Today I have an update for you from a previous millionaire interview.

Today I have an update for you from a previous millionaire interview.

I’m letting three years pass from the initial interviews to the updates, so if you’ve been interviewed, I’ll be in touch.

This update was submitted in March.

As usual, my questions are in bold italics and their responses follow…

OVERVIEW

How old are you?

I’m 62 and my wife is 64.

We’ve been married for 35 years.

Do you have kids?

We have no kids, only God-children, nieces, and nephews.

What area of the country do you live in (and urban or rural)?

We live in a mid-size urban area in the Mid-West.

What was your original Millionaire Interview on ESI Money?

Our original ESI Millionaire Interview was 343.

Is there anything else we should know about you?

I am a Christian, who believes in Jesus Christ, and His instructions and guidance on how to live, including scriptures concerning finances.

NET WORTH

What is your current net worth and how is that different than your original interview?

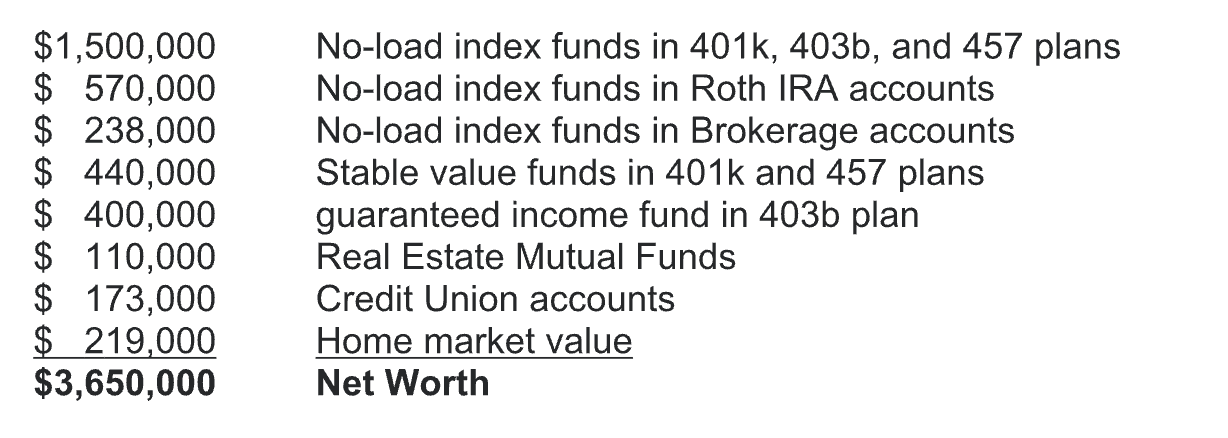

Our current net worth is $3.65 million.

Our net worth at the time of our original interview was $2.8 million.

What happened along the way to make these changes?

Largely good experiences in the sense that we’ve had pretty good returns on our no-load low-expense broad market stock index funds.

We did have a couple of blips. In one situation I put some of our fixed income monies in a no-load low-expense intermediate bond-fund and in one year it went down about $24,000.

We transferred the funds partly to a couple of credit union CD’s that provide four percent return and partly to a brokerage account into a no-load low-expense broad market stock index fund that has had great returns the last few years. These will more than make up for the bond fund loss, even though we know the stock market can have a down year at any time.

Yet, we realize that we have so much money available that we won’t need any of this money for a great number of years into the future.

Our second situation was breaking a CD and paying the penalty to put the money into a syndication deal for a top-notch car wash. I spent lots of time researching the deal and getting guidance on investing in it.

I had the syndicator confirm they bought the property in a great location and were ready to begin building the car wash. Two weeks after I wired the money, the syndicator told the group they weren’t going ahead with the project because of other car washes they understand would be built in the vicinity before they could be up and running.

I got the money back but did lose about $4,000 as a penalty for breaking the CD. This would have been my first deal like this. I was bummed because I thought this was going to be a great investment with great returns.

What are you currently doing to maintain/grow your net worth?

Now, we’re totally back to the concept that got us here in the first place, investing a bulk of our money in no-load low-expense broad market stock index funds and a smaller share in fixed income investments via stable value funds and credit union CD’s.

We are still long-term investors who don’t see a foreseeable need to withdraw from our investments.

But we do sometimes use money from our savings account, money market account, and interest from our certificates of deposit to fund travel each year.

EARN

What is your job?

We both retired seven years ago.

Prior to retirement I was an executive group administrator with the state insurance department.

My wife was a microbiologist with a state university veterinary diagnostic laboratory.

What is your annual income?

Our income is approximately $122,000 made up of $60,000 pension, $54,000 social security income, and $8,000 interest and dividends. We made the choice to take our social security at 62 years of age because our parents died at young ages.

Mine at 63 and 69 and hers at 75 and 81. Our grandparents also died relatively young, early seventies to early eighties and few earlier than that.

Also, our investments will continue to earn far more per long-term annual average than we would get if we delayed taking social security until 67 or 70. We also have everything set up to leave whatever remains of our investments to our church for evangelism and disciple-making ministry and some to our God-children, nieces, and nephews.

How has this changed since your last interview?

We added the $54,000 social security income and the $8,000 interest and dividends.

Have you added, grown, or lost any additional sources of income besides your career?

Yes, we added social security as explained above.

We also must include on our federal, state, and local tax returns interest and dividends from our savings, money market, certificates of deposit, and brokerage accounts.

SAVE

What is your annual spending and how has it changed since your interview?

Inflation has raised our spending a bit, but we’re really simple people with a simple diet, and thus we spend far less than our annual income on our lifestyle. Probably about seventy-percent of it and the other thirty-percent is given to our church and other gospel ministries that also help the needy.

We occasionally use money from our savings account, money market account, and interest from our certificates of deposit to fund our yearly travel and entertainment and for additional charitable donations.

What happened along the way to make these changes?

Well, inflation was pretty bad for a few years during our retirement.

That raised prices for things we usually buy and we’ve greatly increased our charitable donations.

INVEST

What are your current investments and how have they changed over the years?

Sixty-three percent is invested in no-load low-expense broad market stock index mutual funds within 401k, 403b, 457, Roth IRA, and brokerage accounts. Twenty-three percent is invested in stable value and guaranteed income funds in our retirement plans.

Three percent is invested in no-load low-expense real estate mutual funds. Five percent is in credit union accounts.

Six percent represents our home market value.

We have no debt. We paid off our home mortgage 22 years ago, after having a mortgage for 13 years.

By the grace of our Lord Jesus, we plan to remain totally debt-free for the remainder of our lives.

What happened along the way to make these changes?

Largely great returns on our mutual funds and mostly leaving the investments accounts alone.

MISCELLANEOUS

What other financial challenges or opportunities have you faced since your last interview?

The intermediate bond fund, in which we lost $24,000, and the syndicated car wash investment that didn’t work out were our challenges and opportunities.

Overall, what’s better and what’s worse since your last interview?

Our income is twice what it was at our last interview.

Roughly half of that increase was added about two and half years ago and the other part this year.

What are your plans for the future?

We plan to continue tithing and giving about thirty percent of our income to gospel ministry and to help the needy. We take a couple of nice vacations each year, a few lower-cost weekend vacations, and about ten to twelve day trips to Lake Michigan beaches each summer.

We also plan to continue serving in ministry through our local church and other ministries (altar prayer, worship team singing, elder board duties, teaching, intercessory prayer, etc.), and to help others learn bible-based stewardship principles and practices.

Given that you have a bit more wisdom and experience, what advice do you have these days for ESI Money readers?

Continue to read the ESI Millionaire Interviews so they see the habits that many people used to build wealth. While the general principles of good stewardship are what most everyone used to get there, they’ll find everyone does not have to use cookie-cutter processes.

They can be individual and unique letting their personalities and giftings come through as they walk the road to financial freedom and wealth.

Don’t follow and pursue most of the financial advice they hear on social media sites unless and until they find that the principles given have actually been used by a plethora of people to find financial freedom and wealth. For the vast majority of people who want to better themselves there is no substitute for employing good financial stewardship.

Also, as a foundation, time in the stock market is necessary for most people to build wealth instead of trying to time investment markets and using debt as the base for investing.

For diversification purposes I like no-load low-expense broad market stock index funds for a large percentage of my portfolio. Also, I’ve found that good stewardship and having no debt have put us in a situation where we could choose to invest in other arenas like investment real estate, if we wanted, without losing sleep over such investments or putting our financial well-being at risk.

I’m not a financial guru by any means, and there are plenty of other people who have net worths far above ours. However, I’m very happy how life and finances have turned out for us.

It’s pretty good for one who grew up a little ole poor boy in the hood whose family didn’t have two nickels to rub together.

These are the principles we used along the way to get where we are:

- Understand the Lord owns everything and we’re stewards of a portion of His estate.

- Work to be fruitful, produce income, and have cash flow from which you can prosper.

- Be willing to make sacrifices to get where you want to be.

- Be content with what you have while patiently getting the financial education you need to profit and prosper.

- Each person has the power of self-control to stop engaging habits that stop you from getting ahead financially.

- Tithe and give offering to honor the Lord, spread the gospel, and help the needy.

- Eliminate debt – work toward becoming debt-free, which will require controlling expenses to ensure that altogether, they are much less than monthly income, and finding ways to increase income at times so you have more cash flow to pay off debts.

- Refuse to cosign because most people for whom they cosign will never pay the loans, and generally, people (who are not wealthy) who cosign for others are not in a position to cosign without being hurt financially when the other people do not pay the loans.

- Save a reasonable amount of cash flow for emergencies and for other upcoming needs.

- Invest at least ten percent of your gross income in suitable investments like no-load low-expense broad market stock index mutual funds to build wealth from which you can later withdraw for greater giving and living.

- Diversify investments as time goes on. An investment in mutual funds can provide this safety mechanisms and one can add other types of investment like real estate or a business to their portfolio.

The following is the process/steps I used along the way to get where I am and to help others.

- Planned (including tracking and budgeting and completing periodic net worth statements) so we would know the state of our income and expenses, assets and liabilities.

- Engaged in extra income-producing work so I could initially save an emergency reserve fund of at least $1,000 and consistently put enough in our workplace retirement plans to get the employer match.

- Used a hybrid of the debt snowball and avalanche debt elimination methods to pay off all non-mortgage debt as soon as possible.

- Thereafter, we increased our emergency reserve fund to at least $10,000.

- Then we started investing ten percent of our gross income into our workplace retirement plans and maxed out our Roth IRAs every year.

- With remaining cash flow, we put extra principal payments on our home mortgage each month until it was paid off in thirteen years.

- Once our mortgage was eliminated, we greatly increased our charitable donations and savings & investments. We also increased our spending a bit to enjoy more that life has to offer.

We enjoyed some reasonable low-cost treats (dinners, plays, trips, etc.) as we hit milestones along the path to financial freedom and the wealthy place. Much worship including thanksgiving, praise, and prayer, has been offered to the Lord to go along with the above stewardship practices.

I know some people have done things quite different than we did, however I provided this outline because it truly helped us and I’ve been able to use it to help many other people along the way eliminate financial bondage and build far greater wealth than they had when we met.

For those being uniquely themselves who use other strategies, I encourage them to continue to use what truly benefits them. I love reading the millionaire interviews and seeing how they’ve been blessed!

Thank you for sharing your updated details. Congratulations. Your comment, “Be content with what you have while patiently getting the financial education you need to profit and prosper” is so accurate. Be content is a habit many people don’t have and impacts their financial stability and other parts of their life.

Best of luck as you continue to enjoy retirement and continuing in your ministry.

My pleasure sharing the update. Thank you for the best of luck wishes.

Great update. I came across your original interview not too long ago, and then your YT videos and book. Your and your wife’s journey has been an inspiration. Thank you for your example and for continuing to share in multiple ways. I hope you all continue to enjoy this season of your lives for many, many years to come!

Thank you kindly. We’re doing our best to be of value to others.

Hey John. I’d be interested in becoming a mentor in your program. I’ve helped quite a few folks in my life about money and this looks like a good program. I’m not sure where to contact you so I’ll try this forum. Just let me know how I apply if you’re accepting new mentors. Thanks.

See this post:

https://esimoney.com/help-us-reach-500-millionaire-interviews/

Scroll down to where it tells how to become a mentor.

If you need to discuss, you can email me. There’s a “contact” button at the top of every page (in the navigation).

Soli Deo Gloria! Thank you for sharing your journey!

Yes, glory to God alone! It’s my pleasure to serve Him and help others as best I can, even when it’s simply sharing my testimony.