Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in August.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I am 52 years old and my wife is 45.

We have been married for 17 years.

Do you have kids/family (if so, how old are they)?

We have 4 children – a 14-year-old daughter, an 11-year-old son, a 7-year-old daughter, and a 2-year-old daughter.

What area of the country do you live in (and urban or rural)?

We live in the suburbs of Chicago. Our neighborhood lies within a nature conservancy.

It’s amazing because looking out of our back windows, you would think we live alone in a forest, but we are only a short 15-minute walk from our local downtown and train station to the city.

What is your current net worth?

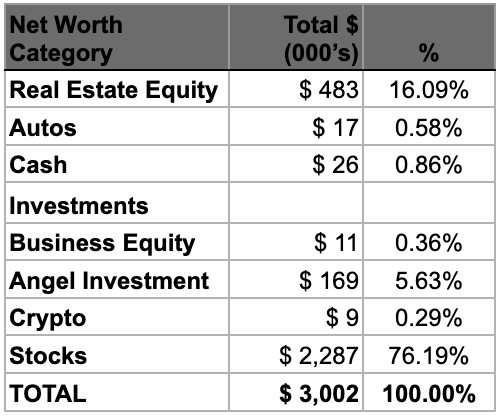

Our net worth is currently just over $3 million.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

Our net worth is broken down into the following categories:

For real estate, the equity is in our primary home, which is currently valued at $1.06 million with $580k of mortgage debt outstanding at 3.125%. Although I would love to be debt-free, we are in no hurry to pay off the house, given the interest rate.

Our autos include a 16-year-old BMW 3 series (bought used for cash 12 years ago) and a 10-year-old Honda Odyssey (bought new and paid off within 3 years). The kids are hard on them, so there is no plan to upgrade until they get a bit older.

We are enjoying having a very low % of our net worth tied up in vehicles right now!

Cash is a little low right now. Eventually, we will build this back up to 6 months of expenses in our high-yield savings account.

Business equity is the value of my business (a consulting company with me as the sole employee), which is just the cash that is left if I liquidate and shut it down.

The angel investment started as a single $10k investment in an AI company in 2020. I have been on the advisory board for the company since then and have been granted several additional blocks of stock/options for my service along the way.

The shares have appreciated in price significantly, but I am prepared for this number to go to zero at any time (given the early stage of the company and lack of revenue generation).

Crypto is composed of some free Bitcoin I was granted 11 years ago, plus $3k we invested in a few other coins in 2021. It is a tiny fraction of our net worth by design and something we only keep for observational purposes.

Stocks are broken down as follows:

- $123k in brokerage account split between Shopify (an initial $5k investment many years ago) and VTSAX.

- $1.69 million of VTSAX in tax-deferred accounts.

- $470k of VTSAX in tax-free (Roth) accounts.

EARN

What is your job?

I am the founder and president of my own consulting company, where I provide product management/digital strategy/marketing/sales/operational support to companies of all sizes.

My wife is currently a Salesforce analyst at a global publishing and information company and is about to move into a strategic sales role.

What is your annual income?

Our 2024 income came in at $295k.

$82k of that was my wife’s salary, and the rest was from my consulting business.

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

I don’t have exact numbers for all of this, so I will estimate based on Social Security earnings and other records:

I got my first W2 job as a busboy in my sophomore year of high school. I made approximately $2k a year until I became a waiter my senior year and increased my earnings to $4k.

My undergraduate degree was a co-op program, so I made between $4k and $18k over the next 5 years as I completed my degree (it was a 5-year program). The income I earned offset most of my tuition expenses.

My co-op sponsor hired me as a mechanical engineer in the automotive industry with a salary of $42k in 1996. I worked in several roles, including purchasing, product engineering, process engineering, and quality engineering, over the next 3 years growing my salary to $52k before I left.

In 1999, I felt like trying something new, so I took a 2-year break to get a master’s degree in computer science. I was able to get my tuition waived by working as a teaching assistant the first year and a research assistant the second year.

These roles came with a stipend, so I made a few hundred dollars a month to help with expenses along the way.

During school, I landed an internship at an investment bank in New York in the summer of 2000, where I made $10k.

This led to a full-time role at the bank starting in 2001 at $60k. Over the next 11 years, I worked myself up to a VP level by performing a variety of technology and operational roles in derivative trading businesses, peaking around $200k in 2011 and ending around $150k in 2012 (partial year).

I spent the last 2 years getting an Executive MBA on nights + weekends.

The experience of gaining my MBA prompted me to start a consulting business in 2013. The original plan was to join my best friend in launching a new consulting firm in Minnesota.

Long story short, I ended up going it alone after I got there (more on this later). My take-home income after expenses ranged from $42k the first year (very challenging to find work when I was starting out and didn’t know anybody) to $250k.

There are years in there where I made zero (choosing to stay home during the first year after my fourth child was born) and plenty in the middle where I only worked part-time (sometimes by choice, sometimes not).

From 2015 to 2017, I was hired to run a business unit at one of my clients. I made between $170k to $250k as an employee during those years before returning to consulting in 2018.

My wife has held a variety of jobs over the years and left the workforce in 2011 as an account manager, making around $70k. She went back to work 2.5 years ago as a Salesforce analyst and is currently making $84k.

What tips do you have for others who want to grow their career-related income?

Focus on working smart while working hard, be open-minded to new experiences you may not have been looking for, and continually seek out opportunities to learn and grow. Stay hungry and be humble along the way.

Despite regular “advice” to the contrary, I have reinvented myself multiple times – starting as a mechanical engineer in the auto industry, moving into a technical role in finance, and then pivoting into a consulting role in marketing (that leans heavily on my tech experience).

I have always pursued work that I find interesting. You don’t have to make a ton of money to win (although that is a great option if it happens for you).

I have had ups and downs and numerous blocks of time off. If you prepare to weather these storms ahead of time and live a reasonable lifestyle along the way, things will work out in the end.

What’s your work-life balance look like?

My work-life balance is and has always been great. Aside from a 6-month stint early in my banking career where I worked 12-hour days for 6 months straight, I have pretty much always kept to 8 hours a day.

I was able to make this work by always being hyper-efficient and effective during the time I spent at work.

Once I started consulting, things shifted considerably, with numerous spells of no work at all balanced out with times where demand was high and I was working constantly. I love the variety between working hard on interesting problems and having lots of time for self-improvement, learning, family, and meeting new professional contacts.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

We have no significant sources of income outside of our careers.

SAVE

What is your annual spending?

Our annual spending is tracking toward $185k for 2025, which is the highest it has ever been. We consciously increased our baseline by moving to a more expensive area and doubling the size of our home in 2022.

Add inflation and childcare (now that my wife works full-time) to the mix, and the numbers are somewhat shocking compared to our $90-100k of annual expenses before moving.

What are the main categories (expenses) this spending breaks into?

Our annual spending breaks down into the following buckets:

- Giving: $4k

- Tax Payments: $17k

- Housing: $61k ($32k mortgage, $2k insurance, $1.5k HOA, the rest on utilities, repairs, and maintenance)

- Transportation: $7k

- Food: $37k ($7k eating out, the rest on high-quality, organic, minimally processed food)

- Medical $5k

- Personal: $19k (mostly optional expenses, such as kid activities, hobbies, entertainment, learning, clothing, etc.)

- Child Care: $22k (nanny, summer camps)

- Miscellaneous: $6k

- Non-Recurring: $7k (vacation, home furnishing, and home improvements)

Do you have a budget? If so, how do you implement it?

I have never been a budgeter until the last 10 years or so (although my wife was a budgeter until we got together). Prior to that, I always made enough money to save some and still do whatever I wanted.

In 2015, I came across an article on Get Rich Slowly about tracking your net worth and other key financial metrics. This prompted me to build a custom spreadsheet to track and manage our income, expenses, investments, and net worth on a quarterly basis.

I would share the results with my wife periodically. By 2017, I fell into the FIRE rabbit hole and could see that we should be doing much better, so we went into a hardcore debt elimination mindset and started using EveryDollar to manage our spending.

My wife was very supportive but happy to let me manage the tracking and details. We switched to YNAB in 2021 for its more robust feature set and continue to use it to monitor our expenses.

I typically connect with my wife at the end of each month to review where the money went, how that compared to the plan, outlook for the next month, etc.

What percentage of your gross income do you save and how has that changed over time?

We are currently saving 14% of our income. Over the last 10 years, we have averaged 23%, with a high of 62% and a low of 0% (driven by taking a year off and choosing to prioritize moving / renovation expenses).

Prior to that, I would say I consistently saved 5-15% via 401k plans while working in full-time roles.

What’s your best tip for saving (accumulating) money?

Leverage your employer’s retirement plans to save so you never get used to seeing that money. I’m a huge fan of simplicity and highly recommend a “set it and forget it” approach.

It also helps to avoid consumer debt. It was hard to save a large percent of our income when a bunch of our cash flow was tied up in school loans and car loans during the few years we carried them.

Wipe that stuff out if you have it!

What’s your best tip for spending less money?

Find a “why” that matters to you and use it to influence your behavior. I have always been very focused on spending along the way and enjoying life while still saving for the future.

That approach worked great until we started a family, prioritized my wife staying home with the kids, and started my consulting business all at the same time.

Without really noticing it, we started to get comfortable with carrying consumer debt (student loans, auto loan) to make it all work. It wasn’t until I discovered the concept of FI that I became aware of our complacency and took action to get back on track.

It suddenly became clear to me that I wanted us to have the freedom to 1) handle the unexpected twists and turns life throws our way and 2) be able to do whatever we wanted within a few short years.

What is your favorite thing to spend money on/your secret splurge?

In general, if I buy something, I tend to get something nice that lasts. My favorite things to spend money on right now is our house and family experiences.

The kids are only going to be under our roof for so long, so I want to really enjoy the time we have together. We plan on staying in this house for the rest of my life, so I am happy to spend money on nice upgrades that I know we will enjoy for many years.

INVEST

What is your investment philosophy/plan?

Simplicity wins the day. We are comfortable taking risk, have a long-term mindset, and believe in the strength of the American economy.

As such, we direct our investments to a US Total Stock Market fund (VTSAX) and leave it alone.

We do have a single angel investment in an AI company and have flirted with VC, PE, other angel deals, real estate syndications, etc. many times over the last decade. Evaluating each of these alternative investments takes a significant amount of time and involves giving up control/trusting someone else to manage our money.

With the blessing of hindsight (and much wisdom gained from the Millionaire Money Mentors forum), I am glad that I passed on every one of these “opportunities”. I believe I am better off saving my energy for my kids while I still have them here at home than chasing performance.

What has been your best investment?

My best investments have been in myself (taking time off for my Masters and my MBA, starting my own consulting business) and marrying my wife.

Without a solid base, it would be hard to generate meaningful returns.

What has been your worst investment?

When I was younger, I chased performance too often. For example, I directed my 401k contributions to tech right before the .com bubble, transferred my 401k into health care and other sector funds that “made sense” at the time, etc.

These moves all turned out to be misses and caused me to lag the performance of the overall market. I also tried an actively managed brokerage account right before the global financial crisis.

Why I paid someone else to put me in a bunch of high-fee mutual funds is beyond me. The most painful part was that I eventually got so angry that I pulled this specific money out of the market for a year or so.

I did end up using it to pay for my MBA, but I missed out on ~30% gains during that time. Ouch.

What’s been your overall return?

For the last 10 years, our investments have averaged 17.5% per year.

Prior to that, I expect we lagged the S&P by a few percent due to the unforced errors described above.

How often do you monitor/review your portfolio?

I formally review and track our portfolio every month. My wife and I will then discuss results and trends and make any adjustments to our cash flow allocation that we deem appropriate.

It’s not unusual for me to run a quick net worth update a few times a month to keep an eye on things between the formal reviews as well.

NET WORTH

How did you accumulate your net worth?

Our net worth is a direct result of working, saving, and investing consistently.

- In our first phase of net worth growth (1996-2016), we always invested something, but it wasn’t a lot (5-15%).

- Our second phase of net worth growth came after discovering FIRE (and ESI Money) in the middle of 2017. When I started tracking our net worth in 2015, it came in at $500k with $90k of school loans, $24k of auto loans, and a $230k mortgage. We started budgeting and attacking debt in mid-2017, and by October of 2018, we hit $1 million net worth, and only the mortgage remained. By July of 2021, we hit $2 million net worth and had $30k left on the mortgage. On top of the debt paydown, we were also maxing out my solo 401k and doing backdoor Roths.

- The third phase began when we were about to pay off our house in Minnesota, but instead decided to move to a larger home closer to family in Illinois. This move has slowed down our net worth growth while increasing our quality of life. In the end, I believe the tradeoff has been worth it.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

They all go together, but I would say I started strong in earnings, have done a decent job of saving, and feel strongest about investing since our investments are now doing the heavy lifting. I will also say that I don’t think we have stood out or excelled in any of the three buckets.

If we can get this far, making mistakes and enjoying life along the way, then you can too.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

In the mid-1990s, I remember reading “The Millionaire Next Door” and “Rich Dad, Poor Dad” and thinking – “Wow, that makes sense” but not doing much about it besides prioritizing a basic level of saving. At the time, I was buying new cars every few years (for cash) because the employee discount made it a “no brainer” and it was the culture.

I did fine selling my vehicles when I was done with them, but redirecting some of those dollars to savings and letting them compound would have given us an additional boost.

After moving to New York, I was able to ditch cars altogether, but thoroughly enjoyed the city lifestyle by eating out 2-3 times a day and constantly going out with friends. It was a blast, and I (mostly) don’t regret it, but there was a missed opportunity to save a bit more during those years.

I also divorced my first wife a few years after moving to New York. The process was very difficult, felt like a massive setback, and cost $25-30k, which seemed like a lot at the time.

In retrospect, there was very little impact on my trajectory, and I ended up much better off after finding my current wife.

In 2011 and 2012, I was enrolled in an Executive MBA program. My employer wouldn’t sponsor me at the time, and I didn’t feel like waiting another year to see if they changed their mind, so I paid for it myself.

This put me in a situation where everyone knew I was going to do something else when I graduated, which resulted in my role being eliminated in the middle of 2012. Even though I was expecting the layoff, it was extremely painful after spending so many years at the firm and working with so many excellent colleagues.

The career team at my business school told me that I should expect to be laid off at least 3 times over my career. That perspective helped me process the transition, but it still wasn’t fun.

I was then asked to move to Minnesota to partner on starting a consulting business with my best friend. This plan was based on a verbal agreement, and with a known opportunity in front of us.

It was absolutely devastating to then have him back out of our verbal agreement and pursue the opportunity himself AFTER I moved my family halfway across the country. I knew it was a bad idea to not have something in writing but I figured he was the one person I could trust.

In the end, I lost someone important to me and learned a hard lesson.

What are you currently doing to maintain/grow your net worth?

We are blessed enough to have reached a point where the net worth is largely taking care of itself.

My wife plans to work for some time, and I will continue working as interesting opportunities pop up to help cover expenses and support optional spending (home upgrades, vehicles, vacations) until we get closer to the finish line.

Do you have a target net worth you are trying to attain?

$5 million is the current target.

Before moving to our new home in 2022, we were targeting $2 to $2.5 million.

How old were you when you made your first million and have you had any significant behavior shifts since then?

I was 45 when we crossed the $1 million threshold in October of 2018. At the time, we were deep into the debt paydown and high savings phase described above.

The $2 million threshold came when I was 48 in July of 2021, after lots of hard work. By that point, I was thrilled to be close to FI and about to make work 100% optional.

Instead, we made the move to Illinois to be close to family and increase the enjoyment we would get out of our home while our kids are still with us. We just crossed the $3 million mark at our new, slower pace in August 2025.

What personal habits and/or traits have you developed that have made you successful at growing your net worth?

I enjoy monitoring our expenses to make sure they are bringing value/enjoyment. We only buy things that we can pay cash for (including a couple of significant home upgrades).

One theme of my journey that is a little different than others is that I have never been afraid to spend and enjoy life along the way. I sometimes wish I had been a little more disciplined, so I would be better off now – but then remind myself that it is hindsight bias.

I have truly enjoyed the journey so far, have had many wonderful experiences with friends and loved ones, have rarely worried about money, and yet still ended up in pretty good shape. I’m not sure I would change much if given the chance for a do-over.

There is no right or wrong answer here – only tradeoffs!

What money mistakes have you made along the way that others can learn from?

Plenty, as outlined in answers above (buying new cars when I didn’t need them, chasing stock/sector performance, investing in a “managed” account, moving and starting a business based on a verbal agreement, etc.)

What advice do you have for ESI Money readers on how to become wealthy?

Find something that you are good at and get some enjoyment out of that people value and run after it. Avoid consumer debt.

Only buy what you can pay cash for (besides your home). Simplicity wins the day.

Enjoy life along the way (not all wealth is financial).

FUTURE

What are your plans for the future regarding lifestyle?

Our net worth has already allowed me the space to not need to work constantly, so I feel like I have a lot of freedom in my lifestyle already.

I will likely be done working altogether in 4-6 years.

What are your retirement plans?

Once I quit working, I will shift into running the household and being more physically active (platform tennis, golf, walking, hiking, strength training, etc.). I used to play in a lot of bands when I was younger, so I also plan to get back into playing guitar and bass while also learning to drum.

Finally, I can see myself getting more involved in the local community (park district board, local history museums, other community events, etc.). I’d also love to take trips to other states to visit friends and family more often.

I’m sure my wife and I will also get back into traveling the world more at some point as well, although I am so happy with where I am at that I don’t feel it is necessarily a priority – just a nice to have.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

Health care costs and navigating Medicare will be challenges, but are not things that I worry about right now. My life is so full at the moment that I will dig into these issues a few years before retiring.

Given the fact that we had 4 children late in our lives, college will also be an issue as it will overlap retirement (I will be 68 when the youngest heads to college). As of right now, our mindset is to take care of ourselves and our retirement first.

We will help the kids analyze and understand the ROI of whatever path they are pursuing, steer them towards work and scholarships to self-fund as much as possible along the way, and most likely provide some light financial assistance as well. They will each be on the hook for funding tuition themselves (no co-signing or parent loans).

We feel this approach has the benefit of giving each child a real incentive and opportunity to be smart about the expenses that they are taking on. We can then help them pay down any debt they may take on when it is easier for us and they have successfully proven to themselves that they can pull off big achievements in a responsible manner.

That’s the current plan – but we will see where life takes us!

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

I learned about finances by reading books like “The Millionaire Next Door” and “Rich Dad, Poor Dad” in the 1990’s. These books got me started with a base level of saving and made me aware that I was playing a long game.

It wasn’t really until 2017 when I discovered FI that things truly clicked for me / I did the math to see where I was headed and how I could accelerate progress.

We were about to have our third child at the time, and I think the combination of wanting to set our kids up for success and seeing how much work it took to get my consulting business up and running made me aware that things might not always be “easy” for us and we needed to be more aggressive in our approach.

Who inspired you to excel in life? Who are your heroes?

I have always admired my father for staying true to himself and starting his own business (a barber shop) when I was a small child. He is the kind of guy who needs to do things his own way, and he quickly figured out that he would be better off working for himself.

I am like him in that regard, even though it took me 17 years to exit corporate life and start my own consulting business.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

My favorite money books to recommend are:

- “A Simple Path to Wealth” by JL Collins. I have given this to several people because it is an easy blueprint to follow to get them started investing and show them that “average performance wins the day”.

- “Your Money or Your Life” by Vicki Robin. Many people I know are always chasing more because it is so ingrained in our culture. Life is more than the endless pursuit of “success,” and this book really resonated with my personal values. I read it around the time that FI clicked for me and found the concept of trading life energy for money to be very powerful. I wish I had found this book much, much earlier!

- “The Millionaire Next Door” by Stanley and Danko. This book gives the classic template and overview on how to build wealth. It got me started and is timeless advice that I would recommend for anyone.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

My wife and I give a small amount to our church every month and work with our kids to allocate money to several charities at the end of the year. We also started an annual process 7-8 years ago with the kids, so they learn the importance of giving back and get to enjoy the feeling of making an impact.

We set aside a percent of each child’s allowance every week throughout the year to build up their “giving funds”. At the end of the year, everyone can choose to allocate their funds as they see fit.

I don’t remember where we first heard about this method, but I would highly recommend it, as it always leads to great conversations as we discuss where we are each donating for the year and why

We have consistently given 1-2% of our income a year to charities. Once our financial future is secured, our plan is to start a Donor Advised Fund and ramp the giving up.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

If my wife and I were to die today, our assets would go into a trust to care for our children. Each child will receive an equal share of whatever we have and will have the ability to access 1/3 of the balance at 25, 2/3 at 30, and the full amount at 35.

Our primary goal was to make sure the kids are taken care of until they can support themselves if something happens to both of us. We landed on the 25/30/35 thresholds as a reasonable solution to just get something in place.

I’m not sure it is perfect, and we may adjust it later if we come up with a better approach.

Our (obvious) preference is for the kids to all be over 35 when we pass, at which point we will have already given gifts to them (and charity) along the way for quite some time.

Finally, we are not planning to talk about our numbers with the kids in advance as we want them to “be hungry” and actively pursue their own success without banking on future windfalls from us.

Thank you for sharing your story with us! I especially loved the investing comment, “Simplicity wins the day. We are comfortable taking risk, have a long-term mindset, and believe in the strength of the American economy.”

If you want the trust to rule over the distribution of your estate upon your deaths, doesn’t everything you want in it have to already be assigned and recorded in it prior to death?

Thank you! Good call out on the trust. I think I didn’t word things as clearly as I should have as some assets are assigned to the trust already and others will transfer on death at our passing.