Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in July.

My questions are in bold italics and his responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I’m 52 and my wife is 50.

We’ve been married for just over 19 years.

Do you have kids/family (if so, how old are they)?

We have a 15 year old son.

What area of the country do you live in (and urban or rural)?

We live in a large Midwestern city.

What is your current net worth?

Our net worth is $3.6 million.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

We are recently totally debt free! We’ve worked hard on achieving that, and we’re really proud of it.

Our net worth is split between real estate, 401Ks, and reserve funds.

We have about $2 million in paid-off real estate, which includes five duplexes. We live in one of the duplexes, but we still count the value of that house in our net worth since we collect rent on it ($2,875 monthly from the upper unit and $850 for the studio unit in the basement).

Now that we are debt free, our annual pre-tax income from the five duplexes, net of all expenses, is $120,000. That feels totally awesome. It took almost 20 years to buy and pay off these properties, but it’s really nice now.

- Personal residence: $575,000

- Rental Duplex #2: $365,000

- Rental Duplex #3: $365,000

- Rental Duplex #4: $350,000

- Rental Duplex #5: $350,000

We have about $1.35 million in our 401K retirement accounts, and the rest in cash reserves for us and the properties.

EARN

What is your job?

I recently retired as the founder and CEO of a large national nonprofit organization, and my wife is a tenured professor at a top public research university.

What is your annual income?

This year our income will be about $440,000 (annualized given my retirement).

I was making about $330,000 (based salary, bonus and deferred compensation), and my wife makes about $110,000.

Now that I’ve retired, I no longer have income from my job, so we plan to live on the rental income ($120,000 net of expenses before income taxes) along with my wife’s income.

My wife expects to retire in about six years, and then we will live on the rental income and our retirement assets as needed.

Our income is much higher now than it has been most of our lives. I would say it has averaged about $150,000-$200,000 per year over the course of our marriage.

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

As a nonprofit executive, my income was much lower when I founded the organization 20 years ago. It grew steadily as my team and I were able to grow the nonprofit from a small operation in one state, to one that is now national in scale. When we got married 19 years ago, our combined income was about $75,000.

I’ve been an extraordinarily hard worker for my whole life. When I was a kid, my family was pretty poor, and everyone I knew worked very hard. My dad worked two full-time jobs to save up enough for him and my mom to buy our family’s first home. All of my siblings, and aunts and uncles, were hard workers.

So when I was about 10 years old, I made little hand-written business cards that said: “[My Name] Year Round Yard Care,” and I went around the neighborhood of our small town and knocked on doors and said I’d do any job they needed done, such as cleaning their basement, garage, cars, or any kind of yard work. I told them if they’d give me a chance, I’d do the work for an hour or two, and if they didn’t agree that I’d done an excellent job, they didn’t need to pay me at all. I got a lot of customers that way.

Soon, I had more work than I could handle. So as a budding capitalist (it’s a little ironic that I ended up founding and running a nonprofit!), I hired my friend to mow lawns with me. I’d charge the customer $7, pay my friend $5, and keep the $2 as profit.

When I was 14, I got a job at the local grocery store. I earned $3.35 an hour.

I’m still quite proud to say that by the time I finished high school in 1986, I had saved $10,000.

I worked and paid my way through college. My first job after college paid $18,500 (the offer was for $18,000, but I negotiated for an extra $500).

I went to graduate school and my first job after that paid $56,000.

When I started the nonprofit, I worked for free for nearly a year, and eventually began collecting a salary of $30,000.

What tips do you have for others who want to grow their career-related income?

Like many of the others you have interviewed here, I would say that it is really important to work hard, do an excellent job, and always aim to exceed expectations. The key, in my mind, is to assume that nobody owes you anything. A misplaced sense of entitlement is a killer. You’ve got to hustle and grind.

But that’s often not enough. You also need to invest in yourself through formal and informal education. You have to develop a skill that is valuable.

I also became good at making sure people noticed me and what I was contributing. That’s harder than it sounds. If you overdo it, you look like an egomaniac. You need to share credit, too. But you need to remember that most of the time no one else is looking out for your interests, so you have to strategically promote yourself to decision makers and other key influencers in your world. The best job security is making yourself so valuable that you seem indispensable.

I would also say that developing “emotional intelligence” is critical. I’ve met and worked with a lot of brilliant, intellectually gifted people. That’s a great asset, but you need to have the right kind of spirit, too. A good sense of humor, especially self-deprecating humor, goes a long way. I always strived to be a compassionate, fun, generous, good natured person, who also demanded excellence and set very high standards. If you can achieve that, it’s a powerful combination in my opinion.

As a CEO who hired, trained and developed thousands of people, I will say that the folks who did some or all of what I’m describing here were always the most successful.

The other saying that you often hear about making your boss’s job easier, or looking for ways to make your boss look good, really are true. When it comes time to select someone for an exciting or important project, or more importantly for a promotion or a big raise, it’s funny how bosses end up picking folks who have made the boss’s life easier!

What’s your work-life balance look like?

It’s great now that I’m retired! But it has been pretty crazy for much of the last 20 years.

Starting and growing a nonprofit is incredibly difficult. By the time I stepped away, it had a $30 million budget with more than 400 employees across the country. I was on the road a lot over those 20 years. I averaged about 50,000 miles flown for the last 15 years or so. That’s a lot of time away from home, usually in super stressful environments.

Meanwhile, my wife was working very hard in order to complete her Ph.D., get a good job and ultimately earn tenure.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

We’ve earned a lot from the real estate, but literally every penny has gone into maintaining, upgrading and, especially, paying it off. As I indicated above, it now provides pre-tax net profit of about $120,000.

We essentially used the Dave Ramsey snowball method to pay the properties off. Once we paid one off, we then used all the profits from the paid for building to pay off the next. Rinse and repeat. By the end, you’re paying them off very fast.

If I kept working right now, we’d have that $120,000 annually to use to buy more properties. But we decided that we have enough now, and would rather slow down and enjoy life a bit more.

SAVE

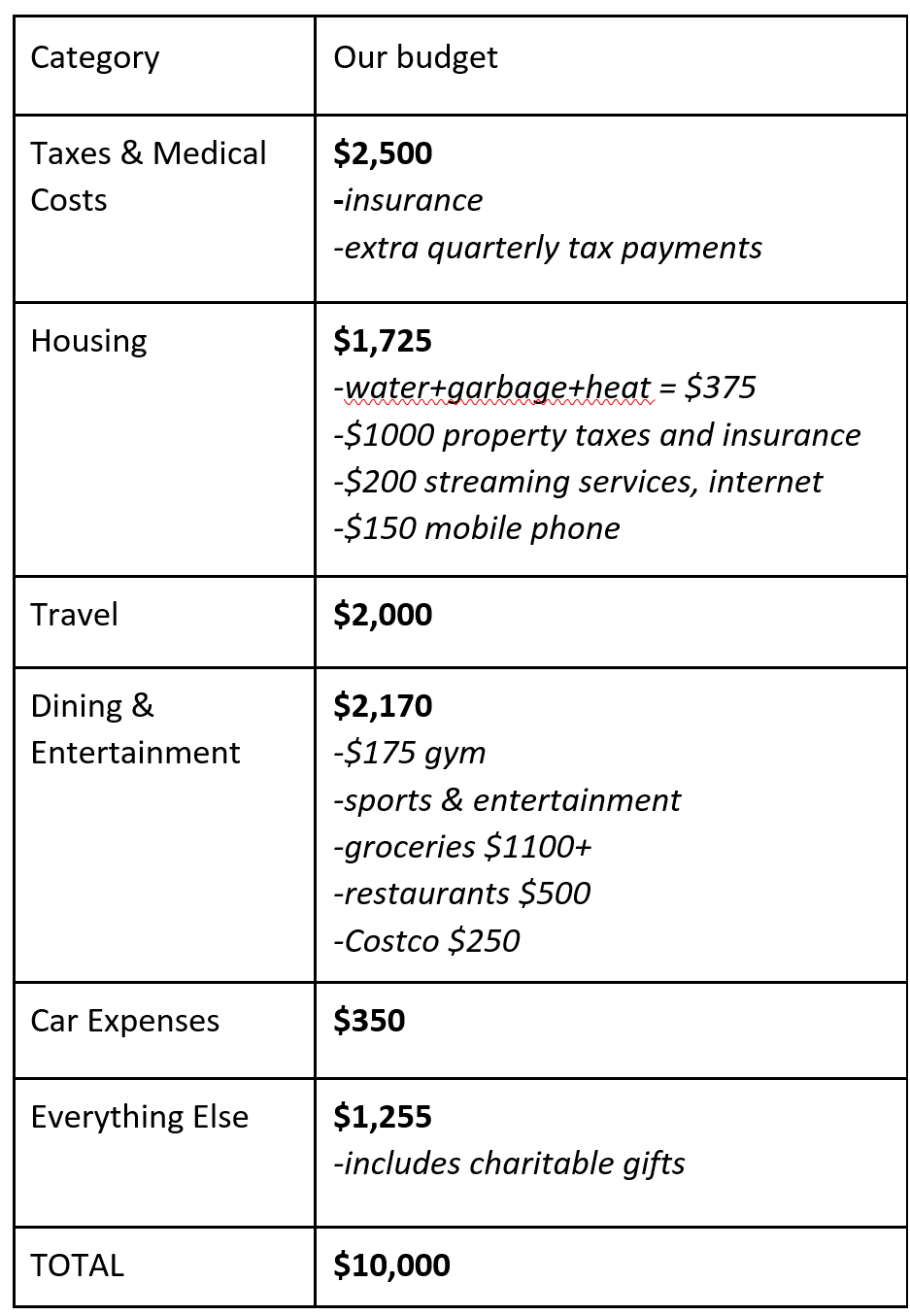

What is your annual spending?

We spend about $10,000 per month. We don’t include our state or federal taxes in our budget since they come directly out of our paychecks, but we pay at least 30% of our gross income in state, federal and Social Security taxes.

For at least 10 years, we have each maxed out our 401Ks. We also now save about $25,000 annually for our son’s college 529. Travel is really important to us, so set aside $2,000 a month for travel (which includes a month in Maine each summer, a ski trip, and other shorter trips as they come up).

What are the main categories (expenses) this spending breaks into?

Do you have a budget? If so, how do you implement it?

For much of our married life, we didn’t use a budget. We subscribed to the idea that if you automate all of your savings (like 401Ks, extra mortgage payments, college savings, student loans debt, etc.), then whatever is left over is ours to enjoy. This worked okay, but often resulted in shortfalls and some misalignment between my wife and me.

About five years ago, we switched to the Dave Ramsey “Every Dollar” budgeting app. My wife took the lead on doing this, even though we’d both agree she’s more of a spender, and I’m more of saver.

That decision was really critical. It helped us get aligned and have a much better line of sight to our savings and spending. Once we got more organized, we have been able to direct our money with much more discipline.

In the last 3.5 years, for example, we paid off nearly $700,000 in mortgage debt on our rental properties.

What percentage of your gross income do you save and how has that changed over time?

It has varied over time, but I would say it has averaged about 30%-40%.

What’s your best tip for saving money?

There are few simple steps to saving money.

One is to automate as much saving as possible. When we were first starting out, we automated almost all of our savings and debt reduction. When we got a raise, we used most of all of it to increase our 401K contributions until we reached the legal maximum. That’s a pretty painless way to increase your savings rate, but it requires you to pretty much maintain your lifestyle even as your income goes up.

But we also do other simple things to save. We bought our cars with cash and keep them for a long time (though, I’m about to buy a nice new car that we have saved up for). I’ve often noted that most of our tenants drive nicer, newer and more expensive cars than we do.

I also shop for many of the basic foods and household products at a Costco.

What is your favorite thing to spend money on/your secret splurge?

Our favorite thing to splurge on is travel.

We believe that experiences are much more valuable and enjoyable than physical stuff.

For 13 years now, we’ve spent a month in Maine each summer. We love it there, and both of us can do a lot of our work remotely. We set aside a very significant amount of money in our budget each month for travel and let it pile up so that we can do nice trips and always pay cash.

INVEST

What is your investment philosophy/plan?

By far our best investment decision was buying rental properties. When we first moved to our city, we rented a duplex. After a while we thought, why not buy one of these and have the renter help us pay for it? We then refinanced it, and used the cash to buy the next one, and so on.

Real estate is clearly not for everyone, but it’s worked really well for us. We typically bought duplexes in neighborhoods we’d want to live in and that has helped us assess the market and rents pretty easily.

We often bought houses that had “good bones,” but needed paint, new appliances and fixtures. I’m pretty handy, so in the early years I did virtually everything myself. Eventually, I found a retired railroad worker who is very handy. He now takes care of all the units for me at $30 an hour. I still advertise and show the units myself, and collect the rent. I’ve been surprised by how easy it is.

Many (most?) financial advisors make owning real estate sound really hard and talk about backed up toilets at midnight, etc. But it’s been pretty easy for us. I would say I put in a grand total of 60-80 hours a year on it, though I’m pretty efficient.

I’ve noticed that many people look for a certain projected return (often really high) on their real estate investments. I think it’s imperative to model out your expected income and expenses. I’ve created more spreadsheets than I’d care to admit. But I would also say that ultimately, you need to avoid “analysis paralysis.”

Could we have found better deals that would have resulted in higher returns? Probably. But I think the most important aspect, by far, was that we moved forward and did it. If you buy real estate for the long haul, it will make you a lot of money because your renters end up buying the property for you. So, don’t obsess on the analysis. Do your math, be rational, make some offers, and get in the game.

With the rest of our investments we strictly go with Vanguard Index Funds. I’m persuaded by the research that shows that almost no investment professionals beat the market over a five year or longer period. We just automate it, put it in low-cost index funds and forget about it. We do the same with our son’s college fund.

What has been your best investment?

Definitely the rental properties.

Look at the duplex we live in: it produces more than $40,000 of income a year! We actually get paid to live in our house!

What has been your worst investment?

We once bought a four-plex in a tougher part of town, which was also further from where we live. It was more like an apartment complex and was much more hassle than our duplexes. After struggling with it for a couple of years we sold it and essentially broke even.

Our lesson was to stick with real estate closer to our home, in neighborhoods that we know and understand. You can often make a higher rate of return on real estate in more challenging areas, but I think we found that it just wasn’t worth it to us.

What’s been your overall return?

According to Vanguard, our personal rate of return on our non-real estate investments has been 8-9%.

I don’t know what the real estate would be exactly, but it’s a lot higher because we mostly acquired all of that property without using much of our own money.

How often do you monitor/review your portfolio?

About 13 years ago we decided to create a family balance sheet that listed all our assets and debts. We have updated that at least twice a year.

That was a great idea because it helped us see how our net worth was growing over time.

We’re both very high-performing, goal-oriented people, so this really helped motivate us.

We now do it about once a quarter.

NET WORTH

How did you accumulate your net worth?

As I described above, about $2 million of our $3.6 million comes from our investment in five rental duplexes. The rest has been savings in our 401Ks and a cash reserve. For at least 10 years we have maxed our 401Ks out in low-cost Vanguard Index Funds.

We inherited $50,000 when my parents died, which we used as part of the down payment for our last duplex seven years ago.

My wife and I never expected to earn as much as we have. Neither of us ever primarily aimed to make a lot of money. I think there is some truth in the idea that if you find something you truly love and do it extraordinarily well, you will come out okay.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

I would say we’ve definitely ended up earning a lot, especially these past 5-7 years.

We also have done really well on our real estate investments.

We have been weaker on the saving vs. spending. As I mentioned, part of that was that we didn’t use a formal budget until relatively recently. But part of it was also that we didn’t want to live so frugally that we’d be miserable either. I think we have eventually found a balance that works for us.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

Financially, we haven’t had many big bumps. But two years ago, at age 50, my doctor told me it was time to start getting routine colonoscopies. I wasn’t looking forward to it too much, but I also didn’t expect any problems since I felt fine. Well, I ended up discovering that I had colon cancer, stage 3A. I had major surgery and then six months of chemotherapy. I’m happy to report that I’m healthy today. I was very fortunate to have good health insurance and very supportive family and friends.

But coming face to face with your own mortality is scary. I decided to make some changes. I put a plan in motion to leave my job so that I could slow down my life a bit and aim for a healthier lifestyle. I’ve now lost 75 pounds and am at a healthy weight. I’m looking forward to a retirement that is focused on health, fun and sharing my hard-earned wisdom as a non-profit executive through some teaching and starting a small consulting practice.

What are you currently doing to maintain/grow your net worth?

My wife plans to work for about six more years, so we don’t anticipate needing to touch our 401K funds for at least that long, and probably longer.

That will give it some time to grow, hopefully.

Do you have a target net worth you are trying to attain?

Not really. Our rough, but reasonable, projections have us hitting at least $4 million by the time my wife is retired at age 56.

How old were you when you made your first million and have you had any significant behavior shifts since then?

It has amazed me how fast our wealth has snow-balled. We first hit $1 million in late 2012 when I was 44. We hit $2 million four years later, and $3 million about 2.5 years after that. If I had continued to work full-time, our wealth would have continued to grow very fast.

We probably look a lot like the proverbial “millionaires next door.” We live in a duplex and drive basic Hondas. I doubt many people would guess that we are multi-millionaires.

So when we hit $1 million, we were excited, but we literally didn’t change anything. It was the same for subsequent milestones: our behavior stayed constant. Now that I’m retired, I am treating myself to a nice, new, higher-end car!

What money mistakes have you made along the way that others can learn from?

I think the single biggest mistake that we made early on in our marriage is that we didn’t really have a plan or clear goal. Since we’re both really goal-oriented, that didn’t work as well for us.

Once we got focused on paying off the rental properties, and had a detailed spreadsheet that showed when each one would be paid off, we started to focus more.

It was around that time that my wife took the lead in setting up a detailed budget. Once we could see the effect of controlling our spending more clearly (like moving up the date that all the properties would be paid for), we were much more focused. That might not be the right thing for all couples, but it really worked for us. I think if we had done that earlier, we’d have gotten here faster.

What advice do you have for ESI Money readers on how to become wealthy?

I would summarize my advice as:

- Automate your savings and debt reduction through automatic payments.

- Invest in low-cost index funds.

- Consider using a budget, but in any case, live below your means.

- Consider the power of real estate.

FUTURE

What are your plans for the future regarding lifestyle?

As I mentioned above, I’ve just retired.

After my battle with cancer, I knew it was time to slow down, be more healthy and to enjoy my life more. It would have been a lot harder to do that if we were not in this financial position.

What are your retirement plans?

I’m planning to eventually do some teaching at the college and/or graduate level, as well as start a small consulting practice. I’d like to focus my future contributions on sharing the wisdom I’ve gained over my career. I don’t think I’ll do much more than 10-20 hours a week, and maybe not even that. The great news is that I can now do whatever I want and whatever makes me happy.

In six years or so when my wife retires, we’ll probably plan to spend a few months each winter someplace warmer than the upper midwest. I’d also love to be able to spend a few months in Maine each summer. I don’t know if all of that will work out or not, but we will probably do something like that.

We plan to organize our days by focusing on getting quite a bit of good exercise. We walk our dog every day at least once, and I enjoy lifting weights. My wife loves running and looks forward to getting back into tennis, as I do, with golf. We hike and ski (downhill and cross country) as a family every chance we get.

I’m also beginning to read much more for pleasure. My wife is a former English major in college, so she’s already helped me develop a long reading list!

Of course, we also expect to travel even more when we’re both retired.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

Like most people who have done this interview, we are concerned about the cost of health care. We’re planning for it to cost us about $24,000 per year once we are both retired.

We’re also thinking about how to stay healthy so that we can enjoy an active life for many more years.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

I think the relationship between work, money, saving and getting things I want started when I was very young.

I remember fantasizing about this one beautiful North Face tent when I was about 12. It cost $235, even way back in 1980. I mentioned to my brother that I’d love to have such an awesome tent. He asked me why I didn’t just save up my money and buy it. He asked, “what are you spending your money on now anyway?” That got me thinking.

I decided to save that $235. At first I saved my allowance, but I soon realized it would take forever to save that much money without some more income. That’s when I started going around the neighborhood with those little business cards. I ended up saving that money, bought the tent, and I LOVED it. I had learned a good lesson about working, earning money, saving it, and enjoying it.

Soon, I was saving $500 increments and then buying 2.5 year CDs at the local bank. This was in the early 1980s when interest rates were in the neighborhood of 12-15%. When those CDs matured, I couldn’t believe how much they had grown and all I had to do was save and not spend my money!

I did that over and over throughout my teen years, and ended up with $10,000 by the time I graduated from high school. That little nest egg enabled me to go to college without any help from parents.

I would say those basic lessons helped me connect working, saving, investing and getting to have some of the key things I wanted.

Who inspired you to excel in life? Who are your heroes?

Though my parents never had much money, I learned about hard work from them. They both worked really hard, and my mom clipped coupons and scrimped and saved to raise five kids on a very low income. They desperately wanted their children to have better, easier, wealthier lives than they had.

I’m proud to say all of us went to college, became professionals and are doing very well financially. We owe a huge debt to our parents for that.

When I was in high school, my dad helped me get a job on a construction painting crew with him on the condition that I promise him I’d go to college and NOT be a painter. He was proud of his craft, but he wanted a better life for me. We could both see the toll such a hard physical job had taken on him.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

I read The Millionaire Next Door![]() when I was younger, and I’ve been influenced by Dave Ramsey (mostly through his podcast).

when I was younger, and I’ve been influenced by Dave Ramsey (mostly through his podcast).

I’m looking forward to learning and reading much more about these topics now that I’m retired.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

We do give quite a bit to charity. We feel we’ve been blessed, and sharing some of what we have seems like a good thing to do.

We are teaching our son to do the same. Ever since he was very young, we have taught him to have three envelopes for all his money: (1) Share; (2) Save; (3) Spend. We’re hoping to help him think about enjoying money, but also saving some and sharing some.

As his “share” envelope grows over time, we periodically prompt him to select a charity to give a donation. One time, we went to a homeless shelter together so that he could make the donation in person and get a bit of sense of how hard some people have it.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

We are still working on this. We have only one son, and we plan to save enough for him to go to college without taking on any debt. We’ll probably be in a position to help him with graduate school, should he choose that, or a down payment on a house (or both). So, we’ll be able to give him an incredible head start in life. But we worry that too much money, or even the expectation of it, could zap his motivation.

We may end up giving some additional amount to him when we die, but put a larger part in a trust for his children to go to college and buy houses. The remainder, if there is any, would likely go to charity.

Thanks for sharing MI206. A few highlights for me from the great advice in your interview:

Your start as a young entrepreneur at age 10

Your emphasis on the importance of working hard, doing an excellent job, and always aiming to exceed expectations

The need to invest in yourself through formal and informal education

Your realization that the best job security is making yourself so valuable that you seem indispensable

Your view on the importance of emotional intelligence

The payoff when you make your boss’s job easier

Thanks for your note. I’m glad this resonated with you.

I enjoyed reading your approach to real estate. As a real estate investor myself, when I first started I thought I wanted/needed to build an empire. But over the last couple of years we’ve actually be downsizing our portfolio to make it easier to manage and investing some of the gains elsewhere.

If we ended up with 5 paid-off duplexes in retirement, I think that would be perfect. Sounds like you know your priorities, and have worked hard to achieve your goals. Thanks for sharing your story!

Thanks for your comment. I think one of the key things is to determine how much you think you’ll need to have a good retirement. We could have kept on adding properties, but at some point we just decided that $3.5-$4 million nest egg is enough for us.

Some of my buddies can’t believe that we wouldn’t leverage the $2 million of real estate to go buy multiples of additional real estate. But as one of ESI’s posts discussed, once you’ve won the game why keep playing?

I asked my manager if I need to bring the question about my raise to a senior manager, and he said no, that I focus on my work, that he’d do the talking. Half a year on, he’d still not done it. So I took the step.

I realized then that no one looks out for your interest and you need to take care of yourself. A little ‘selfishness’ is needed. I don’t think I’ll ever get a raise if I don’t bring it out – which is why I love this advice:

The key, in my mind, is to assume that nobody owes you anything. .. You’ve got to hustle and grind… But you need to remember that most of the time no one else is looking out for your interests, so you have to strategically promote yourself to decision makers and other key influencers in your world. The best job security is making yourself so valuable that you seem indispensable.

Thanks for your comments.

It can be a bit of a tricky balance. You definitely want to advocate for your own interests, but you don’t want to look like you’re an egomaniac, and you don’t want to step on your bosses toes, either.

I would also say that when it comes to raises, you need to make the case that you are creating value for the organization. I never liked it when I was CEO when people would tell me that they needed a raise because of their personal circumstances.

While I was sympathetic to their situation, my job was to run the business. I only wanted to provide raises to people who were valuable to the organization, and where market data showed that they deserve to be paid more.

This is really a great share and a perfect example of solid meat and potato investing with real estate as the bedrock.

“Real estate isn’t for everyone “.

No it’s not but the real estate exposure sure accelerated tax efficiencies and wealth for those of us who get it.

You say that you now have $0 money invested in your real estate portfolio – (likely because of appreciation and early financing ) that’s the same portfolio that is worth over $2 million and brings in an income of $120k.

Think about that.

Congrats on your success and on your altruism at the non profit

Thanks for your note and comments. Yes, there is no way I could retire right now if we hadn’t invested in real estate. We would probably have more non-real estate assets if we didn’t have the real estate, but not a whole lot more.

So when I hear financial advisors, and other people who comment on finances in the media, discourage people from real estate because it will be such a headache, I always think to myself that it hasn’t been that big a headache for us, and it sure is nice to have an extra $2 million of net worth throwing off $120,000 of income for the rest of my life!

As I said in my interview, I don’t think real estate is for everybody. But I think many people could benefit from at least at least considering it. One very simple way to get involved in real estate is to buy a duplex and live in one of the units. We still do that, and as I mentioned in the interview, we get paid over $40,000 a year to live in a really nice house!

Even if you don’t think you would like to live in it long-term like we have done, I think younger people should consider buying a duplex and living in it for a while to build some equity, before buying a traditional single family home. Depending on where you live, and the current prices and interest rates, you can often live in a duplex for less than you would pay for an average or even modest apartment. It’s a fantastic way to “live below your means“ and build up some net worth early in life.

Excellent interview MI206. First off I’m glad your colon cancer was caught early. I had a friend from work that died a few years ago, at 44, from colon cancer. It was an eye opener for me that someone that I talked to every week and was my age could get something so terrible. I think about him and other friends lost to cancer regularly.

Sounds like you have won the game and are now taking the time to enjoy the more fun things in life.

Thanks for your comments.

Yes, I feel very fortunate to have caught the colon cancer. If I hadn’t gotten screened at age 50, my doctors say I likely would have died from it because by the time you have symptoms, it’s often quite advanced.

So I tell everyone to be sure to get a colonoscopy at age 50 (some of the cancer organizations are now recommending age 45). I’m still getting my body scanned every 6 months, and will do so for 5 years. If I make it until then, they will declare me “cured.” I was blessed to have excellent care, good health insurance and a tremendous support network of family, friends and colleagues.

Thank you for your story. My dad had colon cancer diagnosis in his 70s, so insurance won’t allow me to get screen until 50 because that’s not considered high risk. I have to go to my primary care doc to get the Rx for colonoscopy this December. I’m wondering if you have to do that every 6 months…that is go to your PCP for 1st appointment for referral and then go to your GI office to get scheduled for the test?

Hi Amy: I’m an ex-oncology (inpatient and outpatient chemo RN) nurse and had to be screened at 35 for colon cancer because my mother was symptomatic with colon cancer in situ (pre-stage 1) at 40. If someone is diagnosed with cancer, their oncologist will follow them for years, including the routine screenings post-treatment he mentions above. The PCP would not really be involved in the following tests, but would be aware of scans/results. For you, if you ever become symptomatic with any bleeding or pain while using the bathroom, contact your PCP right away, reminding them of your family history of colon cancer so they can schedule a colonoscopy with a GI specialist asap. Usually, the PCP will make the referral and the GI office will call you to schedule, though good to follow-up if they don’t get a call out to you to schedule. Also, sometimes*, symptoms (like bleeding/pain) may be early stage with no further treatment other than polypectomies, like my mother’s. Stay on top of it and you’ll be fine. 🙂

OncRN, thank you so much for the thorough reply. This makes sense. My 1st colonoscopy is just around the corner and I’m hoping they find nothing!

I in my case, my primary care physician encourage me to get a colonoscopy and provided an order for that to happen. At age 50 that is usually covered by insurance. If your father had colon cancer, then you are definitely at higher risk. Our son for example will be expected to get his first colonoscopy when he turns 40.

Now that I have had surgery and chemotherapy, I have been getting a body scan every six months to look for a recurrence of cancer somewhere in my body. I did another colonoscopy after one year, and they found some more polyps, so I did another one this year. Fortunately this year there were virtually no polyps so now I don’t need another colonoscopy for two years. I hope that helps answer your question!

I really enjoyed this one, and I especially appreciate the clear focus on giving – including having it as part of your monthly budget. Congratulations on your success and sharing it with others!

Great story! I wasn’t thinking that you were about my age until you said your first job was $3.35/hour. I remember that number well, since I earned it at 3-4 jobs before and during college!

Your comment about finding colon cancer was shocking. I got my colonoscopy at 50 (currently 53), and totally expected to be clear. That must have been a game changer. I agree with you that it’s important to enjoy the journey. One person said to me once (don’t know if he stole it from someone else) – if you don’t enjoy the journey, and you just want to get to the destination, what is the “destination” of life? What comes at the end? DEATH! Think about it. It changed my philosophy of life 180 degrees. We all need to stop and smell the roses!

I’m curious how you built your RE portfolio. Did you save organically to put a downpayment on your first unit, then finance the rest? If so, what was your magic Loan to Value (LTV) number? Currently, I’m putting 25% down on a new purchase, in order to get the best rate, but I fear it might be slowing me down a bit.

Thanks for a great post!

Thanks so much for your note. I’m glad that my interview resonated with you.

Here’s how we built our real estate portfolio. We saved up enough to get our first duplex, I think with either 5% or 10% down. I then did some work on the house. Things like painting the outside and much of the inside, refinishing the hardwood floors, updating the kitchen and bathrooms, but mostly cosmetically. We then got it appraised and were able to refinance it and take cash out to help buy the next duplex. For our third purchase we tried a fourplex, which as I mentioned in my interview, turned out to not be a great fit for us, so we sold that for a small profit, and used that equity to buy our third duplex.

Once my wife became pregnant we decided to buy a new house and ended up purchasing a duplex about a block and a half from the first one that we had been living in. This one was a real fixer-upper. I did a lot of work on this house. My dad was still alive at that time and was a retired construction painter, so he and I painted or refinished every single surface in this entire building! And this particular duplex is a specially lucrative for us because we live about a block from a private college and rent the upper unit to students who are willing to pay quite a lot. It also has a small studio in the basement, so I guess technically you might think of it as a triplex.

This purchase allowed us to rent out both units in the first duplex that we had previously been living in. We bought the last duplex using my $50,000 inheritance when my father passed away.

By the time we were buying the fifth duplex they required us to put 25% down. We just couldn’t find a mortgage that would allow us to do less. So we had to scrape together everything we had to get the fifth duplex.

Then we began the process of trying to get them paid off. As I mentioned in the interview, we focused all of our energy I’m getting one duplex play it off. We then snowballed the net profit from the first one, and added that to the monthly principal payment for the next one. Anytime I got a bonus or any extra cash we would apply that to paying off the next building. Once we had a couple of them paid off, it went really, really fast. I think by the end we were making additional monthly principal payments of more than $12,000.

As we were doing all of this, I was surprised that the banks would lend us this much money. In the early years I wasn’t being paid very much and I was working for a start up nonprofit! We got a little nervous during what has been called the “great recession” when housing values went down, but fortunately, at least in our area, rent stayed steady or continued to increase. So in that sense, it didn’t really affect us.

Show we ended up with two duplexes in one neighborhood, and then the other three in a neighboring neighborhood about 5 to 7 minutes from here. We usually looked for duplexes in decent neighborhoods, that needed some basic refreshing. In one of the duplexes we refinished both basements to create some extra value and rent. We plan to do that with one of the remaining duplexes as well.

I manage them myself. I now collect most of our rent payments by Venmo. I have a handyman who takes care of most things, and if I need a professional I have a set of folks that I turn to, whether it’s plumbing or an electrical issue. To advertise them I use craigslist, and I have started to occasionally use Facebook marketplace as well. I have some decent pictures of each unit, but the best thing I have is a good video tour of each unit. I include that video tour in the ads so that potential tenants can get a really good look at the unit before they are scheduled to take a look. This saves a ton of time since almost no one is shocked or surprised by the actual unit when they come to visit. When someone emails me about the unit I strongly encourage them to see the video first. I keep the videos on YouTube, so when I advertise I can see how many people are taking the video tour to get a sense of how much demand there is at a given rent.

I know many landlords hire a management firm to do all of this, but by my estimation I only spend at most 60 or so hours a year on this. I think I figured out once that even if I spent, say 80 hours, I would be earning the equivalent of about $200 an hour in savings, as compared to hiring a professional property management service. I would say I am a pretty skilled administrator, and most of this comes pretty easily to me. It certainly makes it a lot more profitable if you can manage it yourself.

Anyway, I hope all of this is useful and helpful.

Such a wonderful and inspiring story, and I too am so glad you caught the cancer early. I’m also curious about how you went about building your RE portfolio. And I’m curious about the reading list you wife helped you put together. Would you be willing to share? Congrats to you and your newfound health (losing 75lbs is no small feat!). 🙂

Thank you for your note and kind words.

Here’s the list she came up with:

Maya Angelou – I Know Why the Caged Bird Sings

Arundhati Roy – The God of Small Things

Franz Kafka – The Metamorphosis (short work)

Cormac McCarthy – The Road

Willa Cather – My Antonia

William Faulkner – The Sound and the Fury OR As I Lay Dying (both critically acclaimed)

Carson McCullers – The Heart is a Lonely Hunter

John Updike – The Rabbit Series, the first of which is Rabbit, Run

Sinclair Lewis – Babbitt

Chinua Achebe – Things Fall Apart

Tim O’Brien – The Things They Carried

Joyce Carol Oates – A Garden of Earthly Delights or Black Water (based on Chappaquidick) or Them

Toni Morrison – The Bluest Eye or Beloved

John Steinbeck – Of Mice and Men or The Grapes of Wrath

Pearl S. Buck – The Good Earth (Loved this book. Beautifully written!)

Kate Chopin – The Awakening

Ernest Hemingway – The Old Man and the Sea

E.L. Doctorow – Billy Bathgate

Louise Erdrich – Love Medicine

Barbara Kingsolver – The Bean Trees

Virginia Woolf – To the Lighthouse

Thanks for sharing your story. I’m very glad you got your detection done at age 50 and was able to get the colon cancer resolved. I got a colonoscopy at age 45 (was covered by my insurance without any out of pocket payment so I wanted to get it done) and found a benign small sessile polyp. I very much recommend to check this as it can save lives.

You have done really well with real estate investing. I think getting into an investment habit / system that works for you and sticking with it for a decade or two normally locks in a victory and highly recommend that people start this as soon as they can.

-Mike

Thank you for your story. I, too, was diagnosed with stage 3(b) colon cancer but one year earlier, at age 49. It was a real wake up call.

Would you be open to sharing what market or city your duplexes are in? Perhaps by private message?

Again, thank you for your story and the encouragement to dive into real estate. I’ve been stuck in the analysis paralysis so appreciate the advice to just move forward.

Best line in this interview “it is really important to work hard, do an excellent job, and always aim to exceed expectations. The key, in my mind, is to assume that nobody owes you anything. A misplaced sense of entitlement is a killer. You’ve got to hustle and grind.”