and $4,057 per year.

From Kiplinger:

The overall cost of new long-term-care coverage has jumped roughly 9% over the past year, according to the American Association for Long-Term Care Insurance, a trade group. A married couple both age 60 can expect to pay $2,170 per year for $328,000 worth of coverage, up from $1,980 last year. Adding inflation protection, which helps the coverage keep up with the rising cost of care, would boost the premium even more.

From AARP:

Premiums for LTC policies average $2,700 a year, according to the industry research firm LifePlans.

Many articles talk about the fact that this insurance is expensive and I guess it is for many.

That said, it doesn’t seem wildly expensive to me.

Other Long-Term Care Insurance Issues

Before we move on, I found several issues that didn’t fit elsewhere. Let’s review these now.

From NPR:

These days, policies typically are capped at three years because open-ended plans have proved too risky for the insurer. The insurance association points to the case of a woman who purchased coverage at age 43. For three years, she paid her annual premium of $881. Then, she needed care, so she stopped paying premiums and initiated her claim. Her care lasted 15 years and cost the insurer $1.7 million, the association said.

It’s cheaper when you sign up by age 60. You have to be medically healthy to qualify. But, like auto insurance, a policy generally has no “surrender” value. That is, if you never have an auto accident, then all the money you spent on car insurance is gone forever. Typically, that’s how it works with long-term-care insurance; i.e., you may pay and pay — and never get back a penny if you don’t medically qualify for care.

Good to know — the coverage may be limited by both time (three years in the piece above) and amount (i.e. $150 a day maximum).

“You have to be medically healthy to qualify.” Here’s another issue: you don’t want to pay a gazillion years and not need the coverage but you also don’t want to wait so long that you’re no longer able to get it. It’s a balancing act for many.

From Forbes:

If you are thinking of obtaining long-term care insurance, it’s best to apply when you are in your 50s. The denial rate is just 17% for applicants in the 50-59 age range. For those aged 70-79, it rises to 45%. The average annual premium is $2,772. And only 0.5% of all businesses offer long-term care insurance to their employees.

From Dave Ramsey:

It’s common for people to try to cheat the system by moving assets out of their parent’s name to get the government to pay for LTC. That is considered fraud—a federal crime—and the government will prosecute you! The government is already having trouble paying for those on Medicaid. Do you really want to count on the government to pay for your long-term care? No way!

I’ve heard of people doing this but not sure how many.

But look at the net worth of the average American and there’s not much there to shelter anyway.

From Nerd Wallet:

The number of insurance companies selling long-term care insurance has plummeted since 2000. More than 100 insurers were selling policies in the late 1990s, according to a 2016 study published by the National Association of Insurance Commissioners. Less than a dozen are selling policies today.

The uncertain cost of paying future claims as well as low interest rates since the 2008 recession led to the mass exodus from the market. Low interest rates hurt because insurers invest the premiums their customers pay and rely on the returns to make money.

The market is continuing to change. Genworth, one of the largest remaining carriers, suspended sales of individual long-term care insurance through agents and brokers in March 2019. The company sells policies to groups and directly to individual consumers through its own sales department.

Long-term care insurance can have some tax advantages if you itemize deductions, especially as you get older. The federal and some state tax codes let you count part or all of long-term care insurance premiums as medical expenses, which are tax deductible if they meet a certain threshold. The limits for the amount of premiums you can deduct increase with your age.

One big concern is that you get a policy and then your insurer decides to leave the business of offering LTC insurance policies. Not sure what the implications are for current policy holders when that happens, but they can’t be good.

From Kiplinger:

Although many consumers have traditionally thought of long-term-care policies as coverage for the catastrophic scenario of a years-long nursing-home stay, about half of new claims are for in-home care, says Bonnie Burns, policy specialist at California Health Advocates. And, she says, the common perception that a person in long-term care progresses from her home to an assisted-living facility to a nursing home “is really not proving to be true” in many cases.

From Forbes:

A few health reasons you might be turned down for long-term care insurance, according to the U.S. Administration on Aging: you have a progressive neurological condition such as multiple sclerosis or Parkinson’s; you have metastatic cancer; you have any form of dementia or cognitive dysfunction or you have AIDS.

Insurance companies keep dropping out of this market because they can’t seem to make a buck selling long-term care insurance. As Ko wrote in her paper, “a decade ago, there were more than one hundred insurance companies writing private long-term care insurance policies. Today, only a dozen remain.” Major carriers that have left include MetLife and Prudential.

That makes me wonder whether a company selling a policy I buy today will stand behind it (or even be in business) when, or more accurately if, I need it in, say, 20 or 30 years.

From AARP:

Long-term care policies can pay different amounts for different services (such as $50 a day for home care and $100 a day for nursing home care), or they may pay one rate for any service. Most policies have some type of limit to the amount of benefits you can receive, such as a specific number of years or a total-dollar amount. When purchasing a policy you select the benefit amount and duration to fit your budget and anticipated needs.

Insurers often turn down applicants due to preexisting conditions. If a company does sell a policy to someone with preexisting conditions, it often withholds payment for care related to those conditions for a specified period of time after the policy is sold. Make sure this period of withheld payments is reasonable for you. If you fail to notify a company of a previous condition, the company may not pay for care related to that condition.

Here’s another issue: you need the insurance and the company fights you on it and/or limits what you receive. Anyone else thing this is standard operating procedure for insurance companies?

As you might imagine, there are many more issues surrounding this type of insurance, but these give you a good feel for it.

That’s it for today. Anyone want to add something? Is there anything I missed or got incorrect?

For more information on this subject, this series continues with Who Needs Long-Term Care Insurance?

I understand that if applying for Medicaid the government will examine your assets for the last five years so if you want to go that option you need to be asset free for that period of time.

Another lower cost option is to receive LTC overseas at a fraction of this price but you would need to explore and be comfortable in this environment.

-Mike H

My wife and I are planning to do LTC if needed in a foreign country. Here are some pointers and estimates to help readers ballpark this:

1. Choose a low-cost country (as compared to US or Canada). E.g. Mexico for us.

2. Make sure you are comfortable in that country. E.g. living in that country for ½ of the year or more. (We live full time.)

3. Learn the language since this will save you about 40% of cost because the support persons that know English well will charge about 1.6 times as much. Plus, there will be a lot more supply of nurses, home health aides, etc. if language is not an issue.

4. Beyond normal costs of living in a country, the added costs for full-blown LTC will roughly be $30,000 for one person and $35,000/year for 2 persons in the same house. E.g. in central Mexico, you will be overall adding this much to $40,000 to 50,000 base for luxurious home living if you bought your own home.

Not for everyone but may be useful for some. (US embassy says that 1 to 3 million US citizens live at least 6 months a year in Mexico. I estimate 30% to 40% of them are retired. I understand that many other US citizens are young Mexican Americans who also had to leave when their parents decided to leave US (either deported or made the life-choice decision.)

Here are a few other points regarding LTCi that we found helpful:

> As you indicated, and because much of what we read indicated that the odds of needing LTCi were about 50/50, we decided to partially self-insure so as not to spend a lot of money on premiums for coverage that we had even-odds of never needing. We budgeted for that possibility in our retirement planning. Should we not need long term care, the funds are there for us to use, or for the one who outlives the other (or for our heirs).

> Regarding protecting assets —> This is one of the reasons we purchased a LTCi Partnership policy. This type of policy offers special Medicaid asset disregards (in case we ever have to go that route).

A Partnership-qualified (PQ) LTCi policy provides a benefit described as “dollar-for-dollar” asset disregard or “spend down” protection. Individuals who purchase a PQ policy ‘earn’ one dollar of Medicaid asset disregard for every dollar of LTCi coverage paid on their behalf. The Partnership Program also protects those assets after death from Medicaid estate recovery.

> Finally, regarding deductibility of LTCi premiums. Though we used to deduct our LTCi premiums, with the recent change in the tax code as a result of the TCJA of 2017 (doubling of the standard deduction, plus our home mortgage paid off and very few other itemized deductions now), we now use the standard deduction and the deductibility of LTCi premiums is no longer a benefit.

Thanks for the article. It provides the basic information that anyone can use as they start down the investigative path for LTC coverage.

I was a medical social worker and know how expensive arranging care can be. I’m in Southern California and home care is around $25/hour. A nursing home is close to $10,000/mo. Patients who had LTC insurance often had a 3 month waiting period before insurance would pay anything and then it was such a hassle for them to actually get the company to pay. I decided insurance was not the way to go for me. Fortunately, we have a paid off house in an expensive neighborhood. We will use our house to pay for LTC. When we are no longer able to safely be at home, we will sell the house and move into a nice assisted living facility. We don’t have children, so we’re fine spending all our money on any care we might need. We will also have whatever retirement funds are left. When the time comes, I want to spend our house! I can see a problem if LTC was needed for only one of us because of dementia. Memory care units are much more expensive than assisted living, but we have enough saved in retirement for many years. Deciding on LTC insurance is a personal decision based on your circumstances, but it is a good idea to start thinking of a plan knowing anything can change.

Short version:

My Mom spent 17 or so years paying into LTC insurance. She paid over 75k in premiums.

When her doctors declared her terminal last year and she went under hospice care and a private nursing home they still refused to pay. She didn’t meet all their criteria.

Family attorney recommended letting it go. She died within six months of diagnosis so not enough money owed to make it worth the cost.

Based on one experience I say it’s a scam. But obviously I am biased.

Thank you for the article and facts, as I prefer to make fact-based decisions. Crazy to think there were over 100 companies pushing policies; that speaks volumes.

I view insurance as a tool to provide money when, I don’t have the money.

Term Life Insurance – Protect family future with basics, should I die before reaching FIRE

Homeowners policy & Auto Policy – protect expensive asses, requirement

Umbrella policy – liability protection

Having reached “FIRE”, I now see #1 as no longer necessary, because my net worth can cover any/all expenses.

That being said, I am approaching LTC from the angle of being “self-insured” by establishing an “investment account” with the necessary funds specifically for LTC. Similar to an “emergency fund” or better, an “HSA” account.

The way I see it, the funds need to keep up with “inflation” associated to LTC cost, but can be invested in low cost ETFs and the money is ALWAYS mine to use as I see fit.

GE Capital went bust writing LTC policies. Insurance companies can’t figure out the actuarial side of these policies because there are simply too many unknowns. Predicting with any accuracy what health care costs will be 20-25 years from now is impossible, period. How much validity would you put in someone telling you what the DJIA will be 25 years from now? Would you plan your life around such a prediction?

Secondly, from the philosophical side of life, wouldn’t it be better to use those enormous LTC premiums to enjoy retirement? I would rather travel, pursue hobbies, family and friends than worry about who’s going to wipe my butt 25 years from now.

We had a presentation on LTC insurance at work last year. I was surprised that the basic policy only provided for 3 years of care. Paying even more expensive monthly premiums covered 6 years of care. We’re planning to have enough in retirement savings to cover 3-6 years of care, so we have elected not to purchase LTC insurance. Another factor in the decision is wondering if the company who is collecting the monthly premiums will still be around when the policy is needed.

Thanks for this series on LTC. It is definitely a topic of interest to me and I’ll be reading the comments here for more info. I’ve run my and my husband’s numbers with two different LTC brokers and both times guessed I’m probably better off self-insuring. (If my Vanguard IRAs keep languishing, though, that will become an even less clearcut call.) The negatives included that my husband and I are now aging into the more expensive premiums and that nagging feeling that when I might need LTC coverage 20 years from today, it won’t be there.

I did hear one thing recently that gave me pause, though, about not having LTC insurance. A friend of mine said that her elderly mom’s LTC was a godsend when the long-distance mom took a turn for the worse–because the family just needed to make one call to set all the coordinated services in motion, rather than trying to cobble them together at the last moment on their own. Since I don’t have kids to rely on, a one-stop phone call for professional help in a health crisis sounds appealing.

But then the friend added that the LTC insurer was very strict about who you can hire, when the services begin, what those services can cost, and what exactly the insurance will actually cover. What YOU think you need/deserve might not jibe with their small print. I guess that’s true for all insurance, but even more worrisome when we’re talking possibly two decades down a rocky road.

I guess, as with all things around “how will I age?,” LTC is murky.

I’ve gone back and forth on whether or not to purchase an LTC policy and my current thinking is to self-insure. We contribute the max to our Health Savings Account and I look at those funds in the future as a way to pay for a portion of LTC expenses should the need arise. I also have a Universal Life policy a former employer started for me as part of their executive program. I took over payments when I left the company and have 2 more annual payments to make on that and then no more future obligations. I will have over $100K in cash surrender that I could use for future LTC expenses or I could simply leave those funds in the account and pay out of pocket and when I pass, my heirs will receive a death benefit of ~$260K which would replenish whatever funds that were spent on LTC when I was alive.

For my situation, this seems to be the best option and we will just continue to self-insure for my wife.

Insurance is a form of gambling so one has to play out the odds. Depending on your asset base, the odds favor self insuring vs. premiums spent over time. Plus, there are so many stipulations tied to qualifying for payouts if and when it’s time to execute the policy. Many insurance companies deny qualification as a means to preserve capital. We are self insuring.

Thanks for this article on LTC. My folks bought a policy when they were 75 and 72! My father passed away 2 months before the policy was 10 years old (which would have allowed my my mother to discontinue paying premiums). At the age of 82 my mother met the criteria for accessing her policy and for the next 1.5 years it payed for her excellent care. That allowed her nest egg to pass on to her three children. We decided to use the RMD from an inherited IRA from her to pay for our premiums. My wife did the same with one of her RMD’s when her mom passed. We took the policy out (Genworth) 9 years ago when we were both 57. The Premiums are $1,415 each. The benefit compounds 5% annually as an inflation hedge. If only one of us needs LTC the other gets both benefits for up to 4 years. They way I have rationalized this is that we are using our kids inheritance to ensure that if need be they can care for us without dipping into the rest of our wealth accumulation (or their own funds). If I would have had a bad experience with Genworth and my mothers situation, I probably would not have purchased this insurance. I have heard many horror stories about premiums going up. That has not happened to me yet (9 years), but it might. In that case I will probably maintain the same premium for less insurance.

Good Article.

My folks also bought similar policy to yours…each policy has a rider that allows the other to use up to 4 years of coverage . My dad at age 74 moved into memory care because of dementia…that was 16 months ago. Insurance has been paying on him from the 4th month on (after 90 day elimination period). Absolutely the best money they have spent…at 7K a month to live in the home, insurance has been a Godsend for my mom

Thanks for your comment Bob. Your parent’s experience a perfect example of when LTCi is worth having. Long stays in a care facility can totally ruin the healthy spouse’s lifestyle. All the best.

Several comments have referenced paying for LTC with the sale of the house. It has always been my understanding a spouse may continue to live in the house and it isn’t included in the assets which must be spent down to qualify for Medicaid coverage. Is this understanding correct?

There are limits to how much money the spouse at home can still have in order for spouse needing LTC to be eligible for Medi-Cal (in California). Also, when the at home spouse eventually dies, Medi-Cal will want to be reimbursed from the estate.

Thanks, good essay on LTC insurance. We plan to self insure. Once all the money is spent and the left behind spouse is broke, then that one will do a reverse mortgage and spend the house or take on a renter and live as a pauper on social security. If the left behind spouse needs a nursing home, medicaid here we come.

My mother bought a LTC policy at the age of 63, a few years after my father passed away. She wanted the peace of mind to have insurance policy so she could keep the inheritance for my brother and myself intact. She could have self insured. We did spend quite a bit of time reviewing options on contracts and stability of companies. We bought through USAA who outsourced to another vendor but USAA strength gave us comfort in a good LTC. My mother, age 72 was diagnosed with ALS which is a fast acting illness and we started on the 90 day waiting period of the LTC contract. The LTC company was very supportive and helpful during our difficult time. Unfortunately my mother passed away before the 90 day period had expired. Several times she was able to tell me how happy she was to have bought the policy to help her. Peace of mind was important.

The contracts were not that difficult to read, you just have to take time to read the details, you cannot assume the seller will tell you everything. LTC is a personal decision and no one will know if they needed one until later in life. Self funding is the way my husband and I are going since we don’t have children to leave an inheritance to.

Is there any “rule of thumb” when your assets is above certain level, it is better to self insure?

I address that in the next post…

Mom is on a nursing floor and Dad is in an assisted living apartment in the same facility. Their monthly bill is close to $16,000 for the both of them. Their LTC insurance pays for about 90% for Mom and a smaller portion for Dad, but they still have to fork out about $5500 a month from their reserves. We could shrink that slightly with a smaller apartment for Dad. The 90 day elimination period was a killer as they had to foot the entire bill. Cash flow is really tight right now, but their condo is on the market and under contract so hopefully the proceeds will help out for about 3-4 years. Their policy is with Genworth for four years. Dad could outlast the LTC insurance. Their facility will not kick them out, but they do need to spend down all their assets. My sister and I are ok with that. My sister says she would not put her worse enemy in the Medicaid facilities in their home town.

“My sister says she would not put her worse enemy in the Medicaid facilities in their home town.”

+1

This is not an option for anyone who is aware of the conditions, facilities, staffing, and quality-of-life for those shunted off to Medicaid facilities. What happens, as I witness, is that families don’t prepare, feel free to ‘spend my children’s inheritance’, make poor choices with multiple divorces, paying for a status college for a useless degree, etc. The Medicaid choices are a lot more limited than one might think, and the state doesn’t “have to” do anything; decisions are often delayed indefinitely, and death is the preferred outcome as strange as it sounds. The places are so depressing, that the grown children and extended family doesn’t visit much, if at all. Thank you, L, for making this comment.

Those I know who have had LTC either found it a blessing or a waste of money. For my friend who’s mother had growing dementia starting with short term memory loss but was physically fine he said it was great. She was one who went from home visiting help, to home live in help, finally to a facility that specialized in her type of memory issue, and he used the policy as intended and it was a true benefit to them. Others I know complain their parents, like mine, basically went into the hospital and were gone before ever needing long term care. Based on the class I just took (and their advice is state specific since each state runs Medicare and Medicaid differently within federal guidelines) situations like my friend’s mother who experience the slow decline with lots of prep time are actually the minority. Typically what happens to people who enter a home is they first go to the hospital for something significant (busted hip, stroke, etc.). They stay for a period of time, 20 days, then get put into a rehabilitation center, where they have to share pay with Medicare from day 21 “up to” day 100 at about $160 a day in our state (note some medicare supplemental plans pay this so that may be something you may want to check out at the time you pick a plan). As they near 100 days they are given their 3 day warning. If they don’t or can’t leave, they are transitioned to “nursing home” status and Medicare stops paying. Then it’s all on them.

One critical note: I used quotes for “up to” 100 days because at any time past day 20, say day 63, it is determined that the skilled care they are receiving is deemed no longer helpful, as in they aren’t going to get better, THAT triggers the 3 day warning and they are on their own day 67. This may not happen often, but happens enough to be aware of.

Keep in mind, most states have a 5 year look back policy and most LTCs are only good for three years. If you wait until then, assuming you are mentally capable, to try and transition assets, you will have a hard time “proving” to Medicare those assets don’t count. Don’t even get me started on what is and isn’t an asset, about all we got from the lawyer teaching the class was “it depends on your individual circumstance” since there are exceptions depending on what it is (e.g. a coin collection might count or might not, bank accounts count up to a point if they are joint accounts, etc.), whether you have a spouse, dependents, etc. In the end I guess it just depends. I can say the class I was in strongly recommended LTC if you are worried about it and had a family history of long life. Additionally the state I’m currently in makes it attractive to have LTC. There is a partnership program that if you have LTC, and say it spends $100K to the nursing home prior to your applying for Medicaid, then instead of the applicant’s assets being down to $2.5K to qualify for Medicaid, they’ll make it $100K. That can be significant for a lot of people. So you really need to research this. For myself I’m still on the fence because I believe I will have adequate assets to cover me and/or my spouse, but the course I took brought up a few relevant points I hadn’t considered so I’m going to look into it more seriously in the next year or so. Part of the problem is I’m not convinced I’m staying in this state in retirement and unclear what state I may end up in, and that can have a reasonable impact on my decision.

I purchased a LTC policy for my mom when she turned 60 y/o; twenty years ago with State Farm at $1000/yr. The policy paid something like $200/day with a maximum payout of $250K. The premiums stayed level.

At age 70, mom had a stroke and couldn’t perform the requisite no. of the six “activities of daily living” and, therefore, qualified for full benefits under the LTC insurance. I looked at half a dozen local Assisted Living Facilities; quality varied widely. For some reason, the facility I wanted must have thought my mom was going to be a Medicaid resident and advised no rooms were available. When I told them I had LTC insurance, a private room magically came available; and she was treated as a VIP for her two years there. The ALF rate was $4500/mo. After the mandatory 90-day waiting period, State Farm paid 80% like clockwork w/ zero problems or delays.

At age 40, I purchased an employer-sponsored LTC policy for myself at a group rate with Unum, at $300/yr. When I left that employer, the LTC insurer allowed me to keep the policy at the same rate. The plan includes a 5% simple interest growth factor, and now pays up to three years, at $250/dy, and a maximum payout of $273K. Fifteen years later, my premium is now $550/yr.

Props to “L” for her last comment. I’ve volunteered as an EMT and have been inside a local “Medicaid” facility many times to pick up patients. Depressing, and the staff doesn’t seem to really care for the residents. Quite often, by the time we got the call for a patient, that individual had declined quite a bit.

Andre does seem to have a good story. I’ll have to check with my employer and see what they offer.

My father did not have LTC and spent the last few years in a nursing home. He had a pension, but not nearly enough to cover costs, and his estate dwindled significantly. I had started Medicaid paperwork with the nursing home, but he passed away before it was needed (Parkinson’s, Alzheimers).

As it stands right now, I plan on self insuring. Looking forward to the next installment on this subject.

I think the hardest thing about self insuring will be writing that check every month for $10,000+ Hard to even imagine😱

No worries, if you need LTC, you don’t know what $10000 means anymore 😂

That’s cold…but unfortunately, true.

At age 53 and 50 years of age, my wife and I had purchased a Lincoln Life hybrid policy, placing a set amount of $100k each, of our net worth, into it. It is essentially a life insurance policy with a LTC rider. We were looking to simply take care of filling in that piece of our “financial puzzle” to assure that IF one of us got dementia or Alzheimer’s we would NOT leave the other remaining spouse destitute. Note: we do know that were fortunate enough to have the $200k to pull to the side to do this, but are aware and understand that not everyone is in a position to be able to do this. Best of luck to all looking into LTC insurance, it really is a hard personal and financial choice.

Would you be willing to share the full benefits that your $200K premium policy provides?

Details of interest would be.

1. Are they individual policies or a joint policy? If joint is the life insurance paid at each death or is it a second to die policy?

2. If both of you died the day after buying the policy what was the life payout?

3. Does the life payout increase over time? By how much is it projected to increase?

4. How much LTC will it payout if you need that portion? Are there inflation adjustments built into the LTC payout schedule?

5. If it pays out LTC does that decrease the life benefit? By how much?

6. And Finally, is the policy guaranteed to be good for both death benefit and LTC until you both die or does it have a time in which it will lapse if more money is not put in?

Hello…I would be glad to answer your questions the best I can concerning our “Money Guard” LTC Insurance policies from Lincoln Financial.

1. We have two separate $100k policies. We paid for them at $20k/year/each for five consecutive years until they were fully funded. As I understand it, there are a variety of options concerning the amount/number of “payments” that can be sent towards fully funding the policy. Concerning payout on death, we are each other’s beneficiaries and our children are secondary after the death of the both of us.

2. We were told that after our first payment, the policies were in full force (concerning coverage). I can only assume that the life insurance payout would be applicable to the amount “funded”, but I am not 100% sure on this.

3. The life insurance part of the policy only moderately increases in value with each passing year.

4. We opted for inflation protection (at an additional cost/but a slight reduction in coverage overall) , I believe at 4% yearly inflation increase.

5. Yes, the simplistic way it was explained to us was…”your funds will be the first to be used, and then the policy will pay for any additional funds required”. So also yes, your life insurance “dollars” decrease when you first begin to use the policy.

6. The policy is good for both LTC “monies” and or Life Insurance “monies” for your entire life span. No additional “monies” will ever need to be added to the policy. So…if we need LTC, we will be using up our $100K first then the policy will pick up the remainder of the “tab”. Or, if we never need LTC, then first the remaining spouse, and then our children will be the beneficiaries of the insurance policies +$200k in funds.

For more specific details on how/if a “hybrid” policy could work in your situation/needs, I would just recommend researching Lincoln Financial’ “Money Guard” policies through contacting an independent insurance broker. My hope is that I was helpful in some way, and hope you are able to find an answer concerning the issue of LTC for your specific situation. Stay safe and stay healthy!

Thanks for answering those procedure questions.

You didn’t answer any number questions however.

So lets just talk about 1 of the 100K policies which you fully funded over 5 years.

So specifically how much coverage did the 100K purchase?:

1. Now that it is fully funded, if you die and had never used the LTC what does it pay in life benefit? Presumably 100K +some other amount? How much is that other amount?

2. If you need to use LTC how much will it pay for LTC? Presumably also some number over 100K, but how high will it go? 150K, 200K, 900K, 900 Million? What is the limit? Once you reach that limit, can I presume the policy is exhausted and the death benefit is also zero at that point in time?

I am just trying to understand how one would evaluate this kind of a policy and without knowing what the payouts might look like it would be impossible to evaluate it.

Thanks.

Below are the beat answers that I can give you, since this policy has a lot of moving parts:

1. My death benefit is currently at $235,200, but it slowly decreases to minimum of $129,604 by the time I reach 82 years of age (I am currently 57).

2. Since I had selected a 5% inflation rider, my LTC benefit is currently at $4,824/month (at age 57) and increases over time to the maximum of $37,480/month or $3,658.601 total (at age 99) .

Also, I had forgot to mention earlier, after your policy is fully funded, you can get a return of your “funds” if you cancel the policy for any reason. I would however assume that there would be minor fees taken out.

Again, I hope this helps.