Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in March.

It’s a long one (which I love!) so I’ll be breaking it into two separate posts.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

This year, I will be 66 and my wife will be 63.

We’ll be married for 38 years this year.

Do you have kids/family (if so, how old are they)?

No kids.

What area of the country do you live in (and urban or rural)?

We live in a suburb/bedroom community of Honolulu, Hawaii

What is your current net worth?

Approximately $6,300,000.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

- Equities, fixed income, cash, tangible assets (cars, home furnishings, collectibles, etc.): $4,500,000

- Real estate/home: 1,800,000

- Debt: credit cards – approximately $4000/month which is paid off in full. No other debt.

EARN

What is your job?

I am a per-diem registered nurse/safety officer and do a mix of patient care activities in addition to keeping our ambulatory surgery center (ASC) compliant with OSHA, state, EPA, and AAAHC regulations. I am currently transitioning out of the safety officer role as I head into permanent retirement.

My wife is a registered nurse and works full-time as a nurse care manager in a 160-bed hospital. She will be cutting back to part-time (about 27 hours/week) starting in 2026.

What is your annual income?

Approximately $205,000 adjusted gross income (married filing jointly) for 2025.

This includes investment income.

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

Myself:

- 1972 – 12 years old delivering papers – $200/year. Salary grew significantly after getting medical training, going to college for my degree (Bachelors of Science in Nursing), obtaining other job-related certifications.

- Nursing offers a lot of on-call opportunities and work is abundant. At any given time, I would have been working up to 3 jobs related to nursing: teaching + moonlighting in an on-call position + working my full-time job.

- If you work nights, weekends, and/or holidays, there are pay differentials that increase your hourly rate. I was also running a small side business teaching basic life support, advanced cardiac life support, and similar training.

- 2017 – 57 years old – hospital supervisor – $120,000+/year on retirement

- Present – 65 years old – $45,000/year (salary only – this does not include investment income)

My wife:

- 1979 – 16 years old working in a small grocery store – $200/year. My wife’s career trajectory sort of followed mine in terms of education – she and I graduated together from the same nursing program; however, she pretty much stuck with the same employer for over 35 years while I jumped around doing different jobs in nursing.

- She currently outearns me and has a little more saved up in her 403b/Roth so she could have retired from full-time employment back in 2017 as well.

- Present – 62 years old – $160,000/year (salary only – this does not include investment income)

What tips do you have for others who want to grow their career-related income?

Keep on learning new things. I took lots of nursing-related courses in areas of nursing that interested me.

This made it easier to transition to more advanced practice areas and admin positions which would sometimes pay more. Along the way, you make lots of friends and new contacts – all of which come in useful for future advancement.

I can name at least 4 positions right off the top of my head where I was hired because the employers remembered me from a class I taught or from a former job.

Work hard and do your best. That whole thing about giving more than 100% is very true.

For the most part, employers do notice hard work and consistent quality. While I’m on it, being a nice person to work with also makes a big difference – nobody wants to work with a jerk so treat others like you’d want to be treated in return.

If you’re feeling burned out and want to try something else, keep your full-time job and start looking for other opportunities. Back when I was just starting out in nursing, I worked a full-time job as an airport nurse, a per-diem job as a flight nurse for an air ambulance company, and taught on the side.

Working 3 12 hour shifts a week (36 hours/week which is considered full-time in some healthcare systems) made this possible.

While jumping around from job to job doesn’t work for everyone, it was great for me. I rarely got bored and if I did, there was always a different job in the field to check out.

What’s your work-life balance look like?

It looks really great for me. I work only when I feel like it.

There are no more missed holidays, no weekend work, no more night shifts, no more mandatory call. I love working at our small ambulatory surgery center – I get the right mix of putting my years of patient care skills to use, socialization with staff and patients, and challenging projects to keep me engaged.

It’s pretty much my ideal retirement job. I get paid significantly less than what I used to make in the hospital as a hospital supervisor, but this job is much less stressful.

I think of it as paid volunteer work. Having the extra time is nice.

I’m currently fixing up the house (our 4th and final renovation), culling through my collectibles (thinking of selling some since they have gone up in value), decluttering as I prep for downsizing, doing financial planning for retirement, and a whole lot of other stuff. There’s extra time to spend with other retired work friends and do more travel.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

Currently, I am looking at other income streams for the day when I decide to hang up my stethoscope for good. So far, none of these are producing anything (with the exception of the last item) as they are still in development:

- Nursing-related blog/YouTube channel – passing on my years of knowledge and experience to the next generation of nurses (tricks of the trade, nursing skills, how to organize yourself for your shift, preventing your patients from dying – ICU focused, dealing with troublesome patients/staff/administrative types, etc.)

- Lifestyle-related blog/YouTube channel – passing my knowledge and experience in how to survive and prosper in Hawaii – one of the most expensive states to live in.

- Writing a book – reflections on growing up in Hawaii and doing what I’ve been doing over the past 40 years

- Going back to school for another degree and getting back into teaching – history appeals to me.

- Moving my investments around for more dividend production – this has increased my investment income from about $30,000 to about $50,000/year

SAVE

What is your annual spending?

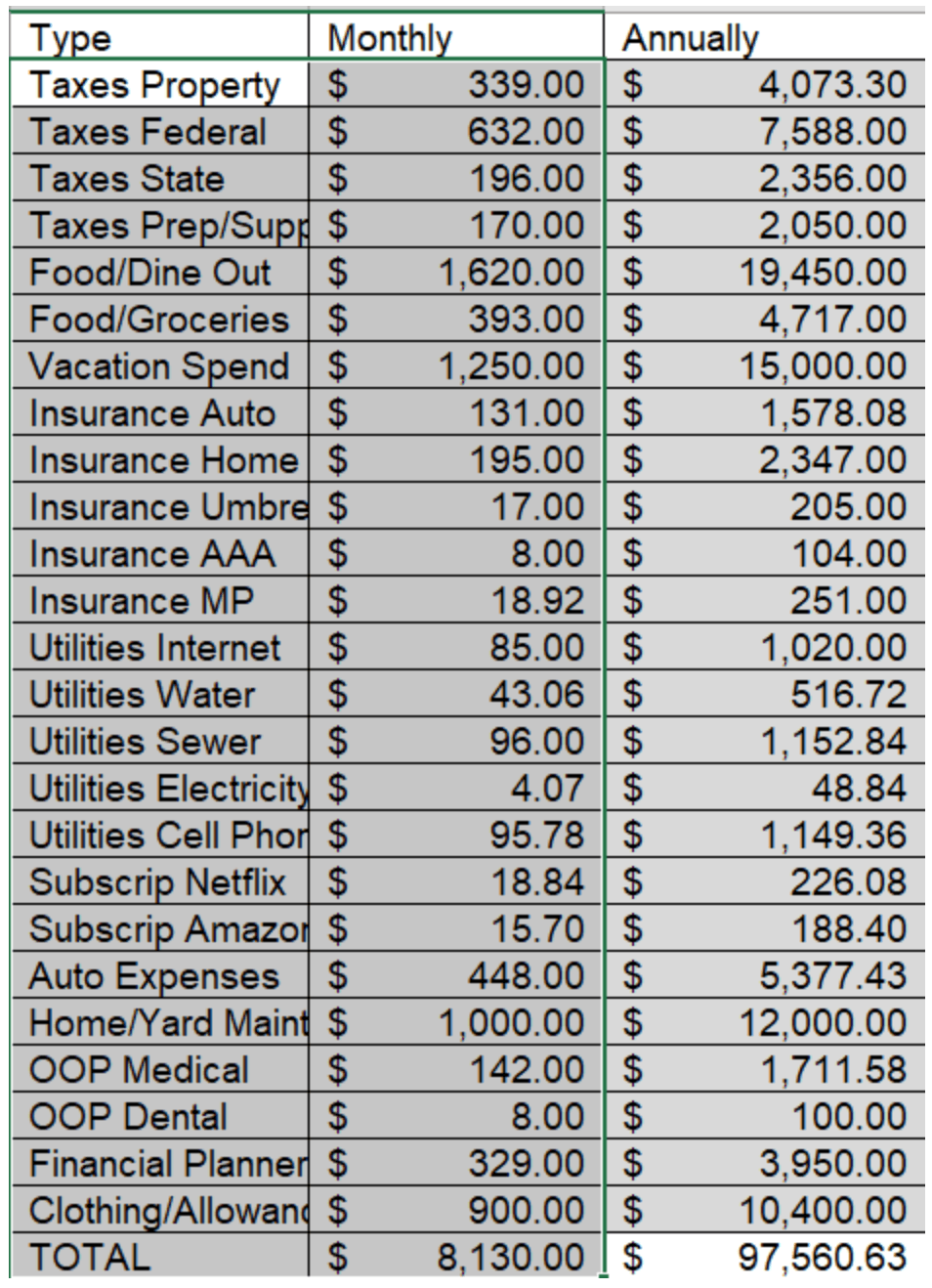

Approximately $108,800 in 2025 which is more than usual (took 4 trips, bought some badly needed furniture, did some needed home repairs, changed out some appliances).

What are the main categories (expenses) this spending breaks into?

This is from an Excel spreadsheet I created to figure out how much we were spending. We use Quicken for our bookkeeping but I like this Excel spreadsheet as I can break categories down simply (Quicken throws in sub-categories which can make your balance sheet look messier and more complicated than it has to be).

Our monthly expenses vary depending on if we are traveling, paying our insurance (February is when we pay our homeowners, hurricane, auto, and umbrella. March is when we pay our taxes.

We also pay estimated taxes so what you see are average monthly amounts.

Do you have a budget? If so, how do you implement it?

I use the budget set-up tool in Quicken and tweak it as the year progresses. To get a quick 1 page view of our net worth, I use the spreadsheet above.

The spreadsheet is a little more elaborate than what you see. I have a separate spreadsheet page for income and investments and another spreadsheet page for income forecasting that includes average cost of living, average investment income, and inflation.

I take care of all the financials as far as bookkeeping and paying bills, but I have been vigorously prodding my wife to take a more active interest in her investments. She is getting better about checking her various retirement accounts and investment portfolio.

She was doing the bookkeeping (with the exception of portfolio tracking, which I did – this was during a particularly stressful period in my job history.) for a few years but I ended up taking it back and pretty much do it all now. My wife has access to all accounts in Quicken so she can check things for herself when she likes.

As far as accounts and budgeting, when we first got married, we had combined all our savings and income into one joint account. As time went on, we realized it made more sense to separate most of our accounts.

Currently, my wife has a 403b and Roth (through work), Roth IRA, brokerage account, local bank money market savings, and a local bank interest checking account. I have a Roth (through work), a traditional IRA where all my past employer retirement accounts are rolled over into, Roth IRA (rolled over from old employer Roth accounts), brokerage account, local bank money market savings, and a local bank interest checking account.

We only have 1 joint account, which is used for paying off bills and joint household-related spending. Our paychecks are directly deposited to this account and we use electronic bill payment/transfers to move money between accounts.

This has proven to be a real time saver.

What percentage of your gross income do you save and how has that changed over time?

We save approximately 30% of our income. We both contribute 20% to our workplace 403bs and Roths.

The other 10% is what is left over after everything is paid off monthly. Obviously, when we first started out, we weren’t able to put away 20% of our paychecks – believe I started out with 5% but gradually increased it to 20% in addition to saving whatever was left over after bills each month.

I don’t include investment income which comes out to about 10% annualized – all investment income was reinvested initially but we no longer do this – all dividends and interest now go to cash (this will get switched around if the stock market tanks).

We are now starting to pull occasional small amounts out of our brokerage accounts to replenish our local accounts. It’s kind of practice for when we start pulling out money regularly in full retirement.

What’s your best tip for saving (accumulating) money?

- Live frugally (but also enjoy life within your financial constraints)

- Start saving early

- Save as much as possible

- Learn as much as you can about financial management (taxes, investing, portfolio management/diversification, real estate, etc.)

- Get expert advice as your net worth grows (CPA, CFP or similar)

- Live within your means

What’s your best tip for spending less money?

- Develop a budget and try to stick with it

- Having said that, you will never be able to stay within your budget categories 100% of the time. There will always be outliers and emergencies that will have you overspending in some areas. That’s life. Don’t beat yourself up about it – just transfer money from another pot and adjust your budget for next year.

- Buy good quality stuff that will last a long time and has a good history of reliability. We never go for the luxury stuff unless we know for a fact (based on lots of research and hands-on trial if possible) that it will last and rarely break down.

- Learn how to take good care of yourself and your stuff. I can’t begin to tell you how many times that has made a difference. I try to stay healthy as much as possible. Yeah, I’ve got high blood pressure and I’m overweight, but I am doing something about it and so far, I haven’t had a stroke or a life-changing medical event. I’ve got lots of tools and they are good quality tools because I do a lot of work around the house instead of having someone else do it.

- Avoid divorce. Be faithful and honest to your significant other and treat him/her with courtesy, kindness, and respect. Try to work things out if there are conflicts. You’ll know when the relationship is broken – try to repair it if you can.

What is your favorite thing to spend money on/your secret splurge?

Ever since childhood, I’ve liked collecting diecast emergency vehicles. Working in EMS and fire stations as a young adult has deepened that appreciation.

To that end, I have an extensive collection of diecast emergency vehicles from around the world. Some items I picked up locally.

Others I have brought back in my luggage from other countries. Incidentally, there is a niche market for these items and some items in my collection that I picked up cheap are now worth 10 times what I paid for them.

I also have a small coin collection.

INVEST

What is your investment philosophy/plan?

- Buy low, sell high

- Diversify your portfolio

- Know what you’re investing in – like what does this company produce and is it worth it?

- Be greedy enough, but not too much (The take-away here is keep an eye on things and know when to get out of an investment).

- Watch out for hidden costs/fees and balance them out with fund performance

What has been your best investment?

- Costco

- Baxter

- Nvidia

- JP Morgan

- Lockheed Martin

- IBM

- Caterpillar

- Tesla (I sold this off a few years ago – took my profits and ran)

- Vanguard Total Stock Market ETF (VTI)

What has been your worst investment?

- Boeing – started out good in 2017, then the bottom fell out in 2018.

- Interspeed – this stock gifted to me by my father basically became worthless in less than 5 years – a victim of the 1980s tech bubble.

What’s been your overall return?

About a 10% annualized return across all accounts.

How often do you monitor/review your portfolio?

Every day except for weekends and holidays – about a few hours in the AM.

NET WORTH

How did you accumulate your net worth?

I inherited very little when my father died. Our family is not considered to be wealthy. Strangely enough, after 17 years, I still have all of the money I inherited form my father though it is invested.

I pretty much made my fortune by working hard and holding down 2-3 jobs when I was younger.

I was really good about saving and when tax-sheltered annuities /401ks/403bs were introduced in the 1980’s, I made sure to contribute as much as possible. I did a lot of our home improvements myself.

As mentioned above, we are both very frugal. I married a lady from a lower-middle-class family who had their share of financial difficulties. She is just as frugal as I am and is also a good saver.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

All of it – all aspects of ESI. As nurses, we typically are not paid well – stevedores and doctors make significantly more than we do per hour.

But I started working early on and volunteered to do overtime many times/week, I did more call, I worked evenings/nights, I worked weekends, and I worked in high-demand specialty areas. Nearly all hospitals pay differentials for working weekends, holidays, evenings/nights, on-call, or working in high-demand specialties (ER, ICU, periop).

All the differentials add more dollars/hour to your base pay rate. So as far as earnings go, earning potential is high for nurses if you work more or work the undesirable shifts.

Saving cannot be underestimated. The more you save and invest in income-producing investments, the more money you end up with.

Investing should be a mandatory part of all high school curricula. My father was a broker for Dean Witter when I was growing up so I kind of knew the rudiments of how the stock market worked by looking over his shoulder and reading some of his financial magazines (Fortune, Business Week, WSJ, Barrons, etc.).

However, I learned how to buy and sell stocks on my own by reading financial books and magazines like Kiplinger’s and Money that were geared to the beginning investor. Also, when I had a period of burnout 20 years ago and was seriously thinking about leaving nursing, I was recruited by AXA and was preparing to take the Series 7 and 66 broker’s exams.

To that end, I underwent a pretty rigorous course of study which I found overwhelming (I was still working full-time as an ICU nurse and the brokerage set up what I thought was an unrealistic deadline of 4 months to pass my exams).

I never took the series 7 or 66 exams but I did pick up a significant amount of education in investing, money, and markets which have served me well to this day. Understanding how investments work and how to invest is powerful.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

Living in such an expensive state has probably been the biggest road block. Everything costs more.

We have discussed moving to the mainland since my immediate family now all live in the Bay Area. However, my wife’s father is in a care home and she doesn’t want to leave him.

Our financial planner says we can comfortably retire in Hawaii, but I’m a little paranoid about living here in the middle of the ocean since we are so vulnerable to natural disasters and the vagaries of domestic/international politics which affect our local economy.

What are you currently doing to maintain/grow your net worth? Do you have a target net worth you are trying to attain?

I have moved to a 60/40 equities/fixed income split after much deliberation and discussion with our financial planner and CPA. I have tweaked our portfolios to maximize investment income as that in addition to social security will provide much of our income once we stop working for good.

The advantage to this is that we will not have to draw down our principal and if so, it won’t be much. My wife’s retirement/investment portfolio has already reached over $2 million net worth.

I am close behind at $1.9 million. I hope to have $2 million in my retirement/investment portfolio by the time I start collecting social security.

Other than that, we know that our net worth will continue to grow if we continue with our current habits.

How old were you when you made your first million and have you had any significant behavior shifts since then?

We paid off our mortgage in 2009 when I was 49 and after settling/recording our title and renegotiating our homeowners/hurricane policy, I realized that my wife and I were both millionaires at that point.

Our behavior has not changed much. If anything, we are much more cognizant of our spending and asset accumulation.

We are trying to reduce clutter and only replacing things when they break down and cannot be fixed simply because we find that the more stuff you have, the more time and money you spend trying to maintain everything. We have not had to resort to renting a storage locker and we will make sure we don’t ever have to do that.

Not to mention my fears about what would happen if a major hurricane hits Honolulu – we stand to lose a lot – clothing, books, electronics, appliances, tools, furniture, other valuables. Our goal is to have just enough but not too much.

What personal habits and/or traits have you developed that have made you successful at growing your net worth?

People think that I grew up rich because my father was a stockbroker for Dean Witter (now Morgan Stanley) and retired as a senior vice-president. But the reality was very different.

My dad made good money initially – enough so that my mom was a stay-at-home mom for much of our childhood, enough for all 3 of us kids to attend private school, and enough for a nice house in a nice suburb of Honolulu.

However, that all changed when the energy crisis hit in the 1970s. My mom had to work to help out with the bills.

I was working part-time at the private school I was attending to defer some of the tuition. In addition to that, I was delivering newspapers and working summers at the school for my personal expenses and clothing.

One memorable event sticks out where I had to withdraw some of my summer job money from the bank to help my father pay the mortgage. My parents were never good money managers and I realized that early on.

If anything, I learned what NOT to do financially by watching the mistakes my parents made – living beyond their means and making unwise investments. I knew that if I ever wanted to live a great life free from want or need, I needed to get smart about my finances.

My parents divorced when I was a senior in high school and I knew that an expensive college education in a frivolous major was out of the question. I attended the University of Hawaii and continued to work while in school. I was living paycheck to paycheck while going through EMT and LPN training.

My wife grew up poor – despite some setbacks and living in section 8 housing, both her parents worked hard and were able to provide a solid middle-class upbringing for my wife and her brother. She also had to work after school and during the summers.

Like me, she learned early on to be frugal and live within her means. We got married in family court and signed the mortgage for our first townhouse condo that same day.

So, frugality was imprinted into our psyches from an early age.

———————————

Great start so far!

To read the rest of this story, see Millionaire Interview 473, Part 2.

Great interview – looking forward to the second half.

Regarding your best & worst investments … the cynical employees of one of your stocks say, “Boeing makes airplanes and Lockheed makes money.”

Love that quote! So true. Just goes to show – great management can make or break a company.

Thanks for the first half of your story. I especially liked the comments, “- Buy good quality stuff that will last a long time and has a good history of reliability. We never go for the luxury stuff unless we know for a fact (based on lots of research and hands-on trial if possible) that it will last and rarely break down.

– Learn how to take good care of yourself and your stuff. I can’t begin to tell you how many times that has made a difference. I try to stay healthy as much as possible.

– Avoid divorce. Be faithful and honest to your significant other and treat him/her with courtesy, kindness, and respect. Try to work things out if there are conflicts. You’ll know when the relationship is broken – try to repair it if you can.

These things our parents taught us that are paying dividends today. I thank the Lord we see eye to eye on them and recognize their great value in our life together.

Thanks MI 343!

Yes, early lessons learned are sometimes the best.