Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in February.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

We are 52 and 49.

We’ve been married 21 years and together 26.

Do you have kids/family (if so, how old are they)?

We have 2 children in their mid/late teens.

What area of the country do you live in (and urban or rural)?

We are in the Eastern US, in a large suburb of a metropolitan area.

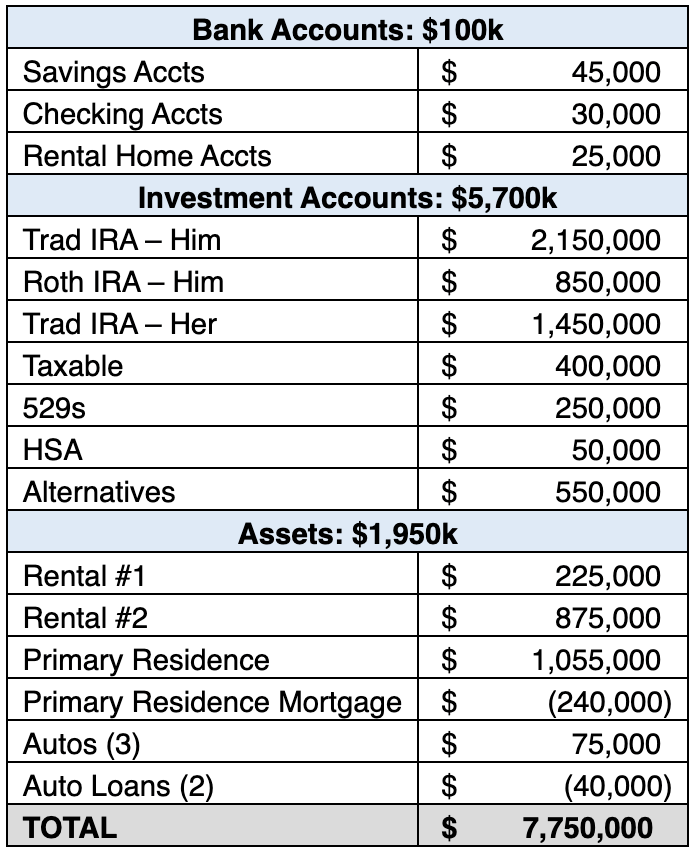

What is your current net worth?

About $7.75M inclusive of assets and liabilities.

I’ve always tracked/thought about our net worth in terms of liquid/investment net worth only, though, since home prices are subjective to begin with and their fluctuation doesn’t do anything to influence our financial position until/if we sell.

Our investment net worth is about $5.7M.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.), and any debt that offsets part of these?

Here they are, roughly:

Notes:

- No other debt; all credit cards are paid off monthly.

- Both rental properties are without mortgage.

- The property valuations are estimates based on Zillow, which I know isn’t reality. And even though I track their values regularly I’m not overly concerned with the valuations of the properties or the cars when looking at net worth.

Liquid net worth was always far more important to me and to my goal of early retirement than a total net worth calculation. The rental properties are income-generating and have appreciated in value significantly since they were acquired.

I have considered whether that equity could be better deployed elsewhere or taken out as leverage for other investments, but don’t have any plans to make changes right now.

EARN

What is your job?

In 2021 we both left our W-2 corporate jobs. Prior to leaving my role was effectively the COO for a 250-person business unit within a large company; my wife was administratively supporting financial management processes at her company.

I continue to actively manage one of the rental properties and spend time every day with our family’s investments and finances.

What is your annual income?

Since we’re no longer in our salaried jobs, for the past couple of years our income has been from capital gains, IRA conversions, K-1s, interest/dividends, and the rental properties. In 2023 it all came out to ~$475k; in 2024 it was ~$335k.

It’s a large drop but those first 3 categories of income can vary quite a bit year-to-year depending on investment sales, cash flow needs, etc., so it’s not concerning.

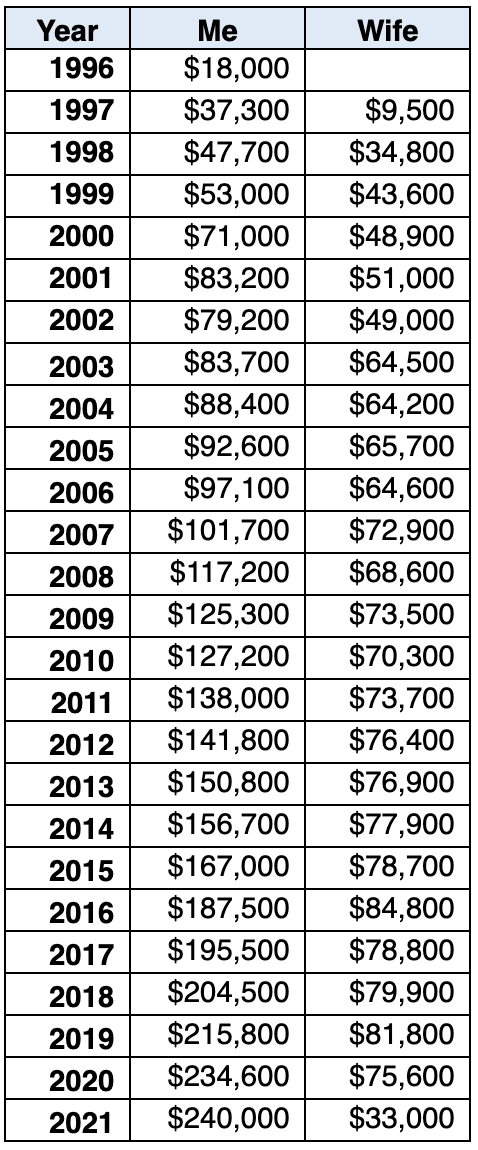

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

Our W-2 income is detailed below since that was the primary source of our income for many years and correlates to our working careers. Values are inclusive of bonuses and performance awards.

This does not include capital gains or other sources of income.

For me, raises and promotions were performance-driven. I don’t recall ever proactively asking for a raise nor did I switch employers to seek a higher salary.

I basically worked at two companies over my career. Promotions were a large driver to salary increases and once I started receiving bonuses that was a nice bump too, especially when recognized as a top performer (i.e., received a larger bonus).

My wife’s job did not offer significant upward mobility or compensation increases but they were not sought after either. What the job did offer was significant flexibility in work schedule and the ability to work from home, which were extremely valuable overall and enabled her to focus time on our children.

Gross rental income has remained relatively steady over the last several years. However, the net cash flow has fluctuated wildly due to maintenance, repairs, etc.

Most years have been in the positive column, but in general, I’d say it’s been far from a great return on the overall asset value. Additionally, the higher-valued rental property is a seasonal vacation property that for various reasons doesn’t return much relative to its value.

Capital gains have fluctuated year-to-year quite a bit.

Over the past few years, I’ve increased our investments in some private market opportunities, listed as Alternatives in the net worth table above. Income from those will be recognized as either capital gains or ordinary income via K-1s and is expected to grow in the coming years.

What tips do you have for others who want to grow their career-related income?

My personal path came to pass by letting my work speak for itself (that is, I was never one to champion myself very well) over many years of working for two large companies (leading to long-term progression and growth). I basically tried to be a dedicated, high-performing employee who delivered high-quality work that was valuable to my managers and my employer, simple as that.

I wore many, many hats over the years (such as Help Desk Technician, Developer, Technical Architect, Infrastructure Analyst/Lead, System Administrator, Project Analyst/Lead/Manager, Program Manager, Financial Analyst/Lead/Manager, Business Development Analyst/Lead/Manager, Contract Administrator, Staffing/Workforce Manager, and likely several I’ve chosen to forget!).

And to think about that laundry list a bit – there are a ton of different skills represented there: technical, written & oral communication, leadership, and sales/marketing to name a few. There were some I was definitely better at than others, but being a Swiss army knife like that led to new opportunities, new experiences, and new doors opening down the road every time.

One tip I’d have is to not ignore skills outside of your core competencies. Early on in my career while in the trenches of “IT” I was identified as a technical guy who could write well, and that combination was valued when developing written communications, putting together proposals, etc.

In general, I was hopeful that I would be recognized and compensated for my efforts and I valued the prospect of long-term employment in an environment that was intellectually challenging, stable, and supportive. By no means is that the right path for everyone and I’m certain greater income could’ve been achieved by taking other paths, but I was satisfied with the result. If income growth was a higher priority, then being more aggressive in job-switching and ladder-climbing would’ve helped achieve that.

However, I considered other sources of satisfaction and gratification from my career path to be rewarding as well (i.e., I didn’t target income growth as the only metric of success). Being able to establish an acceptable work-life balance, being able to work with smart people of high integrity, and being able to work on meaningful efforts were all non-income related qualities of my career that I valued greatly and ones that I wasn’t necessarily willing to sacrifice in the name of income growth.

What’s your work-life balance look like?

For the last few years of our W-2 jobs, it was good for both of us. We were comfortable in positions that allowed us to prioritize that balance.

My wife worked from home for 20+ years and her position generally provided significant flexibility as to when she worked during the day, allowing her to step away for family or household needs and return later in the day/evening if needed. For the last several years (prior to COVID and full-time remote work) my office was two miles from my home.

A dream compared with many years of commuting 50+ miles each way and a benefit I quickly realized I would never want to give up. Otherwise, for the past few years, I was mostly on a ~40-50hrs/week cadence with occasional periods of ~60-70hrs/week once or twice a year for a few weeks or so.

But when I was comfortable that our investments would support us going forward, it was an easy decision to move on from a job that was “good” and paid well but ultimately not worth the time commitment and stress that came with it.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

Rental income has been the primary other source so far, although not a significant one dollar-wise compared with salary or investment gains. Both of the rental properties were inherited.

I have considered expanding real estate holdings to increase cash flow, diversify assets, and take advantage of tax deferrals, however, I am not convinced that the additional complexity, risk profile, and time commitment would be a good fit for me personally. On the flip side, I have also considered selling one rental and investing the proceeds, and discontinuing the other rental and dedicating its use as a personal vacation home.

The Alternative investments haven’t had time to mature into solid returns just yet but most are looking positive. They’re a collection of private equity, private credit, and other investments in that vein.

SAVE

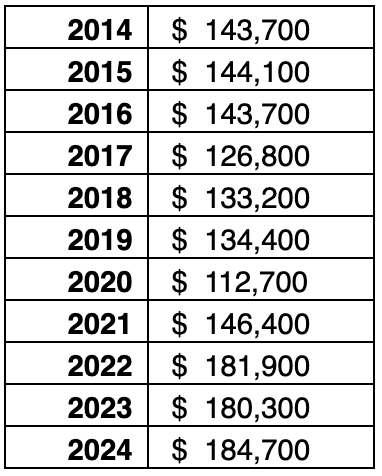

What is your annual spending?

I have tracked almost every penny I have spent since 1995 in Quicken (other than cash-based transactions at least; I use some cash as needed but by default will use a cash-back reward credit card for *everything* – it keeps things simple and I get a reward out of it – win/win). So, I have lots of data. And I’ve looked at it in lots of different ways to calculate a solid foundation to estimate future expenses.

That was always my primary goal for tracking spending – to predict future expenses (reasonably enough, at least) so that we would know our “number” – the nest egg needed to support ourselves at a desired lifestyle going forward.

With that data, I’ve created a baseline of our spending. I make some adjustments to exclude spending bumps that don’t occur every year like buying a car, renovating the house, education, etc. and taxes (since they basically reflect historical income and can change dramatically going forward based on future income).

When I forecast our future spending I add those expenses back in at the amounts/dates when I expect they’ll occur. But here’s a look at our baseline spending over the past 11 years:

The downturn in 2020 was basically due to the pandemic. The primary drivers increasing in the last few years have been significant changes to medical (insurance) and education (private HS & college) expenses and purposeful lifestyle changes: more travel, more dining out, teenagers getting older/more expensive, purchasing two cars, etc.

This was not unexpected, though (i.e., as mentioned I planned for it when forecasting our future expenses).

Based on our expected future annual spending I’ve modeled our cash flow a number of different ways to try and identify the best ways to extract funds from retirement accounts, including investigating if implementing a SEPP makes sense, whether to make a withdrawal from Roth or Traditional IRAs, etc. (under the assumption that our Taxable accounts will otherwise be exhausted by our annual spending).

It’s a first-world problem of the highest degree that the majority of our investment net worth is in retirement accounts.

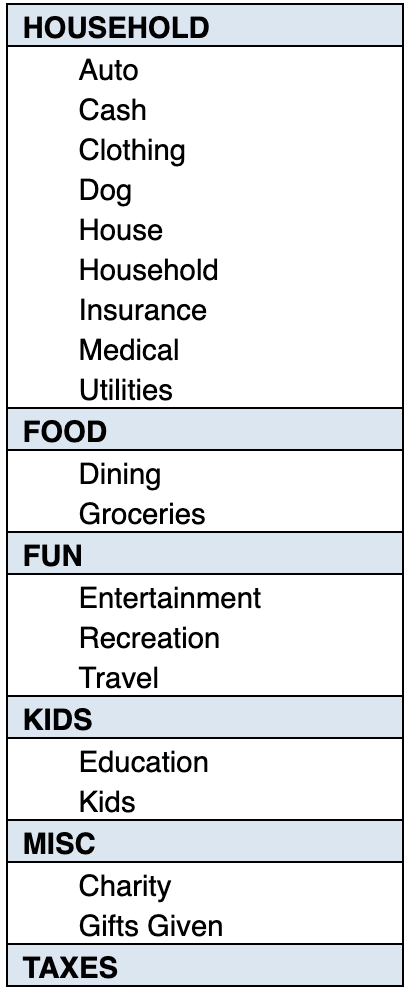

What are the main categories (expenses) this spending breaks into?

I download all transactions into Quicken daily and categorize them into one of the following:

There are occasionally judgment calls and some could overlap, but it works for me.

I also use Tags in Quicken to associate transactions with specific connections – e.g., everything associated with rental property #1, or everything associated with a particular set of home renovations, or a big vacation, etc. Makes for easy reporting.

As needed, I’ll then export the data from Quicken and drop it into spreadsheets I’ve built over the years where I manipulate, track, graph, and model the data, typically by year and by category for both historical tracking and future forecast purposes. My current family financial management spreadsheet has 18 tabs (not counting several hidden ”archived” ones) covering everything from expense tracking, future cash flow modeling, NW calculations, safe withdrawal rate modeling, potential SSA income projections, estimated/actual college costs, investment account tracking, HSA register, etc., etc.

I could probably write several paragraphs on each of the tabs and what I’ve done to track this or forecast that, sources I use, assumptions I’ve made, etc.

Do you have a budget? If so, how do you implement it?

No budget. We both have very similar approaches to spending and find it painful to spend frivolously.

Our threshold for what amount is meaningful has changed over the years, but I believe we’re still relatively modest in our spending relative to our income and assets. It’s just part of our DNA to drive the extra distance to hit the cheaper gas station, avoid the toll road if GPS says it only saves a few minutes, etc.

That said, on the flip side I’m not hesitant to spend far more than that on something special and memorable like a trip, concert experience, or milestone celebration.

I review all transactions daily when loading them into Quicken. I try to let my wife know what’s going on with our finances, and she definitely cares, but she’s not as engrossed in it as I am.

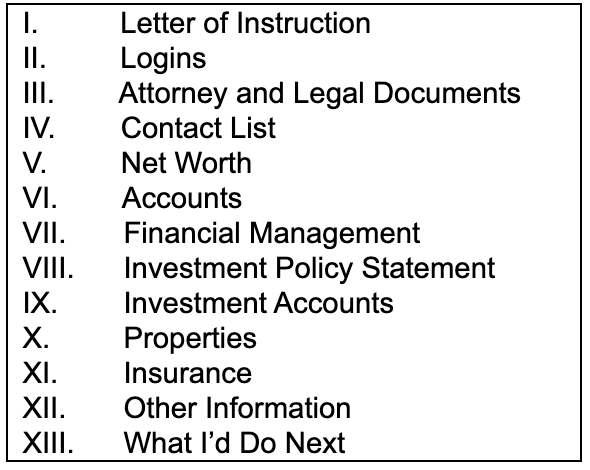

To mitigate the challenge of her managing things in my absence (i.e., if I unexpectedly shuffle off this mortal coil), I’ve written a document detailing every minute detail of our financial lives. I call it our “Family Operations Manual”.

It includes standard estate management material as well as some very detailed descriptions of day-to-day activities that I perform in order to manage our financial lives. I try to update it a couple times a year and review it with her once a year.

It’s currently about 50 pages and the primary sections include:

The process of putting together that document has been immensely helpful to me – having to clearly explain in writing how things are set up, why they’re set up that way, and how to manage them has had a number of benefits. Perhaps the greatest is the insight gained into the inherent value of SIMPLICITY.

Or conversely, recognizing that removing complexity from our financial lives results in less time required to manage multiple moving parts and pieces, less risk of having issues with something going wrong with a finely tuned instrument, and *more time to do other stuff*. I enjoy this minutia but I know she does not/would not.

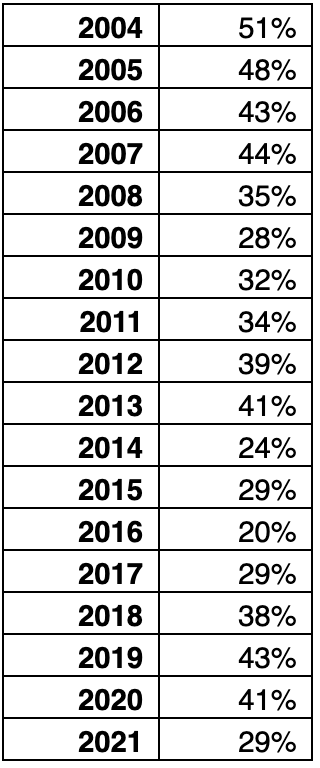

What percentage of your gross income do you save and how has that changed over time?

Our savings rate generally stayed pretty steady over the years. The below table looks at the savings rate defined as total gross income less total expenses (not excluding certain expenses like described before).

As a result, some years the savings rate is less because of the spending bumps or more because of capital gains, e.g. It was an overall average savings rate of 36% from 2004 until we retired.

What’s your best tip for saving (accumulating) money?

The two mindsets that helped us the most were “live within your means” and “pay yourself first”. On the first, I was able to avoid accruing any significant debt (I’ve been paying off those credit cards in full every month since I first got them and was able to avoid loans until our first mortgage).

On the second, every time our financial situation changed via either an increase to income or reduction to the expense side – e.g., get a raise at work, get a promotion, get a bonus, kids age out of daycare, etc., I would take that money and transfer it into our money market (savings) account as if it never existed.

For recurring things like a salary raise or a reduction in daycare costs, I set up an automatic transaction to occur. I also transferred any withdrawals from FSA or Dependent Care accounts and income from rental properties into savings as well.

I developed a fairly comprehensive system of tracking each dollar that was moved in that way – the category/source of funds, etc., so that I could see any trends that were developing and identify any tweaks to make it more effective. Every so often I’d shift funds from the savings account to a taxable brokerage account to add to our investments.

What’s your best tip for spending less money?

Needs vs. Wants. And Needs doesn’t mean bare minimum to survive – it could mean what’s needed to live contently.

But do I truly “need” this? The vast majority of the time I find I can answer that with a no, and will walk away from/modify the purchase.

That said, with where we are now financially if there are things in the Wants category that I think will improve enjoyment of life and are affordable/won’t impact our financial position, I have no issue spending money on those things.

I am also the walking definition of paralysis through analysis. I study and research decisions until I am comfortable that I fully understand every angle, every pro, every con.

Yes, that is definitely problematic at times. An upside of that, though, is that it becomes a type of self-fulfilling process of not spending money frivolously and filtering out Wants vs. Needs.

That process frequently helps me realize that perhaps I don’t really *need* something and I will be satisfied with passing it up, going with a lower-priced option, or waiting until it becomes a true need. And doing so doesn’t feel like a sacrifice to me.

What is your favorite thing to spend money on/your secret splurge?

I’d love to give a unique answer to this, but I expect what I have to say isn’t uncommon. Spending money on experiences has been one of the greatest benefits of having money to spend.

Travel, good food, entertainment, and enjoying time with friends and loved ones – those are the things most fondly remembered. The other would be spending money to “buy time”.

Having the flexibility to do what I want when I want is a valuable resource.

INVEST

What is your investment philosophy/plan?

In general, I think that Warren Buffett’s well-known guidance to his heirs is a perfect example of an investment plan that nearly everyone should follow:

My advice to the trustee couldn’t be more simple: Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund. (I suggest Vanguard’s.) I believe the trust’s long-term results from this policy will be superior to those attained by most investors — whether pension funds, institutions or individuals — who employ high-fee managers.

My version of that is to utilize a “Three-Fund Portfolio” for most of our investment funds. Based on that approach our target allocation for the majority of our investments is a 90/10 split between stocks and bonds in the following ETFs:

- 70% in Vanguard Total Stock Market ETF – VTI

- 20% in Vanguard Total International Stock Market ETF – VXUS

- 10% in Vanguard Total Bond Market – BND

But we don’t solely invest in those funds. For better or worse, and hypocritically/a counter-point to some of my previous statements about the value of simplicity, our current portfolio is more complex than that.

While I dislike straying from the simplicity of having a straightforward asset allocation strategy, doing so has enabled higher returns. And to be honest, I enjoy analyzing and tracking investment opportunities.

So at the moment, I maintain a balance between these three components in our overall portfolio: 1) a passive allocation in public equities via a Three-Fund Portfolio as described above (~60% of investments); 2) a semi-active allocation of investment funds in private market investments (~10%); and 3) an active allocation of funds in individual company stocks (~30%).

What has been your best investment?

The individual company stocks that I invest in are primarily high-growth companies. This investment style has resulted in some very large, very volatile swings in value.

One of the reasons my retirement accounts grew so much is that I had the flexibility in my 401(k) to invest in individual stocks. Most of 2020 and 2021 were absolutely fantastic years for those growth stocks.

That portion of our investment portfolio has continued to outperform index funds that I’d otherwise put the money in, so I keep at it and re-balance our portfolio when needed to maintain the overall allocation percentages.

What has been your worst investment?

Highlight the first two sentences above. Copy. Paste.

Replace the “fantastic years” sentence with: 2022 was an absolutely lousy year for those growth stocks. Live by the sword, die by the sword.

Fortunately, the end result remains significantly positive over the longer term.

What’s been your overall return?

Since 2013 the average annual return across all of our investments has been ~18.5%.

How often do you monitor/review your portfolio?

I monitor it daily. I take action on the individual stock holdings (i.e., trade) about 10 times per year, including rebalancing funds between and within individual stock holdings and our three-fund portfolio to maintain the overall asset allocation targets.

In addition to the family financial management spreadsheet mentioned previously, I have an investment management spreadsheet I’ve built over time with a couple dozen tabs that I use in conjunction with Quicken to assess performance, asset allocation, rebalancing needs, etc.

NET WORTH

How did you accumulate your net worth?

I attribute it to a combination of factors over a long period of time: a very good (but not insanely ridiculous) salary; a strong effort to save, save, save, and avoid frivolous spending; an interest in the stock market and some good fortune there as well; and a long-standing passion for personal finance, tracking numbers, and forecasting.

I consider my path to have been much more so the tortoises than the hares. I’ve also been fortunate in a number of ways financially that acted as accelerators (or at least not decelerators): no student or car loans after graduating from an in-state school, an inheritance at age 40 that increased my investment portfolio by ~10% and kick-started the relatively minimal rental income, and an absence of any financial derailers (e.g. divorce, medical, legal, etc.).

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

It’s difficult to call out one leg of the proverbial three-legged stool as the most important because where would you be without the other two? (falling on your %*$# is where!)

Our investments have easily been the biggest contributor dollar-wise to our wealth-building, but they wouldn’t have had a basis from which to grow if we hadn’t saved as much as we had, and we wouldn’t have been able to save as much if we hadn’t earned as much. So….

But to try to actually answer the question, I’d have to say my greatest strength (as in core ability) is in Saving. I say that as much to call it out as a natural strength as to call out deficiencies in the others.

Because, regardless of results, I still have feelings of imposter syndrome with taking credit for the success of our investments, and I feel that my career earning potential was certainly hamstrung by a lack of natural salesmanship or self-promotion, or job-hopping.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

It took about 17 years to go from $0 to $1M in investment net worth. About half of that period was before I was married, about half after, but for various reasons it didn’t start to significantly accelerate until after.

As mentioned before, we didn’t suffer any massive financial derailers. One potential road bump (we were both included in mass layoffs from our employer the same year) was mitigated because we had the savings in place to support ourselves.

What are you currently doing to maintain/grow your net worth?

I spend a fair amount of time looking at investment options.

Namely individual company stocks and alternative investment opportunities.

Do you have a target net worth you are trying to attain?

Every time I’ve come close to hitting a target I had set I find myself creating a new one, so I’m not sure if that’s motivational or just a self-inflicted state of Tantalus. At the moment I’m eyeing $10M in investments as a target, but I feel like we’ve already hit the number we’d need to be comfortable for the rest of our lives.

The concept of “enough” is important to me and I know we’re extremely fortunate to be in the position that we are.

How old were you when you made your first million and have you had any significant behavior shifts since then?

By looking at our records I can pinpoint the day shortly after I turned 39 when we crossed the threshold of $1M in investment net worth. It’s also the day my dad died. Because of all that happened leading up to that day and the aftermath, I don’t even recall when I became aware that we’d hit that milestone, whether it was at that time or much later.

And his life/death had far more impact on my behavior at a core level than hitting 7 figures anyway. Without getting too much into it, he was never financially stable (a massive understatement, actually) and I’m certain my drive to save, to not be frivolous in spending, and to accumulate wealth comes in part from seeing him do the opposite.

As far as changes, as the kids have grown older expenses have increased in number and levels and we’ve been fortunate to be able to enjoy some special experiences from time to time, so spending has definitely increased over the years but it’s been more so a feeling of slightly relaxing the reins on spending than anything else.

What money mistakes have you made along the way that others can learn from?

20/20 hindsight is a lovely thing. As noted above, our wealth sky-rocketed in 2020 and 2021 due to stock investments.

What I wish I’d done differently.. what I had told myself to do… what I had planned and plotted out so carefully in writing and spreadsheets… was to diversify our holdings more broadly. But I repeatedly convinced myself to ignore those best-laid plans for just a little bit longer because of this reason or that.

And it was extremely painful (emotionally, at least) riding that slide down. Fortunately, it was not overly painful financially other than realizing that some of the more extraordinary dreams would need to wait before becoming reality.

I had an asset allocation model at the time but it did no good being ignored. I’ve since revisited it, reinforced my dedication to it, and now actively re-balance as needed between a three-fund portfolio, individual company stocks, and non-stock investments.

What advice do you have for ESI Money readers on how to become wealthy?

There are a lot of wealth-building mechanisms out there. Real estate, entrepreneurship, investing, W-2 salary/bonus, etc.

Figure out where you’re most comfortable, where you thrive, where you can be passionate, and spend untold amounts of time dedicated to your mission. Be prepared to grind, to work hard, to sacrifice.

Pay attention to the details. Prepare. Plan. Think long-term.

Yes, there’s nearly always some luck involved, but as the saying goes, luck happens when preparation meets opportunity.

And don’t forget there are two sides to the equation: in and out. What also worked for me was watching every dollar I spent, tracking how/where/when/why I was spending money, and adjusting habits as needed to help meet goals.

It also helps tremendously that I enjoy spending a lot of time pouring over the data and building spreadsheets to extract insights into our income, spending, investing, and overall financial well-being.

FUTURE

What are your plans for the future regarding lifestyle?

Depending on who you ask, I’m either already retired or I work part-time managing our investments. My wife is thinking about finding something (job or volunteering) that’s light on stress and high on fulfillment; I honestly don’t know if I could find one of those that would be a fit for me.

It wouldn’t be about the money, though, so volunteering in a position that’s rewarding is certainly on the table.

The only major lifestyle change I see that has potential in the next several years is that we may dedicate one of the rental properties as a second home and stay there in the summer months. Once both kids are out of school and on their own, several years from now, we may think about whether we stay in our primary residence or make a move.

What are your retirement plans?

Financially, stay the course. Manage investments (hopefully with positive results) and monitor expenses.

The past couple of years have been full of kid-related activities, and it’s been absolutely great to not have to be worried about conflicts between work and family plans. We like to stay physically active so I expect that will continue.

More travel is definitely on the list. And our future may involve finding that unicorn work/volunteer opportunity.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

I’m not concerned about our finances in retirement primarily because I feel like I have them reasonably well-defined. I have estimates in our long-term projections for education costs, weddings, increased medical costs, car replacements, occasional home renovations, etc., and I feel like we can generally manage our baseline spending.

Other than financial, we have a solid social network in our community and actively work on keeping ourselves healthy, so I feel like that’s reasonably well-covered also. It’s common that people talk about retiring “to” something vs. just retiring from your job.

For whatever reason that was never a concern of mine. We’re now able to include more of various things that are valuable to us (kids, recreation, travel, DIY, etc.) and I’m totally content with that.

Of course, everything is subject to change, though.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

My deepest and oldest motivation to build wealth was that I did not want to have to worry about money. So from that side, it “clicked” from the start.

I generally learned about finances on my own. I got an undergraduate degree in business (focusing on IT), and although there were courses in Accounting and Finance there wasn’t anything about personal finance.

I bought my first book on personal finance while in college. I also followed several personal finance/investment websites and online forums pretty closely at the time – still do for that matter.

After getting my first real job I saved some money and bought a handful of stocks. One of the more fortunate was buying Amazon in early 1998 (I sold it several years later for a very healthy gain, but nothing close to where it is now – so maybe that’s my worst investment!).

Who inspired you to excel in life? Who are your heroes?

As mentioned before my father was inspirational in an atypical way. Rather than go into details I’ll just say I was inspired to do better.

I’ve admired a number of people for various reasons but it’s tough for me to pick out one in particular on the financial front. In general, I find entrepreneurs inspirational.

I almost started a tech company shortly after graduating and occasionally wonder what could have been…

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

I love books. I value them greatly. I think they’re worth their weight in gold.

I worked at a bookstore in high school. I love being in libraries. And hey, I even bought stock in “Earth’s biggest bookstore” early on.

So to feed that passion for the written word I’ve bought quite a few money books over the years. And for the most part, they sit on my shelf, unread. Sigh.

I seriously don’t know why. I mean, I buy them because I love learning and want to add that knowledge.

I’m sure a therapist could help crack that nut. I still buy a new one from time to time even though I haven’t opened many of the old ones (not unlike my video game collection, actually).

Hopefully one day I’ll figure myself out!

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

Not a lot monetarily, as a percentage of wealth at least. I see it as a shortcoming, truthfully.

I’ve considered setting up a Donor-Advised Fund as a mechanism to donate more. My wife has volunteered a decent amount and taken on some volunteer leadership positions as well, and I’ve joined in for part of that.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

Our revocable trusts basically boil down to distributing our assets equally to our children in stages (I believe it’s 25% at ages 30 and 40, with the remainder at 50). At the moment both kids seem to have reasonable heads on their shoulders so we don’t expect to have to ‘project them from themselves’ or split it unequally.

It seems the current trend is toward advocating for a quicker distribution vs. spread out over time. I fully expect we’ll make adjustments over time as we see fit.

Its clear that you love your spreadsheet! I’m a similar nerd that started working the same year and have done the same. As I was going through stressful times at work (like many many rounds of layoffs and restructuring), it was in some ways my method of convincing myself that we would be fine regardless of what happened.

However, I’m trying to simplify and ween myself off of it. I want to spend more time doing things with people instead of polishing my spreadsheet.

The only question that I have for you is about the rental properties. In your nice write-up, you sort of get right to the point of convincing yourself of selling at least the first of them. The return isn’t great and you want to simplify. I’d say go for it…..cashing a quarterly dividend check isn’t too much work!

Nicely done and best wishes.

Yes, I find myself going in cycles (hopefully not circles!) lately – where sometimes I’ll think of something new I want to add to a spreadsheet and dive deeply into it to build it out, etc., then other times will perform what I’d consider minimal maintenance on the data (monthly updates, analysis, etc) and just let it be. I definitely agree on focusing on the importance of other things in life.

With having rental(s) I’m definitely of two minds – I see the appeal and the financial benefits but also *really* don’t enjoy it when there are problems to address.

Don’t let yourself fall into “1-more year” syndrome, even though you are “retired”, you’ve done a great job accumulating and showing what is possible through discipline and planning. Now your joy will come from helping kids, family, enjoying life, and giving it away. Die With Zero is a book I recommend to everyone, though I hope it doesn’t just sit on your shelf!

Nice work and what a great story to share. Can you a;so share about your family healthcare expense per year and are you purchasing your through an Obama Care exchange?

Total healthcare expenses for our family of 4 (including medical/dental insurance, dr visits, etc etc) for the past few years has been

2022: $29.8k

2023: $24.4k

2024: $31.9k

Medical/Dental Insurance has been ~$22k-$23k for each of those years. Other major factors have been medical procedures and dental work.

We get our medical insurance directly from Anthem/BCBS. It’s an ACA-compliant plan but not offered via the Exchange. Medical plan is a typical high deductible Bronze plan with HSA. We opted for this as it was an EPO that offered greater in-network coverage and did not require referrals from our PCPs to see specialists. The only options on the Exchange in our state are HMOs with more limited in-network coverage and requiring referrals. I’m also currently considering a PPO option, to provide out-of-network coverage as well, but haven’t done a deep-dive yet to see if that plan makes sense.

Great success. Given the market volatility now, are you still rebalancing? Are you mostly using dividends, interest and rental properties to generate your needed annual income? Thx

As a fellow planner, I really liked your “Family Operations Manual!”

Make sure to join the Millionaire Money Mentors forums if you haven’t already! ESIMoney graciously provides you a free membership. By doing your millionaire interview you are considered a mentor on the forums.

Thanks for so many details. You enjoy your spreadsheets and it gives you peace of mind. Even when the market goes down, knowing your assets is a benefit. Your document detailing every minute detail of our financial lives. I call it our “Family Operations Manual” is a great idea.

Thank you for sharing!

I liked the comment, “My personal path came to pass by letting my work speak for itself (that is, I was never one to champion myself very well) over many years of working for two large companies (leading to long-term progression and growth). I basically tried to be a dedicated, high-performing employee who delivered high-quality work that was valuable to my managers and my employer, simple as that.”

We dealt with our careers in the same way, as serving the Lord in the location in which He planted us and had ministry for us to do was of utmost importance. In addition, my wife wanted to stay in the area and maintain stability through our employers. The Lord blessed us with 32 and 35 year public service careers that treated us well among our peers and we sought to honor Him via tithes and abundant offerings along the way. This truly opened the window of Heaven over us in many ways including including our financial situation greatly exceeding anything our good stewardship on its own could accomplish.

Nice job! I also often wonder if I retired – would I struggle to find something that gives purpose and “enough” money. Even though I don’t “need” the money. Well said. Sounds like you are staying busy with your financials.

Can you give more info on your income. I would think conversions wouldn’t be income because you have to pay tax on them and would be letting them grow in your Roth. So what is your true income from properties and investments? Capital gains I kind of get but you can spend them…or reinvest. So was curious if you would share the income side a little more.