Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview raises a very interesting question: Should a pension (or similar “asset” — for example, this could even apply to Social Security) be included in net worth? And if so, how should it be valued? Without it, this interviewee is not a millionaire. With it, she’s well over $1 million.

I’m making an exception (generally I wouldn’t count a pension, but maybe I’m wrong) and allowing this interview to see what everyone thinks about it. I’m sure the conversation around this topic will be interesting.

This interview took place in August.

My questions are in bold italics and her responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

40. Husband 45 (married for 5 years).

My husband and I have been married before.

Do you have kids/family (if so, how old are they)?

In the home: Boys: 16/11

4 adult step kids (3 boys and 1 girl: 20-26)

What area of the country do you live in (and urban or rural)?

Southern VA-urban area.

What is your current net worth?

My husband and I have chosen to keep our personal expenses separate. We have a joint account for household bills and this system works well for us. I am not sure of his net worth but he does have debt.

$495,573 + pension + Tricare health insurance

Present pension value if I retired today ($1.6 million): $55,000 per year with COLA.

Currently obligated for 5 more years. Present pension value for O5 @ 28 years ($2.5 million): $93,000 per year with COLA.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

- TSP Roth: $40,000

- TSP: $182,500

- Vanguard Roth IRA (Managed-VTSAX/VTIAX): $53,000

- Vanguard Money Market (Managed-VTSAX/VTIAX/VTABX/VBTLX): $119,000 (likely house fund)

- VA 529: $46,000

- Emergency Fund: $26,000 (Took $5,000 out when the market dropped in March 2020 and put into Money Market account)

- Other Sinking Funds: $8,500

- 2020 Honda CR-V: $30,000 brought in Feb 2020 and financed until June 2020

- Debt: None

EARN

What is your job?

I currently work as an advanced practice nurse (APN) in the military. I will have 23 years of service in Dec 2020.

I joined the military at 18 and spent six years enlisted starting as an E-1 and commissioning at E-5.

The military offers commissioning programs where they will send you to school and your only job is to be a student. You usually owe 6 years after the completion of these programs. I did not apply for the program and opted to do it on my own because I don’t like people to choose my faith.

I worked full-time, stood duty (work outside of regular hours), went to school and sometimes moonlighted (EMT & Registered Nurse). By the time I commissioned I had finished two associate degrees and my bachelor degree.

I was commissioned at 24 as a bachelor nurse. By then I was a wife and a mom. Pregnancy delayed my commissioning by six months because I could not go to officer training. Leaving my three month old baby was HARD but it was only six weeks and I knew it would improve my income.

Two years after my commissioning I started working on my master’s degree which would allow me to practice as an advanced practice nurse. For those three years, I worked full-time as a staff nurse on 12 hour shifts 2-5 times a week, completed courses, completed clinical hours on my off days, juggled motherhood/wifehood and I was pregnant with my second son. Looking back I don’t know how I did it but I managed. A benefit of working 12 hour night shifts that I was able to complete school work after patients were asleep.

I had my second son in March 2009 and finished my master’s degree in May 2009. That seemed to be my trend, baby then degree. This degree allowed me to re-designate as a nurse practitioner and I moved to my next duty station. This job change increased my income due to a bonus and certification pay. In the military you also get a pay increase after every two years until you hit a certain amount of years based on your rank.

Promotion for my branch is automatic from O-1 to O-2 and O-2 to O-3 as long as you don’t do anything wrong. O-4 and above are competitive which means your record goes up to a board and you are compared to your peers and not everyone is selected for promotion.

In 2013, I put on O-4 which meant a pay increase. On September 1, 2020, I will put on O-5. I was selected for O-5 in June 2019 but you have to wait your turn to put it on and actually get paid for it.

Due to bonus obligation, I have five more years of service left. As long as I stay out of trouble and don’t have a major illness, I will retire with 28 years of service. As an O-5 with 28 years of service, I will get 70% of my base pay. At 20 years of service you get to keep 50% of your base pay and for every year after 20 years of service, you get 2.5% more of retirement.

What is your annual income?

Taxable: $142,000 ($107,600 + $35,000 yearly bonus). I’m on year 2 of 6 of bonus.

Non-taxable: $37,000 (housing allowance, board certification pay and food allowance).

Child support: $9,840 (Goes into 529s plans)

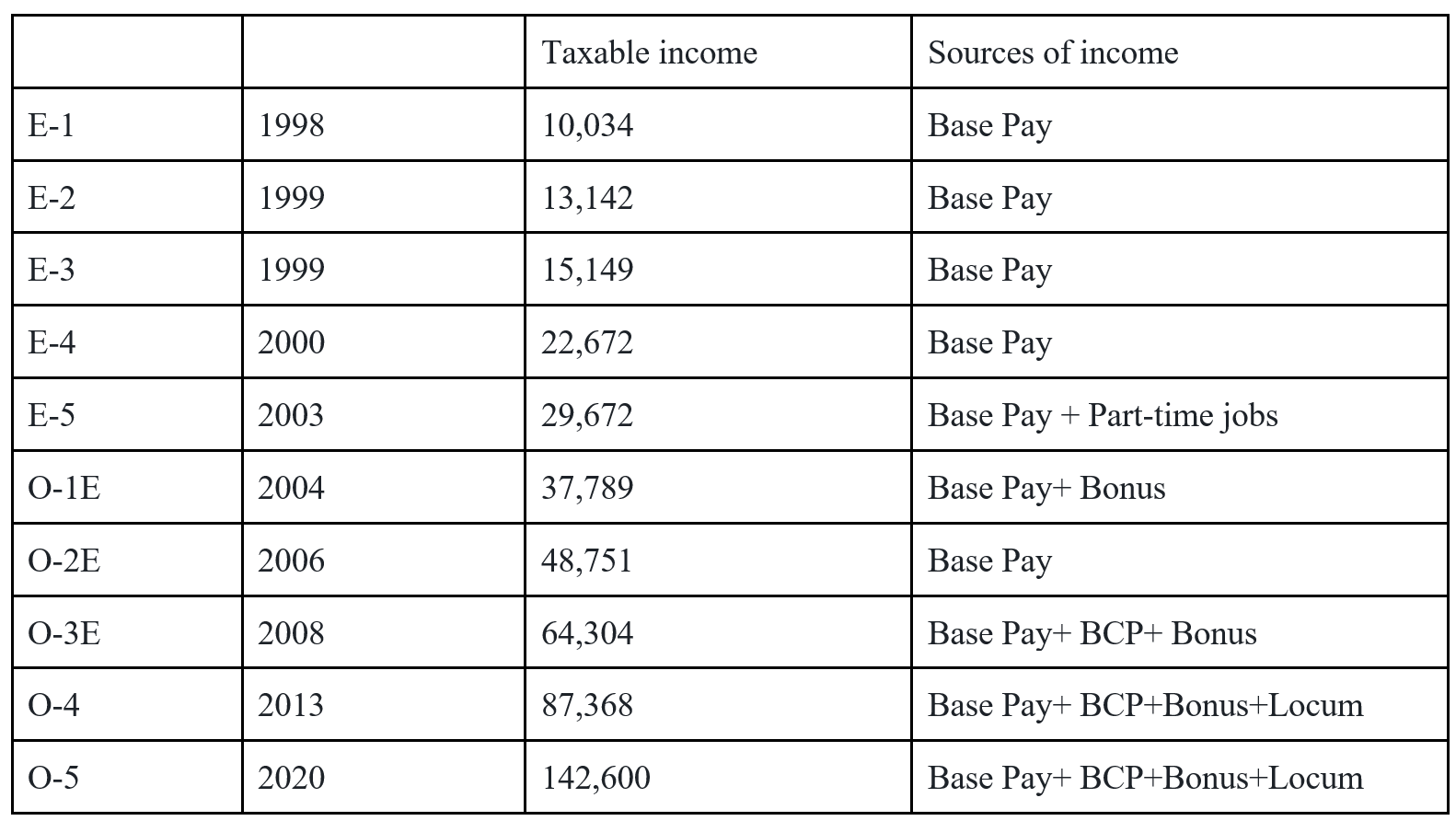

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

I have listed my taxable income below. This chart does not include my non-taxable income (housing allowance, uniform allowance, COLA, special pays) which is hard to track at this time. I spent a good amount of my career overseas which I think is more lucrative.

What tips do you have for others who want to grow their career-related income?

The military is not for everyone but it worked for me. My military career has been kind and stable. The job you pick has a huge impact on your quality of life. My job is not a sea based job. I’ve only been away from my kids for six months in 23 years. At that time I was a single parent and was given a two week notice that I was leaving for six months and I was overseas. Their father and I are not on the best of terms but he will take them if needed.

I always try to make the best of the situation. I have never gone to the duty station that I wanted but I have always enjoyed the adventure while I was there. I am an adventure seeker and like new experiences.

The military paying for my education and my education have been the biggest tools in increasing my income. I have utilized tuition assistance and GI Bill to finance two associate degrees, one bachelor’s degree, one master’s degree and one doctorate degree. The highest student loan balance I have ever had was $11,000. When I used my GI Bill, I had to pay up front for my tuition and the VA paid me later so I took out loans but paid them off aggressively.

Before I commissioned I was thinking about leaving the service but I did a calculation and found that I would make more as an E-5 in the military then as a registered nurse in the civilian world. I don’t pay any healthcare cost and most of my income is non-taxable.

What’s your work-life balance look like?

My work-life balance is currently excellent and I owe that to my doctorate degree. I am in a non-traditional role for my skill set which allows for tele-working and flexibility. Unlike other primary care providers in the military, I am not required to be in the clinic every day which is a nice change.

If anyone is not aware of the work-life of a primary care provider, most providers see a patient every 20 mins and then they are responsible for charting the visits after hours. This cycle day in and day out is mentally and physical exhausting.

I have one year left in my current position and will return to a traditional provider job at that time.

We like to travel as a family and the military gives us 30 days a year for vacation. The boys and I have visited Italy, France, Germany, UK, Netherlands, Austria, Spain, Romania, Australia, Korea, Japan, Vietnam, Indonesia & Panama. Before COVID we had plans to visit Spain and Japan again this year. We are economical travelers so we try to balance cost with experiences.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

I moonlight sometimes for locums. I value my time off from the military so I rarely do it but the pay and light workload is nice.

I also like to see how the civilian world works.

SAVE

What is your annual spending?

As mentioned above, my husband and I have opted to have a joint account for our household expenses and separate accounts for personal expenses.

- Household: ~$40,000 (comes from joint account)

- Personal: Expenses: ~$12,000

- Save: ~$60,000

- Give:~$17,000

What are the main categories (expenses) this spending breaks into?

Joint (monthly)

- Rent: $2050. We have chosen to rent because we like the flexibility and less responsibility. I think it also saves money because you don’t do upgrades because it is not our home. We have been able to negotiate our rent down twice in the last three years.

- Utilities: $600

- Groceries: $400

- Dining out: $200

- Vacation Fund: $200

Personal (monthly)

- TSP: $832

- Dental: $30 (for kids)

- SGLI: $27 (military life insurance)

- Life insurance: $72 ($1,000,000 30 year term)

- Kids: $300

- Fun: $400

- Gas: $100

- Clothes: $200

- Christmas Fund: $150

- Vacation Fund: $400

- New Car Fund: $333

- Sunshine Fund: $150

- Tithes: $1140

- Life Insurance: $72

- Car Wash: $25

- Non-profit: $50

- Roth IRA: $500

- Savings: $2000-2500

Do you have a budget? If so, how do you implement it?

I use zero based budgeting each month but I am not strict.

My savings comes out automatically so as long as I have cash in my checking to cover my credit card bills, I don’t pay that much attention.

I try to put most of my expenses on my credit card for points but pay my bill off monthly.

What percentage of your gross income do you save and how has that changed over time?

These are my current savings rates. I like using sinking funds which are included below.

I am definitely a better saver now then I was in my younger days. I find the use of sinking funds helpful.

- 33% long-term savings (retirement, new car & house savings)

- 9% short-term savings-plan to use in next 12 months (Christmas, vacation, car fix)

What’s your best tip for saving money?

Don’t pay interest. I can’t believe I used to give away $150 a month in interest.

Make it automatic. One less thing to think about.

Make a written budget and compare it against your actual spending. I know I could save more money if I wanted to but I am trying to balance enjoying life now because tomorrow is not guaranteed.

What is your favorite thing to spend money on/your secret splurge?

I love to travel. Once I retire in 5 years, my plan is to work part part part-time to fund my vacations. I am hoping to work eight hours a week but I don’t think I will find a job that will allow it. I will likely do locums until I’m 60. After being in the military for so long, I crave the freedom to come and go as I please. If I want to travel overseas now, you have to fill out numerous forms and submit requests to certain people and I will not miss that.

I also like to spend money to help others. I have a sunshine fund line on my budget and I will buy things that local teachers need, donuts for staff or donate to a GoFundMe campaign. I also like buying gifts for my kid’s teachers. Teaching like nursing is a thankless job so I try to show my appreciation with gift cards to their favorite restaurants.

INVEST

What is your investment philosophy/plan?

My investment plan has been to set it and forget it. My savings comes out automatically and once you make changes to your budget, you get used to living on less.

I use Vanguard Personal Advisor Services because I don’t want to worry about rebalancing. I think the fee is reasonable.

Choose FI has helped me to understand investing better.

What has been your best investment?

Myself. The sacrifices I made earlier in life have paid off. I am thankful that I have made it this far with my health, pension and healthcare.

I hope to pass the lessons I learned to my kids and it will help them rise to the next level.

What has been your worst investment?

1. Paying high fees for investment accounts through my bank. You assume the bank is looking out for your best interest and that is not the case. I didn’t have family or friends to guide me. I am thankful to Podcast and Youtube for teaching me the way.

2. Placing money in “safe” funds because I didn’t want to lose money and not realizing safe funds don’t keep up with inflation. I know better now and realize that the stock market always bounces back and I have time for it to bounce back.

What’s been your overall return?

I have no idea.

How often do you monitor/review your portfolio?

I look at my balances on my TSP and Vanguard daily and do a net worth update with all my accounts each month on my spreadsheet.

NET WORTH

How did you accumulate your net worth?

My wealth came from saving and my twenty years in the military. I never planned to stay in the military but I am glad I did. I am thankful for my lifetime pension and healthcare.

I did sell a house in 2017 which netted me ~$30,000. When I think about the repairs I made during the 10 years that I owned it and the repairs I had to do to sell it, I think I broke even or lost money. You live and learn.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

Earn. The military has funded my education which allowed me to earn my current income.

It is harder to save and invest if you don’t have the money to cover your living expenses. Covering my living expenses has never been a concern for me.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

Making bad choices with my money such as buying a home, credit card debt, co-signing on a loan and putting money in high fee investment accounts have been some of the road blocks during my journey but you live and you learn.

I hope to pass the lessons I learned to my kids and to be more open with money with them so that they avoid my mistakes.

What are you currently doing to maintain/grow your net worth?

I continue to work and save.

I always hope to tighten my budget and reduce spending in categories that don’t bring me joy but it is a balancing act.

Do you have a target net worth you are trying to attain?

My goal is to save enough money to pay cash for a house in 5-10 years.

My pension will cover my expenses so anything else is extra funds for my travel.

How old were you when you made your first million and have you had any significant behavior shifts since then?

TBD but Personal Capital is predicting 47.

I personally consider myself a millionaire. I have a pension that will pay out for the rest of my life and is currently valued at over a million. If I passed away today, my son’s would get over a million in benefits from my personal savings, my insurance policy and the military.

What money mistakes have you made along the way that others can learn from?

Buying a house does not always make sense.

I bought a house in Texas for my sister to live in because I thought it would help reduce my tax burden. I’m not sure if it did. If I could take the money I spent helping her with the mortgage, repairs and other expenses and put it in the market, I’m sure I would have done better in the long run.

Credit card interest. If you can’t pay it off by the end of the month, don’t buy it

Don’t co-sign for anyone. If they can’t get it on their own, they don’t need it.

Investment fees can eat away at your earnings.

What advice do you have for ESI Money readers on how to become wealthy?

You will have to be willing to sacrifice.

I left home at 18 and I have missed many holidays and birthdays due to my military life. Personally as long as my kids are with me, I am okay. When I look at the lives of many of my peers I know I am doing better than 99% of them because I chose to leave home and join the military. I don’t think many people are willing to make that kind of sacrifice.

I also made sacrifices to complete my schooling. I worked full-time and went to school. When I was pregnant with my last son, I was either working or doing clinicals seven days a week. The night I went into labor, I worked a 12 hour shift and got off at 7 pm and went into labor at 11 pm that night. I knew that short term sacrifice would give way to long-term gains and I was rewarded for my sacrifices.

FUTURE

What are your plans for the future regarding lifestyle?

My pension will cover all my expenses. I want a larger vacation budget so I will work part part part-time to fund that.

I will retire fully at 60 and start withdrawing from my TSP. I plan to start withdrawing my social security at 62.

What are your retirement plans?

On a typical day I want to be able to wake up around 7 am and workout.

I don’t have plans for the rest of the day but I would like to help with reading programs for children at community centers.

I would like to fund a reward program to motivate them to read. My youngest son had some trouble with reading when he was in early elementary and I am thankful I had the knowledge (research different programs), work flexibility (child could not participate in after school tutoring program if they are not picked up by 3:30pm) and money (tutors are not cheap) to get him the help he needed. I can see how children can be left behind.

I want to be able to spend time with the kids and grandkids when I want. Since we are a blended family I am not sure how that will look.

I also want to do weekend trips, one overseas trip, one stateside trip and one cruise a year.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

My pension is pretty solid but I wish I had saved more in my retirement accounts.

I hope I get to enjoy my retirement because life is not guaranteed. My oldest son was diagnosed with cancer 18 months ago and you realize how life can change in a blink. He is doing awesome but life is not always fair.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

In 2013 (33 years old), I noticed I was paying over $150 a month in credit card interest and I couldn’t believe I was just giving someone $150 a month.

After that, I made a plan to pay off my credit card and started listening to Dave Ramsey and Suzy Orman. Following their advice, I become more interested in saving, being debt free and never paying another cent in interest.

Who inspired you to excel in life? Who are your heroes?

I always said I wouldn’t have children until I could afford to take care of them on my own without help for anyone. My father was not involved in my life and my mom struggled.

The well being of my children motivates me.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

My favorite podcast is Choose FI & Afford Anything.

Women Who Travel. I love to travel.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

Giving is my love language.

- I tithe 10% each month to my church. I am blessed and realize life could have been much different.

- I give to Patreons like Humans of New York and Hasfit.

- I also give to a friend’s non-profit in San Diego.

- I believe in giving teachers gifts. I think they have a thankless job and I want to show my appreciation.

- I also give randomly to GoFundMe funds when I see campaigns that I am drawn to.

- I like to buy food for co-workers to help them make it through the week.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

I plan to die at 100 and I do not plan to leave an inheritance. I plan to help them during their lifetime and make parenthood easier for them. I’m not sure what that may look like but it could mean helping with home down payment, funding 529s or paying for kid activities.

If I have money left when I die, I will give to Planned Parenthood. As a woman, I know that family planning has a big impact on quality of life and long-term earning potential and I want to limit barriers to family planning.

First and foremost I want to say “Bravo Zulu” for a very good life experience and dedication to your plan. As a Military retiree I completely understand the challenges that you have faced and completed with determination and patience. The question of whether to count your “pension” benefits is moot. I have always considered my pension money earned and saved. Many count Social Security benefits as the same. After 30 years of service, traveling with assignments overseas, wartime service and separation from family, I earned every dollar I get rewarded with monthly. Good work young lady, and continue to persevere in your endeavors. As you have stated, no guarantee of tomorrow. Semper Fidelis.

I too thought about selling my house and renting, but after doing some numbers and thinking long and hard about how it would make me feel, I decided owning is still cheaper not to mention everything I do (repairs/upgrades) only secures my equity. I believe your previous mistakes as you identified shaped your views on homeownership. Question: You stated, “I will retire fully at 60 and start withdrawing from my TSP. I plan to start withdrawing my social security at 62.” I’m curious why you made the decision to take SS at 62 when you stated your pension will cover all of your expenses. Why not wait to take your SS at a higher amount if you don’t need the SS to live on?

FloridaGirl-

Home-The home was in one state and I was in another state so it made everything harder when dealing with the home. Traveling to the area to deal with the home’s needs required me to take vacation days which is not my idea of vacation. I did not have the mental energy to deal with the ups and downs of being a landlord.

I do plan on taking SS and TSP early. I do not plan on leaving an inheritance and will use the money for travel and life experiences. I do not expect my SS to be large due to the fact I plan to make about $25,000 yearly from 45-60 so it will only be fun money. Yes, I could wait another few years for larger amount but nothing is guaranteed. My plan is not set in stone but this is my current plan until I decide otherwise.

I think this definitely qualifies for a millionaire interview. Very impressive path. Intelligent, generous, and motivated. I am guessing a prenup was part of this second marriage. She has worked too hard to be set back!

100% agree!

Betsy-Thank you for your words of encouragement. We do not have a prenup and we never discussed getting one. My husband has a similar background as myself so I didn’t feel the need to get on. I’m sure 99% of people never thought they would need a prenup so I’m not naive but if you knew him then you would understand.

Not to be Debbie Downer here, but it is a statistical fact that 70% of second marriages with minor children involved end in divorce. I’m happily in the same boat and believe beyond a shadow of a doubt that like you, we will both be in the 30% that are able to thread the needle and stay happily married forever. This being a financial independence blog though I can’t help but be alerted by a couple of red flags: 1) You honestly have no idea what your husband of 5 years net worth is? 2) Your husband has debt, but you don’t know what it is or how much?

I’m not trying to pick on you, I only bring this up from a position of wanting to be helpful to others out there in our situation of finding love later in life as we both found our soulmates after creating financial security for ourselves. I don’t have any issue with someone not having a pre-nup (we did but with much larger $’s involved), but not talking openly about finances with your partner can be a recipe for disaster. I sat down with my wife a year before I asked her to marry me and we discussed this openly, zero secrets, it was hard and eye-opening for both of us.

People in general need to keep in mind, a spouses actions and liabilities could 100% derail your future ability to retire. If a person is cool working an extra 15-20 years because having the talk about money was just too hard of conversation or your are worried about offending them, then feel free to roll the dice…30% success rate is good enough for me. I’ve just witnessed too many people in the 70% camp that wish they would have known the facts and talked about stuff up front.

Thanks for your service and good luck!

Great interview! So glad it was included. It brought a very different element which I really liked. If you’re thinking of the millionaire threshold as a proxy for someone who has obtained financial security then this hits the mark! Jut a great lesson that financial security can be obtained without being a senior executive earning a massive income. Hard work and savings gets the job done. Well done!

She’s going to bust through a million with or without the pension so sure she’s a great subject for this interview. I wonder about Social Security, federally backed pensions or even annuities. They definitely are hugely important in retirement in terms of providing a large passive income stream. But they are kind of like your income from a job. That is never counted as part of net worth, it is just a means of growing or preserving your net worth. So even though my Social Security will pay me almost exactly what an invested amount of $1.625 million would at a 4% SWR I’ve never added that to my net worth. One reason, I guess, is it stops when you die, all other net worth assets can be handed down.

Although I agree pensions and annuities shouldn’t count towards net worth, I kind of like adding it in, that’s puts us closing in on $20M then if we do which has a nice ring to it lol!

Definitely a millionaire in my book, awesome income pops in the last couple years too. Present value of money on future cash flows is a thing too.

Thank you for your service and sharing your story. You did great!

Well done and congratulations on your military career! Starting as an enlistee at 18 to commissioning and now with a doctorate is a very impressive feat that took extreme amounts of discipline and hard work.

I definitely agree that those with secured federally backed pensions should be included in the millionaire interviews. I also like how you list your net worth as investments + pension + medical coverage, as each is different but have their own value that must be included in one’s overall financial picture.

Pensions are a tricky beast. First, let me say that at 39 I wish I that I had one and am jealous of those that have *some* certainty around their retirement income. With that said, pension is not money in the bank. There are a number of multiemployer and public pension funds that are dramatically underfunded. If the funds were to default on their obligations, the PBGC’s benefit can be dramatically less than what was “promised”. Single employer pension plans should have a higher level of safety as the PBGC’s benefit is higher and I think there is higher funding requirements to prevent them from getting behind. What does this risk mean? Well, in the whole scheme of things the risk is probably much less than the savings the rest of us have in brokerage, bank, real estate, and other holdings.

Should pension be included in net worth? I’m of the belief that unless it’s money that can be spent, it shouldn’t be included. If the recipient were to die tomorrow, would that money go to beneficiaries? My 2 cents is a cash buyout or death benefit could be included in net worth. Otherwise, it’s a bit like including future dividend streams into net worth. Can we plan on it? Kinda. Is it probably safer to wait until it’s paid? Definitely.

This matches my thoughts.

I don’t think pensions, SS, inheritances, etc. should be counted in net worth because they are not yet realized (and may never be).

This is a federal government pension, so 100% guaranteed to be paid, so I am good with counting it, but using your thoughts, does that mean I can count my military pension since I have retired and am now drawing that pay? That is, did my net worth jump by millions when I retired?

BTW, I have seen some people count it before they hit 20 years – that is definitely wrong. I have seen people leave the military at 18 years, so things can happen and it doesn’t count until you earn it, but once they hit 20 they are getting the money.

Thanks for including it, great read.

100% agree with this comment. A military pension not being received would occur only as a result of something catastrophic happening in this country and if that were the case, every one’s net worth would be in question. The whole “in God and the dollar we trust” would be in question. She has a pension if she retired today. No doubt in my mind it should count. Thank you for your service…ex USAF here but didn’t take the career path.

Thanks for your service Kevin. I never intended to stay, so at 28 years finally decided to stop! Ha ha

Kevin and Scott – agree chances are low that the pension goes away, but I can envision a scenario where the call becomes – “$$ for active duty soldiers or pensions”, “$$ for planes/drones/armor or pensions”, or some variation; so a cut in benefits while politically difficult is not out of bounds.

State govt. employees are already dealing with this issue btw. The pandemic led cut to state budgets and no federal support is threatening a collapse in state pensions.

Just my $0.02

I could totally see how somebody not in the US Federal government might think that but huge differences exist.

State governments fund their pensions through pension funds, employee contributions, tax payers, etc. Also, their budgets must (somewhat) balance (if there is a shortfall). The US government has no military retirement fund, it is a line item in the annual budget and of course the US has carried debt the entire history of the country. So only two ways they don’t pay. 1) The government defaults, which is almost impossible (unless the entire world is defaulting or the US is no longer the US). 2) The US decides to reduce a promised (by law) entitlement. I was in the military from 1984 to 2020 and they have talked about the expensive retirement the entire time. Last year they finally did something (after many commissions and studies) and did a relatively small change but only for new recruits or people who chose to switch. That was a monumental hurdle and took years and a lot of political capital a d it only affected people who would know what the deal was before joining, so reducing an existing entitlement of such huge political proportions has the same chance as the US defaulting (IMO).

Of course it is all an academic discussion and there is no wrong answer. Truth is we need something other than just net worth to commonly measure your retirement financial health, as cash flowing assets don’t always equal a huge net worth amount. On the other hand, these days not that many people are as blessed as those of us with a federally provided, inflation adjusted, surviving spouse gets 55%, pension!

Thanks for providing the forum and allowing these conversations.

I missed vesting in my pension by 450 days. It happens. I keep the money I put in, but I don’t get the match, which would have been 225% of what the value would be when I take it, which would have been about $100K.

Agree that pensions should be counted differently than real investments, real estate, etc., but they need to be included as part of one’s financial health, as while not the same as real property upon one’s death, a high-confidence pension has a substantial impact on one’s financial picture and independence while alive. That all said, in my opinion the best way to capture this in net worth is how this interviewee did – $x + $annual pension.

I don’t count my wife’s pension in my net worth, but I count it in my cash flow in retirement when the money starts to roll in.

A military pension is as close to 100% guaranteed as you can get. Uncle Sam will just keep printing money to pay the obilgation, not something a State or private pension can do.

You can also do a Survivor’s Benefit Plan and insure 50% of your pension to your spouse should you pass first for relatively cheap.

That being said, I don’t include my military pension in my NW, but do factor it into my “retirement number” in that it will cover about 50% of my desired income.

Agree.

While I applaud anyone on the right track to financial security, I don’t believe pensions and social security should be included in NW calculations.

There are no guarantees for tomorrow, just where we stand today.

I would think the question about pension and SSN is what’s the risk of pension and SSN becoming unsustainable and unable to pay for the life time as expected.

“Expected lifetime” is where you run into the problem because no one is promised even tomorrow. A pension is an income stream and not a fixed asset. In my case, I had 2 options; I could take what the company contributed toward my pension as an annuity payment and the voluntary pension that I paid into could either be an additional annuity payment or a lump sum. I took my piece as a lump sum so that is part of my net worth because I have it and I control how to invest that money and it is now part of my estate that can be passed down when I pass away. The monthly annuity is not something I consider in my net worth because no one knows for sure how many payments I will actually receive and when I pass, there is no remainder that becomes part of my estate.

None of this changes the value of the story but I think passive income streams and assets that are part of the net worth are a bit apples and oranges and not a true reflection of what someone actually owns or what they are worth vs. what they will receive in future payments.

My thinking is similar. Pensions, social security and annuities are different and more restrictive than their equivalent lump sum values. I don’t count our expected SS benefits in our net worth figure. I also agree “None of this changes the value of the story”. I honestly don’t care what the millionaire police thinks and seek wisdom wherever it can be found.

Congrats on the hard work, juggling and the education commitment to invest in yourself. These types of stories reflect what the mission is ( HARD WORKING) vs some of the trust fund millionaires that I know….and despise…just my opinion only.

I would include present value of a pension, as it’s effectively comparable to a defined contribution retirement plan (401k or IRA). In both cases, there is real value, however, in both cases there is also a liquidity issue (i.e. you cannot access the value of these things, in some cases at all, in other cases without substantial penalty). In the case of a pension, though, there is another risk, which is the pension fund becoming unable to pay the full promised pension amount. Not sure the best way to value that, other than just to know that, qualitatively, it is a risk. Pensions turned over to the PBGC end up paying sometimes $0.30 or $0.40 on the dollar.

I would not include the value of Social Security. Prudent retirement planning for anyone under the age of about 55 or so includes zero Social Security. If we get any, consider it gravy.

I think current estimates are that 73% of SS benefits will be payable beginning in the 2030s. So I plan at 73%.

Not counting social security in your retirement plan because you don’t think it’s going to exist becomes a self-fulfilling prophecy, at the population level.

Can you talk about why and how you convinced/come to terms with your husband on having your financials separate with a separate joint account? And if you did get a prenup. How did you go about asking before marriage?

Regina-No prenup. See comment above.

My husband and I both came to this relationship with other responsibilities, spending styles and saving styles. Our joint account has worked great for us. Would I do all joint if he wanted? Yes. Do I want all our accounts to be joint? No, don’t break what is not broken.

We discussed debt and credit ratings before we married so we were both aware of our financial status before marrying. Early in our marriage I wanted us to pay off his debt but he refused.

Vested rights to annuity payments from pensions or other secured/unsecured sources is an asset.

Perhaps what you consider in computing your own net worth is the net present value of these types of vested payments, and similar vested annuity streams, like Social Security.

Another terrific interview. I believe that a guaranteed pension should count for one’s net worth calculation as frequently it is the government or military that offers this benefit in lieu of a 401k match. It is also easy to estimate the value of a pension as all one needs to do is to calculate what a SPIA would cost to produce the same monthly income at the appropriate age.

We do not count pension as an asset; however, its difficult to ignore such a sizable future income stream. Similar to OP, we are looking at 60K per year indexed for inflation plus two social security streams. We have planned as if none of these three exist and thus have over-saved.

Sorry, but your reply makes no sense. Please clarify.

If the NPV of a defined benefit pension is 1.6MM, we ignore that value when calculating net worth. For planning purposes, though, we cannot ignore a future 60K per year income stream. I consider the pension, as well as SS, a deferred annuity that will start at 66 and provide 110K-120K income when you sum the three sources. Hopefully this clarifies; if not, maybe a millionaire interview!

Agree with you on calculating the value!

Since we do not include pension include in net worth, we saved as if it will never pay out. Conservative. As a result, one can argue that we saved too much.

Thank you for your service. You have a very impressive story, and I appreciate your giving nature, and especially your commitment to leaving whatever is left to Planned Parenthood.

As a fellow mom, I wanted to comment on your outlook as a parent, because it’s not something you read about often here (or anywhere really). I agree 100% on waiting to have children until you can afford them on your own. This was my motivation for settling down first – with a house in a nice neighborhood, strong income, and investing in myself as much as possible. I wish more young women would take this approach!

Best of luck to your family, and especially your oldest son.

Awesome job M211! I understand the argument against including a pension in one’s NW since it is not inheritable (unless you add the survivorship benefit mentioned above), but I think it would be an unfortunate mistake to discount a military pension when retirement planning. $55-$93k per year with COLA from the military (important distinction) is significant and to ignore it would cause M211 to unnecessarily delay her retirement.

M211 – coming from a blended family situation myself as a high earning/millionaire mom (separate from my spouse), my unsolicited advice, assuming intend to pay for your kids’ college and you don’t expect much help from their dad, is to bump up the 529 contributions for the next several years, beyond just converting child support payments into the 529 plan, as paying for college can be tricky in a blended family, and having the money set aside for your kids in their 529 plan in the form of a “completed gift” is a really nice form of estate planning in case you pass away prior to college, and security against (i) losing your job and not being able to cash flow any of it (again assuming you can’t count on their dad and you don’t want to ask your husband for help), (ii) burn out and want to retire early or reduce your hours, (iii) are blindsided by a second divorce, (iv) become disabled, or (v) some other emergency (or nonemergency) comes up in your blended or extended family and you are pulled into it.

Thank you for your insight. Concerning the kid’s education, my home state of Texas offers a program called Hazelwood Act for military veterans or a dependent that will cover the tuition cost at a state school. Their dad was also military so we will each use the benefit on a child. I should have enough to cover housing and books. I would consider cash flowing if needed. I am also okay with them working a few hours a week to cover small expenses.

Wow! I’m stunned – such incredible hard work and determination! Amazing interview! Starting at E-1 and working all the way up to O-5 is no small feat. I’m really impressed with your journey, especially working full-time, standing duty, and going school while occasionally moonlighting. You certainly deserve all of the success that the future will hold. Keep up the great work!

I think this is a fantastic post for illustrating why net worth itself is insufficient as a retirement planning metric. We tend to use net worth as a proxy for whether someone is wealthy, and wealth as a proxy for ability to retire and be financially independent, but there are plenty of folks out there with high net worths that are not independent of their income. I think if the goal of working to retire is freedom of choice and the ability to do what you want with your time because your needs are covered by retirement income, then OP nailed it…regardless of whether they can be considered a “millionaire” based on net worth calculations.

I’d trade my millionaire status for the ability to retire at 45 in a heartbeat.

I wouldn’t say net worth is a proxy for wealth, I’d say it’s the measurement of wealth. It determines a person’s level of wealth.

But I do agree that what it takes to be FI is not simply net worth.

You need to know:

A. Non-working expenses — living expenses if you didn’t work

B. Non-working income — What income would still be there if you didn’t work (i.e. dividends, real estate earnings, etc.)

C. Liquid assets — That you can withdraw from at 4% (or whatever number you deem correct) to help support your non-working lifestyle

Then, if (B + C) > A, then you are FI.

If (B + C) < A, you are not FI no matter what your net worth is.

Perhaps our labels aren’t adequate. Like nearly everyone else, I run three general calculations: one is the combined value of my assets, including equity in our home and rental property. Two is our combined investments that could be sold and/or generate returns we use for whatever purpose we want. And the third is our cash-flow in and out, which includes pensions and social security.

We don’t all agree on how to label these three spreadsheets. Should net worth include our home? Should NW include the NPV of pensions and social security?

I do use my home in my NW calc, but not pensions. And I only draw from investments when planning future cash-flow requirements (not my home’s value). But my pensions do reduce the needed draw-down on my investments which implies the NPV of my pensions is real, whether I calculate it or not.

We recently had a webinar featuring David Blanchett head of Retirement Research at Morningstar. He talked a lot about the role of pensions and immediate annuities in Retirement Planning. He views both as “financial assets” and therefore they should be considered as part of your overall net worth.

I don’t want to take away from M211, because I would be more than happy to trade spots with her. Well done! It’s a great interview, and I do enjoy seeing different journeys from the more traditional high income families.

However, for the sake of the conversation about calculating net worth, I’d like to vote for using the more traditional definition of net worth ‘millionaire’, which would exclude NPV of pensions from being included. Yes, they are very important for calculations and very desirable for financial strength, I just like to use a more standard definition.

This topic has actually been top of mind recently, as I’m beginning to invest in real estate. The idea of not just having a net worth, but having a net worth PLUS expected monthly income is extremely powerful and desirable. Hopefully I’ll get there soon!

I have to address the issue of the value of a pension in calculating my net worth as well. I actually described how I do it in my profile (#91) – my choice was to only include the present value of the pension account, because I (or my beneficiaries) are guaranteed to receive it.

Congrats, #211, on your financial success!

I read Todd Tresidder’s book “How Much Money Do I Need to Retire?,” and when I was done, my focus was more on cashflow than balance sheet. I now track both net worth (which does not include NPV of pensions or social security) and cashflow over time (which does include both, although only a percentage of social security given its funding issues and probable means testing).

You can get a much better feel for what your retirement income will be by looking at cashflow, and it takes away a lot of uncertainty about sequence of return risk, having to guesstimate inflation and overall return 30-50 years out, and also the fairly morbid approximation of your death year.

By knowing your net worth and cashflow, you can decide if you want to trade net worth for cashflow, too, and when. Is the annuity worth it? Should I get a deferred annuity only to cover basic expenses after I turn 85? Things like that.

It makes much more sense to me than saying “okay, I will die at 92, inflation will average 3% annually, and I will get a blended 6% return on investment.” What are the odds that will happen? 🙂

And this is consistent with my wife’s philosophy of, when presented with “either/or” scenarios, choosing the “and” one. Why not track both? 😉

The story is inspiring and demonstrates the author’s persistence and resilience.

Clearly pensions and estimating a cash value in case of early retirement/death as compared to life insurance policies is that the former is accumulated thru service and work. Pensions like SS benefits can be changed by Congress though and the fiscal deficits we seem to be accumulating at the pace we are – this to my mind is a serious risk.

For our own case, my wife and I don’t consider life insurance policies as part of our net worth. We also don’t consider SS as meaningful for our retirement plans – the trust fund is projected to run out of cash soon. It is run as a Ponzi scheme for all intents and purposes and it is a fool’s errand to count on that for the long term.