Today I have an update for you from a previous millionaire interview.

Today I have an update for you from a previous millionaire interview.

I’m letting three years pass from the initial interviews to the updates, so if you’ve been interviewed, I’ll be in touch. 😉

This update was submitted in March.

As usual, my questions are in bold italics and their responses follow…

OVERVIEW

How old are you?

I’m 38 and my husband is 45.

We have been married for 8 years.

Do you have kids?

No kids, though we have 12 nieces and nephews – up from 9 at my original interview.

What area of the country do you live in (and urban or rural)?

We live in an urban center in a major Texas city in the same town home we’ve lived in since we got engaged.

What was your original Millionaire Interview on ESI Money?

I was Millionaire Interview 105.

Is there anything else we should know about you?

I had a big head start financially.

My grandparents saved enough to pay for my private college and living expenses with about $250K leftover. I used that money to buy my first condo and a few rental properties in my 20s.

DH borrowed for his liberal arts undergraduate degree and for a full time MBA program when he was 30.

When we got engaged at the end of 2013, he had a net worth of about $108K compared around $820K for me. We did not get a prenup though, as we were earning and saving similar amounts and were comfortable with community property state laws dictating that we’d leave marriage with what we came in with and split what we accumulated 50/50.

NET WORTH

What is your current net worth and how is that different than your original interview?

Today it’s just over $5.3MM compared to $2.74MM 39 months ago when I did my first interview.

Wow, that is crazy to see. (Breakdown below under “Invest”).

What happened along the way to make these changes?

We have pretty much stayed the course.

Our fixed expenses are roughly the same, our discretionary expenses have risen modestly, and our incomes have risen still further, keeping our savings rate the same if not slightly better. Throw in a few years of good returns on our investments and voila.

Our NW has been rising at $650K-$825K per year the last few years and should maintain that pace.

EARN

What is your job?

I’ve a Vice President / Private Banker at a large global bank.

I took this job a few months ago which came with a 27% pay raise and larger bonus opportunity as well.

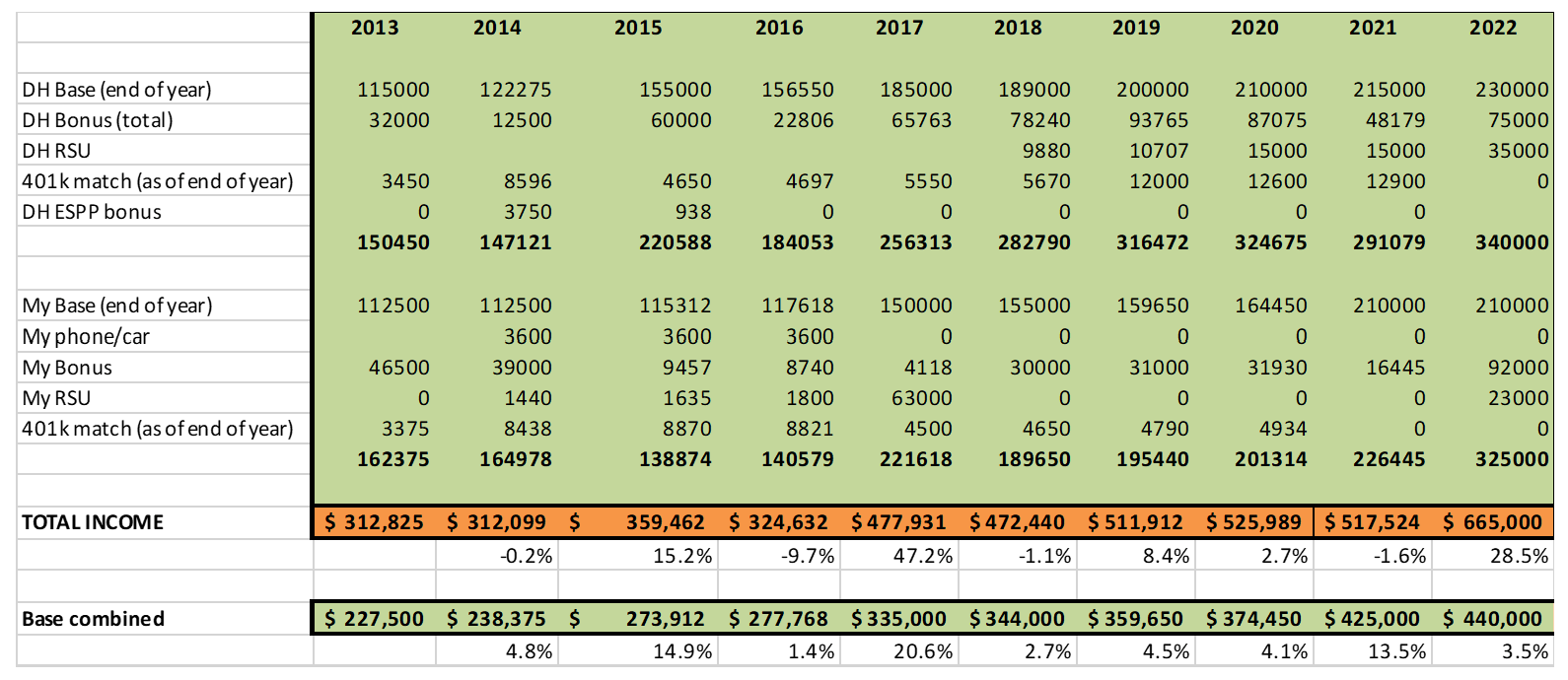

What is your annual income?

Our combined total compensation for 2022 will be around $665K: $440K salary, $167K cash bonus, $58K RSUs, and $0 401k match (I no longer get one, and DH’s firm moved to a once a year match which skips this calendar year).

My salary is $210,000 and my annual bonus target is $115,000, though it’s theoretically unlimited depending on what I bring in. Annoyingly though, I get no 401k match at my new firm because I make too much.

DH just got a promotional increase to $230K for base salary with a 30% target manager bonus.

How has this changed since your last interview?

My previous salary as a private banker right before leaving last fall was $165K, and my bonus target was 20% of base (I was angling for a promotion that would have made it 30%, and I probably would have gotten a $15K to $20K raise too). At my last interview a few years ago my base was $155K with a 20% bonus. I noted then that I expected to be promoted in the next year or so: that never happened.

I was frustrated that my previous employer wouldn’t promote me to SVP over the course of the last two years despite my exceeding expectations in every review and going above and beyond – and despite deserving that title from the day I started at the firm in 2017. Honestly it was just a small family owned company and there wasn’t much room for growth.

Leaving was the best thing for me professionally and financially, but I wouldn’t have done it for a couple more years at least had I not become pissed off and felt undervalued due to the extra hoops they decided to make me jump through before promoting me. I’ll note that this was the first time in my career I felt like the only possible explanation was blatant (if unconscious) sexism, and I was open about that on my way out.

The reality is it was a small family owned firm that had never dealt with much turnover or discontent as it’s such a very cushy no pressure job, so they could afford to be slow to promote and stingy on raises with few consequences. The Great Resignation started to hit them where it hurts though. They’ve since really turned the corner and I hear gave huge raises and bonuses in January nearly across the board.

I like to think me leaving last fall was a big part of waking them up. I left on principle and am proud I stood up for myself, though my husband would say I waited a year too long.

Also, I was being recruited into a prestigious team and the new firm that needed people due to unusual turnover. It felt like a “now or never” opportunity to move to a big bank, expand my role from lending only to include wealth/investment management AND get a big pay raise. I’d considered a similar move 5 years ago but at that time I would have had to take a pay cut to change gears into wealth management since I didn’t have a book of business to move with me.

DH is on the same team he was on previously and has had two promotions in the last few years – to team lead now to manager. He’s worried his incentive comp will drop though now that he’s supposed to be letting go of his portfolio and moving out of a producer role. TBD.

Ultimately he may shift out of banking into a CFO role for one of his clients. He’s recently enrolled in a CFO certificate graduate level course to fill some gaps and be ready if that opportunity ever arises. But the plan for now is for him to take over the team when his boss retires in 18 months.

Here’s the history of our incomes as a couple.

Have you added, grown, or lost any additional sources of income besides your career?

Not really.

My grandparents gave me and my spouse $30K the last two years due to some estate planning that we don’t expect to recur. And several of our real estate syndications have sold off the last 12 months with more expected this year. That’s why we have more cash on hand than usual.

We may buy a wholly owned rental property instead of seeking out more syndications as we are tired of the churn (that’s how the principals make their money – not by buying and holding as we would generally prefer). But our primary income sources are our jobs.

SAVE

What is your annual spending and how has it changed since your interview?

Ooh! This should be interesting.

I’m still using Mint to track our spending so I have the actual figures…these are 3 year averages.

“Today” is as of 12/31/21 and previously was probably as of 9/30/18:

- Federal Income tax & FICA – $171K (was 101k)

- Home – $61K (was $64k -48% mortgage, 18% prop taxes, 16% home improvement, 11% utilities, 7% cleaning/HOA/ins). This probably hasn’t really dropped, but some big home improvement stuff likely fell off the average.

- Miscellaneous – $27K (was $6K). This is DH’s credit card spend plus minor joint entertainment items – after separation we never resynced his cards so I don’t see his itemized expenses.

- Food/Dining – $25k, (was $25K – 36% restaurants, 34% groceries, 16% bars/alcohol, 14% fast food/coffee shops)

- Shopping – $13K (was $20k) (DH’s portion moved to Miscellaneous)

- Travel – $20K (was $13k)

- Auto/Transport – $16K (was $11k) varies depending on new purchase timing

- Personal Care/Golf – $11K (was $11k)

- Gifts/Donations – $9k (was $8k)

- Pets – $5K (was $3k)

- Health Insurance – $5K (was $2k with great coverage at my old job)

TOTAL – $358K (was $264k)

The biggest increase is income taxes, followed by travel and auto due to a new car purchase in the last 3 years. However DH pulled the trigger on a $30,000 graduate program this year which isn’t reflected above. Being able to cash flow that kind of thing is pretty awesome.

We have teetered toward the precipice of major lifestyle increases though. We considered getting a second home a couple of years ago right before covid and shopped around a bit with a realtor even. Doing that may be more likely than upgrading our primary home, though we’ve talked about that too.

It’s just such an increase in cost for a comparatively small lifestyle increase though. DH is starting to hint at wanting to join a golf club which we considered but passed on a few years ago (though the wait lists are years long I think so that’s unlikely anytime soon regardless).

What happened along the way to make these changes?

Our increased income (and recent tax law changes) resulted in increased income taxes for us. Also increased RE values have led to higher property taxes. But other than that we haven’t raised our spending much.

The biggest driver of this has been to stay in our “starter home.” I recently paid $1800 for new drapes and hardware for the bedroom and shuddered at the thought of doing that for multiple if not dozens of windows in a new, larger home if we ever decide to upgrade.

We drive nice cars, but we keep them a long time and don’t drive much. We travel and eat well. We buy designer clothes but infrequently.

We lost one pet but switched from Amazon to a local pet store that is super cute in our neighborhood and happily pay an extra $100 or so a month for their exorbitantly priced canned wet cat food (literally it’s over 2x the price of the canned tuna I buy myself from WHOLE FOODS). But I’ve started paying more to support my local retailers – including Whole Foods – as a lifestyle/neighborhood investment.

INVEST

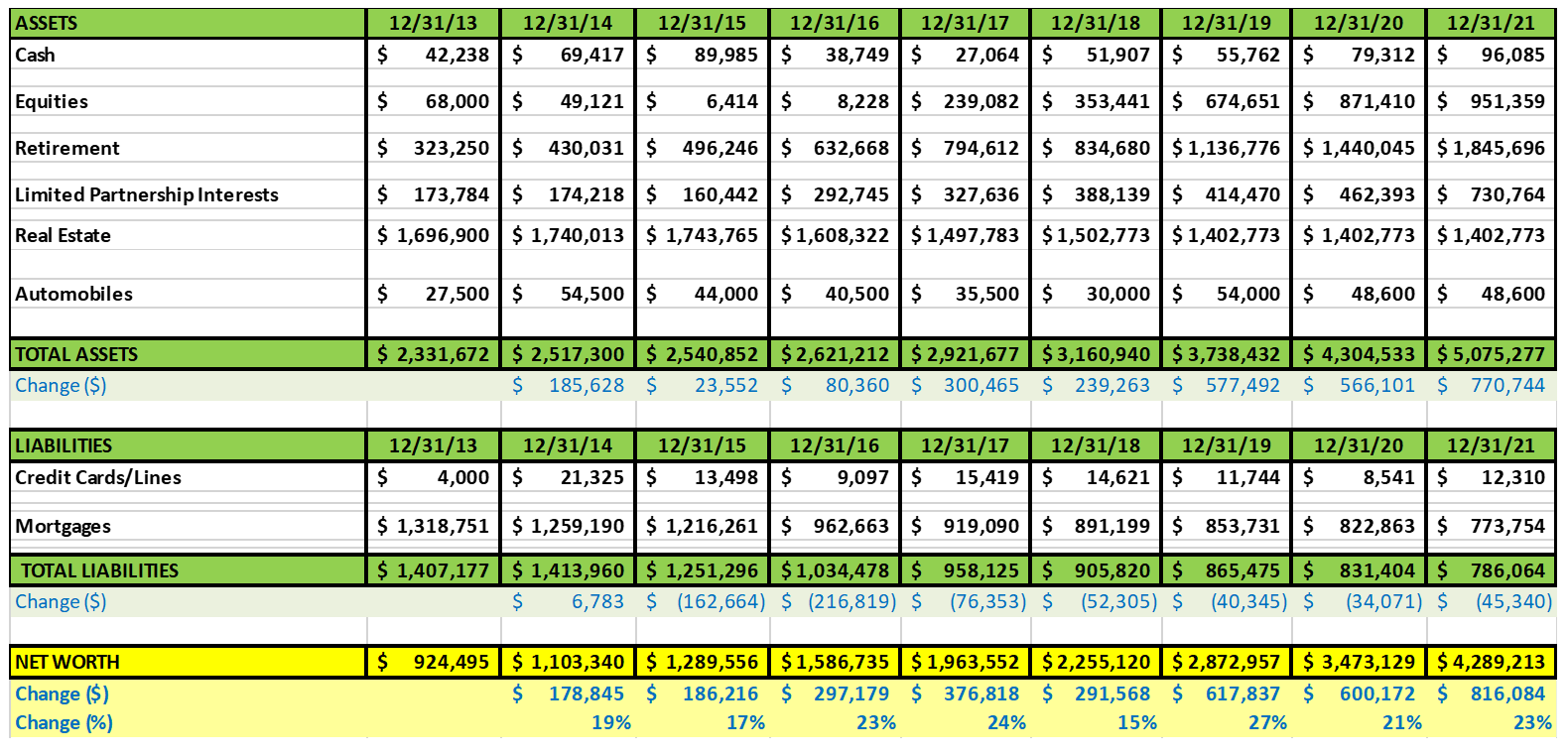

What are your current investments and how have they changed over the years?

The investments are largely the same; we’ve just added to them and the market value has grown. Here is the breakdown – copied from my original interview with updates.

- $339K Cash – was $105,642

- $1,033,868 Brokerage – was $205,458

- $1,769,450 Retirement Accounts – was $919,824 401ks, Roth IRAs, H.S.A., deferred comp plan)

- $668K Restricted Investments – was $473,825 RE multi-family syndications, tech start up accelerator, employer stock/ RSUs). We’ve cycled in and out of many RE syndications in the last 3 years, most of which did very well.

- $2.2MM Real Estate – was $1,933,500. Same properties, just worth a bit more.

- $49K Automobiles – was $34,000 (2 used vehicles)

$6.1MM TOTAL ASSETS – was $3,672,249

- $17K Credit Cards – was $11k (paid in full monthly)

- $0 Auto loan – was $18,495

- $0 Deferred taxes – was $3,168

- $239K Homestead mortgage – was $313,353 (15 year fixed at 2.75%, 12 years left)

- $265K Rental Mortgage duplex – was $130,243 (did a cash out refi and paid off the one below)

- $0 Rental Mortgage condo – was $163,678

- $122K Rental Mortgage duplex – was $139,783 (30 year fixed at 3.0%, 22 years left, mother is lender)

- $135K Rental Mortgage duplex – was $151,337 (30 year fixed at 3.0%, 24 years left, mother is lender)

$780K TOTAL LIABILITIES – was $931,326

What happened along the way to make these changes?

Not upgrading major components of our lifestyle, continuing to save a big chunk of our income and investing regularly. Nothing special – it’s just neat to start to see the compounding effects more dramatically after doing this for 20 years.

Here’s a visual of our NW growth over time since we got engaged and combined finances in last 2013. Note that all real estate is listed at cost which is why it and total NW looks lower that my reported figures above.

MISCELLANEOUS

What other financial challenges or opportunities have you faced since your last interview?

On the surface it doesn’t seem like a lot has changed since my interview 3 years ago, but it doesn’t feel that way.

My spouse and I separated at the end of 2019 and reconciled in March 2020 when COVID lockdowns began. This relatively short-term rupture was fairly traumatic for me (lower case t) as I was blindsided by his discontent and apparent lack of commitment. While I’m happy to say we have an even better and stronger relationship than we did before, it has changed the way I view our combined finances:

- I will no longer consider FIRE/leaning out/taking a lower paying job/retiring until we have sufficient assets and passive income that we will BOTH be financially independent in the event of a divorce after dividing our assets.

- I don’t plan quite so far ahead. I still enjoy my spreadsheets and projections, but they aren’t as detailed, I don’t mess with them as frequently, and I don’t put much weight on the outcomes. I have learned that assumptions about inflation, stock market returns and income can change, but so too can even bigger things like family structure, where we decide to live, and other structural lifestyle realities or desires. I enjoy knowing that I will be ok financially no matter what happens – and increasingly so as my net worth continues to grow.

- I have really loosened the purse strings. Granted, I’ve earned the right to do so financially some might say. But I am really focused more on enjoying my life TODAY versus saving/planning for some magical, theoretical future. I only fly first class now; I only buy designer clothes; I get whatever I want at the grocery store without regard to price. I bought a Mercedes in cash when I found out DH was moving out, being careful to spend exactly what he’d spent on new cars during our marriage compared to me so we’d be “even” if we divorced. It was quite a shopping spree that spring after I realized everything was 50% off if I bought it with our joint account prior to splitting up! I got my first – and last – pair of Louboutins too. They are uncomfortable but gorgeous. When he moved back in I bought a new king size bed, mattress and bedding (we’d always had a queen) and have made some other home improvements we’d always put off.

Maybe it’s reaching what will likely be our peak earning years, maybe it’s deciding pretty much probably for sure not to have kids, or maybe it was almost losing our marriage – heck maybe it’s getting to middle age – but I am a lot more relaxed about money than I used to be. But also more grateful for being financially secure. When my husband left me, the one thing I didn’t have to worry about and which didn’t impact my relationship decisions AT ALL was money. And that was priceless.

Overall, what’s better and what’s worse since your last interview?

Our incomes are better, our income taxes are worse (as a % and $).

Our spending is higher which could be considered “worse” and “better” depending on your definition. 🙂

What are your plans for the future?

Default plan: DH stays in his role and gets promoted again to Manager (different level) and takes over the team when his boss retires in 18-24 months. I stay in my current job and build a book of clients. Our incomes drift up but stay under $500K a year. In 5 years we either retire, overhaul our careers entirely, or become entrenched in our corporate worlds and end up making so much and enjoying our jobs enough that we ramp up our financial goals and spending big time and stay the course over the long term.

Alternate plan: DH takes a job with a client as CFO in the next 1-3 years. Gains a commute but also equity. I flame out from the sales pressure or become disenchanted with the bureaucracy of my job or the excesses of my clients. Abandon the corporate ship to become a writer or teacher or full time auntie/traveler. Who knows?

Marriage plan: We live happily ever after as DINKs. But who knows?! I could get pregnant. We could get divorced. Hope for the best but plan for the worst, as they say.

Given that you have a bit more wisdom and experience, what advice do you have these days for ESI Money readers?

Plan diligently, but be flexible. None of us knows where our lives will take us, from our most intimate relationships to global geo-political events.

Save for tomorrow, but be sure to enjoy today. Incomes and stock markets and interest rates will fluctuate. Don’t waste your precious time trying to predict or over-analyze them. Just earn, save, and invest. Then close the spreadsheet, shut off the screens, and take a walk in nature or hug a loved one.

When I was about 12, I watched my beloved older sister struggle out of a bad marriage exacerbated by her lack of financial independence. That experience coupled with feminism rhetoric of that era molded my personal finance philosophy to always know whose money is whose even if joint accounts are used and to always have the basics of independent finances – money in a single account, my own credit card, etc. In the late 1970s, I had to argue with my employer that I was as full an employee as my husband and deserved my own health insurance. At that time in the fine print, if I were his dependent, he would approve all my medical decisions. Not happening.

I considered these tweaks as insurance in case of a divorce or separation.

We are still married after nearly 44 years, but I am convinced there needs to be spaces for autonomy even within a marriage. Kudos to you for having that mindset.

Thank you for sharing your update and for your honesty about your marriage struggle. That is not something we see much of in this space but it is something that could happen to everyone. I also appreciate the forthrightness about how up in the air your future plans are.

Again, I love your excel tables. Very impressive. Your honesty and openness about marriage struggles is appreciated. Likewise both your earnings and wealth accumulation is also very impressive. It is certainly not easy, but reading between the lines (and also the actual lines) it appears you assume your marriage will likely eventually end in divorce. I recall this standing out in your original MI-105 interview as well. The contingency planning for divorce is a bit of a red flag. If you expect the marriage will eventually end, maybe consider tearing off that band-aid sooner rather than later to increase the odds of a higher number of happier years after this marriage is over. With a bit of reduced spending and a 50/50 split of what you have you already have enough to be independent on your own. You could certainly pad more (and you have a very high income to easily pad quickly) but as out outsider looking in you could easily go it alone financially very comfortably. I recall from interview you had a pre-nup so maybe the split is even more favorable for you. Great update and best of wishes on both financial and personal successes!

“It was quite a shopping spree that spring after I realized everything was 50% off if I bought it with our joint account prior to splitting up! I got my first – and last – pair of Louboutins too. They are uncomfortable but gorgeous.”

You go girl!!!!

WOW – this was a gem!. Interesting to follow your career sucess as well as the stellar progress in your salary/bonus and the net worth you have accomplished. And remember, marriage is even more diffucult to accomplish. Wishing you the best in your future.