Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in March.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I am 62 and my much younger wife is 55. Neither of us feel like this age!

We have been married for 20 years. It is both our second marriages.

We come from different backgrounds but are very happy together. My wife’s family had little money and she worked several jobs through university and landed a well-paid professional job.

My family owned a medium-sized farm. We were never wealthy but had enough in good years for holidays abroad when few of our peers were doing so.

Do you have kids/family (if so, how old are they)?

I have 2 children, both in their 20s and both have their own lives and careers away from home.

They have turned out as lovely talented individuals and we are proud of them. No grandchildren yet and not imminent either.

My wife doesn’t have children but is very close with mine.

What area of the country do you live in (and urban or rural)?

We live in a rural area near to a large city in the United Kingdom.

What is your current net worth?

$6.4 million. Mr. ESI has asked for all figures to be in USD so I am multiplying our British pounds by 1.35 in each instance.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

- Cash $670k

- Pensions (equivalent to 401k) $2.5M

- Tax-free investments (ISA in UK, Roth IRA in US) $750k

- Taxable investments $380k

- Home $1M

- Rental properties (1 house, 4 apartments) $1.1M

No debt apart from a credit card paid in full monthly.

My business was sold for $3 million after all taxes 3 years ago and those funds are now amalgamated into the above numbers. I am still involved in the business as a remote director and advisor but do not go to the office and am rarely called upon.

I know a few people who have sold businesses for 10-20 times as much, and I admire them for it. I was never on that level, but I am content with what I have achieved and I realise it puts us in the top 1% in terms of net worth in the UK.

We have therefore come a long way financially. I also know plenty small business owners who are trapped and unable to exit, as the business cannot run without them.

EARN

What is your job?

I owned a wholesale food supply company which I started from scratch 30 years ago with one outlet, building up to seven small outlets over the next ten years. Some were then sold or closed and after some amalgamation, the business currently runs two distribution centres with 55 employees.

We concentrate on the fresh produce industry from growing crops to delivering seasonal produce to the retail and catering trade. We also own a farm shop.

I have always been the sole director which was good in some ways. There was no one to answer to or disagree with and I had seen other partnerships go pear shaped (pardon the pun), which put me off having a business partner.

It also meant me making all the strategic decisions on my own, although I had a small network of friends in business who would advise.

I started off doing all the jobs from cleaning to driving the vans and tractors. It can be tricky to get out of the engine room and onto the bridge when you are running a small business.

As time went on and the business grew I became office-based, running different outlets each with their own managers. We cover a large area and offer a responsive service with rapid deliveries on a local basis unlike the large food supply companies who deliver imported food from huge warehouses using bigger articulated lorries.

What is your annual income?

$225k total in 2026 mainly from pension, investments and rentals.

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

Growing up on a farm we all mucked in to help at lambing, hay making and other jobs from a young age, not usually paid as such but a healthy and happy childhood. Once I could drive a tractor on our roads (16 years old in UK), I started getting paid minimum wage and was always keen to work as many hours as I could.

At 21 I graduated from agricultural college and, after travelling the world for a year, worked the home farm again for a few more years. My parents sold the farm for development and I moved to a nearby city and worked in farm management and the fresh produce trade for a large company.

My salary was a paltry $15k per annum 35 years ago for working 50-60 hours per week. However, I learned a lot at someone else’s expense.

I always knew I would end up working for myself, possibly due to my farming background, and sure enough once I had learned how a successful business worked I duly left and started out on my own.

When you have your own business, it is often better to draw minimal salary and utilize dividends and pension contributions for tax efficiency.

My salary was probably even less then as I worked twice the hours building up the company. I remember on Saturday afternoons my friends would be at a football (soccer) match or playing golf whilst I was out lifting potatoes or delivering orders in a van.

At some stages I would start work at 3am and work until 10pm. Not an advert for good planning but exciting and all-consuming at the time.

As the business grew I was able to draw a larger combination of salary and dividends. My package grew from $15k initially in the mid nineties to $60k in 2000.

It stagnated at that level for years as I left as much money in the Company for expansion as possible. There wasn’t much time free for spending money either. It then increased to around $100K from 2010 to 2015.

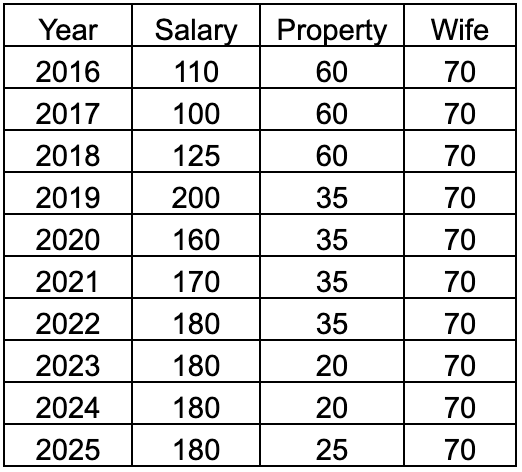

Thereafter our incomes including profits from property, which fluctuated as repairs and work was needed, were as follows. Gross salaries and net property profits in $ past 10 years:

I was happy to borrow money from banks to expand by acquiring other similar small businesses and also expanding organically as we went along. At the same time my wife and I started another two retail businesses which we quickly sold on as they became too much to handle.

I admire retailers who have to contend with rampant shoplifting and abuse in some areas, it was not for us.

I also somehow found time to research several other opportunities in the sporting leisure sector but was beaten to it each time, probably because I had my hands full already.

My family helped me out financially in our younger days with some loans, on which we paid commercial rates of interest, and I will always be grateful for this help. It was essentially a form of advance inheritance.

My parents were always interested and supportive of our activities and a welcome source of encouragement in what can be a lonely lifestyle.

What tips do you have for others who want to grow their career-related income?

Start your own business. This is the best way to attain wealth if you choose the right niche and work hard at it but you have to commit to it 100%.

It really takes over your whole life.

As you hopefully grow the business it becomes important that the business can run without you, otherwise you become the business and it is not worth nearly as much money when you come to exit. Set up systems and processes so the Company almost runs itself.

Everyone should know what is expected of them and who is doing what. Employ people who are smarter than you and can make the big strategy calls.

What made you sell?

When I reached my mid-fifties I realized I wasn’t enjoying it much anymore. My children were not interested in the business and I felt I was on a treadmill.

When we reach our fifties we all have friends or acquaintances who pass away suddenly or become too ill to enjoy retirement and this made me think hard about my life’s priorities. My wife had been offered and accepted a package to retire early from her professional role and was loving her new life.

I now had people who were capable of running the show if I just allowed them the space. I then started looking for an exit.

This can prove impossible for some business owners who are effectively prisoners of their own small business with no-one to take over and no value to a buyer because the owner is an essential part of the business. I spoke with some business sales agents who promised attractive sums from fictional buyers and wanted a large fee for introductions.

I avoided this trap but know others who were led down the garden path and ended up with no buyers. I lucked into two simultaneous options which allowed a decent multiple of earnings so I took it, ending up with $3M after the large professional fees and endless due diligence processes.

I also had an absolute guarantee there would be no redundancies or closures and the managers and supervisors would all be retained, which was important to me as they had helped create the value. I was kept on for a handover period and used it to make sure the promises were kept, in fact I managed to get all salaries increased and profits also grew higher than ever before.

Maybe I should have held on a while!

What’s your work-life balance look like?

Originally, it was all work. In my twenties I was inspired to grow and expand, but I still managed to fit in family and friends somehow.

$As time went on, and especially over the past ten years, I stepped further back and allowed my senior team to take up the heavy lifting. Now, post-sale, I rarely have to work and my time is my own.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

When we married and moved home 12 years ago we were able to keep our original home and rent it out. I also invested in a block of 4 apartments in a large city.

These were all mortgaged but when I sold the business I was able to pay all my loans off. Now the rental incomes provide a nice diversified income.

I use a management company to run them for me as I can no longer be bothered with call outs for leaking roofs or broken boilers. I still have to pay for them though!

The properties were a real stretch financially but we are so glad to have them now for a diversified income stream.

In the early days, I taught start-up businesses the basics for a local enterprise company, the pay was surprisingly good but it became repetitive and less challenging.

SAVE

What is your annual spending?

Same answer as annual income, we draw around $225k from salary, investments and rentals and try to spend it all. We travel a lot and enjoy business class travel and nice hotels and experiences.

We arrived at this figure by taking 5% annually from our pensions and ISAs in addition to our rental income, topped up if required from our cash and taxable investments. This will be reviewed at least annually and can be reduced or increased depending on markets.

At 5% we realise we are deliberately reducing our capital / net worth as we feel £6-7M is way too much to leave as inheritance which, incidentally is taxed at 40%. My IFA commented that we are effectively getting 40% discount on everything we buy…..

What are the main categories (expenses) this spending breaks into?

Our budget for this year:

- Food: 18000

- Cars maintenance, fuel, insurance: 10000

- Vacations: 82000

- Hobbies: 5000

- Clothes: 2000

- Eating out: 5000

- Home improvements: 45000

- Rates, insurance: 5000

- Electricity, Phones, internet, dogs: 5000

- Income tax: 30000

- Gym, classes, Pampering: 8000

- Gifts: 10000

Total: $225000

Do you have a budget? If so, how do you implement it?

I consult annually with our financial advisor as to how much we can afford to spend each year while leaving a safety buffer and allowing for a sensible inheritance for the kids. This figure is currently $225k.

I report this back to my wife who is happy for me to work out our finances. We log all our spending together and can cut back or increase in an effort to come out around the number.

We could fairly easily halve this spending level which is much higher than most people we know. We never spent anywhere near this level when we were younger.

We have worked hard for it and intend to enjoy it.

I ran endless scenarios and variations on how much we could spend through AI much to our advisor’s disapproval! His numbers came out lower most times so we go with his to be safe.

You will see in the table above we spend a large percentage of our budget on holidays and I am surprised how low the vacation spend is for others in this series. We travel mostly business class and stay in nice hotels and do nice cruises but there are people on these holidays in much more expensive rooms / cabins so it is all relative.

We travel somewhere most months of the year, even if it is a local weekend away. Home improvements are high as well as the house we bought needed modernization.

This will slow right back after this year, we hope.

What percentage of your gross income do you save and how has that changed over time?

In the early days of the business, it was zero; we had no spare money to save. In fact, we were highly leveraged.

I had loans from family, loans from banks, car, tractor, and van loans, and mortgages. As the business finally started to make more profits, I saved perhaps 20-30% of my salary into a pension through the Company.

This was a tax-efficient way to set money aside for our future. As mentioned earlier, the Company itself was also my retirement fund of sorts as it had a value building up gradually.

What’s your best tip for saving (accumulating) money?

Work hard but smart, I didn’t always manage this, spending too much time at the coal face rather than steering the business forward. Live and breathe your business.

Network like crazy, the more contacts the better. I joined Rotary and other business networks and went to lots of banking and accountants’ dinners, golf days etc.

Good fun and you always learn from others when you hear their business stories.

Taking money out of a business can be expensive tax wise (almost 50% after all taxes) so it is often better to leave it in the business to accumulate or use it to expand. Then when you come to sell, it is your money, and you can get Entrepreneurs’ Relief for part of it in the UK.

What’s your best tip for spending less money?

Always shop around for the best deal, personally and business-wise. Sleep on a major purchase for a few days, quite often you decide you didn’t need it after all.

Walking the dogs, climbing hills, playing sports are healthy and cheap or free ways to spend time. Stay out of bars and designer shops!

I have just ordered a new car for the first time ever, we always bought decent cars second-hand and ran them for years.

What is your favorite thing to spend money on/your secret splurge?

Holidays, both long and short haul. We can afford quality travel now, business class, not First, but this was not always the case.

When I travelled the world after college we would sleep in cars, tents or youth hostels and we had little money and had to find work to pay for the next meal or flight. Early family holidays were budget affairs but great fun as it was all we knew.

We have already been to all 5 (7?) continents and intend to carry on seeing the world while we are relatively young and fit.

INVEST

What is your investment philosophy/plan?

Hold a balanced portfolio across multiple regions, assets and companies, keeping a sensible portion in bonds and safer assets. I used to dabble in individual shares but found the few winners were cancelled out by the losers.

I missed the Apple bandwagon sadly. Now it is about balanced risk exposure with a large cash buffer to wait out any major market corrections without having to sell at depressed prices.

I feel it is worth employing an IFA advisor to get this right as it is easy to have a poorly positioned investment portfolio which you have worked your whole life to accumulate and which could suffer a large hit without any notice when the next financial crisis comes, which it surely will.

I enjoy reading about finance and investments and how people spend and save their money. I have steered clear of Bitcoin and have rarely gambled on anything apart from the odd game of Blackjack at cruise ship casinos.

What has been your best investment?

Starting my own business and building it constantly over many years. Some acquisitions were great value for us both in money terms and from the people they brought into our group.

These acquisitions were always high risk. We were basically buying a list of customers who could choose to leave us on the first day.

Time spent learning about investing and business is always a good investment.

What has been your worst investment?

Some individual shares tipped by friends, newspapers, online etc. a couple went to zero. A couple of our business acquisitions turned out to be worthless or loss making, mainly down to the individuals who ran them.

All learning experiences!

What’s been your overall return?

12%. This is the compounded return on what I started with to what our net worth is now and is the nearest I can come up with overall.

On the stock markets probably half that.

How often do you monitor/review your portfolio?

Twice a week, too much I know! This will settle back in time as I am still in the early stages of budgeting as we move from accumulation to spending sustainably from our investments.

My financial advisor helps us with which investments to sell and when within our pensions, and I will mirror his advice myself in our other investments. This alone is worth his fee.

NET WORTH

How did you accumulate your net worth?

I received an inheritance of $50k from a grandparent when I was 21. I stuck it all in the stock market at the time, playing about with individual shares with input from my father, while keeping most in safer funds.

I don’t think it grew by much. I then used this fund 5 years later as part of the initial funding to start my business.

For this reason, I am keen to pass a sensible sum to my kids when they can make use of it rather than when they are maybe 50-65 and it becomes a nice to have bonus.

Most of our net worth was accumulated by a long slow expansion of my initial business.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

Earn. Although you do need all three.

In my case “earn” was the capital value building up in my business which was saved and reinvested in the business. This became the engine which produced ongoing profits and income so it comes tops.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

My business never made a loss in 30 years, but the profits were very low for the first 5-8 years, so we had no major road bumps apart from things like flooded premises, vehicle accidents and loss of major customers and contracts which are part of business life in my experience. The early low-earning years were overcome by sheer enthusiasm and energy, dealing with everything that came along and always driving forward regardless.

We have employed hundreds of people over the years and have had all sorts of characters. It can be challenging and stressful dealing with the many issues and problems which staff bring to you.

I have encountered every issue imaginable from affairs to drinking and gambling problems, stealing, bullying and worse. I came to realise that I had to pass HR to the specialists but being the main boss meant it was me that people came to with their problems.

We also have a great core of loyal, decent hard-working people who have been with the business a long time and see each other almost as family. We have had loads of fun and laughs along the way as well.

What are you currently doing to maintain/grow your net worth?

Maintaining a broad portfolio of investments and income streams and regularly monitoring them against our spending. We run a risk exposure of 6 out of 10 currently which we are happy with given our cash buffer and property income.

I have always enjoyed monitoring this and ESI money is a great help to me in this regard.

Do you have a target net worth you are trying to attain?

We intend to intentionally spend down our net worth and so it is unlikely to grow much unless markets continue to race ahead as they have in recent years. We will hopefully stay at around $4-6M for the next ten years.

How old were you when you made your first million and have you had any significant behavior shifts since then?

I think I would have been in my late forties but valuing a business is a subjective, dark art and comes down to what someone will pay you for it. I was lucky that two competing suitors helped increase my exit price.

Excluding the business my first million would not have come until I was in my fifties so it was a long slow grind eventually becoming a compounding upwards curve.

Behaviour-wise, I have become more focused on the big picture, exit strategy and retirement planning. In the early days I would panic about setbacks, now I realise that they all pass.

In very stressful work meetings or scenarios, I would focus on the horizon figuratively speaking and knowing that the issue would pass.

What personal habits and/or traits have you developed that have made you successful at growing your net worth?

The ability to work hard and take risks. I have had high levels of debt at various times and it could have all gone badly wrong.

The business always seemed to go up a notch just when it was needed, hopefully through good planning but maybe dumb luck!

Being off sick was not an option at times; there was no one else to do the work so you just got on with it. Nowadays, it seems easy to get signed off work with stress or anxiety when a days work and the company of those around you would be the best remedy.

I am straying into controversial territory here.

What money mistakes have you made along the way that others can learn from?

Looking back I sometimes wish I had been even more aggressive in expanding and growing my businesses but I am happy overall with how things have turned out.

My investment mix was at times a random assortment of shares and funds which could have made a higher return with professional input. I have mostly avoided paying a fixed percentage to advisors, but do feel it is worth paying for good advice.

We use the Vanguard platform mainly now, having been with more expensive and less user-friendly firms before.

What advice do you have for ESI Money readers on how to become wealthy?

If you are able, and have the drive, determination and ideas then start a business. If you are young you will have time to recover if it doesn’t work out.

Business failure can be wrongly frowned upon in the UK, unlike the USA.

Share your success with your employees, financially and verbally. The better they do the better the business does.

Live below your means. I see new business owners suddenly appear at work in a fancy new car or moving to a more expensive neighbourhood long before they can afford it.

All to project the image of success as they see it. As someone said, When the tide goes out you see who was swimming without any trunks!

FUTURE

What are your plans for the future regarding lifestyle?

We have scaled our planned spending to be highest for the next 10-15 years when we are hopefully still fit and able to enjoy it. We are fortunate to be able to afford a fairly affluent lifestyle but we are not flashy with it. I could buy a Bentley but I would feel too showy.

I play golf but have never once hired a caddy (maybe that’s why my scores are so poor!).

This spending level will then taper off in later years as we slow down and prefer to stay at home more.

What are your retirement plans?

Both retired already, wife had her own career and I have only just exited my business. I was lucky to have a gradual exit, working part time for many years.

Financially we will consciously spend our budget annually whilst sharing our good fortune with others. I do some free consulting and intend to do voluntary work but have no plans to work a job or start another business unless as a silent investor.

We both keep fit with cycling, gym, walking our dogs and golf. Our elderly parents need some looking after. We read a lot and do puzzles to keep our brains sharp.

We enjoy going to concerts, nice meals out and taking things easy at last!

Are there any issues in retirement that concern you? If so, how are you planning to address them?

Possible boredom although this has not happened yet. I have a list of activities and goals which I have barely touched yet.

Health is so important, we have lost friends and acquaintances far too young so we do what we can to stay healthy and enjoy life. Seeing friends, children and parents are all very important to us.

Running out of money is unlikely but we have the option to sell one or more investment properties to give a boost if required.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

Finance has interested me since leaving school. It has been a long learning process with mistakes along the way.

There is a wealth of information out there which I devour daily. I guess it clicked in my late forties when things came into balance with less debt and a better spread of assets.

Having a business, investments and rental properties gives you options when times are turbulent.

Who inspired you to excel in life? Who are your heroes?

I read the biography of Sir James Goldsmith in my teens and have been fascinated ever since by people who have built great wealth by taking huge risks.

I have read dozens of business biographies so the usual names would be heroes but also less well known business people locally who are very successful and fly under the radar, real “millionaire next door” types.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

- Rich Dad Poor Dad

- Tycoon, the life of James Goldsmith

- Made in America, the life of Sam Walton, Walmart.

Very different books about very different people but I found them all helpful and inspiring. There are so many ways to become successful and it is not all about money.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

Through the business we donate to charity, support food banks, support golf and football charity days and we sponsor local teams and events. A win win situation.

Personally we tip well and support local causes. If there is a charity auction I will try to buy something or donate.

I do free consulting for small businesses and intend to do more voluntary work now that I have retired. As we settle into our budgets we will give more financially as well.

It is important to give back. One never knows when we may need help from the various health charities and it is eye-opening to hear how much they need every week to operate.

I would estimate we give around 5% at present and we hope to increase this as we settle into our budget.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

A reasonable but not too large inheritance, perhaps $1-2M total, is what we predict but we will help children and grandchildren financially before we pass with property purchases or similar uses so we can see and share the benefits.

We would rather see the benefits of a living inheritance when it can be used to greater benefit but do not intend to just hand out money for lifestyle enhancement as this can induce laziness. A tricky balance to work on!

Thank you for your writing and for your devotion to maintain your business with the ups and downs that come every day and way. It was an interesting reading and provided a lot to help with understanding your rise in the business market. Wishing you good fortune in your retirement life.

Thank you, we are looking forward to our new life, the old cliche applies, I don’t know how I found time to work!

Thanks for sharing and congratulations on your success. Your point regarding determining the right amount to leave behind vs. spending, gifting, etc., while alive is such an important one. On one hand you can spend “exorbitantly” and whittle away at a lifetime of accumulation, but for most on this forum that goes against the grain of being a lifetime saver / accumulator. On the other if one continues with historic somewhat thrifty if not frugal ways, then the assets will continue growing over 30 years of retirement hitting $10M+ (in your case I expect) which is a fortune to leave and be taxed away.

We are at a similar wealth level and age as you and yours, with two sons in their 20s. We are actively considering our strategy for spending and gifting while alive, with the goal of leaving behind a reasonable inheritance while also enjoying our accumulation now and getting joy from helping our kids. Like you we don’t want to leave a fortune and risk taxation of it. And we can’t risk overextending and falling short, and we don’t know whether / when our sons might have kids of their own which can change everything in our calculus.

It sounds like you have hit on a formula that will work for you and I appreciate your sharing these thoughts for us to consider as we work through and develop our own strategy.

How interesting, yes it’s a tricky one. The other distinct possibility is residential care costs in later life which are $2,500 a week here in the UK for those with funds. This could make a huge difference to our calculations. I am encouraged to read that you think our assets will grow, which they have already actually and we will monitor this closely. Good luck to you

How interesting, yes it’s a tricky one. The other distinct possibility is residential care costs in later life which are $2,500 a week here in the UK for those with funds. This could make a huge difference to our calculations. I am encouraged to read that you think our assets will grow, which they have already actually and we will monitor this closely. Good luck to you.

Thank you for sharing! You give me hope. I’m 52 and hovering just under my first million. I sure hope the next million comes a bit easier/quicker. All the best to you in your retirement!

Thanks May, I agree with the accepted wisdom that the first $M is the hardest!

What a great interview! And best of success in a rich retirement.

Thank you, start of hopefully a long road.

Thank you for sharing your story! I liked your comment, “Start your own business. This is the best way to attain wealth if you choose the right niche and work hard at it but you have to commit to it 100%.” I am a volunteer administrative assistant for a business-related ministry offered by my local church fellowship. Though my business endeavors worked out to only be side gigs to my career (in terms of income-earning power), our ministry shares the same thing you stated with parishioners to help them see they often have giftings and abilities within that can aid them in their quest to care for their families (natural and spiritual) and to be in a position to be generous in helping meet other people’s needs. At the least, they would know after some time that this was not to be the primary method the Lord would use to grow wealth through their work endeavors and they would then be able to be satisfied with a career of working for others and a life of managing the proceeds well so that they could eliminate financial bondage and build wealth and generational wealth for their loved ones and increase giving to endeavors for which they have a passion and burden, like their local church and other worthwhile ministries and charities.

Thank you, I also offer free mentoring to small businesses to give back and most of the time we talk about mindset and choices. Its not for everyone but worth a try to see.