Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in February.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I am 48 years old, and my wife is 47.

We have been happily married for 13 years, so coming up on 14 years now.

Do you have kids/family (if so, how old are they)?

We have two kids, aged 12 and 11.

They are at that fun age where they are starting to ask deep questions, also about money, which I love.

What area of the country do you live in (and urban or rural)?

I live in Singapore. I am originally from a small town outside of Munich, Germany, but have lived here for over 20 years now.

I would not want to live anywhere else at this point. The quality of life, people, weather, food, and the proximity to so many fascinating countries, it all just works for our family.

What is your current net worth?

My current net worth is $7.3 million.

I do not come from money. No inheritance, no trust fund, or the like.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

I structure my portfolio around what I call “eight pillars.” I believe the foundation of a well-diversified portfolio should stand on multiple of those.

Below is a quick breakdown:

- Private equity: $2m. My largest pillar and where my entrepreneurial background lives. I hold shares in four private companies.

- All-Weather Dividend Portfolio: approximately $1.8m. This is my flagship portfolio, consisting of what I consider the world’s best buy-and-hold-forever stocks. I try to buy attractively priced shares of companies that most likely will still be around in 50 years.

- Digital assets: approximately $1.2m. Simply put, I’m grateful for this asset class as it has been quite profitable for me since 2017.

- Cash: $1.1m. $500k of the cash works hard for me in the form of my stable coin farm.

- Physical metals: $616k.

- Thematic portfolios: $375k. These are smaller, focused bets on specific investment themes I have high conviction in, such as Uranium and Tesla at the moment.

- Real estate: approximately $280k. I own one small rental property in Germany.

- Debt: I have $110k outstanding on my mortgage, which my tenant covers.

EARN

What is your job?

I left my last corporate role in 2017 and have not looked back. Before that, I built and ran my own marketing service firm before I was lucky enough to sell it.

Today, I work as a ‘silent activist investor’ for those companies I own shares in, and as a DIY investor. I advise and am on the board of three of the four companies I own shares of, but there is no employment contract, no boss, no meetings or commute.

I also run the financial blog wisestacker.com, where I openly share my portfolio, trades, and passive income. It started as a way to organize my own thoughts, but it has grown into a small community of investors I love exchanging ideas with.

What is your annual income?

I do not earn a traditional salary. Some of the companies I own shares in pay me a small consulting fee to be available in the form of a pay-for-access retainer.

I made $36k this way.

Every other dollar that comes in is passive. In 2025, I made $144k in the form of dividends from private companies, dividends from my stock portfolio, yields from stablecoins, staking rewards from digital assets, and some smaller income streams from real estate and other sources.

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

My first real job out of college was as a project manager in the marketing department of an online bank in Germany, similar to a Charles Schwab equivalent. I started at around $35k per year.

The pay was modest, but the two years I spent there gave me a solid understanding of how marketing departments work and, more importantly, it surrounded me with people who talked about stocks and investing nonstop. That planted a lot of seeds.

After that, I made the leap to Asia and started building my own company. For the first several years, my income was inconsistent and often disappointing.

There were stretches where I paid everyone else’s salary but deferred my own. Building a company from scratch in a foreign country is not glamorous.

It is stressful, lonely at times, and full of setbacks.

But things slowly changed. The business gained traction, and eventually I sold it for $1.5m in shares and $500k in cash. That was the turning point.

From there, I focused entirely on investing the proceeds and building multiple passive income streams.

My income went from around $35k as a fresh graduate to $180k in passive income today, but the real difference is that I no longer trade my time for money. The income arrives regardless of what I do on any given day.

What tips do you have for others who want to grow their career-related income?

I am probably not the best person to give traditional career advice since I left the corporate world fairly early. But here is what worked for me and what I believe applies broadly.

First, work hard in your 20s and 30s. As the old adage goes ‘There is a season to sow and a season to reap, and you cannot do both in the same season’. Those early years are for sowing.

Second, learn skills that compound. Marketing, sales, negotiation, and basic financial literacy are skills that keep paying dividends for decades.

Third, do not be afraid to bet on yourself. Starting my own business was the scariest and best financial decision I ever made.

And fourth, no one will care about your money more than you do. Whether you stay employed or go the entrepreneurial route, take ownership of your financial education. Do not outsource that to anyone.

What’s your work-life balance look like?

Honestly, it is fantastic, and I am deeply grateful for it. I work from home and have done so since 2017.

My wife and I have an arrangement that simply works for us. I follow a consistent daily routine because it sets the right mood for making sound decisions.

As investors, our compensation is not tied to time but rather to the quality of the decisions we make and the patience we exhibit. On a typical day, I wake up at 7pm, make breakfast for my kids and get dressed.

Then I meditate before I plan and structure my day. I might spend an hour or two advising one of the companies I am invested in.

Play tennis or have lunch with an interesting contact.

I usually have one Zoom call per day. I am an introvert, hence I try to limit my interactions to 1-2 per day.

By late afternoon, I am done. The rest of the day belongs to my family. I pick up the kids, we have dinner together, and I have time for hobbies and exercise.

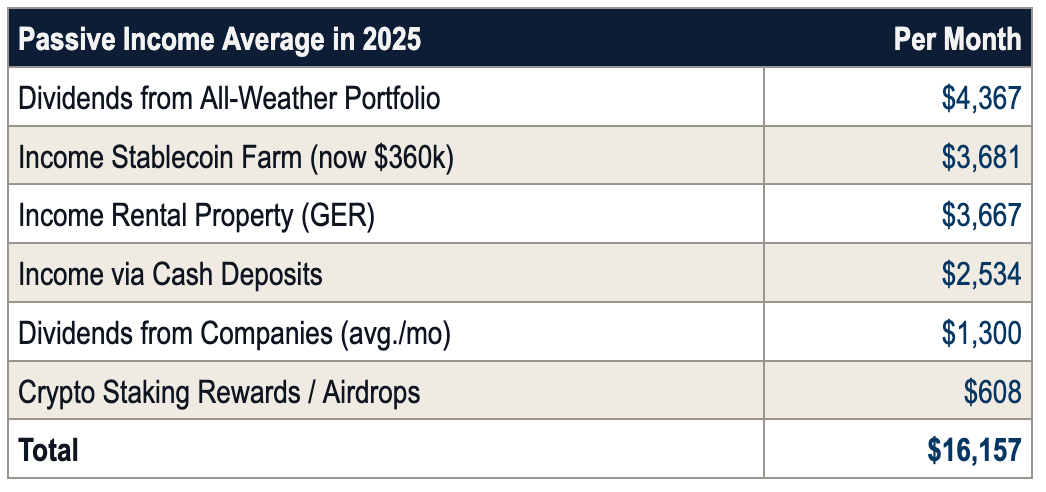

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

Since I do not have a career in the traditional sense, all of my income is essentially non-career income.

But let me break it down:

SAVE

What is your annual spending?

Our total annual household spending is $120k.

We live in a nice urban area in Singapore with two kids in international schools. School fees alone eat up a massive chunk of that number.

If you take education out of the equation, our lifestyle is actually quite modest. We are not flashy people.

I practice stealth wealth, meaning having money without showing it.

Most people around us have no clue we are doing alright financially, and I want to keep it that way. No envy, no drama, no unwanted attention.

What are the main categories (expenses) this spending breaks into?

Our annual spending breaks down like this:

- Education (two kids in international school): approximately $45k. This is by far our biggest expense and one I do not compromise on. I see it as an investment, not a cost.

- Housing (rent): approximately $24k. We rent rather than own our home. In the city we live in, renting makes more financial sense for our situation, and it gives us flexibility.

- Food and groceries: approximately $12k. We eat out occasionally, but mostly cook at home. My wife is a great cook, so that helps.

- Travel and vacations: approximately $10k. We have a small vacation home in the Alps that we visit regularly, and we take one or two family trips per year.

- Insurance and healthcare: approximately $8k. Health insurance for a family of four plus some basic coverage.

- Transportation: approximately $5k. We do not own a car. We use public transport and taxis. One less thing to worry about.

- Everything else (utilities, subscriptions, clothing, kids activities, miscellaneous): approximately $16k.

Do you have a budget? If so, how do you implement it?

I track everything with the iOS app MoneyControl, and no, I don’t have a clear budget. We used to be more rigorous about it in the earlier years when money was tighter, but at this point, we have a natural rhythm.

We know roughly what our fixed costs are each month, and we both have a similar mindset when it comes to spending.

What percentage of your gross income do you save and how has that changed over time?

Currently, with $180k in passive income and $120k in annual spending, we save roughly 33% of our gross income. That $60k surplus gets reinvested into my portfolios every year, which keeps the compounding machine running.

But this ratio has changed dramatically over time. In my early entrepreneurial years, the savings rate was essentially zero or even negative.

There were years where I was pouring everything back into the business and deferring my own salary. Once I sold the company and shifted to living off passive income, the savings rate jumped significantly.

What’s your best tip for saving (accumulating) money?

Automate it and forget about it. Once you have your income streams set up, make sure a portion goes straight into your investment accounts before you even see it.

The best-performing accounts at Fidelity reportedly belonged to people who forgot their passwords or had passed away.

That tells you everything you need to know. Stop tinkering, stop overthinking, and let compounding do the heavy lifting.

Dollar cost averaging into solid assets over decades is boring, but boring works.

What’s your best tip for spending less money?

Adopt the stealth wealth mindset. Once you stop caring about what other people think of your car, your clothes, your watch, or your phone, your spending drops naturally.

I do not own a car. I do not wear fancy watches. I do not care about brand names.

Nobody around me knows what my net worth is.

The moment you start spending to impress others, you are playing a game you cannot win because there is always someone with a nicer car or a bigger house. Opt out of that game entirely and your expenses will take care of themselves.

What is your favorite thing to spend money on/your secret splurge?

Travel with my family, without question. We have a small vacation home in the Alps, and some of my happiest moments are spent there with my wife and kids.

I love nice hotels from time to time. I see such memories as valuable memory dividends for the family.

INVEST

What is your investment philosophy/plan?

My investment philosophy boils down to a few core principles, all developed through decades of trial and error and plenty of expensive mistakes. I write about this in detail on my blog, but here is the short version.

I am a 100% DIY investor. No financial advisors, no wealth managers.

I believe no one will care about my money more than I do. I diversify across multiple distinct asset classes, not just stocks, because I want my financial house to stand on multiple legs like a sturdy table.

My stock portfolio is dividend-centric, focused on fortress-like companies with wide moats that will still be around in 50 years. Think Heinz ketchup and Milka chocolate, not the latest tech darling.

I invest internationally across the United States, Europe, and Asia Pacific, and I plan to never sell my core holdings. Also, I only invest in companies that do good that I can hold forever.

I once read ‘Rich people sell. Wealthy people do not’. There is a big difference.

What has been your best investment?

Two stand out, and they are very different in nature.

The first is building and selling my own company. That single event generated $1.5m in shares and $500k in cash, and the ongoing dividends from the acquiring company continue to be my largest single income stream to this day.

It was not a financial “investment” in the traditional sense, but it was the biggest bet I ever placed.

The second is Bitcoin. I bought my first Bitcoin in 2017 and added more in 2019 at an average price that is below $10k.

I also invested $200k into a long-only digital asset fund in 2018 that paid out $700k. My total realized and unrealized gains from digital assets have been life-changing.

What has been your worst investment?

I have a few scars, and I am not shy about sharing them.

The dot-com crash was my first major lesson. I was young, overconfident, and had over 70% of my personal portfolio wiped out. I learned the hard way that paper gains are not real gains until you actually realize them.

But the more painful and recent wounds came from the crypto space.

In 2022, the Terra Luna collapse cost me approximately $95k (after I made $150k with it). That one hurt because it happened fast and there was nothing I could do.

Then, almost immediately after, the Celsius bankruptcy hit. I had roughly $100k locked up with them when they went down.

Eventually, after two years, I got $60k back, but only after a painful, long and frustrating insolvency process.

What’s been your overall return?

This is a tough one to answer precisely because my wealth was not built primarily through stock market returns. A huge portion of my net worth came from entrepreneurship, selling my company, and investments in private Ltd’s, which do not fit neatly into a percentage return calculation.

For my public stock portfolio, my All-Weather Portfolio, my annualized return so far has been 13%, which I am happy with. I am not trying to beat the S&P 500 every year.

I am trying to build a resilient, income-generating portfolio that lets me sleep well at night and compounds steadily over decades.

How often do you monitor/review your portfolio?

I check markets daily, but my total portfolio value once a month. I sit down, log all dividends received, review positions, and assess whether anything needs attention.

I like to compare it to maintaining a garden. Some plants grew a lot and need trimming. Some weeds need removing.

Maybe something is underperforming and should be replaced with something stronger.

This monthly check-in keeps the portfolio in good shape without overtrading. The key is to be disciplined but not obsessive.

NET WORTH

How did you accumulate your net worth?

Entrepreneurship created the wealth, investing amplified it.

I started hustling at 14, doing odd jobs like car washing and mowing lawns. I then bought my first stock with the earnings.

After college, I moved to Asia and built my own company from scratch. For years the income was inconsistent and I often deferred my own salary to pay my team.

Eventually, the business gained traction and I was very lucky to sell it. That was an important fork on the road for me.

From there, I deployed the capital across multiple asset classes. It took roughly 40 years to hit my first million, but only about four more to add the next six million.

A lot of luck and timing played into that, and I do not take it for granted.

What would you say is your greatest strength in the wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

Save and invest. I always tried to end the month with more than what I started it with.

And patience when it comes to investing. I can buy an asset and sit on it for years while the market crashes around me.

Most people think they can handle a 40% drawdown until it actually happens, and then they panic sell at the bottom. I have trained myself to stay calm and often take the contrarian view when others panic.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

The dot-com crash wiped out over 70% of my portfolio. The 2008 financial crisis tested my company and mental sanity to its limits.

And in 2022, crypto delivered a brutal one-two punch: Terra Luna cost me $95k and the Celsius bankruptcy locked up another $100k.

Every experienced investor has scars.

What are you currently doing to maintain/grow your net worth?

Nothing fancy. I reinvest the roughly $60k annual surplus back into my portfolios, add to my best conviction positions when valuations look attractive, and continue earning yield on digital assets.

I also spend time on research and writing for my blog.

Writing forces clarity. If I cannot explain an investment thesis in simple terms, I probably do not understand it well enough to put money into it.

Do you have a target net worth you are trying to attain?

My original target was $3.5m, which I overshot.

Today, I do not have a hard number I am chasing. The real goal has already been achieved: my passive income exceeds our household expenses every month.

I call that reaching escape velocity. Everything from here is just compounding on top of an already comfortable life.

If I had to name a milestone, $10m feels good, but I am not losing sleep over it. Once I reach that, my goal will not be to make ever more, but to support causes I am passionate about.

How old were you when you made your first million and have you had any significant behavior shifts since then?

I was 40. It was impressively unimpressive. No champagne, just a spreadsheet crossing seven digits and a sense of silent gratification.

The biggest shift since then has been learning to relax. In my 20s and 30s I was in full hustle mode.

After reaching financial independence, I learned that having more money does not make you happier, but having more time and freedom absolutely does.

There is a beautiful German phrase, “Geld ist geprägte Freiheit,” which translates to “money is coined freedom.” That captures it perfectly.

Money is not the goal, freedom is. I went from “more is better” to “enough is plenty,” and that has been the most valuable change in my life.

What personal habits and/or traits have you developed that have made you successful at growing your net worth?

Spending discipline and patience. Make more than you spend, and have a consistent daily routine that creates mental space for good decisions.

Intellectual curiosity about companies and markets. Being comfortable with being wrong, as long as I size my bets so no single mistake can take me out.

That gap between what you earn and what you spend is where wealth is created.

What money mistakes have you made along the way that others can learn from?

Selling Microsoft when I was 14 for a quick small gain instead of holding forever. Watching 70% of my portfolio evaporate during the dot-com crash because I was too greedy to take profits.

Trusting centralized crypto platforms with too much money. And not starting my dividend portfolio sooner.

I only began in 2020 when I should have started two decades earlier.

The best time to start investing was 20 years ago. The second best time is today.

What advice do you have for ESI Money readers on how to become wealthy?

Earn more than you spend, invest the difference, and give it time. There are no shortcuts.

As the great German investor André Kostolany once said: “I cannot tell you how to get rich quickly, but I can tell you how to get poor quickly — by trying to get rich quickly.”

Bet on yourself, whether that means starting a business or investing in your skills. Start investing now, even if it is just $50.

Adopt a stealth wealth mindset and stop trying to look rich so you can focus on actually being rich in time and freedom. And remember that money is your servant and a tool, not a goal.

Once your passive income exceeds your expenses, you have won the game. Everything after that is just keeping score.

FUTURE

What are your plans for the future regarding lifestyle?

Not much needs to change because I already live the life I want. Some people talk about being a time billionaire. I think I am getting close to that.

No boss, no commute, full control over my time. The whole point of financial independence was to design a life I do not need a vacation from.

The only thing that might shift is location. As the kids get older, we may spend more time in Europe to be closer to my wider family.

What are your retirement plans?

I have been semi-retired since 2017 and do not plan to ever fully stop.

I love investing too much. My days are filled with research, writing my blog, advising founders of the companies I am invested in, and spending time with my family.

The key word is “choice.” I do all of this because I want to, not because I have to.

Financially, the plan is boring by design: keep the passive income flowing, reinvest the surplus, and let compounding work for another few decades.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

Two things. First, geopolitical risk. The world feels increasingly unstable, and living abroad adds complexity around currencies, tax laws, and political shifts.

I address this by diversifying geographically across where I hold assets and maintaining the flexibility to relocate if needed.

Second, making sure my kids develop a healthy relationship with money.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

It started at 14 when I bought Microsoft with money from odd jobs. But the real click happened around age 38, when I understood that financial independence is not about a big net worth number but about building enough passive income to cover your expenses.

That mental shift from chasing a number to building income streams changed everything. I was entirely self-taught through books, blogs, YouTube, and a lot of expensive mistakes.

Who inspired you to excel in life? Who are your heroes?

Salvador Dali, my favorite surrealist artist. He encouraged everyone to embrace their unique quirks and wild ideas rather than trying to fit in.

I learned from him that it is okay to see and do things differently, whether in art or in how you live your life.

Warren Buffett, for showing that you can build an extraordinary life on your own terms. Not Wall Street, but Omaha, Nebraska.

Build and live in the environment that works for you, not the one other people expect you to be in.

My grandmother, for teaching me that if you want to build a beautiful tower, you need to spend a lot of time on the foundation first. That lesson applies to everything, from business to investing to raising a family.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

“The Richest Man in Babylon” by George S. Clason. A foundational book for any investor. The principles are ancient but timeless, and that is exactly the point.

“The Four Agreements” by Don Miguel Ruiz. This one changed my life. It is not a money book, but the way you think about yourself and the world directly impacts how you build wealth.

“Think and Grow Rich” by Napoleon Hill. The book of all books. If you only read one book on the mindset required to build wealth, make it this one.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

For the past 8 years, I donated $50 to Watsi – a nonprofit crowdfunding platform that enables anyone to directly fund life-changing medical care.

I am not a fan of donating to large organizations where I cannot see how the money is used. Once I hit my $10m mark, I also want to support specific clubs and organizations of my local home town in Germany.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

Working on it. I have a simple will that already defines 99%.

But one of my main goals for the coming three years is to set up our family bank, a holding company designed to preserve wealth across generations rather than just handing over a pile of cash and hoping for the best.

There is a saying that wealth rarely survives three generations. And I am the 3rd generation. I am determined to prove that wrong.

Great interview!

I know it is great by the number of additional browser tabs I’ve opened while reading…

Thanks, Chris – appreciate it. I hope you got some value out of it.

Very educational and interesting interview. I wasn’t even aware of income opportunities from a “stablecoin farm” and had to look that one up. I especially like the multiple pillars of income concept you have going. Nice work!

Thanks, Cactus Cowboy, yep, stablecoin farms are wild. The current yields are down tho, but I am still making 8-12% p.a. ATM.

How’s life like in Singapore compared to the East coast, US. Can you elaborate in detail if you don’t mind. thanks!

Hey FeistyFire, I never lived on the East Coast, but have travelled there quite a bit. Living in Singapore feels 100% safe, modern, and everything works. You can order anything online if you so like. Everything is spotless. The nicest beaches in the world are an hour flight away. It’s always hot, and I am missing Bavarian springs and winters! But overall it’s difficult to move back once you got used to all of the above!

Thank you for sharing your story! I liked the quote from German investor André Kostolany, “I cannot tell you how to get rich quickly, but I can tell you how to get poor quickly — by trying to get rich quickly.” The Bible contains a similar proverb that says “he who hastens to be rich shall not go unpunished.” For the most part wealth is usually built slowly over time.

Hi MI 343, yes, Kostolany had many good quotes. He did a lot for the German stock market, unfortunately, not enough, because only about 20% of Germans hold stocks. Absolutely crazy.

That’s certainly an interesting portfolio. Obvious question I suppose, but why not simply go 100% in on public equities and follow a 4% safe withdrawal rate?

Also does Noah ever miss the alpine lifestyle?