Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in February.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I am 34 years old and my wife is 31 years old.

We got married in early 2019.

Do you have kids/family (if so, how old are they)?

We do not have kids but we hope to have some soon.

What area of the country do you live in (and urban or rural)?

We live in the suburbs of a MCOL US city.

What is your current net worth?

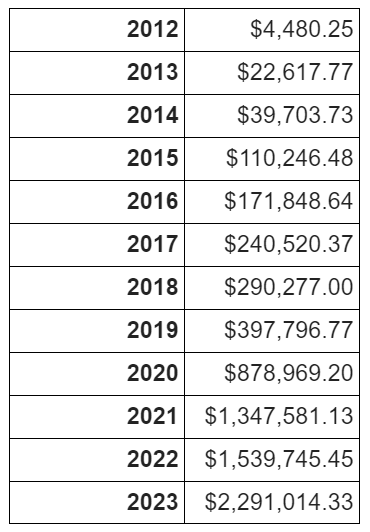

Our net worth as of January 2023 is $2.355M.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

- Taxable brokerage accounts: $1.025M

- Pre-tax retirement accounts: $490k

- Post-tax retirement accounts: $156k

- Savings accounts: $289k

- Checking accounts: $35k

- Home value: $922k

- Mortgage: -$562k

EARN

What is your job?

I am a software engineer in the finance industry.

I build software that connects to financial exchanges and displays the information back to traders and other market participants.

My wife is a management consultant.

What is your annual income?

My annual salary is $135k and my bonus varies as you’ll see in the next answer.

My wife’s salary is $255k and her bonus is usually $80k.

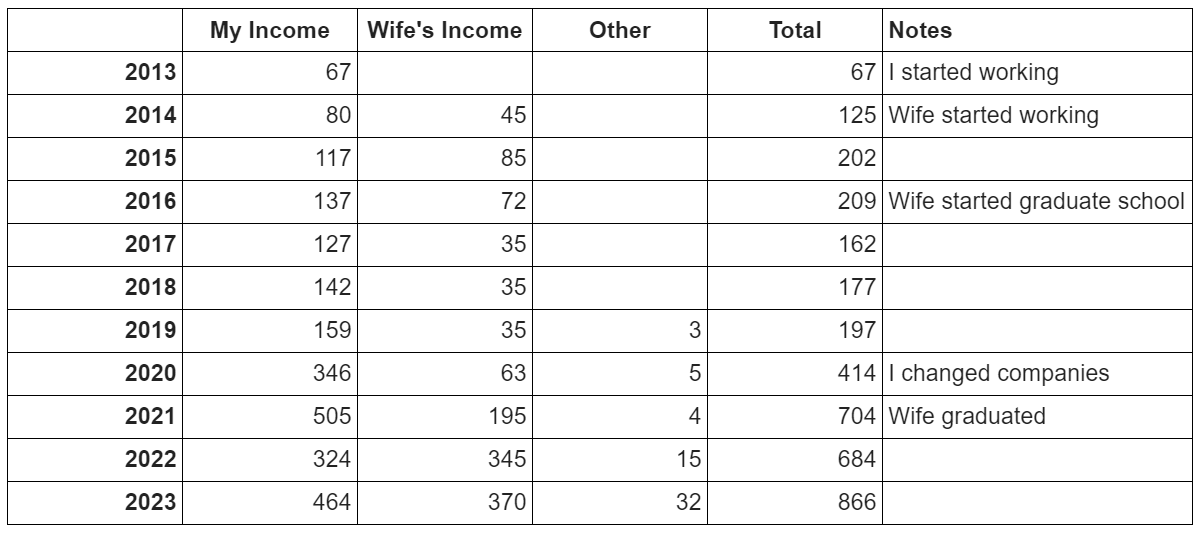

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

I had a few summer jobs during college. They didn’t make much money, but they were valuable learning experiences.

My starting salary was $65k out of college. After two years, I successfully negotiated a 33% raise by taking on more work and then politely telling my boss and his boss that I was doing more work and wanted to be compensated accordingly. (I describe this more in a later answer.) After that, I just got steady $5k to $10k raises annually.

After a few years, I switched companies and got a new compensation model. My salary would be relatively low for a software developer ($135k), but I could get larger bonuses. The work also lined up with my preferred technical interests.

My wife worked for two years after college and then returned to school to get a PhD. After graduating with her PhD, she joined a management consulting firm. Her income has a higher salary but a lower bonus. There is also a predictable career trajectory if she hits her performance goals.

All figures below are in the thousands. The Other column includes income from my wife’s small YouTube channel (about $1k a year), interest from our high-yield savings accounts, capital gains distributions, and dividends.

We don’t expect our income to be this high forever. We will scale back when we have kids.

What tips do you have for others who want to grow their career-related income?

I’m still fairly young so I feel uncomfortable giving advice. But here is what helped my career…

Every business is a relationship business. Treat other people well. Find out your boss’s priorities and make your boss’s life easier.

If you are in a technical field, do not expect to get promotions based on technical skills alone. Improve your soft skills too. The people who write the checks (management) are never purely technical and sometimes feel dumb when listening to specialists talk. Learn to translate technical language to something management can understand easily. They will trust you a lot more as a result.

Also, make sure your boss and company have both the ability to pay you well and the desire to pay you for good work. Some bosses want to pay you well, but they don’t have the money. Other bosses have the money to pay you well, but they don’t want to pay you, for any number of reasons (cheap, don’t like your work, etc.). Find a boss who has both. And this doesn’t just apply to money. If work-life-balance is important, find a boss who values your time.

Check your salary comparisons on Glassdoor and Indeed at least once a year. If your salary is too low for your job title, industry, and location, be prepared to negotiate with this information printed out. My favorite negotiation strategy is to tell my boss a few months before my performance review (before budgets are set for next year) that I plan to negotiate, especially if I took on more work in the previous year. Just knowing that, my boss will give me more thought while planning raises and bonuses. And my boss still has time to increase my pay before “there is no wiggle room this year.”

I did this a few times. The highest I negotiated was a 33% bump up in compensation. I didn’t even “negotiate”. They just gave it to me because I told them in advance that I would negotiate at my performance review because of the extra work I picked up during the year and had the salary data to back up my claim.

What’s your work-life balance look like?

Post-pandemic, I usually work an 8 hour day from home. In the first five years of my career, I was on-call 24/7 and often got called multiple times a night between 1 am and 5 am to fix some broken technology from a different department. I’m glad that is over.

My wife’s work-life-balance is not great. She works 60, 80, and sometimes even 100 hour weeks. She plans to go part-time when we have a child. Ideally she will get 50% of her working time back, but she will also take a 50% pay cut.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

We have some income from interest and dividends. It is growing every year!

My wife used to have a small YouTube channel that made $1,000 a year, but she doesn’t do that anymore since working full-time.

SAVE

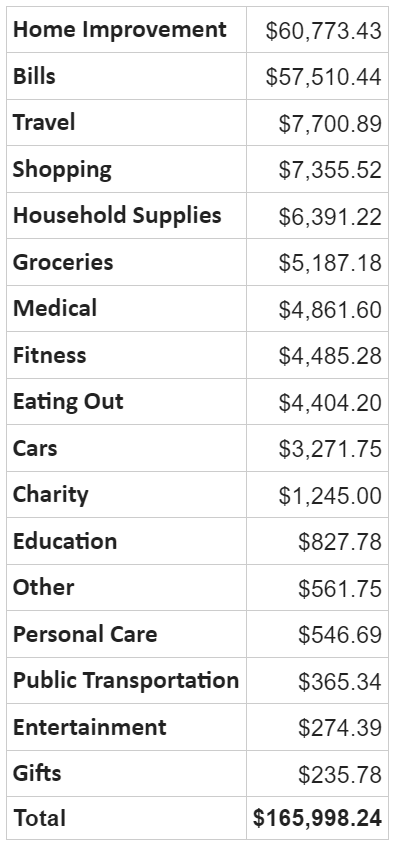

What is your annual spending?

We spent $166k in 2023. That number is higher than what I expect in the future because we spent $60k for home improvements.

We averaged $80k from 2018 to 2022 which helped us put a lot of money into investments. We never felt like we were sacrificing to invest more. We just enjoy inexpensive activities.

I expect that we will spend $120k a year going forward, but who knows how accurate that will be. I can’t predict the future (or my net worth would be higher).

What are the main categories (expenses) this spending breaks into?

Our biggest “expense” is paying ourselves which is putting money into our investment accounts. We put $375k into investments for 2023.

Our next biggest “expense” is taxes (federal, state, payroll) which was $307k. I haven’t prepared my tax return yet so that number is not exact.

Here are how our expenses breakdown by category:

Do you have a budget? If so, how do you implement it?

We have a budget, but it is not a strict spending limit.

My wife created a budget that tracks our spending through a spreadsheet and emails us daily with the remaining amount for the month. We have $2,000 combined of free spending per month. Groceries, restaurants, and discretionary spending come out of that $2,000. Bills and other predictable expenses are taken out beforehand. We monitor our spending during the month using this method.

I also track our spending after each month to get exact numbers. I go through all of our transactions from the credit card and bank statements. Then I categorize them and put them in a spreadsheet.

We use this to see longer trends. I have this data going back to 2016.

What percentage of your gross income do you save and how has that changed over time?

When I started working, I had a rule to save 10% for short-term goals (house down payment, emergency fund) and invest 10% (retirement or brokerage) of all pre-tax income. It wasn’t much when I started out, and it hurt more to save/invest instead of spend. But I learned the discipline to keep saving and investing when my income grew.

Before we got married, my wife was also a diligent saver. She saved $60k in two year before starting graduate school.

Now, we have a nice cash cushion for savings so we only invest extra dollars.

For 2023, we invested about 43% of our income.

What’s your best tip for saving (accumulating) money?

Automate your savings and investments.

If you schedule the money to come out of your checking account the same day your paycheck hits, you will never miss the money you saved or invested. And you will not waste any brainpower trying to decide if you should save, invest, or spend those dollars.

What’s your best tip for spending less money?

Create a fun money savings account and automate some money to that account too.

When it gets large enough to buy something you want, just get it.

This additional account helps me spend less overall by letting me satisfy my desire to buy something guilt-free.

What is your favorite thing to spend money on/your secret splurge?

I used to hire a personal trainer for one session a week along with a plan for the remainder of the week to complete on my own. That was the majority of the $4,000 from the fitness category expenses. I stopped personal training in the middle of last year after my previous trainer left my gym and I didn’t like the new person. I may pick that up again.

My wife likes to do various craft hobbies. She is currently interested in making things out of leather. She only spends maybe $1,000 a year on these hobbies.

We flew first-class last year and I enjoyed it. This might be a regular upgrade while we have a high income.

INVEST

What is your investment philosophy/plan?

I handle the investments for our family so I will speak for both of us in this section.

I prefer simple index funds. I mostly invest in Total Market index funds split between domestic stocks, international stocks, domestic bonds, and international bonds. I want to match market returns and minimize expenses.

I am prohibited from investing in anything that my employer trades, but even if I was allowed, I would not invest in individual stocks or options. Through my work, I have seen many people lose a lot of money trading options and individual stocks.

What has been your best investment?

Marrying my wife. She’s a high earner and a diligent saver. I hope she would say the same about me.

For my best traditional investment, I put a $3,500 signing bonus for my first job out of college in my Roth IRA. It went into a total stock market index fund. The compound interest over a decade makes it my best investment.

What has been your worst investment?

I invested $10k in a Real Estate Index Fund. I still own it and am down 10%. It might be close to break-even if you add the dividends from that fund.

My wife says graduate school. She was out of the workforce for five years and came back to a job she could have done without a PhD.

What’s been your overall return?

I don’t know my exact return because of 401(k) rollovers, but my brokerage firm says my ROI is 10%. I’m fine with that. I just want to match the market and have a long time horizon.

I focus more on maximizing my Lifetime Wealth Ratio, which is the ratio of my net worth to total income earned in my life. I didn’t know this had a name until someone posted it in the MMM forum (thanks MMM!).

How often do you monitor/review your portfolio?

I look multiple times a day. It’s a bad habit that is the result of being bored at work and wishing I could retire.

I also look to make sure there isn’t any unusual activity on our credit cards.

My wife doesn’t look very often. Maybe once a month.

NET WORTH

How did you accumulate your net worth?

We accumulated our net worth primarily through earning high incomes, investing early in our careers, and investing a high percentage of our income. We just followed the simple ESI formula. It started slowly and grew quickly.

I want to note one major benefit we had that many others did not. Our parents paid for most of our undergraduate degrees.

My wife’s parents fully paid for her degree. My parents paid everything except the small federal subsidized loans that were part of the financial aid package.

I took out a manageable $10k in total and paid it off the year I graduated before interest accrued, mostly using money from summer jobs.

Graduating without debt was a huge advantage to get our net worth accumulation started early.

My parents said they would not pay for my graduate degree which is a large part of why I did not continue to get other degrees. My wife’s graduate degree was free and came with a stipend.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

This is a tough one. I think we have a good balance between the three.

Most readers would probably say our strength is Earn because of our high income, especially in the last four years. But I work with plenty of people who make a lot of money and are living paycheck to paycheck.

I think our biggest strength is Save. We saved early and saved a lot which got the compound interest ball rolling.

We are doing well with investments too, but I won’t choose it over savings. I just want to match market returns and minimize fees.

Really, all three are important.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

We had to deal with our parents’ health issues on a few occasions. It was difficult to juggle working and taking care of parents both for managing our time and managing our emotions.

My work was not very understanding of the situation. My wife’s employer was more understanding, but she didn’t get extra time off.

It is difficult to put up with corporate BS when you feel good. It is nearly impossible when you are physically and emotionally drained. I was really tested on my “treat other people well” motto during this time.

What are you currently doing to maintain/grow your net worth?

We are staying the course.

We just keep working and investing every extra dollar in index funds.

Do you have a target net worth you are trying to attain?

My target net worth is $5M.

Withdrawing 4% of a $5M portfolio will give us $200k a year to live off. Even with kids, that should give us plenty of financial room.

But I may stop working before that, as I will describe in the Future section.

How old were you when you made your first million and have you had any significant behavior shifts since then?

I was 31 years old and my wife was 28 years old. She was actually still in graduate school at the time.

We haven’t shifted our behavior much. We are less price-conscious than before, such as getting contractors for home projects. I will pay more for a contractor that will show up on time, finish the job on time, and finish the job correctly the first time.

Also, we flew first class as I mentioned before. That makes traveling more peaceful.

What personal habits and/or traits have you developed that have made you successful at growing your net worth?

The most important trait is the discipline to save and invest at least a combined 20% of our income.

It was enough money to help us grow our wealth, but it was small enough that we never felt frugal.

What money mistakes have you made along the way that others can learn from?

I stayed at my first job too long. The attitude from management was that the company paid below average for the industry in exchange for better than average work-life-balance. It was a lie. After I switched jobs, I got paid more than double and worked fewer hours.

If I knew we would be multimillionaires in our 30s, I might have invested less in retirement accounts and more in brokerage accounts. I would feel less anxious about early retirement if we had more money accessible now.

We also have too much money in savings accounts, even if they are high-yield savings accounts. I wish I invested more of that money in index funds, but I am always planning for that next major purchase on the horizon.

What advice do you have for ESI Money readers on how to become wealthy?

Every millionaire interview says this because it’s true: marry well. If your spouse doesn’t have the discipline to become wealthy, you probably won’t become wealthy. Also, your day is always better if you marry your best friend.

Other than that, treat people well, negotiate your compensation, save 10% of your income for short-term goals, invest 10% for long-term goals, and invest in index funds. I’m sure other investments can work too (such as real estate). Also, be open minded about switching jobs or industries.

Having a large emergency fund gives you more confidence to negotiate your salary and take risks in your career. You don’t have to worry about how you’ll pay your mortgage if things don’t work out right away.

FUTURE

What are your plans for the future regarding lifestyle?

My wife and I want to start a family soon. She will go part-time which will reduce her income for the first few years.

Longer term, we are hoping to reach somewhere near $4-5M within ten years. By that time, I would retire and become a stay-at-home-dad. My wife will continue to work part-time or take a job with better work-life-balance to cover our health insurance costs.

What are your retirement plans?

I hope to retire around the time I’m 40 years old. I want to spend time with my kids while they are young. I’m also tired of corporate life and want to try doing something more creative. I started a side hustle last year, but it is not generating any money yet. There are also a lot of hobbies that look interesting and I want to volunteer in my community.

My wife will work much longer than me to “get the value out of graduate school.” She will work into her 50s, even if it is part-time. Once she retires, she wants to spend more time on her crafting hobbies.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

The big concern is not knowing what to expect with kids’ expenses.

They will need diapers, clothes, toys, braces, and college tuition. I feel like I need to work longer to get through these expenses before I can retire.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

I was always interested in investing. I played those fake stock trading games in elementary school and talked to my dad about his investments. That curiosity is a big reason why I work in finance now.

When I was 19, my older brother gave me a copy of Ramit Sethi’s book I Will Teach You To Be Rich which started me down the personal finance rabbit hole. Then I started reading his blog along with Get Rich Slowly and The Simple Dollar.

I eventually read many other personal finance books. I’ll share my favorites in a later answer.

Who inspired you to excel in life? Who are your heroes?

My parents always wanted me to excel in school. I developed a pride in doing excellent work.

I look up to a former college professor of mine. He was a Fortune 500 CEO in the 90s, then he retired and returned to teach part-time at my university (his alma-mater). He is always so patient and kind to everyone which is very different from the image the media portrays of many hard charging CEOs. I still talk to him from time to time to get career advice. He is a big reason why I believe treating other people well is good business practice in addition to just being good manners.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

My favorite is The Millionaire Next Door. Even though my parents are frugal with their own money, they always told us kids to get high paying jobs and then buy big houses and expensive cars. They were setting us up to spend all our money instead of investing it. Fortunately, I read The Millionaire Next Door in college which opened my eyes to how wealth is actually built.

As I said before, I Will Teach You To Be Rich by Ramit Sethi. I don’t like Ramit’s new content very much, but this book is a gem (especially for people in their 20s). I still follow a lot of the advice in it. I also recommend his online courses if you’re willing to do the work. I picked up the negotiation strategy I mentioned above from one of his courses.

Finally, The Smartest Investment Book You’ll Ever Read by Dan Solin is a great book for anyone who wants to make money in the stock market.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

As noted in the expenses section, we donated $1,200 to various charities in 2023.

I used to donate more to a charity that did work throughout our state, but it no longer exists.

Now I’m searching for another organization to support.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

We don’t have kids yet so this is hard to answer.

If we pass away before they are adults, we will leave all of our money so their needs are fully funded through college graduation.

Otherwise, we will decide what to do as they grow up and we understand their worth-ethic.

Great Job! Very impressive… Your target net worth is too low! Even with your wife slowing down when you grow your family.

How confident do you feel you will be able to walk away at 40?

I understand the motivation if you have children, but I’m working in one of the international advisory firms and I can’t remember a single person walk away from their $500k/year jobs at 40. Early 50s is really the earliest I’ve seen. At some point I feel like they are working to give the money to their children, rather than for themselves. I’m getting ready to retire at 55; at 40 it wasn’t even on my radar.

My has very unstable compensation and no defined career path unlike advisory firms. People have good runs of 5 years at a time before their trading strategy stops working. Then they have to start over again. I won’t make $400k ten years from now. Once my good run is over, I’ll retire. I had a coworker who is 32 years old retire earlier this year, actually.

Retiring that young seems crazy to me. Use your earnings for security and helping others. Financial Samurai is going back to work! lol. I can retire now and am much older but won’t. come on? 32yo? Sheshh. lol

I manage people in their 30s. Some think their career is almost done. lol

Wait till the market gets crushed. It isn’t always upwards.

Excellent question. I think the author has some good intentions about retiring early and focussing on parenting, but even parenting has a limit on how much time it takes, how fulfilling it can be, and how long it lasts for before children leave home and need less. Whereas retiring at 40-ish leaves a huge amount of uncertainty in how much money one needs for themselves, their family, their charitable priorities, and just general risk management. Plus I can see the first class travel spending creep in the post – that sort of thing is hard to give up on and can make a high income harder to walk away from.

I’m pretty confident I will walk away by 40, but it depends on how much our investments grow by then.

My industry is very unstable and has no predictable career growth. People tend to have five years of high income when they have a good trading strategy. Then the strategy stops working and they need to start over. Many never get back to their peak earning years. As a result, the people who invested their high incomes often retire early. I have a former coworker who retired at 32 years old after a good run in his 20s. Many others retired in their 40s. Some others transition to small business ownership by buying an existing business from a retiring owner.

As a result, I doubt I’ll make $400k+ five years from now. My wife’s income will cover our expenses and give our investments more time to grow. It will be obvious when it is time for me to walk away from my industry. If retirement doesn’t work out, I can always try part-time software consulting.

You guys are about a decade ahead of moat peopke in terms of NW. congrats.

The biggest bill you have is your tax bill. High earning W-2 employees pay an excessive % of taxes in congrats to lower wage earners or high wage business owners. Do something to get that under control and do it aggressively.

I rarely hear anyone address that here.

I chose real estate to defray my high 1099 income. Do what you must but it is possible to get your realized tax rate into single digits , even with a $700-800k income.

I save $135-150k+ per year just by paying attention and putting a plan in place.

You guys are really on a good path here. Don’t give it away !

I’m very interested in what you pick up on here. I have high income W2 with effective tax rate approaching 40% and marginal tax rate more like 45%. But there is absolutely nothing that I know of that can be done. There is no avoidance for straight W2 income. You mention 1099 options, but pure-W2 earners don’t have those. I expect the author doesn’t have those either, like me. But if they exist, it would be great to hear of them!

You can purchase real estate or other depreciable/amortizable property that you leverage to maximize non-cash expenses like depreciation/amortization Careful though the rules are complex. Get a great accountant or lawyer.

Nothing that stops the initial W2 income tax

Basically you are creating a loss in your “business” that hits your personal total income, bringing down your taxable income. Your “business” could be a rental house that you over expense, most throw all their purchases against the rental house whether they are for the rental or not, increasing their write off and decreasing their taxable amount. Real Estate is just one example.

This is an interesting idea. I have consulted some financial professionals about lowering our taxable income, but there isn’t much more they can add for W2 employees. Real estate is interesting, but it feels like adding more work to our limited schedule. Nevertheless, I’ll look into it! Thanks!

And pardon typos

Being in your age range, I’m in awe at how fast you grew your income and net worth. Retirement in your 30s is totally reasonable, and with a high quality of life. It’s so important to have this impressionable moments early in life to get interested in high paying careers. You’ve got a good balanced life, enjoying and also giving back. Loved this line: There are also a lot of hobbies that look interesting and I want to volunteer in my community.

Look forward to reading your update when you retire!

Thank you for your kind words!

This was such a well written interview, with lots of really interesting aspects to it – thank you!

The “I’m still fairly young so I feel uncomfortable giving advice” humility was actually followed up with some of the absolute best career (through a finances lens) advice that anyone could give.

I saw some pretty wildly fluctuating incomes (via bonus) and I wonder how MI-402 feels about that part. My income is subject to wild fluctuations (my performance, company performance) as well, and I find that really impacts my approach because there’s a lot of risk management having to be layered in on top of the general principles. Related to that, I think it’s been basically 16 years since anyone has really seen extreme pain in the markets, yet I think everyone should be considering that risk more than they do. This can be income concerns (most people’s income and/or job security is tied to general economy success) and sequence of returns issues for investments already accumulated (retiring early and then seeing a major correction in the market would be a very bad experience).

Lifestyle creep is also very hard to predict. Perhaps the family that’s started will get a taste for those first class flights, the nice house, vacations etc. Having a strong saving ethos helps combat that but it’s still a factor. $8K/year on travel is peanuts these days (try taking a family on a Disney week) as another example.

Thanks again for such an interesting interview, wide ranging points, and great advice.

Thanks for the comment!

Myy unpredictable income sometimes makes me nervous, but it is a half-blessing. It is one reason why we live so far below our incomes. When my wife was in graduate school and we relied on my income, we decided we would only live on the salary portion. Bonuses mostly got invested with $1-2k used for a one-time splurge. Now that my wife is working, we decided we will live as if we make $200k pre-tax in a year. That feels like a reasonable amount that we can get back if one of us lost our job and the other got no bonus.

In regards to lifestyle creep, increased expenses for a family is my biggest worry. I hope we won’t have too much because we keep everything to the lifestyle of a family making $200k annually. We only flew first-class once so far and it was for a domestic flight. I enjoyed it, but my wife didn’t think it was worth the price. We both agree that we aren’t flying first-class when we are with kids because we don’t want them to get used to luxury. I doubt I’ll get to fly first-class again for 20 years until the kids are adults 🙂

Amazing income and discipline, ESPECIALLY at your ages. Congrats and keep it up! If you play with retirement calculators, it could shock you would your net worth could get to should you decide to keep working past 40. But there is also nothing wrong with deciding you have all you need. Do you have any ideas for an “encore career?” I can’t imagine you won’t want to work at all from age 40 to death. We need purpose.

Yes, I definitely have plans for an “encore career”. I like that term.

But it won’t be for making money. It will focus more on making a (small) positive impact in the world.

Congratulations on your success! You appear to be one of the people interviewed here who thanks their younger self for good financial decisions early in their working life. Enjoy your freedom to continue working if you chose … or doing something completely different.

Your mention of “Wealth Ratio” was interesting, and certainly a valuable metric. I didn’t know it had a name or was even a thing. But recently I discovered that our net worth slightly exceeds our lifetime W-2 earnings and was completely blown away as I mention in my interview coming up next month.

I’m looking forward to reading your interview!

Thank you for sharing!

I like your comment on automatic investing and how it’s helped you build wealth thus far. I would have approximately a million more if I’d done this when I started earning payroll income. Once I started some years later automatic investing via payroll and ACH transfers was my go to. Along with consistent tithing and abundant charitable giving and investing a significant portion of our ivestible funds in no-load low-expense stock index mutual funds of the S&P 500 and Total U.S. Stock Market variety, this has helped enrich our lives and put us in the position we’re in.

Congrats to both you and your wife on achieving such a high NW in your early 30s!

My husband and I mirror your stories quite a bit, in terms of high NW in early 30s, $5M NW FIRE target (I’m the management consultant wife and my husband is the SAHD) – only we’re a few years ahead of you.

We’re now in our late 30s with 2 kids below 5, and recently retired last year and spent some time traveling with our kids.

It is absolutely doable and it’s been a blast so far! Not missing work at all and NW has actually gone up since retirement even after spending more than we normally do pre-FIRe.