Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in January.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

My wife and I are both 40, college sweethearts, and were married in 2004, 5 days after graduation.

Do you have kids/family (if so, how old are they)?

We have 2 kids, a 14-year-old daughter and an 8-year-old son.

What area of the country do you live in (and urban or rural)?

We live in the Southeast part of the country in a suburban neighborhood.

We have a modest home that we purchased in 2009.

What is your current net worth?

Our current net worth is $1.3 mm.

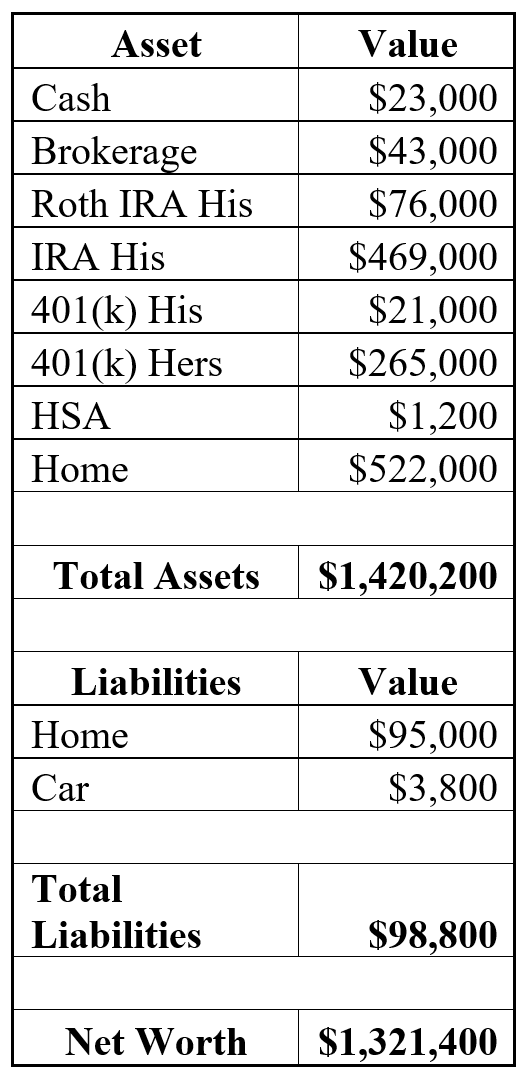

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

Below is a personal balance sheet that outlines our finances.

I started the Roth shortly after we were married. The traditional IRA is a result of rolling over 401(k) balances after changing jobs and I’ve only been with my current employer a little over a year which is why the 401(k) is so low.

EARN

What is your job?

My current title is Strategy and Planning Consultant, which is a bland corporate title that means very little. I have spent my entire career in Corporate Real Estate and currently am a part of a Construction Management Team where I provide various types of business support.

My wife is a Senior Financial Analyst and that is a much better title for what she actually does.

Both of us are individual contributors, though we both have had jobs with management responsibilities. In the grand scheme of things, neither of us is very senior within our respective organizations.

What is your annual income?

My current salary is $122,500 with a bonus target of 12% – as of the writing of this, variable compensation hasn’t yet been communicated, but based on what I’ve heard, I’m expecting to receive the entire 12% ($14,700) which would make my annual salary $137,200.

My wife’s annual salary is $102,682 with a more performance driven bonus structure which can range from 0-25%. Last year was a really good year and she received a bonus of $20,187 for a total annual salary of $122,869.

This gives us an annual household income of just over $260,000.

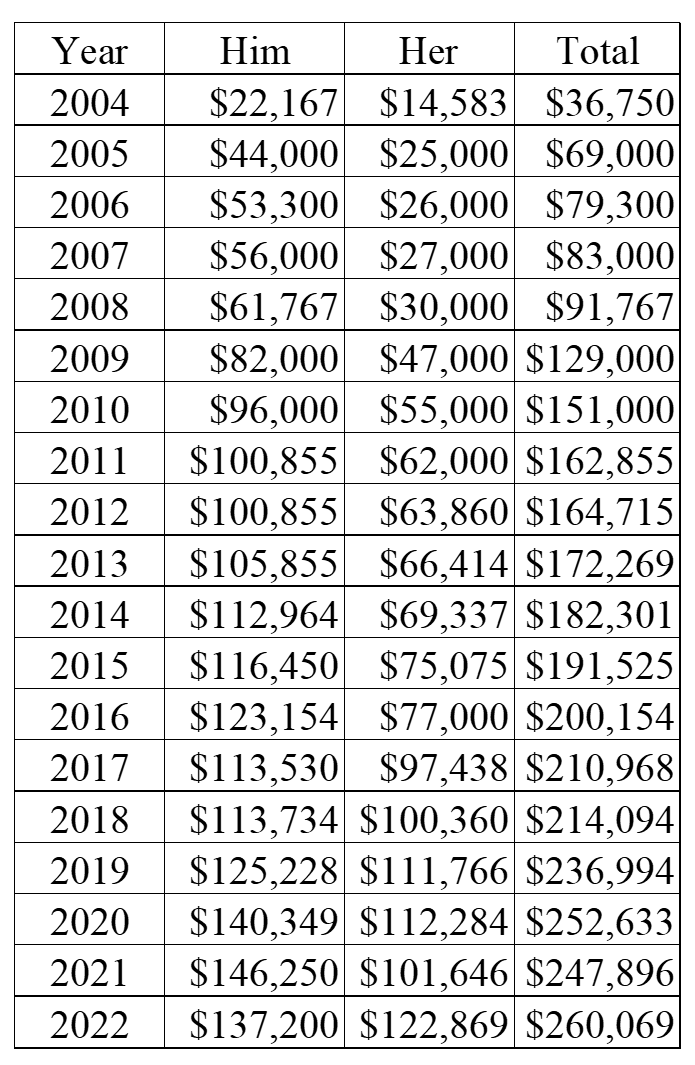

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

My wife and I both began our careers in entry level jobs in June 2004. As I’m sure you’ll see throughout this interview, I track a lot of things in spreadsheets and our annual income is one of those.

Below is a chart that shows our salaries (and any bonuses) for each year since 2004. For 2004 this is a proration since we didn’t enter the corporate workforce until June.

My first annual salary was $38,000 and that first year, I received a bonus of $2,000 and thought I had hit the jackpot!

My wife’s first salary was $25,000.

Our annual income has increased by 2.76x and has grown by an annual rate of 7.65% since 2005 (first full year).

I wouldn’t describe either of us a corporate ladder climbers. We both do our jobs well and have taken advantages of opportunities when they present themselves. I took a small pay cut when I began this job in late 2020, but it offered more stability than my previous job and I really liked the people I would be working with. Outside of that, I’ve been fortunate to have a couple of managers that appreciated me and took care of me financially because of the work I did for them.

What tips do you have for others who want to grow their career-related income?

Without sounding too cliché, I think it’s pretty simple – do your job.

When I started my first job out of college, I decided that I would make it my top priority to make my manager look good. I figured that my manager was going to be the one to either make or break any compensation decisions and if they liked me and were happy with me, they’d take care of me. With a few exceptions, that has worked out pretty well. Figure out what is important to your boss and then do that well.

When I was a manager, the first conversation I would have with my people was to ask them what they thought their #1 priority was. I got all type of answers and then would tell them they were wrong and that it was to make me look good. I always enjoyed watching their reaction to that.

Afterwards, I would explain to them that it was my job to take care of them – whether that was to be the shield when the shit hit the fan or when it came to compensation time. During a performance review one year, my manager made the comment that my team was extremely loyal to me and would go to war for me. That observation proved to me that what I was doing was working.

Also – don’t burn bridges. Treat people with respect and get to know them as people. I have found it’s a lot more difficult to be mean to people who you know personally, and it makes for a better work environment.

What’s your work-life balance look like?

I have worked from home since 2006 (though I may have to start going into the office a few days a week at some point) and my work-life balance is great. I am involved in my children’s activities as a coach or parent volunteer. I cook dinner for my family most nights of the week and rarely have to do any significant work outside of the normal business day.

My wife also works from home, though she has only done so for the past 2-3 years. My office is downstairs and hers is upstairs, and we text each other during the day more than we speak face to face, but it works for us. She is also involved in our children’s activities and while she does work outside of normal business hours more than I do, it’s typically only a day or two a month – usually during her month-end close period.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

Currently neither of us does anything outside of our day jobs. There was a time when my wife was part of a multi-level marketing company, selling scrapbook materials, but that was more just to help pay for her habit. She never really made much money and she stopped doing it after a year or two.

I had a small side hustle about 5 or 6 years ago, working for a former manager who had started his own business and needed some help with some of that work. I would make a few hundred dollars a month depending on how much work I did for him, but after a while that went by the wayside.

SAVE

What is your annual spending?

I don’t track my spending as closely as I did 10-15 years ago. Part of that is due to having more and not being worried about not being able to cover expenses.

We used Microsoft Money to track our finances from the time we were married until Microsoft stopped supporting the application. In those days, we kept all of our receipts and balanced the check book each month. We tried to switch to Quicken, and I didn’t like the tool as much and eventually just stopped using it altogether.

I do look at my bank account regularly to ensure everything is good and there’s no surprises. My wife loves it (sarcasm) when she receives a text asking her what she spent $47 on, when I see a charge and don’t recognize the vendor – but that is about the extent of my tracking.

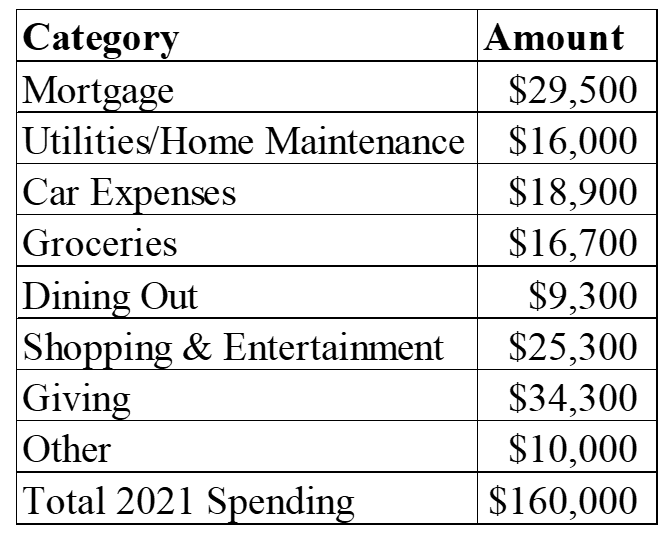

To answer the question though, in 2021 we spent about $160,000 according to my bank website.

What are the main categories (expenses) this spending breaks into?

I’ve included a chart below that outlines our spending by category for 2021. I’ll provide a few notes on these things:

Mortgage – Since the first day I’ve had a mortgage, I have paid more than the minimum.

In the beginning it was only $50 a month, but it was something. We bought our current house in 2009 (remember the housing bubble in 2008?) for $285,000 – a builder spec that had been sitting for about a year, it was a good deal! We had enough equity in our first home to put down 10% and were paying 4.75% plus PMI of about $100 a month plus an additional $100 in extra principle.

In April 2013, we refinanced to a 10/1 ARM at 2.875%. By then, our home had appreciated enough, and we had paid enough principle that we were out of PMI. My monthly payment dropped by about $350 a month, we no longer were paying PMI and so I began paying an extra $600 a month in principle. As my kids got out of daycare, or we paid off a car, I’d take a portion of those dollars and put it towards the mortgage.

Today, I pay an $1,050 extra each month in principle (more than double my monthly payment). If the current trend holds, our house will be paid off by early 2026.

Utilities/Home Maintenance – We have standard utility bills; power, gas, cable/internet, cell phones and pay someone to clean our home every other week and a professional yard service to maintain our yard.

Car Expenses – We own two cars; I bought my car in April 2020 (another great timing purchase) and have paid it down significantly over the last 2 years and will finish paying it off in a month or two.

Groceries – We eat at home 4-5 nights per week and this includes alcohol purchases – my wife has a wine habit and I have a bourbon habit.

Dining Out – This is probably a little higher than what we spent in 2020, but not as much as we spent in 2019, for obvious reasons. My wife and I used to average a nice dinner out ($150-$200) about once a month and that is slowly starting to return, but generally speaking we dine out more locally and fast food.

Shopping & Entertainment – This represents general merchandise we buy for ourselves and others throughout the year. If there’s something we want, we typically buy it – I’d guess most of this is via Amazon.

Giving – This number is a bit higher than it normally is, as we just finished a 3-year, $50,000 pledge to our church’s building project. Now that we’ve fulfilled that pledge, that category will decrease in 2022.

Do you have a budget? If so, how do you implement it?

We do not have a formal budget.

I monitor our spending and if I see something getting a little out of control, my wife and I will discuss it.

I do look at our finances closely prior to making a major purchase and we typically discuss those things to determine if we’re comfortable spending that money.

What percentage of your gross income do you save and how has that changed over time?

We save roughly 20% of our gross income each year and that is almost entirely made up of contributions to our 401(k)s and I include our employer’s contributions in that number.

This percentage has increased over time. When we first started our careers, we only contributed enough to get the full match, but as our incomes have grown, we have increased our saving percentages as well.

What’s your best tip for saving (accumulating) money?

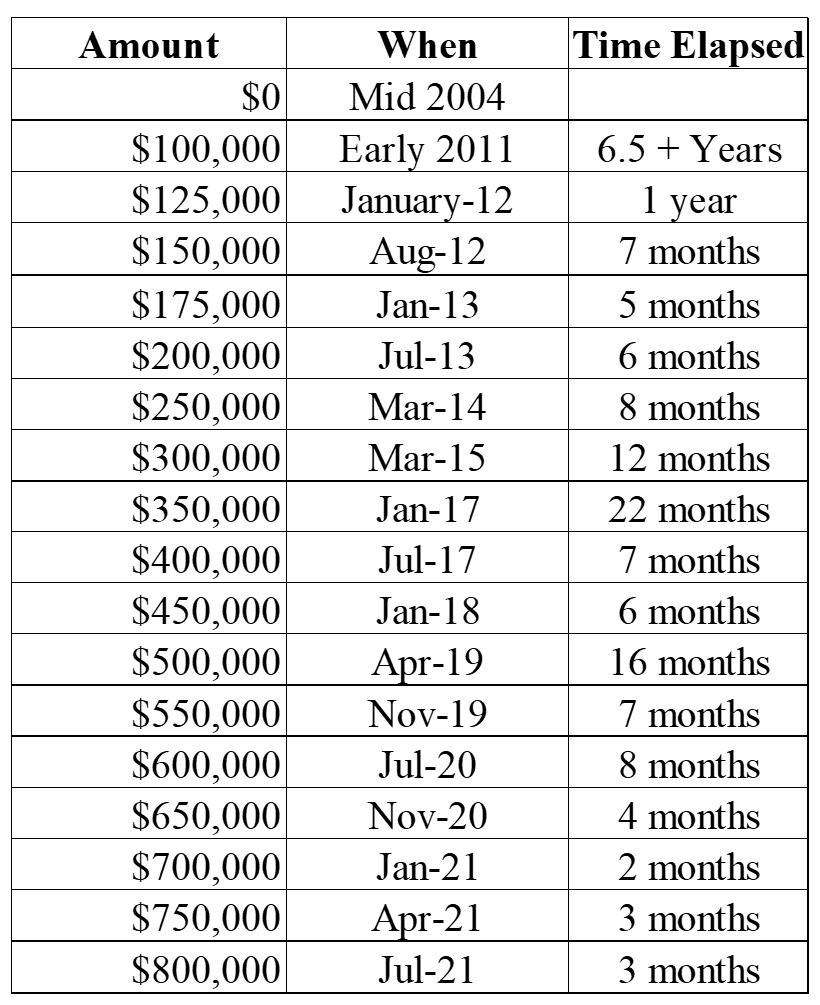

Save early and save often.

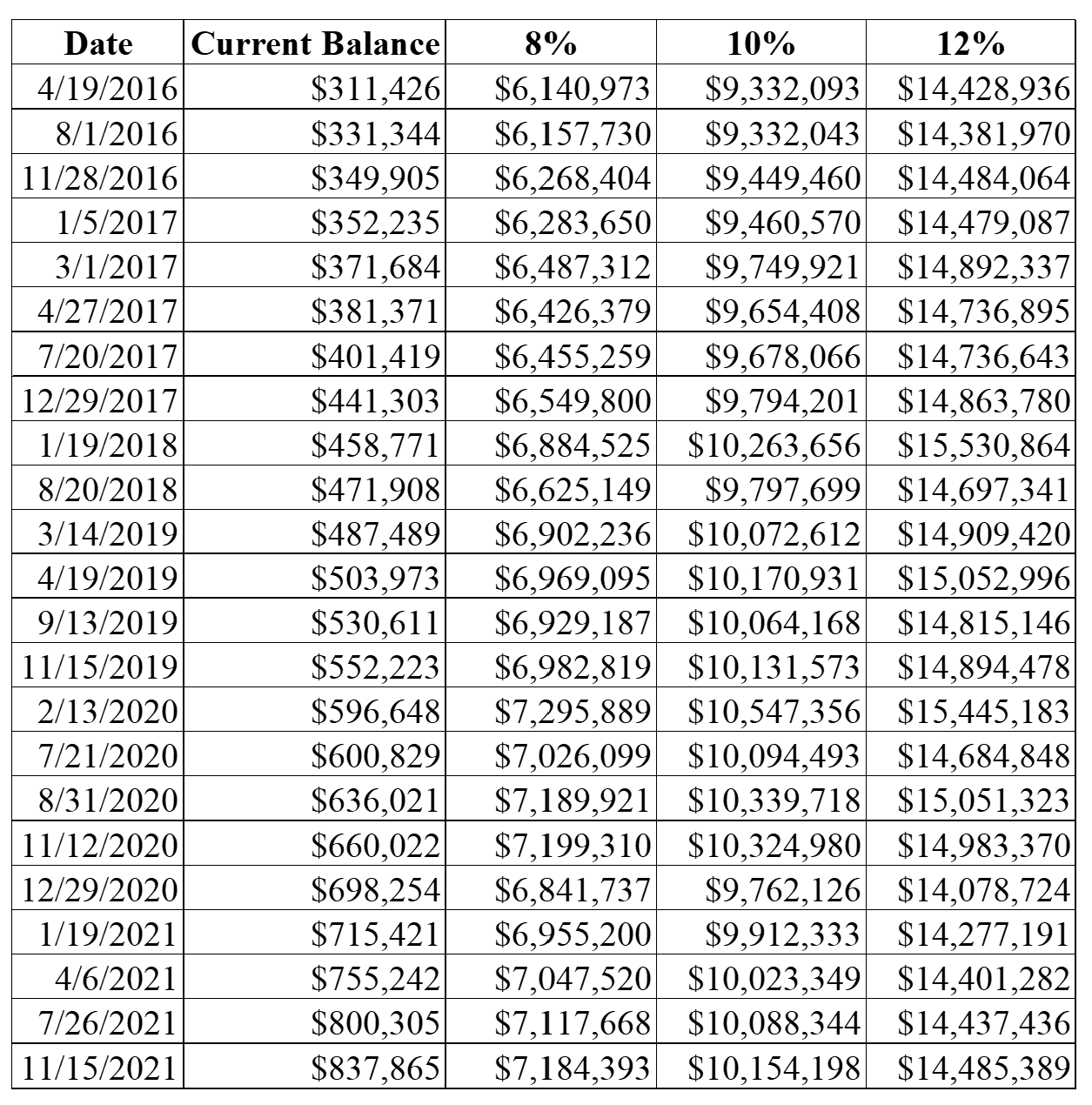

Compounding interest is a wonderful thing. Below is a chart where I track our retirement balances. It took 6.5 years for us to accumulate the first $100,000, it takes far less time to accumulate $100,000 now – of course we save a lot more now, which helps, but all the money we have saved since 2004 continues to work for us.

As an aside, it’s also easy to see where the market has done well and not as well over this period of time.

What’s your best tip for spending less money?

I’m fairly disciplined when it comes to spending and have always been that way. I’m obviously a little looser with my money than I was when I had less of it, but there are times when I will stare at the Amazon screen and really debate whether or not I need to buy that $15 item. It’s a blessing and a curse – sometimes I waste far too much time on something silly, but it has served me well and kept me from overspending for my whole life.

If I had to give one tip, it would be to call your providers (cable/phone/etc.) and tell them you want to cancel and when they ask why, say it’s too expensive.

For example, my wife and I both have SiriusXM in our cars. I love satellite radio and even though I only listen to about 2 channels, I want to have it. I have a reminder on my calendar each year to call them and tell them I want to cancel it about 2 days before it’s set to renew. The regular price is $18 a month plus tax/fees – about $240-250 a year. When I call to cancel, they offer me a 1-year promotion for about $100 a year.

It isn’t a huge savings, but that’s a cost avoidance of almost $1,500 over the 10-year period. Over time, things like that add up.

What is your favorite thing to spend money on/your secret splurge?

I will spend money on food and drink and items for my kitchen. I’d rather have high end equipment and good quality food and drink. I am a bit of a snob when it comes to food and drink and usually will go without (in a nice way) rather than consume poor quality items. This comes in to play when we travel – I will only consider places that have great food and it’s typically the tipping point when selecting a resort.

I kid my wife about how much she spends on wine. When she first started to explore wine, I would complain if she spent more than $7 or $8 on a bottle and now, we won’t even consider anything that’s less than $20 a bottle.

INVEST

What is your investment philosophy/plan?

I believe in diversification and appropriate risk management. I’m fairly hands off with the specifics of my investments. I don’t have the desire to actively research equities and try to time the market – so I outsource that to people that are more knowledgeable about it than me.

My wife and I both invest in target date funds within our 401(k)s. I use the fund that is 5 years after my intended retirement date, in order to keep my money in higher yield investments longer.

My IRA and brokerage portfolio is managed by a large financial institution, and I simply provide my risk tolerance level (moderately aggressive) to my financial advisor and their program does the rest.

My IRAs are primarily in ETFs, and I couldn’t tell you which ones or any specifics. I check the balances frequently and as long as I’m in line with the market, I’m happy. Some years you win and some years you lose, but my hope is that by being in long term, my wins are more frequent than my losses. Thus far, this strategy has worked well for me.

This comes back to my understanding of compounding interest. I have a retirement forecast spreadsheet that I update periodically and see how my current situation and forecast change over time – see below for details. I forecast my retirement savings with several assumptions and calculate the expected future value at various rates of return.

I didn’t start time-stamping this until 2016, despite having this spreadsheet since about 2005, but I wish I had done it sooner to better see how things have changed over time.

The amounts in the last 3 columns are what I project to have accumulated by the time I turn 60 – my goal is to see those totals stay flat or increase over time. It gives me a sense of what my actual rate of return has been over time.

Since 2016, I’d estimate that it has been between 10-12% (the market historically returns 12% over the long term) based on these numbers. I keep notes to the side to indicate if there are special circumstances that impact the forecast (i.e. bonuses higher/lower than expected, market conditions, etc.)

What has been your best investment?

I can’t point to one investment as being my “best”, I think that based on the way that I invest, utilizing the long timeframe I had has been my best investment decision.

What has been your worst investment?

When I was in college, one of my roommates gave me a stock tip. He told me about a nanotechnology company on the pink sheets that I should invest in because the government was investing heavily in nanotechnology. His name wasn’t Jordan Belfort, but he convinced me, and I opened an E-Trade account and bought $1,000 worth.

Several years later, I sold it for a little over $100 as E-Trade was charging me a monthly fee and making my loss bigger than it already was. It was the only time I’ve ever had a stock loss write off on my tax return.

What’s been your overall return?

This is one metric that I haven’t really tracked over the years.

If I had to guess, I’d say I’m probably somewhere between 10%-12%.

How often do you monitor/review your portfolio?

I view the balances of my portfolio every weekday. Part of my morning routine is to log into my banking website and check the balances of my bank accounts and investment accounts. I do this primarily to ensure there’s nothing unexpected.

I’m a long-term investor, so I don’t panic about changes to my balances. I will admit, spring 2020 was a rough time, as I saw dips of about $100,000 in my total portfolio, but at that point there wasn’t anything I could do about it, and I the only thing I would have done, had I had the cash, would be to invest more.

NET WORTH

How did you accumulate your net worth?

In the story of the ant and the grasshopper, I am the ant. When we graduated college and got married, my wife and I had a net worth of about $5,000, about $1,000 of that came from wedding and graduation gifts.

I have always lived within my means and didn’t worry about keeping up with the Joneses. One of my proudest accomplishments is that in my entire life, I have paid interest on a credit card exactly one time (I was in college and just didn’t have the funds to pay the entire balance – it was less than $20 in interest). We have made a relatively high amount of money and that has certainly helped, and not to sound like a broken record, but time has been our biggest ally.

I have worked for 3 different companies in my career and the first day on the job, my top priority is to enroll in the 401(k). I have collected every single cent that my employers have offered to me via matching funds – I’ll never turn down free money. As my salary increased, so did my percentage of contribution. I have kept my money invested in long term investments and don’t try to time the market or score big on a hot stock.

I have also experienced good luck in the timing of some of my major purchases. We bought our first home in 2004, we closed on reading day instead of studying for final exams. We sold that home in 2009 during one of the lowest points in the housing bubble for about $10,000 more than we paid for it and right before many of the homes in the neighborhood began to go into foreclosure.

When we bought our new home, we paid over $100,000 less than the builder’s “sticker price”. When rates were hitting historic lows, I refinanced my mortgage and between the refi and the additional principle, estimate that I’ll save around $130,000 in interest based on what I would have spent had I made the regular payment for 30 years.

Finally, I set goals. In early 2005, I opened a Roth IRA and met with a financial planner who asked my wife and I lots of questions about our financial plans. That conversation helped us to set goals and then we made it a priority to reach those goals. Currently, our goal is to pay off our home and purchase a vacation home that we can enjoy and hopefully rent to help offset the cost of owning it.

When there are major purchases we want to make (be it a new car, a vacation, or home improvements) we prioritize those items, set a budget for them, and then save until we have the money required to execute (though I have always financed cars, but do put down a substantial amount and then pay them off as quickly as possible). This may mean we have to sacrifice the present for the future, but that’s the price you pay for living that ant life.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

I hope it’s fairly obvious at this point that my greatest strength is saving.

I consider paying down debt a form of saving and am thrilled that we are to the point where our long-term debts are less than $100,000.

I am adept at avoiding instant gratification, though I probably indulge more now than in prior years, but it’s at a level that we can afford.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

I can’t really recall any significant road bumps.

My wife and I have been fortunate to always be employed and to be able to weather any unexpected financial hiccups.

Both of us, along with our children have been relatively healthy, so no major medical bills, and we’ve done an adequate job of maintaining our home to avoid unexpected home repair bills.

I can’t really take much credit for any of this other than to say we’ve been lucky.

What are you currently doing to maintain/grow your net worth?

To quote Joe Dirt, we just “got to keep on, keepin’ on”. We’re sticking to the plan.

I routinely check the MLS listings to see what homes are on the market in our area. I’d love to have a bigger home with some spaces that we don’t currently have in our home (a media room and wine cellar come to mind), but I always come back to the plan.

We talk about how it would be nice to take big family vacations more often (it’s been about one every 3-4 years) but again, we need to stick to the plan.

Do you have a target net worth you are trying to attain?

I don’t have a target net worth goal – ideally, I’d like to be debt free.

I have a goal of about $7 million (give or take) in retirement accounts. I’m sure I’ll refine that goal as we get closer to retirement, based on current expenses, cost of living, etc.

As I get closer to retiring the mortgage, we’ll reassess and determine what the next phase of the plan is and go from there.

How old were you when you made your first million and have you had any significant behavior shifts since then?

We are relatively new to the millionaire club, having entered it just over a year ago in December 2020. We were 39 at the time.

There haven’t been any significant changes to our behavior since that time.

I had hoped to hit the mark before I turned 40 and was glad that I did so, but nothing changed as a result.

What money mistakes have you made along the way that others can learn from?

I don’t really feel that I have made many money mistakes, certainly nothing that stands out as being egregious – which is probably why I am where I am.

If I had to choose one, it would be negotiating better when I bought my first new car. I was young and dumb and didn’t really know what I was doing. I probably could have saved $1,000/$1,500 on the car, but it was a lesson learned.

I’ll offer one more tip on buying a car – don’t negotiate inside the dealership. You should negotiate over the phone or email and don’t walk into the store until you have an agreed-on price. I’ve done that with my last 2 cars, and I’ve saved a lot.

I get online quotes from multiple dealers and then forward the lowest one to the 2nd lowest dealer and ask them to beat it. Then I take that and forward it to the original lowest and ask them to beat it. I let them bid on my business.

My sister just bought a new car last month – she didn’t ask my advice prior to doing so – and wound up being stuck in a finance office for over an hour, buying gap coverage despite a large down payment, and agreeing to an inordinately high interest rate. What really got to me is the realization that she isn’t the exception, she’s the rule, and the number of people that get taken advantage of because they don’t know any different.

What advice do you have for ESI Money readers on how to become wealthy?

Stop me if you’ve heard this before, start saving now. For some people becoming wealthy can happen seemingly overnight. For me, it’s been 18 years of being focused on the end goal and sticking to the plan.

Set goals, short-term goals and long-term goals and maybe even a BHAG (big hairy audacious goal) or two. What is important to you? Prioritize your goals – don’t try to boil the ocean, it is far too large.

Once you’ve done that, create a plan to achieve your goals. Write it down and then make it a priority to check your progress routinely. Be honest with yourself and make sure your goals are realistic. If you’re married or have a significant other, include them in the process. I make most of the financial plans/decisions (it’s more of a passion of mine than it is hers), but I always talk to my wife about it to make sure she’s on board and to ensure she is in agreement.

If you’re not sure where to start, search the ESI archives – there’s lots of good stuff in there.

After that, if you’re still not sure, talk with a financial advisor. Most banks offer “free” financial planning in some capacity. Take advantage of that and at least have the meeting.

One word about financial advisors – they only make money when you give it to them, primarily via fees. While there are good ones out there (I have one) you also have to take any advice they give you with a grain of salt.

Example – when I first began working with my current FA, he offered a suggestion of opening a HELOC, and using that money to invest, with the thought that I could make more in the market than the interest on the loan. I shut that down quickly because that is far more risk than I care to absorb. He understood and has learned about me.

If the FA doesn’t spend 20-30 minutes asking you questions and learning about you prior to offering you advice, you should not work with them, good ones will look to build a relationship and trust with you. If you make money, they make money (generally speaking – pay attention to the fee structure).

FUTURE

What are your plans for the future regarding lifestyle?

Currently, I hope to retire from the corporate world at age 60. That has been my goal since I started and the plan that I am on.

I don’t anticipate any significant lifestyle changes but depending on how our income grows and what happens after we pay off the mortgage, some of that may change.

What are your retirement plans?

My plan is to retire at age 60 and enjoy what time I have left for as much as I can. My children will be grown and hopefully there will be grandchildren in the picture to spoil with both time and money.

I’d like to play golf and travel with my wife to places where we can eat new foods and try new drinks.

I’ll also look for opportunities to volunteer my time – I don’t have any idea what that may look like, but I’ll look for something to keep me busy while helping others.

As far as financials are concerned, my plan is to draw no more than 4% of my retirement funds each year to live on. Assuming we’re able to purchase a vacation home and collect short term rental income on it, then I would expect to have some extra income from that aspect as well.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

The only issue I see at this point, is potentially healthcare.

I’d like to think that my retirement savings would be sufficient to cover healthcare expenses, but I’ve started to make a more concerted effort to contribute to an HSA. The balance is low now, but I’m going to attempt to max it out going forward so that I can invest the funds to use during my twilight years.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

I think I picked up things throughout my childhood that taught me about finances. My parents are not wealthy, and I would say that we were lower middle class growing up, but they did teach me some things. My mother taught me about credit cards and how when she used them, she always paid the balance each month. While we didn’t really want for anything (outside of the original NES that I begged my parents for, asked Santa for, and even bargained with God – no one came through for me) but I always knew that my parents lived within their means.

I had a savings account as a kid, and whenever I got money for birthday or Christmas, I had to put half of it in my savings account. As much as I hated it, it was a lesson that I needed.

It wasn’t until I was in college that I’d say it “clicked”. I was an accounting major at a school that prides itself on its Trust and Investment Management program. As a school of business student, I was required to take some classes that I likely wouldn’t have taken at other schools. One of those classes was called Financial Planning and it was required for all business undergrads. The textbook was a 3.5 inch binder full of information and it sits on my bookshelf as I type this.

This class opened my eyes to a variety of aspects of a person’s financial life that I never knew existed. I learned about personal finance, insurance (never buy whole life, always buy term), credit management, capital accumulation, investments, tax planning, retirement planning, estate planning and more. The class was designed to teach students how to serve their clients as Financial Planners, but for me it was a gateway into a hidden world – one that I was excited to enter, and I soaked up as much of it as I could.

I also was learning about time value of money in my accounting classes. I had to buy a financial calculator and learned how to calculate present value, future value, and payments. I learned how to amortize a loan and how to calculate the discount price of a bond. I began to play “what-if” games on my calculator to see how much money I’d have under various scenarios.

It wasn’t long before I learned that Excel was capable of performing these calculations and before I knew it, I had spreadsheets that allowed me to imagine an infinite number of possibilities. I suppose it was a bit surreptitious that I wound up at this particular college, but that is a story for another time.

Who inspired you to excel in life? Who are your heroes?

I can’t pinpoint any particular person who inspired me to excel. It’s been an internal drive for me. I have always wanted to have money and have been willing to do things to obtain it.

In middle school, I would carry people’s lunch trays and do other tasks for money. I dreamed of being rich as a kid and continue to do so today (I have a plan in my head if I were to ever win the Powerball).

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

I don’t read a lot and when I do, it’s not typically about money. In the interest of answering every question here are 3 books that I really like:

- The Dynasty by Jeff Benedict – It’s a book on the Patriot’s dynasty from how Robert Kraft became owner to how Belichick became the coach to how Tom Brady became the GOAT. I’m not a Patriot’s fan, by any stretch of the imagination, but it was a fascinating book, and I couldn’t put it down.

- The Politics of Jesus by John Howard Yoder – I used to belong to a theology group that would read and discuss various theological writings. This book makes the case for Christian pacifism and is foundational to my personal theology.

- Atlas Shrugged by Ayn Rand – While I’m not 100% onboard with Rand’s Objectivism philosophy, I read this book 15 years ago and appreciated it greatly. There are days where I have longed to find Galt’s Gulch and hoped to be allowed in.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

We do give to charity, and I’d estimate that it’s about 10% typically, a little more the last several years.

Outside of our church we give to the local Performing Arts foundation, which helps fund some of their programs and provides us with some perks during the theater season – we are season ticket holders.

We also give to our kids’ schools at various times throughout the year.

Previously, we had given to our alma mater but have not done that in a few years due to other commitments.

We feel it is important to give. John Wesley, the founder of the Methodist movement, said during his sermon entitled, “The Use of Money”, to “earn all you can, save all you can, and give all you can”. If ESI were to adopt a mantra from a religious aspect, I think this would fit in nicely.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

We had wills drafted prior to our first child being born – another tip: if you don’t have a will, a living will, and power of attorney, stop what you’re doing and call a lawyer to make an appointment; and have not changed them since.

If we were to both die tomorrow, we would leave everything to our children divided equally.

At some point, I think we’ll need to revisit that, but for now that is it. I don’t have any intention of disinheriting my children, but I could see us setting up some provisions to give some of our wealth to charitable causes.

This interview has an update which you can read at Millionaire Interview Update 71.

Estate planning is an ongoing process, not a one and done. Laws change, and more importantly, families and close friends change. Sounds as if you are overdue for checking your designated beneficiaries on all your accounts, life insurance, etc. then verify that all your personal representatives on powers of attorney, executors, and guardians for your children are still the best choices. Make sure they know about and agree to serving in the capacity you need.

About five years after we had set up our wills with designated guardians for our minor sons, we realized that all three couples were no longer in a position to serve. Our first choice couple had the misfortune of the wife dying at 38, another couple had divorced, and the third couple had divorced and married other people.

Now that our sons are grown and established, we have made one of them a backup executor in case my husband and I are both taken out in an accident such as a car wreck.

We have reviewed our estate plan about every three years ever since.

Thank you for the comment! We have discussed that and fortunately for us, we have chosen siblings for our representatives (they are all still the preferred choices) and annually check beneficiaries for our accounts.

Once our children are grown, we’ll certainly be making some updates.

Nice write-up — congratulations to you. Your piece of advice, to make your boss look good and you will thrive in return, is interesting. That works as long as there is a trust relationship, your boss shares your values (make me look good I will take care of you), and you have a shared definition of what payback looks like (comp, promotion, new opportunities, etc…). I’ve worked with good bosses and not-so-good bosses over my career. Some were in it for their own success, some shared the values you describe. The trick is figuring out quickly which your current boss is, and when they can’t be trusted or don’t share your values, get out and get out fast (or if staying find ways to make sure you stand out when your boss is grabbing all the credit). My point being the advice doesn’t always work out. Ideally the bad bosses are identified and pushed out because no one wants to work for them, but too often they just keep plugging along.

Thank you for your comment! You make a very valid point and are absolutely correct. I’ve had 7 different managers in my 18 year career and this strategy worked well with 4, not well with 2, and I’ve been with my current manager less than a year, though signs are promising thus far.

The 2 that it didn’t work well with were with the same employer and without going into all the details, had the same approach towards me. I was with the first one about two years and was getting ready to start looking when we had a restructuring and it only took me about a year with the second to start looking for a new job. Fortunately, I was able to find something else and get out of that situation.

Trust is huge for me and the first 12-18 months under a new manager, I do everything I can to earn as much trust as possible and in every situation where that has happened, good things have followed. It is also why, in 18 years, I have only voluntarily changed managers twice, as work happiness is significantly more important to me than climbing the corporate ladder. My philosophy is to figure out how to earn more money by doing the same thing I’m currently doing. For the most part, I’ve been able to do that.