Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in November.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I am 59 and my ex-wife is 56.

We were married for 30 years.

We separated in July of 2020 and divorced in June of 2022.

Do you have kids/family (if so, how old are they)?

We have 3 kids: 30, 28, 26.

All three are married.

What area of the country do you live in (and urban or rural)?

I have lived my entire life in the Midwest.

The past 30 years has been in a city with a population of about 60,000.

What is your current net worth?

Pre-divorce net worth was over $3.0M.

House was part of the divorce settlement to my EX to avoid alimony, so current net worth is $1.5M.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

- Cash : $24k

- Inherited Annuity: $62k

- Rollover IRA: $1.39M

- Rollover Roth: $79k

- Health Savings Account: $16k

EARN

What is your job?

My career in Information Technology spans 30 years with the last 24 working for a British multinational information and analytics company headquartered in London, England.

On April 1, 2020, my role was eliminated and rode off into the sunset. This was by my design, as I had achieved F.I.R.E. status in 2019 and was ready to enjoy life post-career.

I now consider myself retired and love to say, “I no longer trade my time for a paycheck.”

Here are the roles I head during the 24 years:

- Sr. Director, Global Production Operations (2013 – 2020)

- Director, Open Systems (2012 – 2013)

- Business Relationship Manager (2009 – 2012)

- Manager, IT Modernization Program (2008 – 2009)

- Manager, Storage Engineering (2006 – 2007)

- Manager, PC Hardware & Service Desk (2002 – 2006)

- Manager, Offshore Development (2002)

- Manager, Remote Services (2001 – 2002)

- Program Manager (2000 – 2001)

- Senior Hardware/Systems Engineer (1996 – 2000)

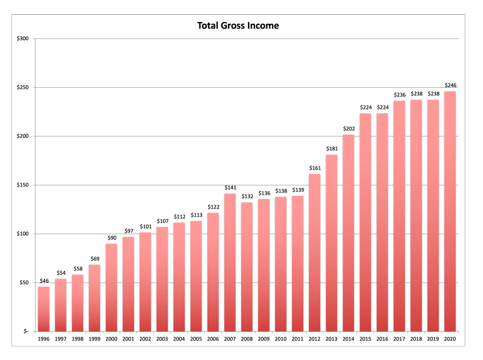

What is your annual income?

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

As a fresh graduate in 1987, I landed my first job making around $25k/year. The role was to manage office automation and write an inventory control system to track raw materials and finished goods for the printing industry.

After a few years, I became somewhat bored and landed a new role with a private company. I spent 6 years writing code, supporting two dozen manufacturing sites, office automation, fax machines, network upgrades, phone systems, hardware refreshes, software support for the engineering group, etc. Honestly, I loved the role as I was the “jack of all trades, master of some” and worked with smart people. However, the compensation wasn’t keeping up and the organization was extremely flat, so career progression stagnated.

In 1996, I took a role working for a British multinational information and analytics company headquartered in London, England with offices around the world, including the town where I was living. My daily commute was 15 minutes each way. I drove West in the morning and East in the evening. Talk about perfect, I didn’t even need sunglasses!

I started as an entry level engineer with a base salary of $50k. Over the next 24 years, I progressed into ever more challenging roles, eventually spending the last 7 years in a senior executive position. My career progression along with compensation is listed earlier in this interview.

What tips do you have for others who want to grow their career-related income?

While not a comprehensive list, here are some items which served me well throughout my career:

- Work harder and smarter than your peer group. Be willing to take uncomfortable positions which stretch and grow your skills and abilities.

- Develop self-awareness with respect to your “skills” and your “talents”. Skills are things which you can explain and teach to others. Talents are things you do naturally, but when asked to explain “how” you do them, you struggle to explain and usually end up saying “I don’t know, I just do it!”

- If you want to work at the “next level”, then behave as if you are already at that level.

- Invest in soft skills, especially communication. You can have the best idea, but what good is it, if you cannot communicate it to others. Therefore, take advantage of public speaking training and opportunities during your entire career.

- Always have an appetite to learn, technology, business acumen, project management, etc.

- Be resilient. Yes, there will be bad days and that is OK. Strength of character is the ability to fail and then try again.

- Treat your career like playing the card game Blackjack. To win at Blackjack, you must vary your bet. Bet the same amount each hand, eventually the house will have all your money. In your career, time is your currency. Learn how recognize when to “invest” 80 vs 40 hours in a week. When to work late or on the weekends. Remind yourself, today’s long hours will pay dividends tomorrow.

- Be comfortable at being uncomfortable. Often, when you are struggling and feel challenged, you are growing.

- If you are the smartest person at the table, find a new table!

What’s your work-life balance look like?

This answer is situational, based on the phase of my career and longevity of the role.

At the start of my career, I was focused on completing objectives ahead of schedule. Therefore, I often worked 60 to 80 hours in a week. I viewed this time as an “investment” in my long-term career (see blackjack comments above).

During the first 2 years at the firm, I was extremely driven to work harder and smarter than my peer group. There was so much to learn, not only with respect to the role, but with respect to the Company, office politics, relationship building, establishing my reputation, etc. Therefore, I averaged 50-80 hours per week. I viewed this time as “paying my dues” to establish a solid foundation with respect to my “brand”.

As my career progressed, I took on new roles which broadened my experience and knowledge. Each time, I would apply a 90 day “immersion” process to fast-track my understanding and impact. As I matured in the role, I could then pull back on weekly hours and improve the work-life balance.

As my career progressed into leadership positions, I continued this approach, especially in roles involving people leadership. Standing in the trenches with others, at all hours, is a great way to show respect and appreciation for their sacrifice and commitment.

The final 8 years of my career, I was leading a 7x24x365 production operations organization (Data Center, online applications and services). Unless I was on vacation, I was available 7x24x365 to lead any production related issues. While this was somewhat disruptive to my personal life, I still managed to strike a good work-life balance by empowering and developing leadership skills with-in the organization.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

No additional streams of income.

While working my primary job, I did a few years of consulting. While the consulting money was nice, it came at the sacrifice of being away from my family. Coupled with the demands of the primary job, the cost was just too great. Therefore, as a family, we decided I would focus on career growth at the primary job, living below our means and spending more time with the kids.

Looking back, this was one of the very best life decisions. You can always make more money, but you can never get back time.

SAVE

What is your annual spending?

As mentioned above, my annual spend over the past 3 years has been influenced by life changing events; divorce, loss of primary residence, moving twice (rentals), and buying furnishings.

I retired in April of 2020, with 39 weeks of severance, which enabled me to experience a full year of income. Starting in 2021, I was paying expenses from “cash on hand”. During this time, I was using Personal Capital to track accounts, but it had two flaws:

- It would not connect to my Apple Credit Card.

- PC was purchased by Empower and I have a long history of Empower screwing things up.

Therefore, I thought I would look at this answer from two angles: 1040AGI and expense/budget spreadsheet.

- 2021 1040 income: $114k

- 2022 1040 income: $88k

- 2021 Budget: $75k

- 2022 Budget: $70k

- 2023 Budget: $104k

The 2023 budget accounts for the fact that my girl friend and I are now cohabitating. While we continue to manage separate accounts, we have created a combined budget. Two car loans, which were paid off by July of 2023, vacations, pet care, etc.

As a footnote, she reached F.I.R.E. status in 2020.

What are the main categories (expenses) this spending breaks into?

- Housing ($30k)- includes monthly rent, utilities, insurance, base services such as internet and entertainment (Netflix, Hulu).

- Insurance ($16k) – auto & health

- Subscriptions ($5k) – includes OrangeTheoryFitness(healthclub), audible, car wash, AppleOne, Google, YouTubeTV, Hulu, Disney+

- Travel ($30k) – We are spending a bit heavy, by design. We are in good health and enjoy traveling, both by car and plane. Realizing slower days are ahead, we have decided to stretch the budget now.

- Installments ($2.8k) Various zero percent purchases, majority end 12/31/2023.

- Special Projects ($8k) for new deck on rental. Side note, we agreed to pay 100% of the cost upfront and take a rent reduction for xx months until 50% of cost has been covered by rent reduction.

Do you have a budget? If so, how do you implement it?

During the 30 years of marriage, I was the budgeting and finance person. There were many times in which I attempted to get my spouse to engage with respect to finances, but she consistently resisted. At some point, I just quit trying. We consistently lived below our means and always saved at least 10% pre-tax into company sponsored 401k plans.

I can still vividly recall arranging bill due dates to prevent ever being short on funds. In the early years, I arranged payment dates over the course of each month to ensure bills would be paid on time. Over time, as my income increased, we managed to keep core expenses down, save for retirement and build up the emergency fund (6-9+ months of expenses).

Eventually, income greatly exceeded annual expenses and we started building up a cash savings to pay for “life events” such as a 3rd car, college education, weddings, etc. Upon turning 50, 401k contributions were increased to the maximum allowable under IRS limits, including the over 50 catch-up. We took advantage of Health Savings Account (HSA), contributing the maximum amount each year. This is a great tool for building up a bucket of money specifically for healthcare expenses.

Post-retirement AND divorce, I am still the spreadsheet king. The significant difference is that my new partner is fully engaged. We are on the same page with respect to when and how money is spent. We balance each other out, especially when one of us begins to worry about daily/weekly market swings. When one begins having a narrow focus on the markets (daily/weekly changes), the other is there to help adjust the perspective and calm the emotional spirit.

What percentage of your gross income do you save and how has that changed over time?

At the beginning of my career, my mother recommended I set up 10% of my income toward the 401k plan. I followed her words of advice. As she explained, upon the first salary increase, I would never ever miss the money going into retirement. By consistently investing, over a long period of time, the magic of compounding interest and dollar cost averaging would build wealth.

As a single income, family of 5, it took more than a few years before we were able to save significant post-tax dollars. We were not living paycheck to paycheck. However, with kids, expenses for food, clothing, school activities, it can eat into the family budget.

Over time the post-tax savings grew. Excess cash was directed into savings to build an emergency fund. Eventually, we accumulated 2 years of expenses.

At this point, the emergency fund was named the “FU” fund. If things at the current job became too unbearable, I could walk away and the family would not suffer. Thankfully, this never happened but I slept well knowing the option was available.

Likewise, it took true financial discipline to NOT spend those funds on glamorous vacations, expensive cars, overpriced clothing and the list goes on and on.

What’s your best tip for saving (accumulating) money?

- Time is your friend, start saving NOW and be consistent.

- Live below your means.

- Make saving automatic. If you don’t see it you never miss it.

- Invest in low-cost index funds.

- Invest in what you know and understand.

- Never follow the herd.

What’s your best tip for spending less money?

Honestly, this is a tough one for me to answer. During my life, I am often “penny wise”, “pound foolish”.

Of course, many may say…Don’t try to keep up with the Jones”. Ultimately, it comes down to a desire to NOT spend every dollar you earn. Having financial discipline. Avoiding living paycheck to paycheck.

What is your favorite thing to spend money on/your secret splurge?

This question took some thought as the answer is based on specific periods in my life. However, I have come to realize that my favorite thing is “experiences”.

Some of the amazing experiences include taking family deep sea fishing, flying an authentic P51 Mustang, soaring in a glider, tandem paragliding, ride in the Oracle Stunt plane (did multiple hammerheads and pulling 8.5Gs.), open water scuba certification, completing the Triple-bypass bike ride in Colorado, completing multiple 100 mile bike rides and vacations.

INVEST

What is your investment philosophy/plan?

- Invest in what you know and understand.

- Start early, be consistent.

- Take advantage of compounding interest.

Day 1 of my career (1987), I set my 401k contribution percentage to 10% and never looked back. The early years were tough making ends meet, but I refused to ever reduce the percentage.

Investment choices were limited to mutual funds, so I looked for those with a solid track record over time (5, 10, 15 years). Typically speaking, I maintained a rather high percentage in domestic stocks, the remaining percentage was in international stocks. Domestic investments were split between blue-chip and technology.

Around 2007, this changed when Apple introduced the iPhone. At the time, Research In Motion (RIM) owned the corporate/mobile market with the blackberry platform. As I watched the Apple iPhone keynote presentation, not only myself, but all the technologist around me reacted in a visceral way.

I was convinced the iPhone was going to be significant and I wanted to invest in AAPL. At that time, my employer was offering a new option in the 401k program called a Self-Managed Account (SMA). I jumped at the opportunity and purchased close to 800 shares of AAPL. During this year, I also purchased shares of EMC, Starbucks and Cisco.

What has been your best investment?

Well, I had to go back and gather up my facts to answer this question.

Two stocks stand out in my self-managed account: Apple (AAPL) and Tesla (TSLA).

Apple had been part of my portfolio since early 2007. As the value of my holdings grew to exceed 6 figures, I would grow nervous with the total dollar weight in my portfolio tied to a single equity. Therefore, I would typically take some realized gains and then invest the gains in other equities. The online system will only look back 3 years and indicates AAPL returned 234%.

After following Tesla for about 10 years, then buying a new Model S in 2017, I began stalking the stock. I wanted to buy shares at around $200/share and missed one opportunity. Then, on June 7th of 2019, I grabbed 100 shares at $206/share.

For those who don’t recall, TSLA then executed a 5:1 split on August 31, 2020 and a 3:1 split on August 25, 2022. After the first split, in September of 2019, I sold 200 shares to lock in capital gains, retaining 50 shares. In 2023, I had to liquidate my entire self-managed holdings to ensure proper execution of the qualified Domestic Relations Order (QDRO) associated with my divorce (long story for another time). My investment in TSLA returned 1,116.6%

What has been your worst investment?

Family Golf Centers (FGCI).

I purchased on advice of friend without doing any homework. Believe my initial investment was $5k and I rode it all the way to zero.

What’s been your overall return?

It took me a bit to look up this information and validate my numbers. On my 401k quarterly statements, they included a quarterly ROI and Annual ROI.

- 2022: -18.04%

- 2021: 18.53%

- 2020: 33.26%

- 2019: 29.38%

- 2018: -2.53%

- 2017: 26.90%

- 2016: 3.64%

Based on these numbers, even with some great years, the average is a 13.02%.

I must call out 2022 as a truly rough year. Due to pending finalization of my divorce, I was unable to make any investment changes throughout most of the year.

How often do you monitor/review your portfolio?

I look at it daily, but just for awareness.

Quarterly, I meet with my financial advisor to discuss and adjust where necessary.

NET WORTH

How did you accumulate your net worth?

My net worth was achieved through implementation of the ESI model, before the ESI model existed. As documented above, through hard work, my career and earnings progressed. Expenses were controlled, which enabled accumulation of post-tax dollars. I took advantage of 401k plans, self-directed broker accounts and defined pension plans.

In the middle of 2016, my mother passed away and I received around $400k in inheritance. This was a combination of P.O.D. accounts, an IRA and an annuity. I was planning to retire in the next 3-4 years, so I rolled over the IRA and annuity to delay paying income tax. If necessary, these funds could be used without early withdraw penalties, as a source of income until I reached age 59.5.

EARN: For me, it all starts with working at a company that provides future opportunities. This translates into income security for the family. As a single income family of 5, my first objective was to earn an income that would provide for the needs of the family and to take advantage of every opportunity to grow my income through career progression. I would never allow my peers to outwork me, and I sought out all opportunities to grow my career and earnings.

SAVE/INVEST: The best move I made was consistently contributing to my employer’s retirement plan at a minimum of 10%.

EXPENSES: The next step was controlling expenses as income grew. If all expenses could be covered before the raise, then the additional income would be translated into savings for a rainy day.

We purchased our first home in 1992 and lived there for 6 years doing a ton of sweat equity; New windows, new roof, finished basement, paver patio, new garage door, new driveway. Upon the arrival of baby #3, it was time to find a larger home. We found our “dream” home, purchased it on in 1999 on a 30-year fixed mortgage. We refinanced the home to a 15-year fixed and then paid it off early in 2018 for “peace of mind.”

When we needed a car, I took advantage of GMAC zero percent financing (free money) and purchased a new Chevy Suburban. This was the family car for the next 15 years. All other vehicles were purchased used and paid for with cash.

Once the emergency fund (6 months of living expense) was funded, we started saving for future expenses. My now ex-wife and I agreed on a life goal – By age 50, we would be in a financial position which enabled either of us to take a job, despite the associated paycheck. As such, when it came to spending money, we would discuss how the expense impacted achieving the life goal.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

All three components are interdependent, but I feel investing is the key. There are only so many hours you can work in a year.

Saving or controlling spending frees up dollars for investing.

Investing enables money to work for you…while you sleep.

The investment moves I made with respect to my self-managed account (SMA) truly accelerated my path toward financial independence.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

There were no significant road bumps along the way.

I say this, because I viewed the journey as a marathon, not a sprint. Staying focused on our financial goals enabled us to make rational decisions with respect to controlling expenses.

What are you currently doing to maintain/grow your net worth?

Working with a financial advisor, we have developed a sequence of returns model. This enables planning of annual income with an eye to controlling income taxes.

Investments are a mix of equities designed to product 50% of annual expenses in the way of dividends. The balance is taken from principle.

We review on a quarterly basis. Having retired 01-April 2020, I have no desire to trade my time for a paycheck.

Do you have a target net worth you are trying to attain?

While still married, the target was $3M which we achieved in 2020, the year I retired.

How old were you when you made your first million and have you had any significant behavior shifts since then?

Around November of 2016, my 401k crossed over the million-dollar mark.

What personal habits and/or traits have you developed that have made you successful at growing your net worth?

Financial education is critical.

Having a general understanding of the markets and investment tools.

Spending time learning from others, establishing a few “trusted advisors” who have achieved success and using them as sounding boards.

What money mistakes have you made along the way that others can learn from?

Investing in what you don’t understand or have not researched.

Family Golf Centers Inc (FGCI) was an investment made based on the opinion of others.

Invest in what you know and understand. If you don’t know, learn. If you don’t understand, don’t invest.

No one will care more about your money than YOU. You don’t have to become an expert, but you do need to be knowledgeable.

What advice do you have for ESI Money readers on how to become wealthy?

- IMHO, there are no short-cuts or overnight success. The race is a marathon, not a sprint.

- Find a career which enables personal growth and competitive wages.

- Day 1, consistently invest in your retirement savings programs.

- Throughout your life, control expenses.

- Establish long-term financial goals and consider those goals when faced with spending opportunities.

- Build an emergency fund which covers 6-9 months of expenses as it enables you to take calculated career chances and cover unexpected expenses.

- Take care of the things you already own to control future “replacement” expenses.

- Plan for future expense and start saving now!

- Whenever possible, avoid interest and fees. Use a credit card, pay the balance off each month. Purchasing a major appliance, look for zero percent interest offers, 90-days same as cash, etc.

- Never spend future earnings – Don’t take a vacation now, assuming you will pay it with a bonus, which isn’t guaranteed. Don’t be Clark Griswold in Christmas vacation.

FUTURE

What are your plans for the future regarding lifestyle?

My net worth enabled me to retire at age 56 and I have no intention of heading back to the workforce.

I subscribe to the thinking that between now and age 65 represent the “go-go” years, so I am enjoying traveling, socializing with others, daily exercise, biking and other adventures.

I am focused on maintaining a very healthy lifestyle of exercise and diet to help keep medical issues to a minimum.

What are your retirement plans?

For the past 3+ years, I have truly enjoyed every day of retirement.

Each day is filled with exercise, both mentally and physically.

Mornings are a time to enjoy a cup of coffee, catch up on email, read a few news feeds which often then drive a deeper dive into specific topics related to current events.

Afternoons are a mix of projects around the house, creative activities such as wood working, making quilt blankets for grandchild, nieces and nephews, connecting with others, spending time outdoors, bike riding, etc.

Gone are the pressures of deadlines, such as completing this interview. 😉

Are there any issues in retirement that concern you? If so, how are you planning to address them?

Like most, healthcare is a significant issue. Fortunately, I was able to continue group coverage, through my prior employer until I am eligible for Medicare.

Another option is the open market (ACA). However, once I turn down the employer option, I cannot go back.

In looking at the details between the two options, I feel the employer option is best. This translates into paying the “full” monthly premium for coverage, which equates to $600/month for a bronze Plus High-deductible plan. As such, this also enables me to continue annual funding of my HSA account. As I continue to be in good health, the monthly premium represents 99% of my medical cost.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

The first financial teacher was my mother. She came from a very modest home and ran the household finances. She taught me the power of saving a percentage of every dollar earned.

I would say teaching began when I was in my early teens, cutting lawns around town. Delayed gratification; waiting for sales. Asking for a discount to pay in cash. The power of compounding interest. Zero percent financing. 90-days, same as cash. Paying off credit card balances each month. Don’t buy what you cannot afford. Take care of what you already own. Do not try and keep up with the Jones’. Don’t flash your wealth.

Who inspired you to excel in life? Who are your heroes?

My parents instilled a strong work ethic, honesty and generosity to others.

I have always been self-motivated and willing to take the path less traveled, never one to be caught up in the herd. As an Apollo program fan, my hero’s include John Glenn & Gene Kranz. Joe Sutter who managed the design team in charge of creating the first Jumbo jet, the Boeing 747.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

My top 3: Millionaire Next Door, How to Retire on Dividends and Bogleheads Guide to Investing.

In addition to these books, I leverage the following sites and/or podcasts:

- NPR’s Marketplace program: provides a nice business summary each weekday and a Friday recap of the week’s events

- ESIMoney – Do I really need to say more?

- Mr. Money Mustache

- Dave Ramsey books and podcasts

- Investopedia

- Techinvestornews

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

Charitable giving is driven not by a schedule, but by how life events touch or call me to action.

I am currently participating in the College Promise Program acting as a mentor to a high school honor student. It is a 4 year commitment on both our parts.

Likewise, giving is personal and I choose to typically make it private. More often than not, if someone asks, I am generous.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

I plan to leave inheritance, but I’m not limiting my “living” to ensure my children have an inheritance.

I believe there are risks associated with generational wealth and frankly, I need to spend additional time and effort in this area of financial planning.

Thank you for the story — on my read it offers a lesson on late-life separations / divorces and the impact such an event can have on a lifetime of saving / planning — I’m sorry you went through that at this stage. I am curious what your financial planner says about your budget vs. assets. Assuming the 2023 budget of $104k includes both of your contributions, you are running slightly under 4% withdrawal rate on your own (no idea of your cohabitant’s financial situation). If $104k is your contribution to combined living expenses then there is probably room for concern. I guess the question for me comes to the strength of your relationship and what happens if it doesn’t work out. I’m guessing your financial advisor is looking at this and offering an opinion, but on my read there is quite a bit of risk (outside of sequence of return) based on your assets and lack of your own housing if the relationship doesn’t work out. It appears your are investing part of your budget in a rental (which you aren’t part owner of?) — again, this is fine if the relationship is strong. I am curious what you are doing for healthcare. Best wishes on your continued retirement.

On the relationship, extremely strong. Regarding annual income(distributions), excess funds roll into ROTH. No rental income. We rent and it works for us. Private owner and we have a fantastic relationship in which I offset cost by handling basic maintenance. Healthcare is through prior employer’s group plan. We can carry this coverage until Medicare.

Big congrats to you on managing through a tough life event post retirement. I’m likely having the same, so love the success stories :). Probably missing something on the numbers..expenses roughly $100k with a $1.5M NW is a 6.6% withdrawal rate, no? Congrats and thanks again for sharing your story.

Yes, ran a bit rich the past year, but we are in our “go go” years and so it was a conscience decision based on the opportunities at hand.

I admire how you enjoy your life and are resilient in the face of a difficult life event, especially after 30 years of marriage. That can’t be easy, and good for you to take care of yourself and still maintain a strong purpose in life and give back. There are many people who spiral down after a divorce, and you’re proof that life can be just as great afterwards.

thank you for such kind words.

Congratulations on your FI goal. Another example of relationship roulette. Sad to hear it didn’t work after such a commitment. Salary history vs spend rate seems out of range. The 10% initial earmark, which is fine as a starting minimum, likely should have increased with salary increases. (Note: I was in a relationship while in college that gave me an education in psychology; habitual lying and cheating. Luckily I dodged that bullet. The other guy eventually had two kids with her and then divorced. He had all the signs. Go figure.)

Regarding the 10%, that was the starting rate day-1. Later, as earnings increased, the percentage adjusted up to hit annual maximum contributions set by IRS, including over 50 catch-up.

Good on ya for keeping up with the cycling! Since our early retirement, my Wife & I have been ticking off completing a century in every state – we’ve got 20 left.