Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in March.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I am 38, and my husband is 33.

We have been married for 8 years.

Do you have kids/family (if so, how old are they)?

We have two children: ages 6 and 3.

What area of the country do you live in (and urban or rural)?

We live in the Midwest in an urban area.

What is your current net worth?

We just squeaked over $1,000,000.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

Assets:

- Cash: $71,000

- Retirement accounts (401k, 457, Roth IRA): $470,500

- Pensions cash value: $31,000

- Taxable brokerage/individual stocks: $74,000

- HSA: $30,500

- 529 Accounts: $58,000

- Primary residence: $535,000

- Rental property: $230,000

Total assets: $1,500,000

Liabilities:

- Mortgage on primary residence: $369,000 (5.625%)

- Mortgage on rental property: $90,000 (2.5%)

- Small Business Administration Loan: $23,000 (5%)

- Home improvement loan: $4600 (0%)

- Additional home improvement loan: $8200 (0% interest until the promotional period is up. We plan to pay it off at that time.)

- Credit Card: We average $4000 on our credit cards, and we pay it off each month.

Total liabilities: $498,800

EARN

What is your job?

I am a lawyer, and I work for the state. I’m in the mid-part of my career.

My husband is a data scientist, and he is in the earlier part of his career.

What is your annual income?

Combined, our annual income is about $280,000, including a bonus that my husband receives.

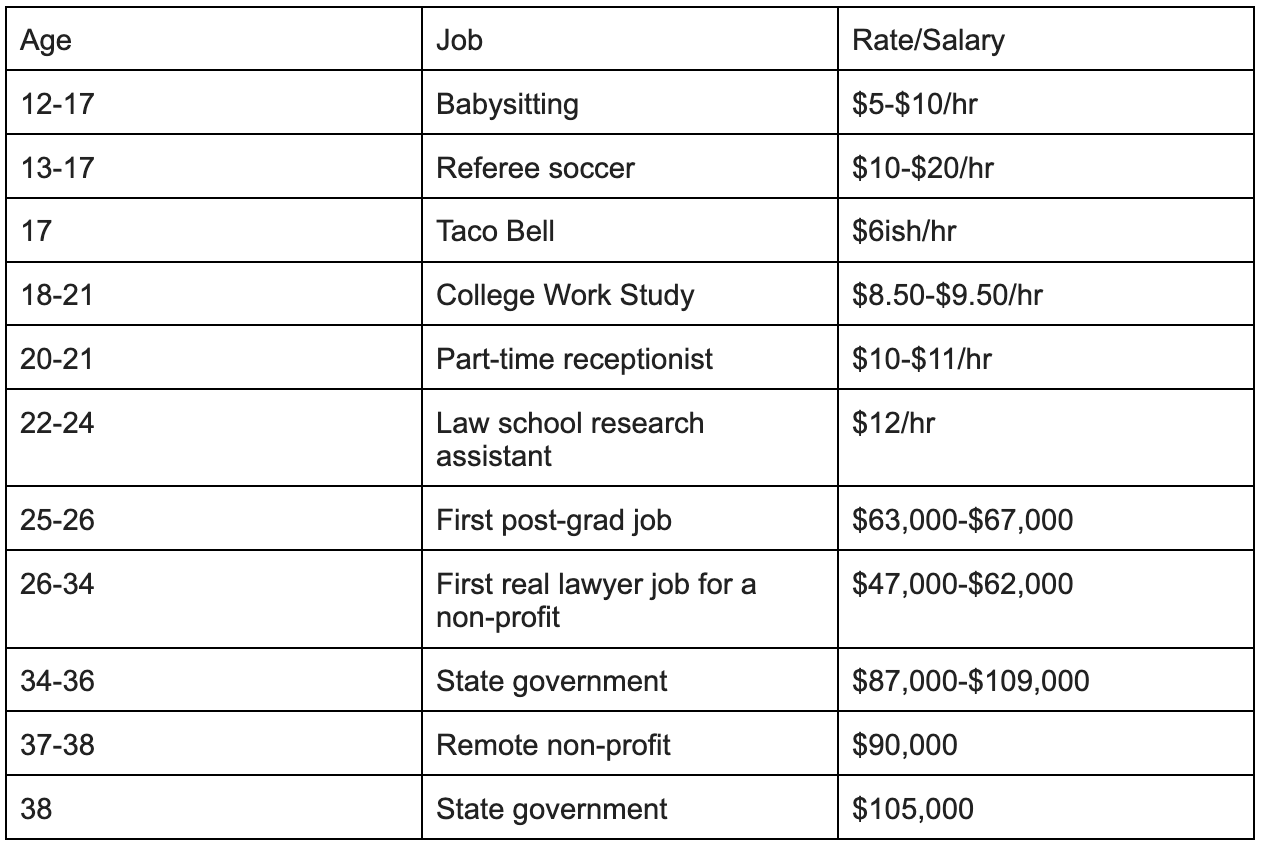

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

When I was looking for a summer associate position in law school, I had a difficult time finding something. I turned down a paid summer legal job to work instead for a nonprofit with a small stipend (<$2000) because the paid job said there were no opportunities to get hired, and the stipend job had opportunities to get hired.

I ended up working full-time for that stipend job for 7.5 years later on. I will need an alternate universe plot to figure out if that was the right move or not, since that really sent me off in my practice area and public service.

My first job out of law school was “JD preferred” and was not considered practicing law. It was a difficult time to find a job since many of my classmates who graduated in the 2 previous years had their offers rescinded or deferred due to the great recession.

The JD preferred job wasn’t the long-term goal for me. I did receive a “salary adjustment” early on that boosted my pay.

I then took a job opportunity to practice law, which had pros and cons. The job was well-respected but underpaid.

It was at the non-profit where I did my summer externship for a stipend after my second year of law school. I did not apply for the job, but I was offered the job out of nowhere.

During my time there, I was promoted to a manager, and I supervised other attorneys in this role. I gained valuable experience but felt burned out and underpaid after 7.5 years.

I did turn down a private practice job after about 4 years that would have increased my salary to $100,000. A headhunter contacted me, so I applied and interviewed for the job, but realized maybe not having to work long hours was worth a lower salary.

In 2021, I left to take a state job because the earnings would be substantial for me as my husband was still in grad school, and our family was growing. I also left to go to a job that had paid maternity leave. (I was pregnant when I switched jobs).

The job I was leaving did not offer any paid maternity leave, but I did have sufficient sick time built up. The nonprofit did not offer me any salary increase to stay – they said because they couldn’t come close to the new job’s salary.

That job did eventually provide salary adjustments about 7 months after I left, and they now offer 12 weeks paid maternity leave.

After 2.5 years at the state agency, I was looking for a 100% remote job to have more flexibility with my schedule and 2 children. The one I found was at a non-profit for another pay cut.

Unfortunately, the remote job turned out to not be flexible, in addition to being a pay cut. I requested flexible scheduling multiple times and was told that I was an exempt employee who didn’t qualify for flex time, even though it was contrary to what I understood when I took the job.

After just one year, I went back to work for the state in a different state agency.

My husband was in grad school until 3 years ago. While in grad school, he earned a stipend of around $30,000 for 5 years.

Once he took a job in the industry, I believe he started at $135,000. His base salary is now $155,000.

He has received a bonus each year. It brings him up to the $175-180k range.

What tips do you have for others who want to grow their career-related income?

My income has not been linear growth. I would say to not be afraid of a pay cut if it is going to be a more interesting job, a better career trajectory, or a better lifestyle fit.

I would also say that if you change jobs and it’s not a good fit, it’s okay to change jobs again. I am much less afraid of making a job change than I was 5 years ago.

I am not worried about the job changes on my resume.

What’s your work-life balance look like?

I work a 37.5-hour work week, and I am hybrid.

It offers flex time, and everyone I work with really takes advantage of the flexible hours.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

I have a rental property that nets around $6000 – $7000 per year. I bought this property as my primary residence when I was single and earning $48,000 per year.

I used some money from an inheritance for the down payment. I lived with roommates to subsidize my housing costs.

I did not know I was “house hacking” at the time.

SAVE

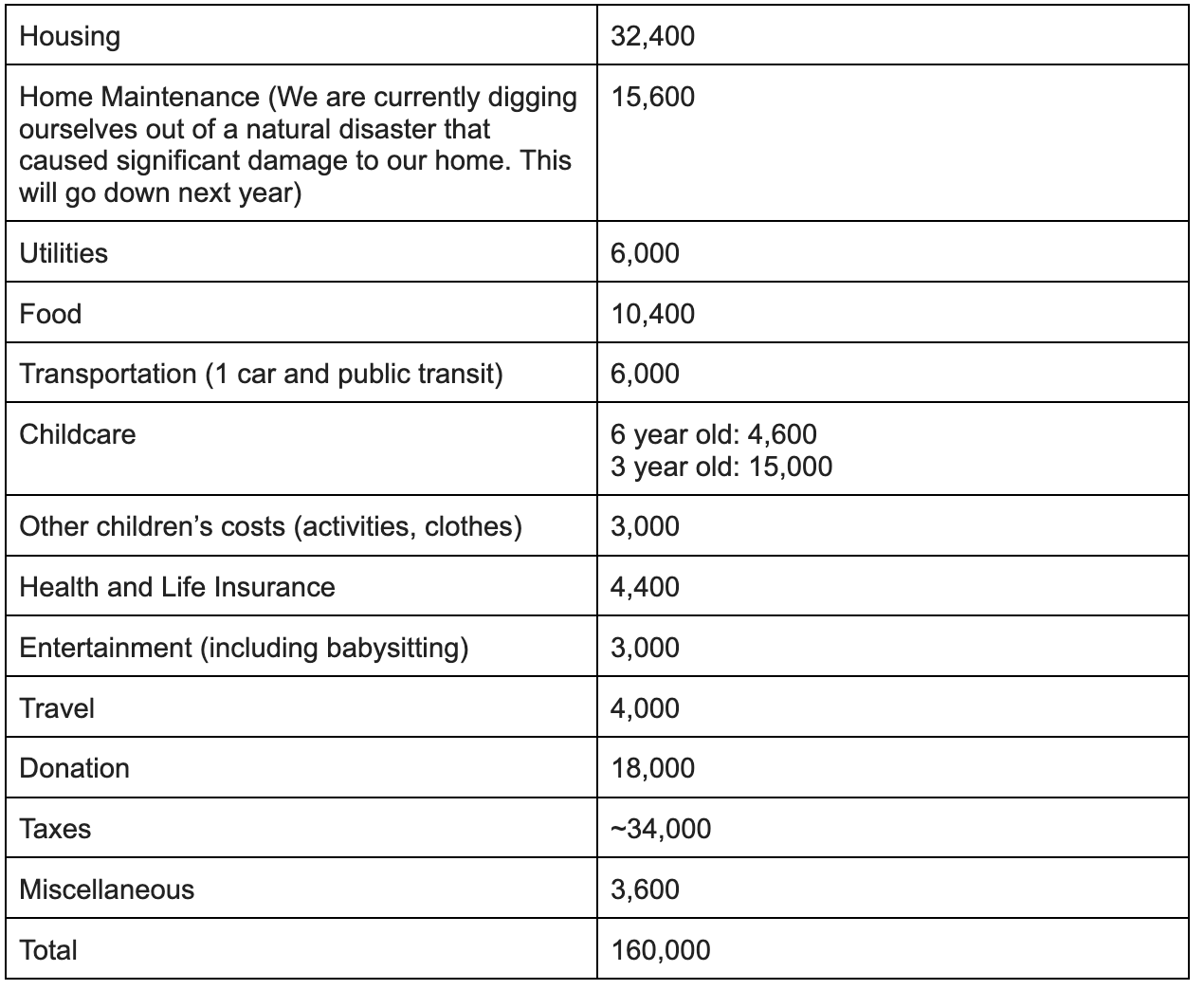

What is your annual spending?

$160,000.

What are the main categories (expenses) this spending breaks into?

Do you have a budget? If so, how do you implement it?

I have a loose budget with these numbers and categories. I am not tracking it that closely.

However, when I sign my child up for summer camp, I add that number to the line item. When our car registration goes up, I adjust those numbers.

The entertainment, travel, taxes, and miscellaneous categories are much more general estimates that I’m not tracking closely.

My husband and I review the big picture together quarterly. We discuss big expenses together. We don’t set allowances or limits on our spending.

What percentage of your gross income do you save and how has that changed over time?

~42%. I’ve always been a saver. It’s probably been pretty stable at around 40%.

My goal is to save 50%, but our costs just keep increasing.

What’s your best tip for saving (accumulating) money?

Automate savings and investing.

I plan to max out all of our retirement accounts first. Then, I add in other expenses.

What’s your best tip for spending less money?

My best tips are:

- Try to repair items first.

- Get multiple estimates for any home improvements and ask around for recommendations. We had massive damage to our home in 2023 due to a natural disaster, and we sought out many estimates to understand what we actually needed to repair the damage to our home. We used a few different contractors to do different types of work, and we ended up spending around $50,000. We got lots of estimates that ranged from $30,000-70,000.

- Look for used items first. (I am a big fan of Buy Nothing groups)

- Take advantage of coupons and deals. I rarely pay full price for anything because I know it will go on sale at some point. (I’ve started following some couponers on Instagram, and it’s been a fun game to figure out.)

- Be grateful for food allergies because that means you don’t go out to eat that much, and you learn to cook great meals at home.

What is your favorite thing to spend money on/your secret splurge?

Theater tickets, but I know the tricks and tips to get tickets around $30 pretty regularly. The trade-off is that I don’t get to pick the seats.

INVEST

What is your investment philosophy/plan?

Currently, we are maxing out all of our retirement and HSA accounts. We have a set goal for 529 accounts.

I invest in index funds. I have 1 individual stock that I inherited.

We are looking to increase our investing in taxable brokerage accounts this year and start focusing on saving money where we will be able to access before the 59.5% penalty fee. We are also planning on selling our rental property because being a landlord has not been enjoyable.

What has been your best investment?

Index funds.

What has been your worst investment?

The rental property probably hasn’t been our worst investment numerically, but I did have to go through the eviction process this past year, so it has been the least enjoyable.

What’s been your overall return?

I really don’t know. Similar to the S&P 500?

We really started learning about finances in 2019.

How often do you monitor/review your portfolio?

I update my net worth quarterly. I review the information sometimes weekly, sometimes monthly.

I don’t make any changes.

NET WORTH

How did you accumulate your net worth?

My grandparents set up a mutual fund for me that I didn’t know about until I bought my condo in 2014. I used about $15,000 of the $30,000 at that time for a down payment on my condo.

I also inherited about $65,000 of an individual stock in 2017. It grew over the next few years, when I cashed almost all of it out in 2022 to put a downpayment on our home without needing to sell our condo.

I did cash it out at a pretty terrible time in 2022, so that was a bit of a bummer seeing the value take a big hit and needing to cash it out.

I had my student loans forgiven under PSLF in 2023. My income-based repayments were on pause due to the pandemic from March 2020 through forgiveness, so I only had to make seven years of payments.

The total forgiven was just under $50,000. I chose to go to a relatively inexpensive law school.

My undergraduate and graduate school loans totaled around $70,000 ($16,000 undergrad and $54,000 graduate school).

I chose to graduate undergrad in 7 semesters because the cost of tuition was increasing at an alarming rate, and I couldn’t afford to keep attending. During my last semester of college, I lived at home and commuted to college 2 days a week (30 miles) and worked as a receptionist the other 3 days a week.

I also kept working my work-study job, so I was on campus from 8 am to 11 pm on Tuesdays and Thursdays during that last semester.

My husband has never had any student loans due to the GI Bill and grad school paying for tuition and a stipend. He has never received an inheritance.

The rest of our net worth has been through our earnings.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

I would generally say saving, although looking at our current spending feels a bit outrageous. I did put myself in good positions to save even though I had low-earning years.

My personal strength of the 3 is saving.

You could probably argue that we succumbed to lifestyle creep, but we really made conscious decisions related to our housing costs and our earnings level. I don’t feel like we live an extravagant lifestyle, but we do spend a lot of money each year. I’m hopeful that some of these costs are going to go down soon. (childcare mainly)

Currently, our combined strength is earning, but that is relatively recent in the last 3 years.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

The Great Recession impacted my ability to find a job out of law school. I didn’t really have any mentors on how to find or interview for a legal job.

I have had relatively low earnings for my entire career because of the public interest path I took/fell into.

The rental property has been more of a headache, and I’m ready to be done with it. The HOA costs have substantially increased due to years of not prioritizing maintenance.

The renters we have are not ideal, and I hope they move out at the end of their lease term so I don’t have to start the eviction process with them again.

Our primary residence also had a host of problems since we moved in. I would recommend you understand what, if any, recourse you may have with the sellers regarding repairs.

We bought from a builder company that flips houses, and we had a 1 year warranty, so luckily, a lot of the issues, like gas leak, frozen pipes, and improper electrical, were able to be remedied through that process. The natural disaster we experienced was not covered under the process and was apparently also excluded from our homeowner’s insurance policy.

What are you currently doing to maintain/grow your net worth?

Continuing to save and invest as much as possible. I am looking at starting some sort of consulting really part-time, in my area of expertise.

I haven’t really gotten it off the ground yet, so maybe there is some other potential earning in the future on a part-time basis.

Do you have a target net worth you are trying to attain?

I would like to hit $2,000,000. I may take a sabbatical before we get there.

The next plans are always adjusting.

How old were you when you made your first million and have you had any significant behavior shifts since then?

38. It was this month, so no.

I signed up to do this interview to celebrate.

What personal habits and/or traits have you developed that have made you successful at growing your net worth?

I don’t buy a lot of things. Growing up, I was told “no” a lot when it came to buying clothes and things.

I was afforded a lot of experiences as a teen, so I have carried that over to my adult life.

I do enjoy travel, but with two small children and limited PTO making travel more expensive and challenging, I’ve had to really reevaluate what I enjoy about travel. Luckily, I live in a city with amazing things to do, so we’re going to the museums and seeing theater regularly from the comfort of sleeping in our own beds at night and with discounts for being residents or knowing how to use the free days.

What money mistakes have you made along the way that others can learn from?

I didn’t know about Roth IRAs until 2019. I thought that since I had a 401k through work, that I couldn’t contribute to other types of accounts.

There were at least 7 years that I should have contributed something, if not the full amount.

I didn’t understand one of my job’s 401K matching mechanics for several years. My company matched 35% of what you put in up to 7% of your salary.

For the first several years, I only put in 7% of my salary, thinking that was the ceiling of the match. I needed to put in 20% to get the full 7% match.

I probably would not have been able to do 20% from the outset, but I could have gotten there sooner had I understood it.

When I sold my inherited stock to put a downpayment on my house, I just used the cost basis as the first business day after my grandma passed away. Then I learned that I could have picked any date in the 6 months after her passing, so I should have picked a date with a higher value to not have to pay as many capital gains taxes on it.

Sometimes, I think we should have just sold our condo and used that money as the down payment instead of selling the stock. The 2.5% interest rate (and everyone in FI communities having rental properties) lured me into becoming a landlord.

I just don’t like having to drop everything to fix something, and renters definitely do not take care of the unit the way I would hope they would. They also stopped paying rent for a time and then were able to get rental assistance, but it was still a several-month process.

When I get to the withdrawing my funds phase of life, I will need to study a lot more on what to do to make sure I do it correctly.

What advice do you have for ESI Money readers on how to become wealthy?

I don’t have any novel advice. I think that you should not be afraid of a dip in your income.

If you make intentional choices, you will make adjustments to your spending, and you will still make progress. I know that if I make a change, it will not derail my plans completely.

Definitely find a partner who has the same overarching goals and interests. My husband is less interested in “retiring early” because he likes his job.

But we’ve definitely discussed that being financially independent is never a bad goal to have and that no one is immune to job loss or bumps along the way.

FUTURE

What are your plans for the future regarding lifestyle?

I am hoping to retire early in 7 years. We will need to reevaluate if we can both fully retire early at that time based on updates in spending and if we’ve made as much progress in our taxable brokerage growth.

Based upon this rate of spending, I don’t think the numbers will work out unless the stock market really takes off. But hopefully our spending can level out a bit lower.

What are your retirement plans?

My retirement plans include volunteering with my children’s schools and my community. I currently volunteer for a national organization a few hours per week in a data capacity, and I would be interested in doing more volunteering.

I also hope to be able to spend more time biking, walking, playing sports, and just being active and not sitting all day at a computer.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

Natural disasters are a significant concern of mine. We were able to receive funding from FEMA and a loan from the Small Business Association.

We also joined a local HOA that offers financing for home improvement for homes in our area since the homes are so old. We were able to get $6000 for 0% interest for 5 years.

They offer loans at 0, 2, and 3.5% interest rates but we were ineligible to get more because we didn’t have enough equity in our home at the time. Now that we have mitigated the damage, I tried to get additional coverage in our homeowners insurance policy, and I cannot add it.

I also cannot switch insurance companies right now due to the claim we made. (No one will insure me). So, a bit of self-insurance is really all I can do.

I was less concerned about health care than everyone else in these interviews, but I am not looking forward to the changes that are likely coming over these next few years.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

My mom taught me to pay off my credit card every month and to contribute to my retirement account from the beginning. My mom was always the financially savvy person in my family and there was a lot she didn’t know or teach me.

When I had saved my first $10,000 in 2013, I didn’t know what to do with it, and I contacted some financial advisors. I decided to not do anything with it and just save it until I could figure out what to do next. I saved it instead before I really had a concept of a dedicated emergency fund.

I think understanding personal finance really clicked around 2019 when I started learning about finances in more detail. I was around 33.

Again, I was always a saver, but I was not actively saving or investing with any sort of strategy until this time.

Who inspired you to excel in life? Who are your heroes?

My parents always believed in me and supported me.

I am grateful to them for all that they have done for me.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

Wallet Activism definitely changed the way I view money and helped me have a desire to use my money for good. I have made some lifestyle changes since reading it, such as not buying meat.

The Color of Money: Black Banks and the Racial Wealth Gap also changed the way I view my privilege and the systems I am part of.

Your Money or Your Life helped me put into perspective the value of what I am spending on and to think through purchases much more to buy back years of my life.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

I volunteer a few hours each week to a national organization. I donate blood every few months.

I try to get involved in local legislation by contributing to policy discussions where I have some expertise. I plan to continue to do these things and increase my volunteering as I have more time.

We recently opened a donor-advised fund, and I hope to grow that more. We donate a significant amount of our money to our church under the principle of the tithe. It is about 10% of our AGI.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

My current plan is 100% to my husband, and my contingent beneficiaries are my children 50/50. I hope to provide for my children in their early adulthood where it can make the most impact.

I am grateful that I was able to receive an inheritance at 30 when it made more of an impact than the inheritance my mom received at 60, so I hope to use the money strategically during their lives.

Thank you for sharing your story! For some of us it took a while to get a handle on stewardship that would better our lives, including finances. I followed the path below and now I’m able to broaden my horizon to engage things I would never have been able to engage (like a private equity investment) had I stayed on the poor stewardship course I was on previously.

(a) I budgeted to know the state of our income, expenses, assets, and debts and used that info to motivate us to curtail unnecessary / unreasonable expenses and spend well under our net income and to seek no cost low cost ways to increase income such as entrepreneurial efforts or temporary second jobs, (b) I used discretionary cash flow to build a reasonable emergency fund, (c) then paid off our non-mortgage debts while putting at least 10% of our gross income into no-load low-expense large cap, mid cap, and small cap stock index mutual funds longterm, (d) then paid off our mortgage, (e) all while tithing and giving abundantly to honor the Lord and allow Heavenly windows to be opened over us. This is how I became a millionaire by 48 on a lowly state government public servant salary and retired in 2018 at 55 a multi-millionaire.

It’s good to see you on a faster track than we were and to see you honoring the Lord for blessing your lives! Keep up the good work.

I’m always trying to refine my processes and cut out the excess. I definitely try to incorporate giving into my plans. Thanks for reading!

A great journey so far, millionaire’s in your 30’s while also raising kids! And with a government job on top of that. Sure, you got an inheritance and student loans forgiven, but I like what you said about saving.

Also, didn’t know contractors fluctuated that much, and I can see how having a food allergy inadvertently helps reduce food costs!

Love that you are actively volunteering in your community and want to be involved in local politics. That’s important for us millennials to learn and do.

Thanks for your kind words! I’ve definitely been fortunate and I don’t take that for granted.

I’d love for people to get fired up about restoration companies because they all quoted us $8000 that we ended up doing the work for $500. That saved us a ton. Then we had one contractor tell us that we needed to dig out our entire foundation and redo the entire thing since our home was built in the 1880s and it wasn’t the standard foundation we have today. Turns out they have patented some beam technology that they wanted to put in our basement that no one else was remotely talking about. It was a challenging several months to figure out our best plans moving forward. We ended up using 2 different companies – one for the mitigation, and one for the rebuild. I learned to be patient and to keep calling more companies!