Here’s our latest interview with a retiree as we seek to learn from those who have actually taken the retirement plunge.

Here’s our latest interview with a retiree as we seek to learn from those who have actually taken the retirement plunge.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview was conducted in August.

My questions are in bold italics and their responses follow in black.

Let’s get started…

GENERAL OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I am 64 years old and unattached.

I married in 1980 and have been divorced since 1990.

Do you have kids/family (if so, how old are they)?

I have one 38 years old daughter.

She has been on her own since graduation from law school.

What area of the country do you live in (and urban or rural)?

I live in a large California city.

Is there anything else we should know about you?

I wrote Millionaire Interview 169 in October 2019, posted in January 2020.

My family immigrated to the United States in 1973 from the USSR.

RETIREMENT OVERVIEW

How do you define retirement?

For me retirement is leaving the company where I worked for 34 years, not having an earned income and receiving a pension.

How long have you been retired?

I retired on April 1st, 2018, over 4 years ago.

What was your career and income before retirement?

I retired from a supply chain management position at a major aerospace company. I was a senior manager when I retired.

I was with the company for over 34 years, started after graduate school as a member of technical staff then switched to supply chain management, where I progressed from subcontract administrator to program manager.

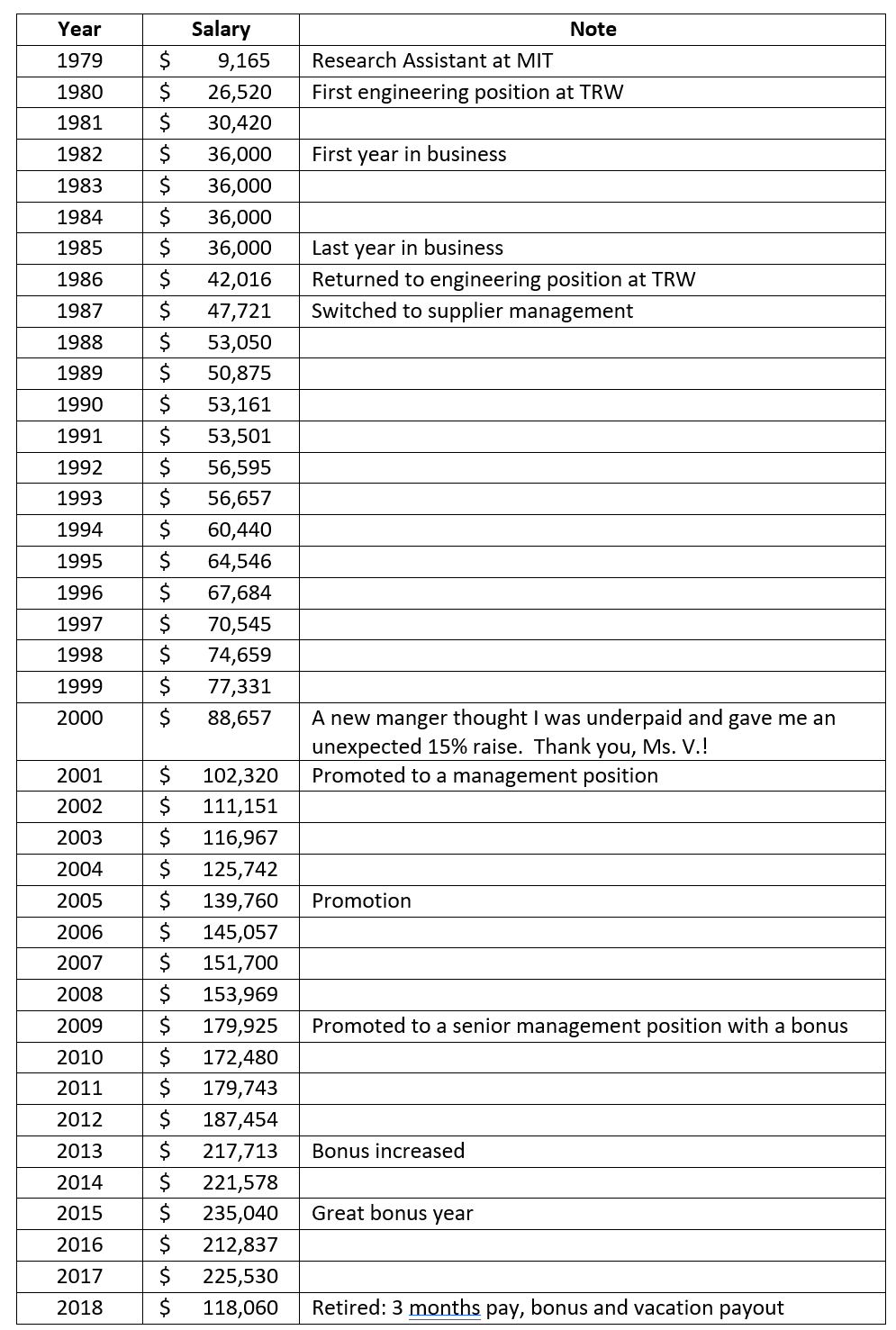

My job income history is as follows:

Why did you retire?

My retirement was purely voluntary, aided by a maturing pension, unfavorable management changes and desire for freedom.

I always took my work responsibilities very seriously, did my best to meet deadlines and deliver above expectations. This often caused a lot of stress and many additional hours of work above the usual 40 hours work week. Work often spilled into nights and weekends, and I never learned how to turn it off at home. Work stress was affecting my eating habits, sleep and overall health.

A few things converged to help me decide to retire when I did:

- The main program I worked was winding down and many of my work friends moved on to other projects or retired

- Retirement savings were sufficient for a comfortable retirement

- Full pension age was attained

- I had 35 years of maximum or close to maximum Social Security earnings achieved (32 years at maximum, 3 years a few thousand dollars short of maximum)

PREPARATION FOR RETIREMENT

When did you first start thinking seriously about retirement and when did that turn into a decision to do it?

I started planning for early retirement in my early 40s, with a goal to retire at 55 in 2013.

At 55 I could have started receiving a reduced early retirement pension benefit, which was 80% of full benefit reached at age 60. But when I turned 55 my net worth was somewhat smaller than projected, my retirement accounts took a big hit during the 2008/9 global financial crises.

My salary increased and also my bonus target went from 10% to 25%. So, I decided to work one more year, and then another, and another, and another, and another. The dreaded One-More-Year (OMY) Syndrome.

Not all considerations to stay on the job were financial. I happened to be working on an interesting program, with a wonderful set of colleagues and frequent international travel, reporting directly to two vice-presidents, who were looking out for me. The knowledge that I can walk away at any time helped in reducing work stress.

All that changed about a year before I retired; a corporate reorganization caused a retirement epidemic to sweep through the ranks. I lost my mentors, inherited a pile of new responsibilities without a corresponding increase in compensation, and my major program was wrapping up. My nest egg improved substantially and I decided to pull the plug.

What were the major steps you took from deciding to retire to developing a plan to do so?

You can say I started planning for retirement when I got my first paycheck post graduate school in 1980, since that’s when the first 401k contribution was made. The same year first IRA contribution was made.

I started looking at my finances seriously in my mid-thirties. The first major step was to maximize 401k contributions and resuming IRA contributions.

As my compensation grew, I started contributing to after-tax 401k account, which eventually was converted to a Roth IRA at no cost.

I also converted most of my investments to equity index mutual funds for better growth opportunity.

I started reading personal finance books and articles, used various retirement calculators and cash flow projections. I created worksheets to track my spending, net worth, pension estimates, Social Security estimates, future cash flow, etc.

When I finally decided to retire, I carefully chose my retirement date to ensure that I received the prior year’s bonus. I also hoarded my vacation hours the last two years and received 10 weeks of vacation payout at retirement.

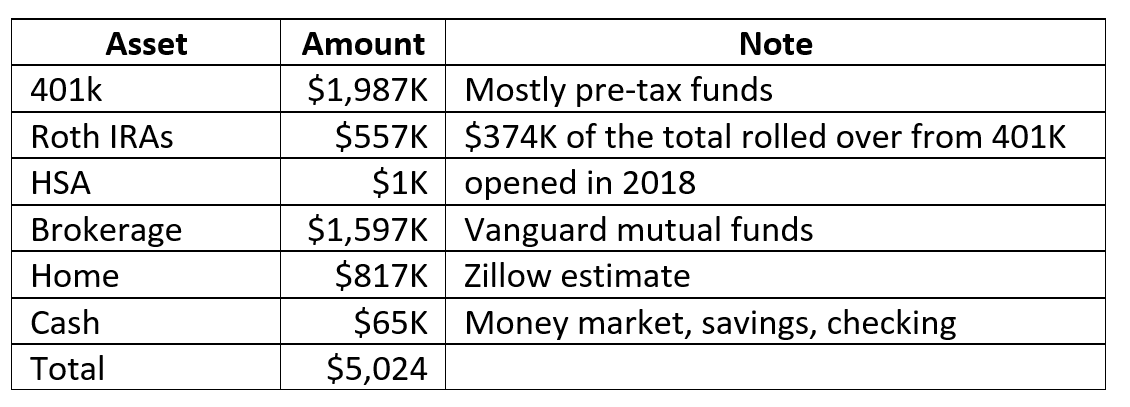

What did your pre-retirement financials look like?

My pre-retirement assets were as follows:

I had no mortgage or other debt besides credit card balances, which I paid off every month.

All the funds in 401k, IRA and brokerage accounts were in stock index mutual funds and ETFs, closely following Paul Merriman’s recommended Ultimate Buy and Hold Portfolio with 100% equities.

The 401k balance did not include $882K lump sum payment from my pension plan.

What was your overall financial plan for retirement?

I had detailed spending history going back 12 years prior to retirement. My spending averaged around $100K per year not counting retirement accounts contributions. Various taxes averaged about $60K per year, leaving about $40K per year for living expenses.

I figured my taxes in retirement will be reduced to under $10K per year, and $40K per year for basic living expenses, my needs. I figured that it would be nice to have another $50K per year for wants, such as travel, toys, gifts, house improvements. So, my goal was to spend at least $100K per year.

My income would consist of a company pension, dividends, Social Security and asset liquidation.

At retirement, I had a choice to take a partial lump sum distribution from my pension plan of $882K or an annual payment of $54K. After much deliberation, I took the lump sum and rolled it over into my 401K account to avoid immediate taxation.

Pension payments have no cost-of-living adjustments, and I didn’t feel safe in case inflation spikes in the future. I reasoned that prudently investing the lump sum, I have a fair chance to keep up with inflation; time will tell if this was a good decision.

In addition to the lump sum, I still get a partial annual pension of $32K.

I planned on taking Social Security payments at 70 to maximize the overall benefit.

To reach my goal of spending $100K per year, I would get $32K from pension and $68K from savings through age 70 (1.3% withdrawal rate). After 70, Social Security would provide $54K per year and my withdrawal rate would fall to just 0.3%.

I also estimated that the maximum income I can have assuming a 4% safe withdrawal rate is $235K.

Did you make any specific moves to prepare your finances for retirement?

I paid off my mortgage in 1999 and own my house clear and free.

For a couple of years prior to retirement I started channeling dividends in my brokerage account into a money market fund instead of reinvesting in index funds to build up a cash cushion.

Who helped you develop this plan?

I did all the retirement planning on my own.

I read many personal finance books and followed quite a few sites: ESI Money, MMM, Early Retirement Now, New Retirement, Bogleheads, JL Collins, and Paul Merriman to name a few.

I used several retirement calculators to assure that I had sufficient funds to retire with high probability of success.

What plans did you make in advance to leave your job?

I increased my 401k contribution so I could fully fund it for the year even though I only worked 3 months.

I bought a set of glasses and had dental and medical exams done.

What were your pre-retirement concerns (financial or non-financial)?

Working the additional 5 years during a roaring bull market and being 98% in stocks put me in a solid financial condition. However, I was concerned that rising inflation will erode the value of my pension over the years. I was also concerned what not having a regular paycheck would do to my psyche, a history of 40 years of earned income is hard to abandon.

I am an introvert by nature, INTJ I believe (just like Elon Musk, Michelle Obama, Vladimir Putin and Walter White (Heisenberg)). I don’t make friends easily, but am devoted to those I have. A big part of my social network was at work, and although I was planning to keep in touch with some people through social media and occasional lunches, it’s not the same as stepping into the next-door office and chatting at your whim.

Also, people I was closest to have retired moved away. I was concerned with social isolation as I get older.

I’ve been blessed with fairly good health most of my life, but lately parts of me hurt that never hurt before. Declining health was definitely of concern.

I was concerned that my transition at work would not go smoothly and my reputation may get tarnished.

One of my managers from the late ‘80s retired a few years ago. He had three children, a much younger wife who still worked, a nice house near the beach and drove a Porsche. After a couple years in retirement, he was back working as a consultant and eventually a full-time employee reporting to me. When I asked him what possessed him to come back, he replied that his wife made him do it since he was buying too many toys and squandering their nest egg.

There were a few other folks that “flunked retirement” and were back working full time or as contract labor. I was concerned that circumstances may drive me to seek employment again after retirement.

How did you handle deciding on and paying for healthcare?

My former company had a subsidized retiree medical plan. When I retired the monthly cost was $140.

They eventually discontinued the retiree plan, but I was grandfathered in as a long-time employee.

The plan had $1,700 annual deductible and $6,500 out-of-pocket limit and qualifies for HSA. This benefit lasts through age 64, at which time I will switch to Medicare with a small Medicare subsidy ($2,160 per year) form my former employer.

How did you tell your family and friends of your plans?

I started telling my family and close friends about my plan to retire at 55 a couple of years before that.

Being infected with OMY syndrome, I stopped talking about it for a few years.

I finally told my family and friends outside work about 3 months before I pulled the plug.

I told my work friends a month before when I gave my notice to management.

THE ACT OF RETIRING

How did you ultimately retire?

I reached 90% confidence level that I would retire at 60 about 6 months before my birthday. I double and triple checked my projections and started thinking about my transition plan at work. I decided to work through March 2018 to get my annual bonus and be able to fully fund the 401k account for the year.

My initial plan was to give a 3 months’ notice to assure a smooth transition of my responsibilities. I reached 100% confidence level during year end 2017 holidays and for the next 2 months I did my best to avoid accepting any new long-term projects.

After doing additional research on retirement notices, I decided to give a 1-month notice. I finally gave my notice on March 1st 2018. At the same time I notified HR, Benefits and Security. I had a fairly new functional manager at the time and I don’t recall any sort of reaction from him. I immediately started transitioning some of my responsibilities to my employees, I was blessed with having excellent people working for me. My functional manager took his time naming a replacement, and I ended up with only one week transition period. I completed all the paperwork for my pension and was given a retirement checklist from HR.

A week before my last day my manager arranged for a retirement lunch. Actually, I had a few going away lunches that week. On the last day I packed my belongings, went through a security debriefing and had my phone disconnected at noon. I went to a program status meeting around 3 pm and my program manager asked me why I am still here.

I experienced the surrealistic feelings the last month on the job, received many well wishes from employees and vendors I haven’t talked to in years and was bombarded with financial advice questions/requests. I retired from the same company that gave me my first professional job after college. The last building I worked in was just a couple of blocks from the first building I started my carrier in.

I had a sense of euphorbia the last working week, but the last few hours were very emotional, I had a very hard time holding back the tears. After all, I devoted over 34 years of my life to this company. As I walked up to my car and turned to see my building for the last time, the tears started pouring.

What went well?

I retired from a large company and they had solid processes for retirement. It all went very smoothly. I actually received my first pension deposit 2 days before retiring.

I am a worrier and always look for the worst-case scenario in stressful situations. I have to say the retirement process went very smoothly with no issues.

What didn’t go so well?

When I started receiving my pension, I noticed that the gross amount was a little less than the estimate I was provided before retiring.

A phone call to benefits resolved the error quickly and the underpayment was refunded.

How did you ultimately find the courage to do it?

As you can see from above, I suffered from one more year syndrome 5 times.

Eventually all pieces fell into place: my main program was winding down, my finances were solid, my back pain made it difficult to sit through a workday combined with a 50 miles round trip commute on a busy California city freeway. The company where I started my carrier was purchased by a bigger company and they eventually froze the legacy pension plan, which meant I would actually loose money to inflation the longer I stayed, and the lump sum would decrease as I aged.

Because interest rates were very low at retirement, the lump sum pension option was very attractive. I am not sure that it took all that much courage to retire at 60, let’s call it earlyish retirement.

RETIREMENT LIFE

How was the adjustment, especially the first few months after retirement?

During the first few months I went through a detoxification stage of retirement.

I loved all the free time. Waking up in the mornings without an alarm clock and realizing that there is no job to go to was bliss. Monday became my favorite day of the week. I caught up on all those TV shows everyone always talked about and I didn’t have time to follow (Breaking Bad, The Game of Thrones, The Americans, The Wire, Westworld, Top Gear, lots of good stuff). Reading a book a week was nice also.

It felt weird going for a walk in the middle of a workday. It felt like I was ditching school and being naughty. I often had work related dreams; waking up and realizing it’s no longer my problems was wonderful.

My father got very sick shortly before I retired and eventually passed a few months after. Having the free time to spend with him and my mother was a blessing.

I always had company laptops and cell phones which satisfied all my personal needs. At age 60 I had to buy my first laptop and cell phone.

How is retirement life now? What do you like about it and what do you dislike?

I am enjoying retirement life. I like all the freedom I have now, I can do whatever I want at any time. I also have a lot less stress in my life: no more daily commutes in heavy traffic, no worrying about work assignments. I definitely don’t miss that queasy feeling in my stomach on Sunday evenings.

It took me a while to disassociate my identity from my career. I was very proud of my educational and professional achievements, which were ingrained in my identity.

It took a few years to be comfortable with saying that I am a retired person.

What do you do with your time? What does an average day look like?

I don’t have much of routine.

I usually wake up around 7 am, turn on the local news channel, read my emails, read blog articles.

Most days I go for at least an hour walk around my neighborhood, or do yardwork, or go food shopping.

Then I prepare and eat lunch or meet a friend for lunch.

After lunch I check my investments, read a book, read blogs, play on-line poker, or work on a hobby.

I usually have a light early dinner at home.

In the evening I watch TV or socialize online, or visit my mother, sister or daughter.

What are the major activities that fill up your time in retirement? Are there any new ones you’re planning to try?

I am losing weight, limiting intake of white carbs and sugars, walking more and may rejoin a gym soon.

I enjoy listening to music and watching movies. I have nice home theater set ups in my family room and bedroom. One of my hobbies is speaker building, I’ve built several sets of speakers and a couple of subwoofers.

I like riding my bike in a local park.

I enjoy travel and plan to do more of it in the near future. I would like to visit Spain, Greece, Scandinavian countries, Italy, Australia and New Zealand to name a few.

I started dating again and plan to do more of it, even though I hate the dating scene; hoping to find a travel companion.

I also manage investments for my daughter, sister and mother, and do their taxes.

I like cars and may volunteer at an automotive museum after Covid subsides.

What is your social life like?

My social life definitely took a hit after retirement. I was very social at work and most of it is gone now. I meet with some of my former coworkers for lunch occasionally and joined a company retirement association; they hold several social events every year.

I have a few close friends that I visit regularly and spend time with my daughter, sister and mother, who all live nearby.

I have made a few online friends at various social sites. I am looking for more social groups to join.

Looking back, what would you have done differently?

Most of my retirement planning was concerning financial matters.

I should have spent more time planning what I am retiring to.

Was there any emotional impact from leaving the workforce?

I strongly identified myself with what I did for a living: an engineer, a senior manager, a “rocket scientist”. It took some time to get used to the fact that I no longer any of those. Most of my programs were for civil space, such as weather satellites, space telescopes, and scientific earth observing satellites. I felt that my work contributed to making our planet a better place to live for all.

I do miss the sense of pride when a project is completed followed by a successful launch. I also miss some of my former colleagues.

However, I do not miss the work itself: the deadlines, the tight budgets, management demands, employee issues, and many, many other issues, problems and setbacks.

What surprises (financial or non-financial, good or bad) have you had since retiring and how have you handled them?

The biggest financial surprise is much higher stock market volatility than I expected. So far, we had a big downturn in 2018, the Covid sell-off in 2020 and the current 2022 bear market driven by war in Ukraine and high inflation.

I am a buy-and-hold investor, so I do nothing except for rebalancing and harvesting losses when appropriate. My net worth is large enough to weather the volatility without much worry.

A pleasant surprise is that I rarely if ever find myself bored or anxious. I used to get regular headaches when working, which are much less frequent or severe now.

What are your future plans?

After Covid subsides some more, I would like to resume travelling and start looking for volunteer opportunities.

I hope to find a partner for companionship and to improve the quality of home cooked meals.

I plan to take more courses at a local community college. Maybe learn to play guitar again, I had one during my early teenage years, but was never very good at it.

I need to get my estate planning in order, not getting any younger.

RETIREMENT FINANCES

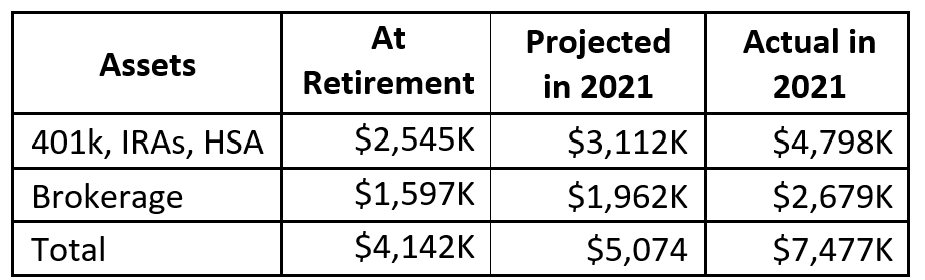

How has your financial plan performed compared to what you had estimated before retirement?

When I retired in 2018, I had projections for future financial assets.

The following table shows the amounts I projected by the end of 2021 and the actual amounts:

My projections were very conservative, the secular bull market was very good to me from 2019 through 2021.

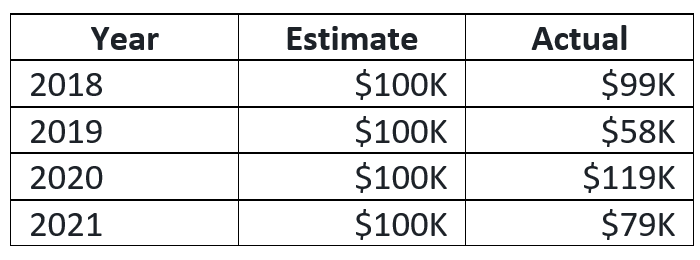

Spending estimates vs. actuals are as follows:

My income consists of pension and dividends and is very close to what I estimated.

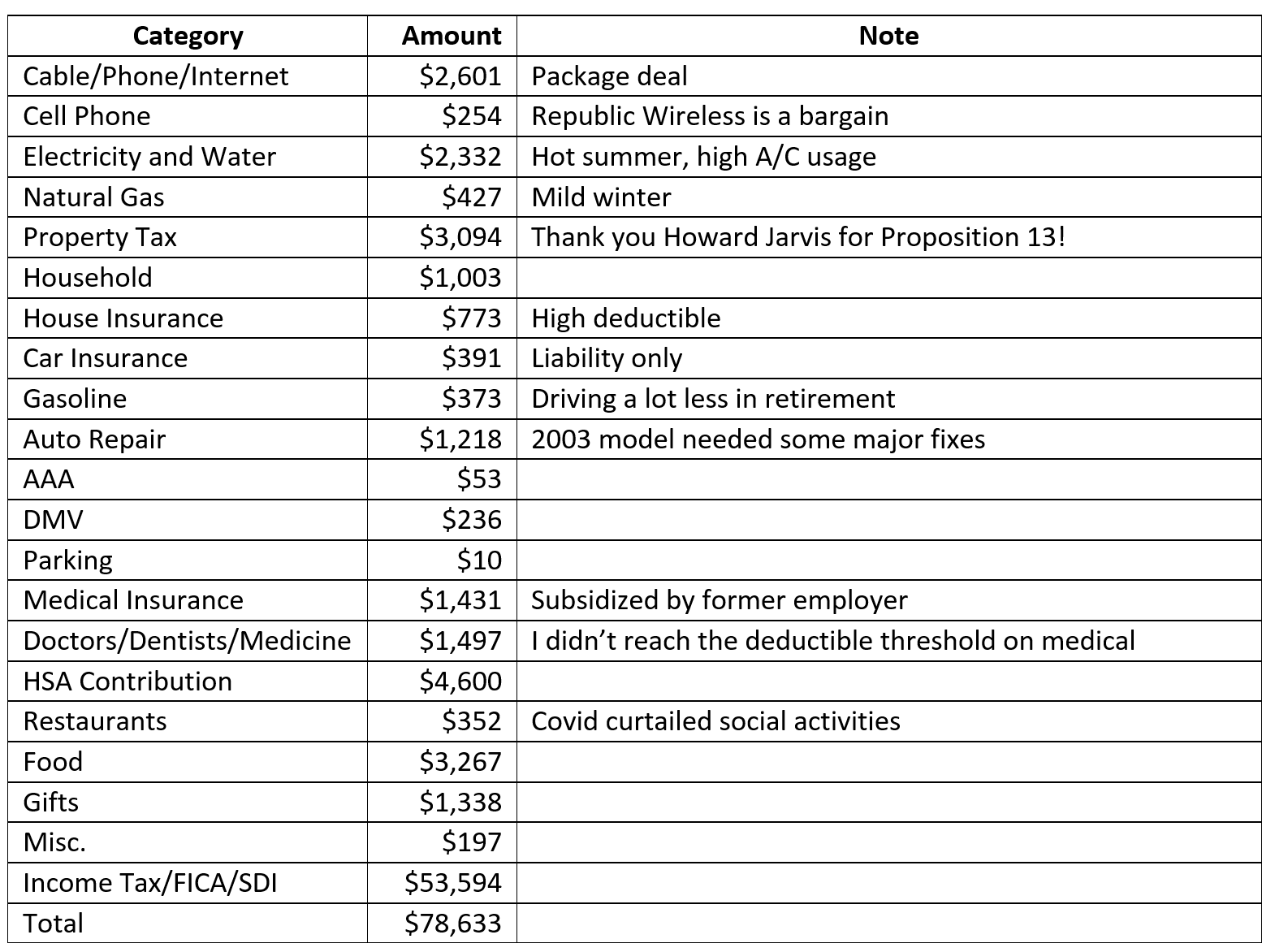

Can you give us some insights into your post-retirement spending and income? How much do you spend annually and on what? And where does the income to pay for your spending come from?

Last year my spending was as follows:

The expenses were paid by $32,091 pension and $46,542 from savings (0.75% withdrawal rate).

So far, I haven’t made any withdrawals from my IRAs or equity ETFs in brokerage accounts; all withdrawals came from my cash cushion, which is being replenished from taxable equity ETFs dividends ($36,722 in 2021)

How are you handling Social Security, required minimum distributions, tax issues and the like?

My current plan is postpone taking Social Security until age 70 to maximize the payment amount.

The thought process is as follows: a cash flow analysis shows that the breakeven age for taking SS payments at 70 vs. 62 is around 80, give or take a year or two depending on discount rate assumption. If I start payments early and live a long life, I loose. If I start payments late and die early, I loose, but I don’t care since I am dead.

Due to my large traditional IRA balance, I will have substantial RMD withdrawals starting in 2030. I estimate my RMD payments will start at $180K, which will push my taxable income over $315K per year and into the 35% federal income tax bracket at today’s rates. To reduce the impact of RMDs, I started doing Roth conversions to fill the 24% federal income tax bracket as soon as I retired. So far, I converted $506K, and plan to convert another $1.2M over the next 8 years.

Did you return to paid work? Why or why not?

I must admit that I was perusing the company job openings for about a year.

Right now I have no desire to return to paid work. I have more than enough funds to live a very comfortable existence.

Did you find it hard going from being a saver to a spender?

I have a spending problem, as in – it hurts to spend. I have been a saver the latter half of my life and am now struggling with loosening up those purse strings.

I always had that warm and cozy feeling from drawing a good salary; now my guaranteed income is down to $32K. The transition from being a saver to a spender proves to be difficult for me — I am open for suggestions.

And no, I am not going to invest in your hair growth miracle drug, pay for space tourism or buy you a boat. Actually, space tourism could be cool.

Looking back, what do you wish you knew in advance?

Because I did so much planning pre-retirement, I didn’t have any big surprises.

What advice do you have for those wanting to retire?

Plan, plan, plan then do it. I am jealous of the ESI readers who are taking investment education seriously in their 20s and 30s. Oh what bright futures await you!

Think what are you retiring to, rather then what you are retiring from.

Working an extra year or two to beef up the nest egg is not a bad idea — you will sleep better at night.

Thank you for your honesty. You gave simple yet profound descriptions of the feelings related to wrapping up a 34 year career at the same employer. How strange it must have felt when someone asked you why you were at that last meeting. It is a poignant reminder that these companies/jobs move on instantaneously. It is a powerful reminder that we need to invest our time and energy into relationships, activities and identities outside of work to help with the retirement transition. I hope you find your travel companion and enjoy the heck out of your retirement!

Congratulations. Well done, in virtually every aspect. Good luck finding a travel companion, you deserve someone that is awesome.

Thanks for sharing. Fantastic! Will you consider to fund 529 plan for grandkids? Or maybe gifting your daughter to annual maximum?

Thank you livelovelaugh (great name). I have no grandkids, and I doubt there will be any. My only beneficiary is my only daughter. I am seriously considering gifting her substantial sums while I can, doing the annual maximum of $17K a year will hardly make a dent in her inheritance.

Rock solid pre planning for retirement. Proof that if one applies themselves, read, learn a little, financial literacy can be achieved as a diy.

here’s a spending idea. u say u like cars, get a brand new car! esp since u can afford it. Ever owned a brand new one? noticed ur car is a 2003. No better time for an upgrade. That should eliminate the annoying fixes. This suggestion is only because you can more than afford to. so what if it depreciates. Give some money to causes you believe in. That’s another idea. I didn’t see much charitable giving outside of gifts to family?

it’s your golden years. Spend on what you like, if you like. Just some suggestions. Go on an adventure , enjoy your well deserved retirement. You won.

Thank you for your suggestions MJ. Every car I ever bought was new, I just keep them until they fall apart; the current one was bought new in 2002. I would love to get an electric sports car in the near future, right now there are none available that appeal to me.

Congratulations on living a financially-disciplined life. Your net worth at retirement was impressive and your frugality has continued into retirement. You should consider spending more on travel, family, or whatever. Very well done.

Thank you Dan. I am planning to substantially increase my spending on things that bring me joy. But I must admit, watching my net worth grow over the years also brings joy:)

Congratulations on all your achievements, very well done. Just one friendly suggestion, looks like you will have an estate tax problem, 2026 estate tax will be reversed back to $6 million, anything above that will be taxed at 40% plus whatever your state may tax also. I would start spending more, gifting more to family and charity.

Thank you Hospitalist. I may indeed have an estate problem. One thing that helps somewhat is converting traditional IRA funds into Roth IRA, to date I paid $228K in federal and state taxes to convert $670K. This reduces the estate total, while increasing the more desirable Roth funds. I am also considering gifting more.

I’m glad you had a great career. I also was blessed with a wonderful career. I stayed a few extra years also. On the day I retired, I cried all the way home. It was very difficult giving up my job. But, it was time and I also knew that if I didn’t retire soon, I would never do all the other adventures on my todo list. Best wishes on your retirement!!!

Thank you D. I shed a few tears on the way home that last day of work, leaving behind 34 years of memories, accomplishments, triumphs, and meaningful relationships is not for the feint of heart.

Congratulations on your excellent post.

As I woman, I congratulate you on your wonderful retirement planning which you have so carefully thought out.

Not only have you empowered yourself but you have also helped immeasurably your family. Your daughter has you as an excellent role model.

It has saddened me over many years to see how many women put everyone else first and then find that the cupboard is bare when it comes to themselves in old age.

May you have a wonderful retirement, you deserve it.

I think this was a very good, down to earth and honest assessment to retirement; a ‘retirement story’, planning, and execution that is very relatable to a career 9 to 5 person. Especially narrations on the fears, anxiety, regrets (?), and a new hope for the future.

I appreciate your candid and frank ‘walk-through’ leading up to your retirement.

Went on to read your Millionaire Interview 169 after I finished reading your retirement interview – you are hysterical! Yours was a very interesting and fun read. And coming from an Eastern European background myself, I get you – there were so many things that you said that were so relatable. Congratulations on your American success story! Hope you are enjoying your retirement and the fruits of your labor!

Congrats on a successful career and retirement!

Congratulations you have done a fantastic job. Like you I am a saver and trying to spend is very challenging. How did you decide what amounts to pull from your taxable accounts and what tax brackets are you aiming for? We are Canadian. Have substantial amounts in taxable accounts that eventually at 71 force the % withdrawal so I am trying to take it out now and place in non taxable accounts. My husband has incurable cancer and if he passes he’s entire account will be taxed. There are no calculators to help with this. He has approx $670k , is 63 so hopefully I have about 8 yearsOur brackets are 15% on 53,359 the. 24% on 106,717, 29 on 165,430. Should I just forge ahead and get it out? I am dyi like you for I vestments and accounting

Thank you Jane. I am very sorry to hear about your husband’s illness, I hope his remaining time is happy and pain-free.

I am not familiar with Canadian tax code, but it sounds that it’s somewhat similar to the US system. I can tell you what I do. So far I have only withdrawn money from my taxable IRA account to do Roth conversions (Roth is a tax free account). These conversions are subject to taxation. The US tax brackets for a single filer in 2022 are 10% up to $10,275, 12% up to $41,775, 22% up to $89,075, 24% up to $170,050, 32% up to $215,950, 35% up to $539,900, and 37% on anything above $539,900. Also, gross income above $200,000 is subject to a 3.8% investment tax. In addition, the state of California has numerous tax brackets, but the one I fall into is 9.3% between $66,295 and $338,639.

For the last several years I have converted IRA funds to fill the 24% federal bracket. I created a worksheet to calculate my taxes; I know what my pension payment is and I can estimate my dividend income fairly accurately. You can also do a provisional tax return using tax software. I usually do the conversion at the end of the year, when dividend information is available. But in a couple of years I did most of the conversion after a substantial market drop, that way I can convert more shares for the same dollar amount. I do the transfer from IRA to Roth IRA in kind in ETF shares and pay the taxes from my after-tax brokerage account.

Since I don’t know your income or deductions, it is difficult to say if you should be withdrawing your taxable retirement funds now. However, withdrawing enough to fill the 24% tax bracket seems reasonable, unless you expect to be in a lower tax bracket after age 71. The whole point of conversion is to pay less taxes now, rather then more later. I also assume that your husband’s account will not be paid out in lump sum, but be a percentage based on your age for the rest of your life. For example, in the US the annual required minimum distribution for a 71 year old is 3.53%, or $23.7K on a $670K account.

I hope this helps you with your decision, feel free to reach out if you need anything else.

Nicely done. You’ve worked hard for a great retirement, and now can afford to treat yourself, be generous and volunteer. I am just now reading the book Die with Zero and after reading your interview and difficulty spending think you will enjoy it. How fortunate your daughter is that you are looking out for her. Hope you also find some hobbies and social causes that you are passionate about.

Thank you Financial Fives. I have seen a few recommendations for the Die with Zero book, and it’s in my holds at the library.

I second die with zero.

I ‘borrowed’ the audio version from my library.

After listening to it, I had to buy it, and have listed to it 5 times since.

The book convinces me to spend a ‘little’ more each year.

I don’t follow the book’s advice, but I do allow it to influence my decisions.

Great interview and well done. Very helpful to see your projected and actual for assets and spending during your retirement.

Thank you Isam. Since I did the interview, I have that actuals for 2022:

Assets Projected Actual

IRA $3,267K $4,010K

Brokerage $2,060K $2,213K

Total $5,327K $6,223K

Spending $100K $89K

My net worth took a substantial hit in 2022, down $1,254K due to poor stock market performance, but still above my projections. Spending is close to projection.

That is helpful too. Do you do new projections every year or are these values from the projections that you did when you retired?

The projections are from my retirement in March 2018.

It is truly incredible how much you saved.

I’ve been with the same company 30 years, and my total salary was well above yours, however my net worth is not significantly higher than yours, so very well done.

I am not a spender, but I didn’t have enough in the market during this long bull market.

I see a lot of similarities in your story to my life.

So my question to you RI-41 is, should I retire as planned at 55, or OMY for a few more years?

My biggest fear is not running out of money, but rather regretting leaving a career I have spent a life time achieving with no real opportunity to return if I leave.

After 30 years of adrenalin from too much work, I do fear it will be hard to adjust.

I don’t expect to drop a tear when I leave, but I do expect to wake up stressed from a lack of tasks to accomplish. On the other hand, there is a risk I will realise I should have retired years earlier.

Thank you for your comments Clay. Regrets are tricky to navigate, but you have to realize that you are the only one in the best position to figure out the best path to take at this particular moment. Only you know the benefits and shortcomings of your carrier and what your retirement may look like. In my case, I originally planned to retire at 55 and was in a financial position to do so. Six times I contemplated the retirement decision and for 5 years the benefits of working OMY outweighed retirement, until finally at 60 the balance swung the other way and I pulled the cord. I am yet to wake up stressed from a lack of tasks to accomplish, sometimes I wonder how did I ever find time to work:)

Whatever you decide I can assure you knowing that you can walk away at any time substantially reduces work stress. If you love your job, are very well compensated, are in good health and have no sold plans on how to spend your retirement time, working OMY may be your best bet. On the other hand I just read an article where the author named several friends and acquaintances that died shortly after retiring and had very little time to enjoy retirement.

All I can say is don’t wait if you don’t have to or better yet see if you can go part time, take the time to travel while you have health insurance because if you do get sick which is not uncommon you will have at least done that. For us almost now impossible to get cancellation or medical insurance without spending a ton of $ due to pre-existing conditions. Use ESI to help plan what you will do with your time. It’s true you won’t know how you did accomplish life & work while you did work – adrenaline is a mighty motivator! Such cliches but as they say life is too short and your kids grow up fast are so true.

I may have missed something. Your living expenses were around $25k but the taxes were over $53k. What kicked in the high tax? And how does SDI work in retirement?

The high tax is due to Roth conversion. I assume SDI doesn’t apply since I stopped paying for it when I quit my job.

Congratulations on retirement and controlling your own life. It is great that you have a subsidized health plan. You certainly have been a saver and moving to spending takes time. I’m like you with buying a new car and keeping for a long time but mine is a 2007 Lexus, so you have me beat by several years.

Regarding travel and finding a companion. One thought would be to sign up for a few travel companies and start to read what packages they offer. It is fun to dream and think about where you might want to go: USA or International, so many choices. Also, many travel companies have a single person price. Go with a group of people and be the single person that has a blast making your memories. Travel while your health is good. We went on our first “Gate 1” travel package in February 2020 to Australia/New Zealand for 27 days. Fabulous trip and we were super glad to return to the USA as some strange disease was beginning in China. On that tour, there was a single guy and it didn’t seem like he had a problem doing any activities and as a group we all had fun together. There are many travel companies, so look up a few and plan. No need to wait to find someone to travel with.

What an excellent interview! I really appreciate you writing about what it felt like near the end working up to your retirement. Also, the scope of retirement life is outside of just the financial aspects of it. I had been so focused on just the money for years and have only recently been focused on the life part once I retire. Spoke to a wonderful retired neighbor about the things I wanted to do in retirement and his reply was “That is vacation. What are you going to do after you’re done with that two months into your retirement.” A wise man who shook me awake. I’m definitely going to save your interview to reread a few times over the next two years as I prepare to walk away at 62.

Thank you for the kind words Debbie! Visualize what a typical good day will look like 2 years, 5 years and 10 years after retirement. What can you do now to make that vision attainable? A solid financial foundation is a must, but what you build on it for a wonderful retirement is mostly non-financial. Good luck to you Debbie and have a great life after work.