In How I Added Dividend Stocks to My Portfolio, Part 1 Millionaire #140 made this comment:

In How I Added Dividend Stocks to My Portfolio, Part 1 Millionaire #140 made this comment:

I noticed that the vast majority of millionaires do index funds, and for almost a decade now I’ve done nothing but buy individual dividend stocks.

There’s been several times I’ve second guessed the strategy, it’s always hard to go against the herd unless you have an unnatural level of confidence. But my annual dividend income is now up to $277,661, so I must be doing something right.

I think any investing strategy is going to be a double edged sword that has some good factors and some bad. It just depends on what fits your interests, personality and goals. Doing something (anything – as long as you don’t lose money) beats doing nothing.

To which a reader replied as follows:

MI 140, Can you share your story? You and Mike have a monster dividend portfolio. I’ve been doing mostly index funds but also wanting to add some individual dividend stocks as well. Would like to know more.

So I reached out to MI 140 and asked if he could write up something like Seven Steps to Creating Passive Income through Dividend Investing.

And he was very gracious to provide us with the following update.

Hold on to your hats, it’s a doozy!

So without further ado, here’s Millionaire #140…

—————————————————–

Time for an update! Of course, it’s been an interesting couple of months, to say the least. I’ll first talk about the meaty part of the story that some have been asking about, my dividend income and investing.

So, I ended 2019 with $157,200 in dividend income and since 2019 was a great year for the stock market, the value of my stocks saw a nice price appreciation of $514,386 over the year.

Firstly, going into February, I was 100% invested as always. When it comes to dividend income, I am like a crack addict. I can just never keep any cash around. I do keep about a year’s worth of expenses in actual cash as an emergency fund, but I am talking about keeping a meaningful percentage of your portfolio value in cash, such as 10-20% or more. In any market, there just always seems like there is something that looks attractive at the time.

By the end of February, I had built the dividend income up to $192,852.

To recap my original millionaire interview, my annual spending is under $100K, and my goal is to retire at the end of 2020. So at that time, I felt like $200K of dividend income (over twice my annual spending) was a reasonable goal for retirement.

Market Meltdown

And then March came and the coronavirus rolled around. We started seeing some days that were the fastest the stock market had ever dropped in the shortest amount of time. Like, ever in recorded history. Even compared to the great crash in the 1920’s and the great depression. As they say, the bull climbs the stairs, and the bear jumps out the window.

It didn’t take long for all my 2019 gains to disappear. And then it wasn’t long after that until I was looking at well over a million dollars of losses, and then I think at the peak of the low, it was down pretty close to 1.5 million. That is so much money. Years of work, and probably about equal to all the profits I have ever made (including dividends and price appreciation) in the seven years or so that I’ve been seriously investing.

So, at first I did the things you are supposed to do.

I didn’t panic. I realized that stock prices are just what someone else is willing to pay you for your ownership stakes in the company at that exact point in time, which can be far higher or lower than the actual value of those ownership stakes. So I didn’t sell anything.

In fact, I knew that what was going on felt like panic. I knew that in situations of panic, people do things that are not rational. I thought there was a very good chance that people were over reacting. I thought that the prices that stocks were selling at were probably way, way lower than they were actually worth.

I always look at the yield of stocks. The way that most stocks work, is that the dividend rate (the actual amount of money one share of the stock pays out) generally doesn’t change much. The price that a stock sells for in the stock market changes constantly. That affects the yield.

So for instance, if I buy a stock at $100 per share, and it pays $4 in dividends, that stock would have a 4% yield. If the price later falls to $50 per share, now I can “purchase” that same $4 in dividends for $50 instead of $100, so now the yield has gone up to 8% instead of 4%. So I was seeing yields in some areas that had literally not been seen since my great grandmother was a little girl in the great depression. Like 10-15%, sometimes even more than that.

Getting a Margin Loan

This was right before any of the big closures of restaurants and gyms and things like that. Life still seemed normal, and I don’t think I had any idea of what was to come. But I did know at the prices we were seeing, I could not just sit there and do nothing. So I put in an application for what is known as a “margin loan” with Vanguard.

So, how this works is they will loan you money, using your stocks as collateral. The interest rate varies some depending on your outstanding balance, but it’s basically about 5.5%, not great, but not payday loan or high interest credit card type bad either. And, at the time, many of the stocks I wanted to buy had a yield of over 10% in dividends, so I figured collecting 10% while giving back 5% isn’t the most horrible thing.

Within a day or two, Vanguard gets back to me and says they will loan me up to 2.6 million dollars cash. Immediately, that saying about “Enough rope to hang yourself” came to mind.

The main danger with a margin loan, is that the value of the stocks has to stay high enough to cover the value of your loan balance, plus an additional amount of “safety.” It’s similar to how you have to put a certain amount “down” on a house when you buy it (usually 20%) so that the bank feels comfortable loaning you the rest, even though they have the house as collateral. If the value of the stocks falls too low, they can do a “margin call” which means you have to either give them more cash to build up the safety margin, or you have to sell stocks (usually at a rock bottom price of course) to come up with the money. It can be very dangerous and it’s how many people got “Wiped out” during the great depression when the stock market lost 90% of it’s value.

So here’s the thing. I had no money. But I knew I was going to retire at the end of 2020. So I had spent the last six months building up the entire next years inventory in the business. (If you recall from my millionaire interview, I own a mail order business that sells parts for classic cars.)

I did a sales report, and if this year just equaled last year’s sales, I was due for 1.8 million in cash to come in from the business before the end of the year. Just from selling the items that were already sitting there on our shelves. So somehow I came up with a million dollars being an amount that I would be comfortable borrowing on margin.

This would allow for somewhat of a slowdown in sales from the business. And, I would be collecting a bunch more dividends from the stocks that million dollars bought, and I estimated my dividend income would be up to about 280K after I put that million dollars to work. Plus, I figured even if the business burnt down to the ground and I never got another cent out of it, all I would have to do is let the dividend income pay down the margin balance, and it would be automatically paid off in about 3.5 years. ($1,000,000 divided by $280,000 = 3.57.)

In actuality, it would have taken somewhat longer than that because you are paying taxes out of the dividend income, and you also have to pay the interest on the margin debt, but it still wouldn’t have been that much longer.

Anyhow, between about March 12th and March 15th, I bought $1,020,000 in stocks on margin debt. It was a fun few days. It’s amazing how fast you can spend money like that. With just a few mouse clicks I went from not owing anyone in the world a single penny to over SEVEN FIGURES of debt.

Here’s what I bought:

- Cullen Frost Bank: 60K

- Wells Fargo: 100K

- Whirlpool: 60K

- Viacom CBS: 60K

- Unum Group: 100K

- UPS: 60K

- US Bank: 60K

- Simon Property Group: 100K

- Prudential: 100K

- IBM: 60K

- Ameriprise Financial: 60K

- Exxon Mobil: 100K

- 3M: 60K

- Shell: 100K

I had been studying these companies for months, sometimes years. I knew by memory what their financials looked like. You could have covered over any of their names and I would have been able to tell you which company it was just by looking at the financials. So that gave me to confidence to know what to buy, and to spend the money so quickly.

Having Second Thoughts

Then, the market continued to drop, and drop, and drop. I started to think about the margin call thing and how stupid I was, that I could technically lose everything if the market just continued dropping.

There were a couple of nights where I didn’t sleep very well. I started to think about how I could come up with cash in a hurry if I had to. You never want to be in that position. Dumb, dumb, dumb! We now know that the low point of the market (at least so far) was right around March 23rd and then it started to come back. So I was a week or two early.

Stock prices, especially in extreme times, usually go up or down much more than you think they will. Currently, I’d say more than half of my margin buys have gone up nicely, a few are down, and a few are just about the same.

So, as I write this, (May 6th, 2020) I have been putting every spare penny of cash flow from the business into paying down the margin debt. It’s currently at 709K and should be paid off by the end of August. If stock prices stay basically where they are, my portfolio will be worth over 4 million at that point.

Since the virus, we have seen a HUGE increase in the level of business. I guess when people are stuck at home with nothing to do, they get to work on that old project car in the garage, or surf the internet ordering car parts.

Since we are a mail order warehouse and basically not open to the retail public anyway, we have been allowed to stay open and operational. Unfortunately several employees have not been able to work very much due to not having child care since school is cancelled, and other personal issues, so my own workload at the office has greatly increased in order to keep things running smoothly. But I am very grateful we have the sales coming in which will allow me to pay of the margin debt even sooner than I anticipated.

So now I’m thinking I’m sitting pretty, getting ready to collect my 280 grand a year for the rest of my life. I even set my goal to end the year at a nice round 300, since I’ll still have a few more months to buy some more stocks after I pay off the margin debt.

One Problem with Dividend Stocks

And then…Companies started cutting their dividends.

Dividends are not guaranteed. If a company falls on hard times, they may choose to keep more of their money instead of giving it away to shareholders to help them get through hard times.

I had a couple cuts from my lower quality companies, and they reduced my total income by a few thousand dollars which didn’t hurt too much, but then Shell cut their dividend. I had almost 10,000 shares of Shell. That one cut chopped a good chunk of income off. They had not cut the dividend in over 70 years. Hitler was rolling through Italy in tanks last time they cut the dividend. My mom (now in her 70’s) was in diapers last time they cut it. I didn’t expect that. So my current dividend income after all the cuts (up until now at least) is just over 248K. Don’t cry for me, I’ll make it through somehow.

So what have I learned through all this?

First, dividend investing, or any investing where you are buying individual stocks is not easy. It’s not that it’s super complicated, or that you have to be a genius in order to do it (if it was, the higher someone’s IQ was, the greater their net worth would be, and there is absolutely no correlation among these two things), it’s just that there are SO many potential pitfalls that you need to avoid to do it correctly.

The yield should be higher than normal, but not too high or there is the potential for a dividend cut. The earnings and price should be going up, but not too much, because it might be a bubble. Should you sell and take the profit, or would that be a mistake? What if you doubled your money? That would be great, right? What if you sold after your stock doubled and a couple months later it was worth five times as much? Now, looking back, “doubling” your money was actually a huge mistake. That actually happened to me with Tesla stock.

When I first got into classic cars, at 15 years old, I wanted nothing more than to be a super skilled mechanic. I wanted to be able to take a complete car, disassemble it into all of its individual parts, lay them all out on the floor, and then be able to reassemble the entire car again. I not only got to that point, but I actually went even further and got to the point where I could actually design and manufacture many of the parts from scratch.

And then when I got into investing in my mid 30’s, I felt the same way about that also. I studied Warren Buffett and others, and I wanted to master that skill. To be able to spend your time doing anything you please, while endless “mailbox money” constantly shows up automatically in your accounts every month, well that just seemed like a super power to me.

And so for the last 8 years, there has hardly been a day where I haven’t put time into reading, learning and doing, always working on improving my investing skills. And after all those thousands of hours of putting out my absolute, best efforts, I’m not sure I’m any better or worse at investing than a monkey throwing darts at a dartboard. There’s a reason why, over 15 year time periods, 92% of professional investors and fund managers fail to beat the index. And these are the professionals, people that go to the office every day for years and work on their investing for 8 hours or more.

There are strong and valid arguments for index investing. Unless you really enjoy the process of doing investing and have the drive to become great at it, indexing has a likely 90% chance of getting you better results overall (as far as long term total returns), and you’ll get those results with probably 5% of the work and time involved vs. buying individual stocks. So for probably 95% of people, indexing is the better choice.

If you do want to be one of the 5%, the benefits of dividend investing can be significant. For me, to have two hundred to three hundred thousand dollars in cash show up in my account every year for the rest of my life, regardless of what the stock market is doing price wise is a pretty significant benefit. And it’s worth the extra work and probably even the potential (possibly) lower long term total returns.

Dividend Investing Tips

ESI Money asked me for my “secrets.” There really are no secrets.

Just like in most things, there are basic sound principles to follow. Principles that will lay a solid foundation and will build over time, like compound interest. You aren’t going to “get rich quick” or make something out of nothing. You will likely need to purchase assets with money made from your labor, and over time those assets will grow. So if you choose the much harder path of the 5%, here’s the best way I can sum up my 8 years of experience:

Warren Buffett has this saying: “Only when the tide goes out do you discover who has been swimming naked.” The tide is definitely out these days. I think he means that only during periods of stress do you really appreciate those companies that have financial strength and stability. They say the safest dividend is the one that has just been raised. I should have paid more attention to dividend raises instead of just current yields. Shell hadn’t raised the dividend since 2014. That should have been a warning sign. How can you avoid that?

Stick to companies who not only pay a dividend, but raise it every year. Those who have been able to raise it for over 25 years are called the “Dividend aristocrats.” Google it and you’ll find the list of about 63 of them. A lot of things have to go right for a long time for this to happen. Stick to this list. Buy them when the yield is over 4%.

Don’t let any single position get to be over 10% of your total, no matter how much you “love” the company.

Never invest any more than you would be willing to lose in any one thing. History is littered with companies that were the most stable, bluest blue chips that are now shadows of their former selves…GE, Sears, and now Boeing, to name a few.

Probably the best rule you can make for yourself, is that once you buy something, never sell it. If you can’t manage that, at least make a rule to never sell anything at a loss.

One of Buffett’s most famous quotes is “Rule #1 is: “Don’t lose money.” Rule #2, is “See rule #1.” It’s way easier to not lose money if you never sell at a loss. If you stick to only the highest quality companies (dividend aristocrats), purchase them when they are undervalued, and hold them for the rest of your life, I believe this would have the highest possible chances for getting the best possible results from dividend investing.

As I said earlier, it’s not super complicated, but that doesn’t mean that it’s easy. Most people’s temperament and emotions are what gets in the way of initiating and sticking to these simple actions.

Only three possible things can happen in the stock market. When you are a dividend investor, they are all positive:

- The market goes up and your net worth increases and everything you’ve bought is worth more than you paid for it, and you get free new money coming in every month to either live off of or re-invest.

- The market stays the same and you get free new money coming in every month to either live off of or re-invest.

- The market goes down, and all your favorite companies go “on sale”, and you get to acquire ownership of them for less than they are worth. Oh, AND you get free new money coming in every month to either live off of or re-invest.

Sounds like a pretty good deal to me! Thanks for reading my story and I wish you the best of luck out there!

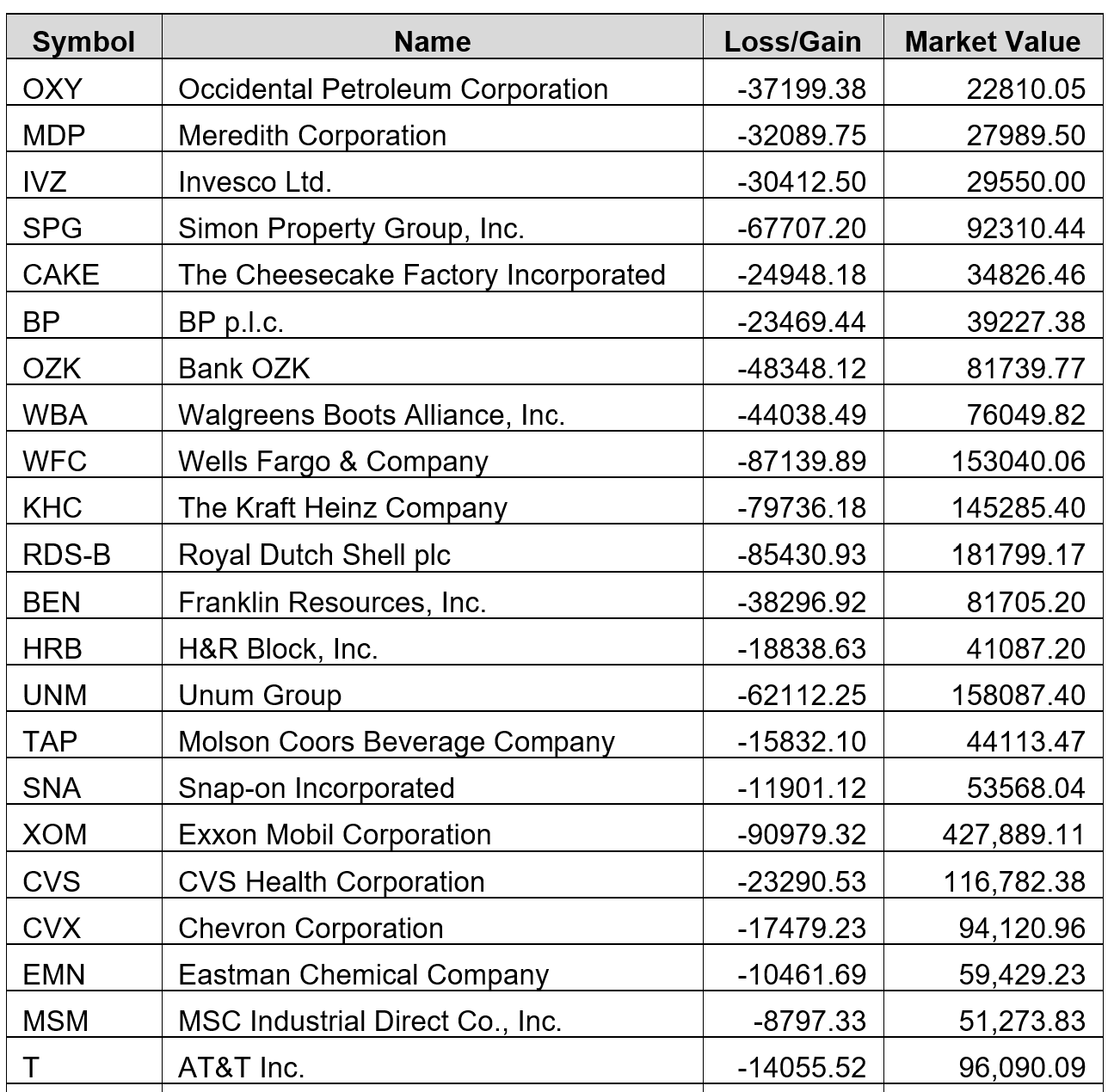

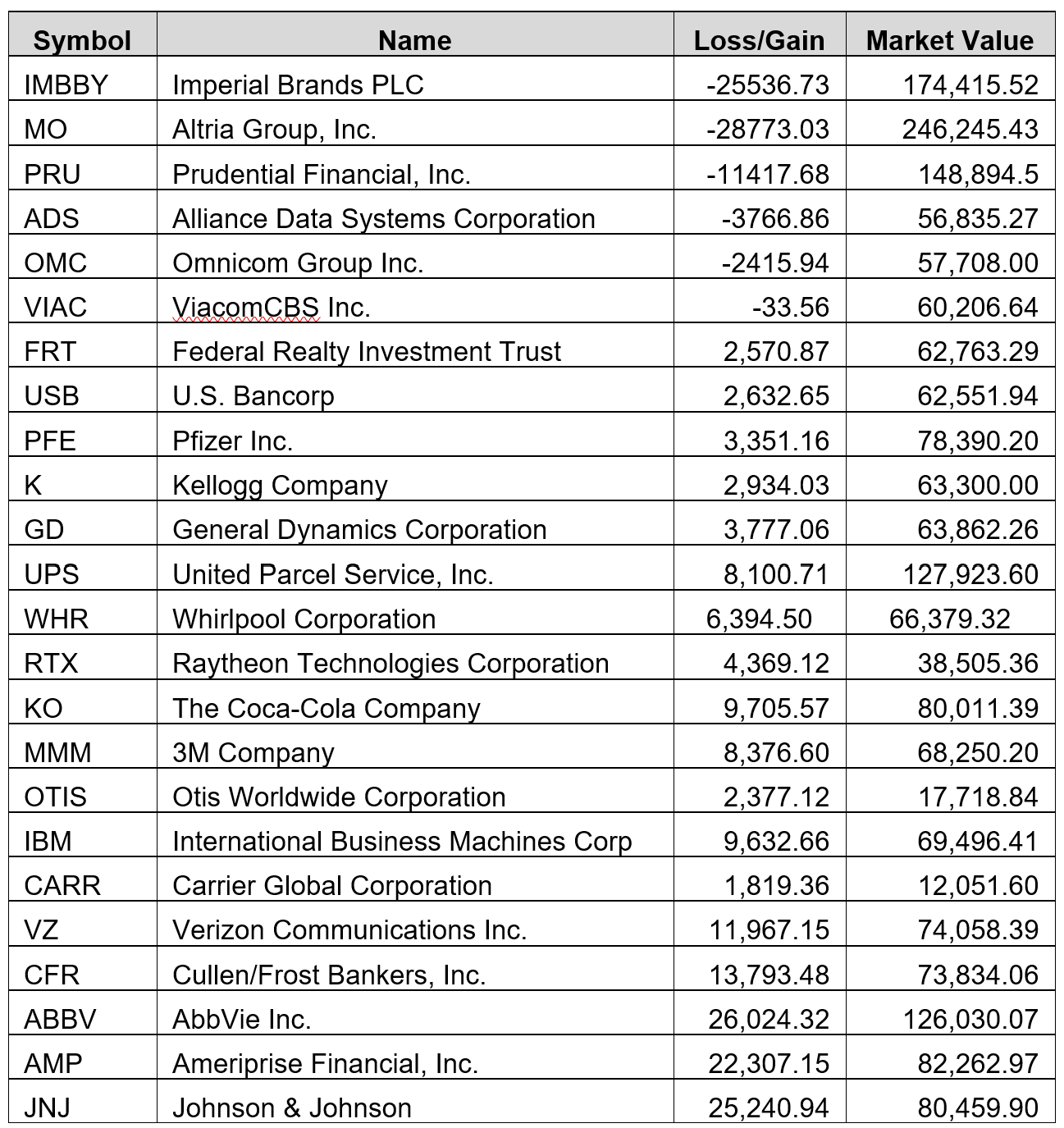

And just in case anyone is interested, here is my portfolio, including my gains and losses on each position as of today.

Of course, that is price movement only, it doesn’t take into account the huge amounts of dividends I’ve collected over the years, which technically offset much of the losses. And the market could hardly be considered “normal” right now.

Is it any better than a monkey throwing darts? You decide.

Hi MI #140,

Thanks for sharing the details behind your investing on margin. Given the strong cash flow of your business you were just pulling forward profits by a year or so. You have some serious cajones there to buy so much on margin.

Given that I don’t have those sources of income there is no way I would buy anything on margin even though I have the credit facilities to do so. Instead I just slowed down my investing rate to what organic cash flow allows. All my consulting work and side hustles have dried up during the lockdowns so psychologically that is challenging. Also I’ve been hit with dividend cuts and suspensions so it looks like I will be fortunate if I break $123k in dividend income for the year. Oh well that’s the way it goes and we just need to play the hand we were dealt.

Like you, I had the chance do a lump sum investment about 2-3 weeks before the market bottom- I had the opportunity to liquidate a bank account Of about $140k and put this to work so the timing wasn’t great but it was better than investing at the peak I suppose.

-Mike H

Superb reading! Thank you for sharing your story.

Looks like you’d have been far better off with the sp500 index then. Lots of oils companies, yeah they’re cutting dividends… As will property. But interesting and good luck!

I have contemplated on investing in dividend stocks instead of regular index before, its very tempting when dividends can easily double, however finally decided to go with index and make up the difference by selling shares, main reason is to control the amount sold up to my desired tax bracket and take advantage of the lower taxes in long term capital gain. Some people may not be used to sell shares as this is considered their capital, but I’ve gotten used to it, the drawback is that sometimes you need to sell in a down market which is not ideal

I do think the main drawback to index investing is that you may be forced to liquidate the principal in order to generate income during a period where the assets are undervalued. We havent really lived though one lately, but if you look at the stock market over the last 100 years, there were several periods where it stayed low for 5-10 years. If we go through that again, it would be the most likely possible “dent in the armor” for index investing.

MI 140,

a question for you, can you elaborate on the below?

“Don’t let any single position get to be over 10% of your total, no matter how much you “love” the company”

Does this mean 10% of your overall portfolio (of all equities individual and funds). For ex, 100k of 1,000,000 is too large a purchase or does it mean from the purchase date, it grows above 10% trim it down to stay at 9.99%?

What about dividends are they reinvested since it would push the amount above 10% or you use these to purchase shares that have declined?

Of the purchase you made in march do you still own them? which do you feel still are worth buying? (for instance, USB and WFC are two you and MI139 both recommended – in the comments below)

They say the safest dividend is the one that has just been raised. I should have paid more attention to dividend raises instead of just current yields. Shell hadn’t raised the dividend since 2014. That should have been a warning sign. How can you avoid that? *how exactly are you checking for this and how often?

thank you

Thats a good question! Generally speaking, I wouldn’t make so big a purchase as to exceed 10% of my total. You hear about all these people that “bet the farm” on some great idea or up and coming company, and end up losing their life savings. Keeping things to a reasonable percentage of the total keeps that from happening. As far as a position growing to be more than 10% AFTER you purchase it, that is a slightly different story. If it grew slowly and organically over a long period of time, it was a large stable company, and the P/E was in a normal range (like say, Johnson and Johnson or Proctor and Gamble or something like that) I would probably just leave it be. If it was Tesla, where you bought it at $180 a share, and two and a half months later it’s at $1000 a share, and the P/E is 987, well, that I would probably sell some and trim it back to where it was less than the 10%.

As far as dividend reinvesting, I don’t do that. I like the dividends to pile up a bit of cash, and then I research what the best deal is, and then buy that. It doesn’t make sense to me to automatically reinvest in something that could have been undervalued when you bought it, but is currently overvalued. I always want to get the best deal out there.

As far as my purchases, I still own pretty much everything. I did sell Cullen Frost towards the end of May in order to buy back Cardinal Health and PPL. Cullen Frost showed a big drop in earnings, and I had about 10K in profit on the position, so I took the money and bought into the other two, both of which have had (and continue to have) very steady earnings thoughout the events we are going through.

I also sold a little bit of CVS, (they haven’t raised the dividend since 2017), I’m using the experience I gained with Shell here and starting to reduce the position. I also sold some Shell and Kraft that I was able to sell at a profit. I am already up to about 90K in capital gains this year, so likely I will take some tax losses later in the year to try and offset my gains. It is my goal to eventually sell all the dividend cutting companies.

The good news is, my business has still been doing really well, and I’ve paid the margin debt down to 329K, so it won’t be too much longer until all of that is ancient history. Good riddance, debt!

As far as what is worth buying still, I do think WFC is still a good buy, but some people are saying they may cut the dividend. I think MO and PM are both still a good buy. I like T, and of course Exxon and Chevron are still at a pretty good price point relative to what they’ve been historically.

And to answer your last question, how I check for past dividend raises and cuts, mostly I use FastGraphs. But there is also a site called Simply Safe Dividends that gives a lot of useful information. Both of those sites charge a subscription fee, but even with free sites like Yahoo Finance you can get almost all of the financial info you would need about a company. And there is a great list that used to be kept up by a man named David Fish. It’s known as the “fish list” if you google it, you can download it, and it is completely free. As far as how often I check, I don’t keep a specific schedule. I do read the financial news, and if a company is in the news for something, I will check up on it, or I just look through things at random as I am researching what to buy and/or sell.

Happy investing!!

Thank you, ill check in every so often as it’s also a great “How i did it” story and learning lesson

I am reading this for the first time. Since May it would be interesting to see how far up your portfolio is now. I own several of the same companies you do, at a lesser amount. I never considered Margin borrowing during a market meltdown, but I will do that during the next meltdown.

I too am a DGI. I bring in about $45K in dividends per year. I (DRIP) reinvest all the dividends back into the stock. Upon retirement, I will stop the DRIP and collect the cash.

I enjoyed reading your story and would love to see how much your portfolio has grown since May…Big time, I am sure. Congratulations!

Hi Glen, thanks for your comment. The portfolio is doing great. $5,396,242 as of this morning actually. And I have paid off 100% of the margin debt, so it’s nice not to anyone any money. When all was said and done, I ended up paying about $10,500 in margin interest to make about 600K in capital gains. I purposely took about 200K in losses as an opportunity to get rid of some of my losers that had cut the dividend (Shell, Wells Fargo, TAP, etc). My dividend income is currently about 260K and my goal had originally been 300K, so I didn’t meet my income goal, but of course nobody suspected the extent of dividend cutting that would happen. Looking back now, the whole thing ended up being pretty lucky, but not something I would probably ever do again. And now that I have a good collection of dividend stocks, I will probably just stick to an index fund like VTSAX in the future, and not count on lightening striking twice. Thanks for reading!

M140,

Thank you for the inspiring story.

How do you diversify your brokers risk. Few years ago MF Global went bust and few other brokers during 2008 crises. How many brokers do you use?

Do you use any from outside USA as well?

Last question what do you do for asset protection? Do you use LLC?

Regards,

Petyo

Good questions, I don’t diversify brokers, I just have Vanguard. They do have insurance that covers investment losses due to fraud or something like that. I figure if the world gets to the point at which Vanguard goes under, at that point my investments will switch to beans and bullets anyway.

I also don’t have an LLC, I just have a normal brokerage account under my name. It’s probably not a bad idea to do an LLC, but then I’m pretty sure you have a file a separate tax return for the LLC every year, and you have to do the minutes and all of that. It’s an extra expense and complication that just seems like too much trouble right now. If I’m lucky enough to make it to the 8 figure club in the future, maybe I’ll start looking at doing those kind of things. I do have umbrella insurance, hopefully that would help in an asset protection situation. Thanks and good luck!

Another consideration that is also impacting the market demand and stock prices as we know them are some changes with the institutional investors who manage 401k accounts.

Many companies during this crisis have cut the 401k matching funds for employee accounts, so the amount of money that is regularly available to invest has also been cut. This equals less buying demand for some stocks that make up those portfolios, many of which are historical dividend paying stocks like those in your portfolio.

Just when you think you have this all figured out, the wind of change comes down through the valley.

A wise man once said “Risk is what is left over, after you have thought of everything else”

Margin debt is an attractive strategy but that leverage runs both ways. I have a relative that pursues a yield-chasing strategy (stocks in the 8% to 20% yield) AND does this on margin. His investment portfolio was values at a little over $5 million in January 2020. Today it’s worth $1.25 million. Amazingly he’s re-upping on the same strategy. This seems like gambling to me not investing. I guess I can understand margin on blue chips but as your example demonstrated, even Shell isn’t 100% safe during turbulent times. I doubt that I will ever use margin debt to fund investments.

I definitely don’t recommend using margin debt. Hopefully nobody comes away from reading this post thinking that. As one of the comments above said, I was basically “pulling forward” less than a years worth of profits from the business. At the time, I had no idea how much of a possibility it was that those profits could disappear. As it happened, I got lucky and business profits actually increased, but it could have easily gone the other direction. Thanks for reading!

Would you try to take out a margin loan now end of May (yields on REITs for example are still high 5-8%) and invest in dividend funds?

When do you decide to sell a stock?

Does anyone consider BDCs (business development companies) for income? Many of these BDCs are yielding 10% to 13% at current share prices.

Some examples are ORCC, GSBD but there are many more.

I am thinking of putting 10% of overall portfolio in BDCs for income during retirement. Bonds seem overinflated with little yield.

I would just be cautious about the losses they’ll be likely to take in a recession.

You do have to be careful as the most BDCs have declining NAVs so your dividend in those cases include a return on & of your initial investment. You need to look at the credit underwriting record of management & fees which can be high.

Packer

Are you concerned that the favored tax status of dividend income may change in the fixture? After the November election?

Over time, taxes are going to go up and down. Of course, I like to keep as much of my money as possible, which means paying as few taxes as legally possible. But changes in the tax code are one of those things that are outside of your control, so it’s better in life to focus on the things which you can control. Since my dividend income is 200-300% of my living expenses, any possible tax increases don’t keep me up at night, but it is something I would consider in my overall long term plan if the situation changed. Especially if it changed drastically. But we have a lot of older folks who are, directly or indirectly, deriving much of their income from dividends, and they are a large percentage of the voting population, so I doubt we will see drastic changes in this area for a while.

That is very possible but if it happens it will be applied to both qualified dividends and capital gains. They are currently treated exactly the same and any attempt to raise one will almost certainly be applied to both. That would mean that index investing or any other form of investing would suffer the same tax penalty that dividend investing would from such a change.

Taxes are going up. I have been saying this for years. I don’t know when exactly but 20 years from now taxes are going to be higher. What are the most likely tax increases that are coming. Below are 9 that I see as things to watch out for. I would say I am listing these in an order where I think the more likely ones are listed first although I certainly wouldn’t say this is an exact order of likelihood. There are other minor things like carried interest etc that are so arcane that I am not even going to get into the likelihood of some of those things changing. Certainly there will be other odd aspects of the tax code that change but these are the types of things that are more generally applicable.

1. Corporate tax rate which was cut from 35% to 21% is going back up. Zero chance this stays at 21%. It probably won’t go back to 35% but it is going to go up.

2. Top tax brackets are going higher The current top tax bracket at 37% is going to be raised likely back up to the 39.6% that it has been at multiple times since the 90s, perhaps even higher. Possibly there will be an even higher tax bracket added for incomes in the millionaire range.

3. Social security taxes get applied to more income. Currently wage income is subject to social security taxes up to 137,700 and is raised every year. Likely this cap gets drastically increased or removed entirely where Social Security taxes are applied to all wage income.

4. Estate tax exemptions getting lowered allowing many who escape estate taxes on estates worth up to 20 million currently will likely be lowered to a considerably smaller estate value.

5. Stepped up basis on capital assets gets eliminated. For those who don’t know about this, stepped up basis means that if you have a greatly appreciated asset you can hold it until you die. When your heirs inherit it and sell it their basis in the asset gets “stepped up” to the value at the time they inherited it. That means if you had sold it they day before you die you would have owed significant capital gains taxes but if your heirs sell it the day after you die they would owe zero capital gains taxes. This is a brought up for repeal repeatedly. It will be more subject to getting rolled back now than it has been in a long time.

6. Capital gains tax breaks for long term capital gains will be reduced bringing capital and investing gains to tax rates closer to normal income rates. This would likely apply to both capital gains and qualified dividends.

7. National VAT (Value Added Tax) on all goods. Most all European nations have these taxes. They act as a hidden national sales tax and everyone pays them at the point of sale without realizing it because contrary to an actual sales tax, all the producers pay them at the points of production so the tax gets added to the price of the products sold to cover the producer’s cost of the tax.

8. Social security taxes get applied to all income not just wage income. This has already been done for medicare taxes with what has been called the Obamacare Tax on all income over 250K even if it is not wage income. Its the first time in history that any FICA tax was applied to non-wage income. I see it as the camel’s nose under the tent. Eventually the whole camel usually comes into the tent. (This would hurt passive income drastically. This would be a huge tax increase on rental income, interest income, dividend income, and investing capital gains.)

9. Elimination of 1031 tax exchanges which allow like property to be exchanged for other like property without paying any capital gains taxes on the exchange. This is usually done with real estate assets. This is also brought up for repeal repeatedly. There is a greater risk of that succeeding now than in a long time.

Another huge benefit of real estate investing is depreciation where you get to deduct the cost of the depreciable portion of your investment from taxes. This is a benefit all business use on their buildings and equipment actually. I see very little chance of this getting repealed. This is a real cost that businesses have and repealing it would crush many businesses. Real estate investors get a greater benefit because their depreciable assets actually tend to appreciate so they get to deduct the cost and actually gain value. Most depreciable assets like equipment are worth close to zero after the end of their useful life so not being able to deduct those costs would make business completely unprofitable as in they would owe more taxes than the income they can generate. Real estate is a bit unique in that aspect so depreciation cannot go away.

I agree many of those taxes could go up. The only one that I think is probably quite unlikely to pass is the VAT tax. America is not Europe. A large part of our population has certain strong feelings about specific things like VAT taxes and gun ownership and other things, wheras you don’t see those type of feelings in Europe. In any case, focusing your energy on things over which you have no control over generally ends up being a poor use of that energy.

Great read. Thanks so much

This is great. I was resigned to believing I was the only one on the planet that doesn’t rely on index fund investing. Dividend investing appears to have it’s benefits.

I’ve done things a bit differently as well. I went with sector funds rather than index funds. Started my career at 27, currently I’m midway to my full retirement age of 67. To date, I have all my market investments in tax advantaged accounts (IRA, 401(k), HSA) which of course is limited by annual contribution limits and all dividends are reinvested, so it’s not really conducive to dividend investing. It has been criticized since sector funds have higher fund fees, but I’ve managed to get to currently about $2,300,000 in my advantaged retirement accounts at age 47, after the COVID hit. I have no reference but I think it’s pretty good. If it doubles twice by retirement, I’d be looking at close to 8 figures there.

Regarding dividends, my real estate is spitting out almost $400K/year, let’s say 25% of that goes to overhead. One can actually call our income (including pass thru) from our business as a dividend by the business, as the business also requires monetary investment – that’s big for me, just under 7 figures annually.

Just paid off my office building, so I’ll have a free cash flow after taxes and expenses now of $800K annually. Trying to figure out how to invest it. Index fund, sector fund, dividend, more RE, business expansion, etc. MI 140’s dividend numbers are impressive, so it gives me something to think about.

This was so useful, MI 140! Thank you for your post. I’m still relatively new to investing and so far have invested largely in index funds, especially those providing very broad exposure (total us market, s&p 500, etc). But for whatever reason, your dividend strategy just makes more sense to me; I like the idea of focusing on income rather than (just) numbers on personal capital. I have an embarrassingly naive question for you. Although I see that you’re invested in a fair number of companies, there really aren’t all that many as far as I can tell. So what happens if several go out of business or cut their dividends substantially? I understand that you buy and hold forever, so should that occur, how is your yearly dividend income safe? Do you have a strategy for replacing poorly performing (or closed) companies in order to try to insure your 250-300K planned income? Thanks for such an enlightening post. Makes me wonder if you should do some blogging yourself once you retire! You write so cogently. 🙂

Thank you! Sticking to the aristocrats list keeps the probability of selecting companies that may go out of business (or cut the dividend) as low as possible. Many people make a rule that they will sell any company that cuts the dividend. Even though you might have to take a loss on the one position doing that, if you keep any individual holding less than 5-10% of the total, and you stick to the list (which is the top 60 out of 5000 total companies) your winners will be very likely to far outweigh your losers.

I wrote a few blog posts as a relatively new investor back in 2014, and a bunch of people stole them and reposted them as their own. I’m flattered that people thought it was good enough to steal. It seems in order to be successful at blogging (and to monetize it) you have to be constantly posting new content, which is a lot of work, as I’m sure ESI Money can attest to! So, I gave up on it pretty quickly and decided my efforts were better focused on running my company and focusing on the income from that, and how to invest that income. Who knows, after retirement maybe I’ll try to put everything i’ve learned into writing a book or something. Or maybe youtube. I’ve been watching Andrei Jikh lately, he’s a dividend growth investor on youtube. Once you build up a decent following, you can make really good money. He made over 6 figures last year just from his youtube videos. If you have a passion for something, figure out a way to share that passion with the world! Do that, and the money will automatically find it’s way to you.

In case you want to read the blog posts I wrote, the internet archive captured them here:

https://web.archive.org/web/20141229213405/http://dividenddad.com/

MI 140: Thank you for sharing so many details on your strategy. You certainly have courage. My husband wanted to take some of our cash and buy additional individual stocks as the market was plummeting. I requested that we wait since I am concerned about the balance of the year as companies continue to report earnings. We own quite a few of the stocks that you mentioned plus have bought some of the Dividend Aristocrats over the years. We are retired and pay estimated taxes quarterly to pay for the dividends that we receive each year. Good luck as your plan your retirement for this year.

APEX: interesting list of potential areas to increase taxes.

Go big or go home! I don’t have stomach as strong as MI140 but I hope his gambles pay off. As for me:

– I’ve considered dipping into a margin account after I blow all my dry powder but the market needs to drop much more (say 50% from all time highs) before I’d blow all my dry powder and start thinking about margin.

– If I were to do this, I’d go with Interactive Brokers with current rates at 1.55% for $25k of borrowing. Maybe it’s a small consolation during big swings but I’ll take whatever risk free differentials I can get.

– Rather than risk my life savings, I give myself “play money” of around $300k to gamble in the market on individual stocks, sectors and regions. It’s enough to keep me interested in the game but not so much that if I lose it all, I get into real trouble. With this stash, I can test my theories and actually earn enough alpha returns to justify buying some extras/luxuries when I’m lucky. I’m not convinced investing in dividend stocks is any better than other strategies. Big ERN did a recent article on a comparison of strategies including a “high-dividend portfolio” and this strategy actually had worse sequence risk than a basic “buy the market” strategy.

The Big ERN “high dividend portfolio” has very little in common with the dividend strategy being talked about here with respect to sequence risk. Be careful not to take his implied headline at face value, look at the data and see if it actually leads to the suggested conclusion. When I look at his data, I find the whole thing to be a useless exercise in futility.

https://earlyretirementnow.com/2019/02/13/yield-illusion-swr-series-part-29/

Frankly I wouldn’t touch that model portfolio with a 10-foot pole. I know he was just modeling some yield shield portfolio that some other FIRE blog recommended. To be fair he did say how a high dividend portfolio CAN increase sequence risk, not that it for sure would, but the implication is there that high yield is no safety at all. It is certainly true that high yield is no guarantee of safety from sequence risk. A bad portfolio of high yield can certainly increase sequence risk. This was a bad one. But the implication is still left hanging there that yield doesn’t provide sequence risk protection. But this doesn’t prove that at all. It just proves this particular mess of a portfolio doesn’t provide sequence risk protection.

It contained the following:

10% Government bonds paying 2.69%

10% Corporate bonds paying 3.56%

10% REITs paying 5.06%

15% total market ETF paying 1.88%

5% vanguard high dividend ETF paying 3.20%

30% vanguard international ETF paying 3.03%

20% preferred stock index fund paying 6.02%

20% bonds which provide no inflation protection and the corporates are still subject to the risk of default. Some of them do during recessions.

10% REITs whose yields are more at risk during recessions especially the last one which was all about housing.

15% total market funds that pay low yields and provide negative sequence risk due to their low yields.

30% international fund which I have no way of assessing its dividend reliability. This is just submitting to diversification dogma. I do not trust what half of these international countries and companies are even doing. I might own a very small amount of international in an index fund, but for dividend safety and sequence risk protection I wouldn’t trust any international funds. When it comes to safety, I am with the BOSS. Born in the USA baby.

20% preferred stock. These yields have special rules that make them very easy to flat out skip in recessions with no obligation to repay. This is exactly the type of high yield asset that increases sequence risk. These should not be in a portfolio trying to eliminate sequence risk.

This portfolio seems to have been put together by someone who didn’t understand how much the components in it increases sequence risk. It is like it was custom designed to blow up under stress. And low and behold that is exactly what happened. The portfolio actually did exactly what you would expect it to do when you look under the hood. Big shiny turbo with a supercharger and a little 4 cylinder engine that blows out under stress.

The real question is which dividends are most reliable. Which hood isn’t suped up but just has a straight 451 V8 under it. The answer is those dividends that have a long history of being raised every year, namely the Aristocrats.

A good test would have been to get the Aristocrat list prior to the great recession and then test a portfolio made up of equal weightings of all stocks on the Aristocrat list. I will bet it outperforms every other indexing stock/bond mix on sequence risk and not just by a little bit, by a long shot.

That’s the type of high yield generally being talked about here. If you want to test sequence risk, test the straight V8. Those are the Aristocrats.

Dividend investing may be better for income and sequenxe of returns as a goal, but definitely not if you want the highest total return. 2009 showed me that dividend investing gets hit twice both in terms of capital losses and after that dividend cuts. To make up for the risk you’re diversifying until you have 50 shares which is basically just a crude index approximation.

I remembered the term “yield shield” from the book “Quit like a millionaire” by Kristy Shen and Bryce Leung. It’s chapter 15. That’s an interesting book. I’ve studied the ideal portfolio lists of the major bloggers, and seeking alpha writers, and dividend investing books, etc, etc, and what it all comes down to in the end, is that the proof of the pudding is in the single question, “How long have they been raising the dividend.” They say, in business or in a job, after everything is done, the paycheck is what is left over, and kind of “all that matters.”. After the product is designed, manufactured, packaged, sold, shipped, supported, the vendors are paid, the workers are paid, the rent is paid, etc, etc, the money left over (profits) are “what matters.” It’s like how you mine and smelt 2 tons of ore to get one ounce of gold. When a company has been raising the dividend every year for decades, that is the only bottom line that matters, the actual results. Warren Buffett has this saying that people tend to take things that are relatively easy and simple and make them super difficult and complicated. And it think it’s because (figuratively) we are sifting though the two tons of ore instead of just looking at the one ounce of gold. The gold is the raising of the dividend for decades. Everything else has to be done right in order for that to be the end result. That’s why only about 60 out of the roughly 5000 publicly traded companies can be considered dividend aristocrats. So, that’s why I recommended sticking to that list for dividend stocks. I do realize by doing that, you may be missing out on some of the growth factor. Perhaps, once your income needs have been met with your dividend stocks, perhaps any additional funds should be put into index funds in order to capture the growth factor that one might be missing out on with dividend investing. That would seem to me to be a prudent strategy.

And one more thought… there’s a lot of talk of funds. One of the biggest strengths and benefits of dividend investing is that you can value and purchase individual companies, and select only the ones that are undervalued. Being able to value a company and purchase ownership for less than it is worth is the “superpower” I was referring to and really the essence of what investing actually is. With funds, you are just buying somebody else’s entire “collection” of stocks, and you lose the ability to focus on anything specific. Being able to focus on value is what increases the yield and boots your overall results over time as the share price of the companies come back into fair value. That’s why I recommended sticking to aristocrats and buying them when they are yielding over 4%. The best tool to help with this is the web site called FastGraphs. If investing is akin to solving complex math problems, then Fastgraphs is like having a calculator vs. having to do all that work by hand. I really wouldn’t even recommend trying to buy individual stocks without using Fastgraphs, unless you have an extensive background and education in accounting and financials.

I think MI140’s approach is logical and repeatable so if this strategy is comfortable to him and anyone else, I agree those folks should stick to it. As for me, out of research laziness and lack of such a formalized way to evaluate individual dividend stocks, I bought sectors but it’s curious how I think they do overlap a bit with what individual stocks MI140 bought. I bought XLE (energy) which I think correlates with MI140’s Exxon and Shell holdings and XLF (financial) which I think also strongly correlates with the bank holdings. Maybe not as I didn’t dig into it too much but when I bought, both those sectors were down quite a bit (relative to the S&P 500). I’m also long on some travel related stocks and emerging market ETFs that I don’t think will hit MI140s radar. I think the main take away is that folks need to have a logical, consistent strategy to know when to systematically get in and out of their positions. After that, I think it’s really anybody’s guess as to which strategy is better. Apex is correct that Big ERN’s analysis is much different from MI140’s strategy and the only point I was trying to make is that I don’t think focusing on quality dividend stocks is any better or worse than other reasonable strategies out there. But if this strategy is consistent with you values as an investor, then I say you should do it since you are much more likely to stick with that strategy and not buy high and sell low due to panic and second guessing yourself.

Curious which EM ETFs you’re interested in. I’ve been loading up on those this year, including a couple that have high expense ratios like DEM and DGS.

I never said that the Yield Shield has everything in common with the portfolio presented here. I compare the Yield Shield to a 60/40 portfolio and point out the danger of shifting into higher-yield but also higher-risk assets and increasing. It’s actually a very important exercise for people planning FIRE or in FIRE. It’s not a “useless exercise in futility”…

ERN,

I posted my comment generally at the bottom by mistake.

The one thing I would add to MI-140’s list of what to look for when dividend investing (or investing in general) is for companies who’s revenue is increasing. It’s difficult to continue to increase dividends when your revenue isn’t increasing. A lot of dividend aristocrats are older companies and some of them are getting disrupted by younger companies, so be careful with that too. I’m younger and tend to look for companies that will become dividend aristocrats in 10-15 years. This leads to lower current yields, but I think will add some price appreciation as well.

Exactly. You can’t increase dividends for very long when your revenue is decreasing. So, with the aristocrats having been able to do that for a minimum of 2.5 decades, sticking to the list kind of automatically does that for you. But you are also right, past results are no guarantee of the future, especially in the changing world we live in. So, many people make a rule for themselves where, when a company cuts the dividend (and of course they would automatically fall off of the aristocrat list at that point), they would instantly sell the company. But that is not a very common occurrence.

MI140 – it is like we are cut from the same cloth (I have also read Kristy’s book)! I too have an individual stock portfolio that produces $264,070 in dividends each year and I also bought stock on margin in March of this year. I did not jump in at the same amounts as you as I am currently retired and I am living on dividends alone. Nevertheless, I could not pass up some of the unbelievable deals that were available. I am Canadian and the Can banks were selling at yields over 6-7%…had to get some more!

I have built my portfolio of dividend stocks up since I got out of mutual funds in 2010 and have about 50% of my portfolio in US stocks and 50% in Canadian stocks. The husband and I own a home in Florida where we spend about 5 months a year (escaping the winters!) and we have a farm in Ontario so we need both USD and CAD income. We have been retired since 2017 and living on dividends alone (well my hubby also gets CPP but that is small potatoes!). We own mostly the defensive blue-chip dividend stocks that are dividend growers and many of the same that you have in your portfolio. We own more utilities and consumer staples than you and of course the Canadian banks, pipelines and telecommunication companies.

Our dividend income is more than 2.5x our annual spend so we have room to absorb any dividend cuts and since we own both RDS and IMBBY (recently announced a cut) I feel your pain. But, having said that, we also own JNJ – recent dividend increase of 6.3%, AAPL – 6.5%, PG – 6%, AQN – 10%, MDT – 7.4%, PEP – 7.1%, TD – 6.8% increase etc. The good will outweigh the bad over time so long as you have a balanced portfolio. I never have more than 5% of my original cost in any one stock. I also do not rebalance since I generally hold for the long term. My portfolio is 100% in stocks but I do have a cash buffer of one years expenses – just in case.

I think to be a successful investor you really need to have a plan that you are comfortable with. No one plan is right for everyone. You need one that you can stick with even with the ups and downs of the market. DGI is the right one for me but will not be for everyone. I am not writing to boast, I have been very fortunate in life, but wanted to let you know that it is possible to be retired and living on dividends with a portfolio similar to yours. It can be done…..

Wow, we have done things almost identically! How old are you? I am 44. I hadn’t heard about IMBBY cutting until just now. Dang it! Another one bites the dust. At least it’s only a 33% cut. I will likely start trimming many of my overweight non aristocrat holdings, in situations where I am able to do so with gains or minimal losses.

I agree that everyone must do what feels most comfortable for them. Like most things in life, no single solution fits everyone.

I agree that we have done things almost identically. I also use FastGraphs and found it to be invaluable when I was building my portfolio. I am currently 59 (hubby is 70) and have been retired since age 56 from an executive level, high stress, corporate job. Best thing I have ever done! While I loved my job, it was all I was able to do. Sitting on my butt day in and day out. Now I bought a horse, ride every day, compete with my horse, golf with the hubby and rarely spend time on my butt (well except for in the saddle LOL!). All funded by my dividend stream.

nice! DGI is a great system. Do you have a targeted dividend yield across the portfolio, or how do you establish a balance that the dividends will grow with inflation/compounding?

Wow, congratulations on a job well done. That is precisely my goal. I’m 39 now and have 50k div income, but I’m selling off my real estate properties and shifting to high div yielders. So I should be at a 100k by 40 yrs old and semi retire. Thank you for sharing your story like the author. It’s very encouraging!

ERN,

The comment was not directed at what you had said but at what one of the commenters here said. His statement was that your analysis showed that high yield increased sequence risk. I pointed out that your analysis showed increased sequence risk in a very particular high yield portfolio which was this yield shield portfolio. The futility comment was based on this being a particular poor sequence risk portfolio and then drawing any kind of a general sequence risk conclusion about high yield portfolios based on this one particularly poor example portfolio.

This is the thing that easily becomes a misleading extrapolation from a very specific and narrow analysis of one example of a product in a general category that then gets assumed to be representative of the entire category. You didn’t state that assumption directly, but it is not a large leap to get there and the commenter here seemed to be making that leap.

I was not familiar with this yield shield portfolio but as I stated I wouldn’t touch it with a 10-foot pole. Your analysis did a good job of showing that during the great recession the yield shield portfolio sucked at providing sequence risk. I would have expected exactly that based on what is in it. It almost seems taylor made to blow up during a recession (again back to my reason for finding the exercise a bit futile). I am surprised anyone points to it as any kind of a safe sequence risk portfolio. In fact your analysis of this portfolio seems to pretty much reach the same conclusion that this portfolio has all kinds of things in it that one should not expect to provide sequence risk protection but that are actually more likely to increase sequence risk.

As such a complete examination would seem to require analysis of better high yield portfolios with respect to sequence risk. To be fair I have not reviewed anything else on your site so I don’t know what else you have analyzed with respect to high yield portfolios.

It would be a great exercise for you to do what I had suggested as a way of testing sequence risk in what I would consider the gold standard high yield portfolio for sequence risk. Namely create a portfolio of all the Dividend Aristocrats from 2008 and see how that would have done on sequence risk versus that standard 60/40 portfolio. I will bet it beats it handily for sequence risk and holds up just fine on growth and performance too. It seems like a good addition to your SWR series. You may or may not find such a portfolio to be lacking in categories such as growth, diversity, etc, but that is a separate issue from whether it provides sequence risk.

Apex:

Well, the numbers are in: VYM (general dividend-weighted), SDY and NOBL (dividend aristocrats, though using slightly different rules) did very poorly in 2020 both in absolute terms and relative the S&P 500.

But don’t get me wrong: I wouldn’t say that they did worse BECAUSE of the higher dividend yield. It’s a different equity investing style. Sometimes it will do better, sometimes worse than the broad index. It’s what I tried to convey in my SWR Series Parts 29, 30, 31: on the equity side (international vs. domestic and high-div vs. index) it’s a crapshoot. On the fixed-income side, you will necessarily do worse with the Yield Shield during a recession.

I am earnestly interested in a true and fair analysis here but count me confused.

I honestly have no idea what this comment means. 2020? Is that a typo or did you just decide to change from a full cycle recession and recovery to 3 months of COVID for your analysis? Absolute terms and relative to the SP500? How does that relate to sequence risk?

I am happy to look at any data you have, but this comment doesn’t have anything in it that seems to be related to the topic (sequence risk) and has no data or link to any analysis to comment on.

MI 140 and ESI:

Thanks so much for this post, full of great info. I discovered the FIRE community about 5 years ago. Since that time I’ve been focused on increasing income, lowering expenses, and building net worth. Only recently did I realize it’s not about your net worth, but monthly passive income. That’s the whole key to financial independence…with proper insurance and safety margins, of course. Thanks for the primer and tales from the trenches!

Can you give us an approximate idea of the 7-figure amount in your portfolio that generates this type of dividend? 5-6 million? Thank you for sharing your experience. Over the long run (past decade), has your annual average growth rate exceeded that of S&P 500 index funds? I understand that your portfolio has outperformed the S&P 500, but I wonder over a long time horizon if you have been able to exceed its return.

Awesome reading!

I am a similar investor to you, albeit I have a core of ETF’s and dividend stocks around that.

Great reading!

M140

Thanks for your insight and all the details you shared. Our investing mindset is similar. Where we differ is I try to buy stocks when they are on sale and sell when fully valued. In non retirement accounts, I went into all cash at end of 2019. It was more because I was planning on investing most of that money in real estate in Florida than anticipating a downturn. Towards the end of March I put a million back into stocks and bought GS, USB, WFC, SKT, SPG, MAC, PFS and fully margined everything so bought $2 million of stock with the $1 million in equity. I have continued to buy more And generated some short term profits as it goes up so now have $4 million in stock and $2 million in margin loan. I used interactive brokers for a .75% interest rate margin loan interest rate but I have to pay for trades. I also traded a few other stocks and took some short term gains.

I try to forecast earnings and cash flow twenty or thirty years out on any companies when I invest. I am not as concerned with current pay on dividend as how much cash flow the companies generate that can and will be distributed to owners. I generally try to only buy companies with strong earnings.

PSH is a really interesting closed end fund trading at a significant discount. Bill Ackman did an amazing job hedging the PSH portfolio during coronavirus by making a $27 million dollar hedge that earned over $2.5 billion that he closed out at the bottom and bought more stock. It trades on odd exchanges so a little harder to figure out how to buy it. I think all the other stocks I own will have pretty solid profits this year but likely substantial declines from prior year profits. There is a reason they are half price or more off prior stock prices.

It’s horrible to use margin in a declining market or if you can’t afford any potential margin calls. It’s really powerful for those incredible rare times when quality companies go on half price sale. I feel I am using margin to buy future earnings with a strong margin of safety when I use it. I don’t recommend it unless you have multiple ways to pay it off and are able protect yourself from any margin calls. The market can remain irrational longer than we can remain solvent has an incredible amount of truth to it.

“I try to forecast earnings and cash flow twenty or thirty years out on any companies when I invest. I am not as concerned with current pay on dividend as how much cash flow the companies generate that can and will be distributed to owners. I generally try to only buy companies with strong earnings.”

thanks for sharing, could you explain more how you actually do the forecasting process? Thank you as your post and the above post have really been inspirational.

I recently used gurufocus for 30 year historical financials. You can also use sec.gov or the companies investor relations website for historical sec filings or annual reports. I try to estimate future earnings based upon most recent facts and using historical earnings. As an example Simon properties or Tanger are unlikely to ever fully recover prior earnings level but you could pretty conservatively forecast how far earnings would drop and realize the price they were trading for was too low based on future discounted cash flow. Both companies are shareholder friendly in dividend payments and stock repurchases.

You could also forecast a company like amazon thirty years out showing amazing growth but eventually their growth will be limited to how fast the economy is growing. You can calculate how long it will take to earn your money back based on the current market capitalization of the company.

My analysis allows me to be a pretty efficient at identifying companies trading lower than tangible value but causes me to miss on investing in some great long term growth companies.

I have one account that has been the same funds invested for about 27 years and I average about 17% per year in that account with no taxes taken out since it’s a Roth IRA and no contributions have been made since 1993. I am a CPA, MBA and have years of finance experience so it’s fairly easy analysis and I am not that detailed with it. The challenge is the growth assumptions. USB and WFC are somewhat easier to analyze since banks generate earnings based on return on book equity and then book equity is either reinvested or distributed to shareholders via dividend or stock repurchase. The stocks generally trade as a factor of book equity so you can forecast long term stock price when you forecast long term book value and earnings. Let me know if that makes sense. If not I can try to explain a different way,

Right now I am actually selling some of the positions and going to cash. I think stock valuations have gone up too far, too fast with coronavirus still out there, likely bad second quarter earnings coming up, unknown president in 2021 and protests in the street. I think SPG is up from $76 to $96 in the last couple trading days, my initial buy was just under $50. BA is up crazy in a week. I don’t trade short since I never had much success at it. I oftentimes miss some really good upside by selling too early. I bought BRK today since they are lagging the market and it has some upside if the market keeps going up and won’t go down much in a downturn.

I am different from the average E,S,I person since much of my effort on the E side is investing in different areas to make higher returns on my investments while using leverage. I will likely deleverage sometime soon (next few years) by selling investment real estate and some stocks.

Thank you for the feedback.

Are you doing your calculations via excel or some kind of software? I see, Gurufocus can do analysis such as discounted cash flow as well.

are you unloading your SPG in full?

Interesting. I used to also analyze shares, thought it helped to work in private equity and have an MBA. Realized that the quality of analysis on listed shares differs to unlisted equity. In the listed space you have the market price, and mostly its correct except for the few oversold days.

I realized that I couldnt outearn the market return since analysts like us are the market. I just want equity returns, leveraged, and go with that.

A serious question, I’m interested in why do you think your analysis would generate alpha compared to the other market participants?

Bob,

I can probably only generate alpha once every 10 years in the stock market when the market is in a dramatically oversold position and some stocks/sectors are even more dramatically oversold. I did really well in 2008 and 2009 and have done really well this year. I had a great 2017 as well when I was trading Berkshire in a band. It would go up and down a few percent pretty consistently and I also traded their earnings releases after the fasb rule on Mark to market accounting on their stock portfolio was new. The same strategy did not work in 2018 and I lost a little money while the market went up a lot. I generally underperform in upward trending markets since I am not invested in what is trending up the most. I know that so I end up moving money out of public investments and into private investments in everything but my retirement accounts. Most of my money is made in real estate that moves much slower and I also have a lot of losses in real estate from 2008. Right now you can make 20% margins building new homes in Florida and I split the profit 50/50 with the an experienced and trustworthy local builder. Our unlevered returns are 40% per year with making 20% twice a year. Levered can be significantly higher. There is usually alpha to be made investing somewhere. I also started/invested in a skilled home health care company this year. We have nurses and OT’s and PT’s provide in home visits and are reimbursed by Medicare and insurance companies. The returns on equity invested will be very good. There is alpha to be found but it’s rarely available in the stock market.

USB and WFC are still likely still undervalued today but you need a year to make it through the volatility. Banks don’t have a lot of bad debt from the downturn. Many of the unemployed are earning more than they ever earned working and that is laying the foundation for a pretty strong recovery. Zero percent interest rates and printing trillions is a new experience for the US. It will definitely have an unpredictable impact.

I sold spg in my retirement accounts and sold covered calls at $65 strike price 6/19 expiration in taxable account. I think the market gains the last 10 days have been a little too much. I am holding PSH, USB, MAC, WFC and sold or sold calls on SPG and SKT. I probably would have been better just holding but I had such big gains so quickly, that I am trying to protect them. I had big gains 4/25 to 4/29 and gave them all back 4/30 to 5/13 and didn’t want to repeat the experience.

I sometimes use excel, I sometimes just do really simplified calculations, I sometimes see what seeking alpha has posted. There is a good DCF article on SPG that just got posted on seeking alpha. It says buy under $60, sell over $90 in quick summary.

Could you share an example of how you do your simplified calculations?

Also, “The challenge is the growth assumptions. USB and WFC are somewhat easier to analyze since banks generate earnings based on return on book equity and then book equity is either reinvested or distributed to shareholders via dividend or stock repurchase. The stocks generally trade as a factor of book equity so you can forecast long term stock price when you forecast long term book value and earnings. Let me know if that makes sense. If not I can try to explain a different way”

Could you elaborate on this? My understanding is valuation is based on free cash flow, I’m finding your explanation here interesting and something I did not know.

Mark,

If you want to send your email contact info to ESI money to forward to me, we can mutually decide on a stock to analyze and i can send you excel spreadsheet. Have a great day

M139, that would be great. will do

Your losses in May 2020 had me fainting. Where are you at now?

I am up just under 100% on the Roth IRA for the year and as of today mostly in cash with my largest non cash position being in PSHZF. I am trading in and out of SPG and try to buy at the lower end of the trading range and sell when it goes to upper end of the trading range.

My taxable accounts are doing substantially better than the Roth on both rate of return and total dollar gains, my entire initial basis is out of the taxable account so the balance is the earnings from this year. I have a lot of SPG with covered calls sold on all of it as of today. Both last Monday and Friday were really big up days, I hedged half of Mondays SPG gains and closed the hedges on Thur and then hedged all the SPG gains on Friday afternoon. I see SPG in a $60 to $84 range and will likely close hedges around $68, depending on what else is going on in the market.

I also own PSH that I don’t hedge and it is not nearly as volatile. Take a look at their website for Pershing Square and click on NAV values. You are buying a portfolio of 10 stocks for close to a 30% discount and Bill Ackman has been a really good asset manager for the last two years. His $27 million investment in late February to hedge the portfolio from COVID losses paid out over $2 billion in a months time and that is all shared with the owners in PSH. I like SPG because they are profitable every single day and pay a decent dividend. I think half the malls in the country can close down but the remaining class A malls will likely do ok into the future. I like the management of SPG and their balance sheet. They have a lawsuit starting this week related to Taubman merger that has some downside to the stock and its unknown how much mall retail will be negatively impacted as states impose additional shutdowns. As a flyer I bought a little PEI common stock and some of their preferred stock on Friday that are both trading at a substantial discount if they can survive. I don’t own Wells Fargo or the banks anymore.

It’s really interesting right now with COVID numbers shooting up that is a market negative, an election still not fully finalized that will likely happen in the next week or two, and light at the end of the COVID tunnel with a vaccine.

Thanks for the update. I am really surprised to hear you are mostly cash in your Roth. Is that due to the uncertainty you mention regarding the election?

It’s because I made a mistake as of this morning. Valuations are high and I think shutdowns are likely to get Covid cases under control. I have had a great year and happy with my return for the year. I am not your typical investor. I am a cpa, MBA and really feel I am buying in as part owner of the company rather than buying a share of stock that I think someone else will want to buy from me in the future. I love Tesla and Amazon but struggle with the current valuation. I read annual reports, listen to quarterly conference calls, study the business, etc before I invest

That is a very interesting post and I have always been a big proponent of dividend investing. I have always believed that yield is the most important indicator of value and long-term return performance. This is not always true for individual stocks, however, but is a great indicator across the market broadly.

With that said, I do question several items in this post. For one, 5.5% margin interest is probably the lowest you could possibly get as an individual investor. The average available to most individual investors in likely closer to 8-9% even in today’s interest rate environment. Another, I think a weighted average 8% yield across a diversified portfolio of quality companies is unrealistic. For example, the current yield on the S&P aristocrat dividend fund is approximately 2.75%. You can find value companies with high yields, but they are very risky (as the high yield was created by a significant price drop) and you have to be prepared for them to go down another 20, 30, 50, 70 percent and hope they continue to pay the same dividend. If you have great fortitude, go ahead and this if you want, but I certainly would never do it on margin. I cannot think of a higher risk strategy than buying high yield stocks on margin. They are high yield because their prices have fallen dramatically and may fall further. You literally could lose everything.

Final point and probably most important, index investing and dividend investing are not mutually exclusive. I hold only passive ETFs and mutual funds and am still getting a weighted average of approximately 3% yield without any risk associated with individual equities and while still having most of my portfolio in growth stocks (although I never buy anything that does not provide any yield). The yield portion of my portfolio consists of passive funds consisting of HY stocks, MLPs, Prefs, BDCs and a mortgage fund.

SL

Thanks for your comments. Interactive brokers pro account is .75% interest rate for over $1 million. You have to pay for trades in pro but cost is not that bad. IB has a free trading account with 2.59% margin rate for any margin balance.

https://www.interactivebrokers.com/en/index.php?f=46376&p=

You absolutely are correct to get 8% yield over a diversified pool of quality companies is completely unrealistic. The most important thing that any company generates is earnings and free cash flow. A 8 percent dividend that is well supported by earnings and cash flow will likely result in either a decline in earnings, cash flow and the dividend rate or an increase in the stock price. The key is identifying the company that actually has the future earnings that can really support the high dividend payout.

You are correct buying high yield stocks on margin is likely a very risky strategy to pursue.