Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in September.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

My spouse and I are both 62.

One of the driving reasons behind my wanting to share our story on this forum is because we are a lesbian couple, and when we first got together, there was no legal protection for our relationship, unlike heterosexual marriage. I thought this might be helpful to others in the ESI Money community.

We had a holy union, and that is our “primary anniversary,” but it was not legally recognized.

We married a second time at City Hall, but that was overturned by California’s Proposition 8.

Our third and final wedding was in 2008 when it was legally recognized at the Federal level.

To clarify, all our weddings were to one another. LOL.

Do you have kids/family (if so, how old are they)?

We have two, and both are college graduates.

We paid their undergraduate; they will be on their own if they elect to attend graduate school.

What area of the country do you live in (and urban or rural)?

We live in a quiet pocket of California, technically urban but our street is pretty suburban.

What is your current net worth?

$5.3 million

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

- Tax deferred retirement (401k/IRA/Cash Balance) – $3 million

- Tax free Roth – $105k

- Cash and mutual funds – $1.1 million

- Home – Zillow “zestimate” $1.1 million. Not bad since we paid $305k. We paid off our mortgage in 2018 – an empowering feeling. Many on ESI Money recommend keeping a mortgage, for the tax advantages etc., but being debt free is worth far more than money for our family.

Two cars, paid off, not included in net worth.

No debt.

EARN

What is your job?

My wife retired from a career as a resource and referral manager for a nonprofit childcare organization in October 2020.

I retired from technology project management in June 2021. Three Fortune 500 financial institutions were my employers since the mid 1980s.

What is your annual income?

Annual income, including bonuses, with both of us working was $230k.

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

I worked as a bus girl for a steak house in a small town in the south as my first job, but that didn’t last long.

I worked in white collar secretarial roles through college, with some housecleaning and term paper typing as side gigs.

My Social Security earnings for 1971-1980 (when I graduated from college) were about $4k. I don’t have details about the salaries for those positions, but I recall at 25 getting my first FTE position and it was for $25k.

1991 $40k per Social Security

Steadily up until 2020, at $177k.

My wife’s Social Security earnings for 1971-1980 (when she graduated from college) was about $3k. Like me, she worked in high school and through college for spending money.

1991 $23k per Social Security.

My wife’s salaries were up and down until 2020 when she retired, at $48k. She was in the non-profit sector so her salaries weren’t high, but she had great benefits and (mostly) good work/life balance.

What tips do you have for others who want to grow their career-related income?

- Have a strong work ethic without forgetting that we work to live, not live to work.

- Be proactive, responsive and respectful to others, no matter where they are in the organization, or outside the organization (actively network).

- Enjoy your work and your co-workers, as this will result in others wanting to (1) have you come work for them, (2) come be your co-worker or (3) join your team with you as their manager.

- Don’t over-stress as this is contagious and will make folks around you be stressed also.

- Reach out to others to learn from them – and offer the same to others as they are coming into the field.

What’s your work-life balance look like?

When my wife became a manager she had a ton of stress and worked extra hours (and worried about it when she wasn’t working). She made a decision to turn down an Executive Director position in 2018, and instead took a step down to be a non-exempt employee, taking off the pressure. That step preserved her (and our family’s) mental health.

I was a virtual worker for the last 16 years of my working life, and I absolutely kept to 40 hours (or even sometimes less) per week, most of the time. I got the job done efficiently and am driven to anticipate work, and address things on time or before. I was responsible for setting schedules for complex technology projects with budgets of $1 million, and often more than 30 individuals on the team.

For our software implementations, I would often work evenings and weekends, but those were only about quarterly, and I would shave off hours the following week. I treated my FTE positions as a consultant would, because I valued my time and was highly motivated to have a rich family life.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

My wife and myself are not interested in side gigs. We always felt satisfied with our salaries, kept a relatively simple lifestyle, except for some wonderful vacations, and felt no need to earn additional income.

We are both very active as volunteers. My wife organizes and plays music at our church, and I am currently active with a Covid vaccination volunteering organization, on our local YMCA board, with the local food bank and also at our church etc.

SAVE

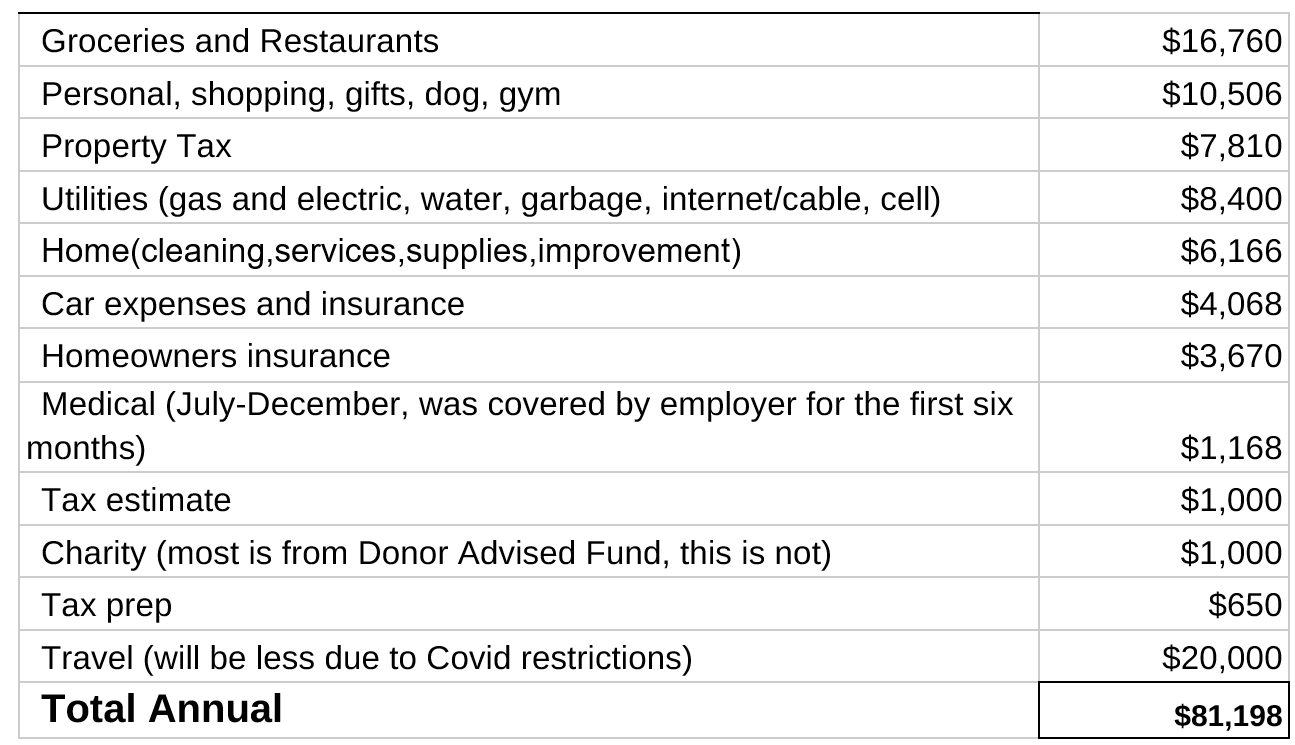

What is your annual spending?

We have budgeted $90,000 per year, including a generous travel budget of $20,000, which of course we haven’t been spending due to the Covid restrictions.

We spent $66,000 in 2021. We are frugal in the large things (home, cars) but enjoy spending on restaurants and travel.

What are the main categories (expenses) this spending breaks into?

Do you have a budget? If so, how do you implement it?

This is the arena that I enjoy and see as a hobby.

Like others on this forum, we no longer budget per se, but do a monthly “look back” using Mint, and notice if there are trends or any alarms. With that software tool it only takes a half an hour each month.

We review this monthly and generally this is good news, because we have tended to be under budget. We are no longer concerned about pinching pennies.

My wife’s contribution to the monthly activities is to update our spreadsheet with our actual balances. We have many different accounts, so this is no small feat. This is a healthy engagement which keeps her in touch with the accounts.

It’s a natural activity for me to update our account information, having worked in financial services for 30 years, whereas for her it takes discipline, so hats off to her. And it’s important that we both have eyes on different perspectives of our assets – she spots things I don’t.

What percentage of your gross income do you save and how has that changed over time?

I have good records for the last 13 years so that is below.

Savings percentage does not include college savings, so that would make the % even higher (listed below are year, AGI, and savings rate):

- 2008 – 165k – 28%

- 2009 – 182k – 23%

- 2010 – 172k – 13%

- 2011 – 178k – No savings data due to laptop virus

- 2012 – 182k – 20%

- 2013 – 203k – 26%

- 2014 – 215k – 21%

- 2015 – 217k – 18%

- 2016 – 213k – 19%

- 2017 – 205k – 24%

- 2018 – 174k – 21%

- 2019 – 196k – 22%

- 2020 – 183k – 27%

- 2021 – 124k – 64% (we socked away a ton to reduce our taxes during our last income year).

Regarding college savings, when we decided to have children, we had 18 years to save $100k for each of them. We were gifted an additional $25k/child from my wife’s parents.

They both elected to attend public universities, so were able to keep within the budget. We had discussed that each would “pay back” $8k after they graduated – but we decided after our youngest graduated, we would surprise them and “forgive” that, leaving them with no debt.

We did not use a 529 account, but just a separate regular checking account, as we did not want restrictions on the use of that money.

What’s your best tip for saving (accumulating) money?

I agree with others in the “ESI world” – pay yourself first – as you get an annual increase (also Christmas or birthday cash, bonuses), sock it away (as long as you are fully paying the credit cards, mortgage, college savings etc) – so you don’t see it as “available” to spend.

Make the savings automatic at the beginning of the month.

Always invest the max in any tax-exempt vehicles (401k, 403b, Health Savings Accounts). It’s so sweet to get the employer match for the 401k and 403b.

What’s your best tip for spending less money?

Pay yourself first.

I also wanted to share an out of the box idea which changed my orientation toward accumulation and spending, and has heightened my awareness for all things “green”. Ten years ago, a friend challenged our church community to reduce our impact on the earth – reducing new purchases (except for essentials like underwear, consumables etc.), instead borrowing or buying from thrift stores. The Frugalwoods, whose blog I enjoy, also have this mindset.

My friend developed a “sharing network”. For example, if I need to clean our carpets, I send out an email to the group: Does someone have a carpet cleaner I can borrow? I will arrange to borrow it, maybe give them the cleaning solution when I am done, avoiding the rental/purchase cost and reducing the impact on the planet by not buying a new appliance for our family. It’s greener, cheaper, and builds community as we inevitably chat when we go borrow/return the carpet cleaner. The Buy Nothing project provides an ability to explore this in your local area.

Our neighbors share their Sunday paper weekly, and I make them a loaf of bread periodically in exchange. We also receive magazines from friends after they are done with them, and in turn, I bring my magazines to our “Little Free Library” or YMCA to share with others. Again, this builds community, saves money and is greener. Plus I don’t enjoy reading online (Other than ESI Money, of course), and don’t want to accumulate more “stuff”.

What is your favorite thing to spend money on/your secret splurge?

We have discovered the Road Scholar travel organization, and have loved the trips we have taken with them.

We look forward to going to Egypt next fall on a river cruise (all participants vaccinated, of course!)!

INVEST

What is your investment philosophy/plan?

We use financial advisors to handle our investments, and they know our risk tolerance and have mutual funds associated with the various sectors.

“Buy and hold” has been a focus.

What has been your best investment?

My best investment, though not measurable, is my relationship with my wife. Our values are in sync – financial, ethical, spiritual, social etc. It has been a wonderful journey going from college age when we had no money, to now when we do not need to worry about it.

Financially, purchasing our second home for $305k, which is now “zillowed” at $1.1 million, was a great investment – we purchased the “worst house on the block” and we have made improvements to it, but it is in a great neighborhood in a high cost housing market, so this appreciation is normal. Our first home was purchased at $175k, sold at a loss at $125k in 1996. The market was very far down but we more than made up for it when we purchased our current home.

What has been your worst investment?

We lost money on our first home but (way) more than made up for it when we purchased our second home.

So I would say I can’t think of a bad investment. Our conservative approach has worked for us.

What’s been your overall return?

For our investments managed by our financial advisors (56% of our assets), return has been great – 2021 was 16%, and the trailing 5 years, 8.5%.

For my 401k (23% of our assets), 8.25% is what we have for the last year (not available for prior years).

Rest is a hodge podge and not easy to retrieve.

How often do you monitor/review your portfolio?

I review our actual spend versus our financials monthly (process described earlier – both spending and investment accounts).

I am lax about policing our investments as I trust our financial advisors to handle our retirement accounts (that is what we pay them a healthy amount to do!), and our asset allocation for my 401k (blend recommended by our financial advisors) is working fine.

NET WORTH

How did you accumulate your net worth?

Mostly we have always saved and left the money in investments to grow.

We received an inheritance from my father-in-law, which made it possible for us to retire a year early. (We opted not to, due to Covid travel restrictions.)

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

Because my wife and I are both on the same page as far as savings, I would say Savings is ours.

We are completely dependent on our Financial Advisors to handle the Investment side.

And Earning is now over – but we both had steady increases in our jobs as well as promotions frequently.

We are both looking forward as we transition to “Enjoy” now that “Earning” is off the table.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

Our bumps were like others in this forum: the market has had downturns. I just stop looking at the account balances for a few months until the dips are over.

Sometimes it has been isolating, and hard to share concerns and ideas related to money with friends and family. We find that they may make assumptions about my wife and myself not having much money, since we live frugally (“stealth wealth” has been cited by Millionaire 94).

We talk about sex, drugs, rock and roll, politics, but cannot talk about personal finances, due to the anticipated jealousy factor etc. This is a great benefit of ESI Money and the MMM forum – to get real world advice about how to draw down from our savings and how to begin enjoying the Spending process.

Without the specific formulas and testimonials from ESI Money, we would have continued working until 65, like a lemming to the sea. I never would have dreamed we would be part of a “millionaire” forum. The site has been very helpful, and I have shared it with others.

What are you currently doing to maintain/grow your net worth?

We have financial advisors who manage our retirement accounts. We don’t really pay attention to that other than seeing what results they are providing for us.

Although I was in financial services for many years, I don’t enjoy the investing side and love that we have delegated that. It is a significant cost but worth it to take it off our plates.

Do you have a target net worth you are trying to attain?

No, we have far exceeded our expectations!

That enabled us to retire early at 62, and we do not plan start taking Social Security until we reach age 70. We feel very blessed.

How old were you when you made your first million and have you had any significant behavior shifts since then?

- 1-2000 – age 41

- 2-2012 – age 53

- 3-2017 – age 58

- 4-2019 – age 60

- 5-2021 – age 62

No behavior changes, but because I was from a very working class background, just sharing the above data is a mind blower.

What money mistakes have you made along the way that others can learn from?

Our first home was in a working class area, and the “best house on the block”.

We were 30 years old, on the upward trajectory for income, and thus should have “stretched” to go to a better neighborhood.

We ended up selling at a loss and paying the brokers on both sides, rather than just pushing ourselves to buy a home once and be done with it.

What advice do you have for ESI Money readers on how to become wealthy?

In our early, low income years, I started on my spreadsheet habit (before Excel was available!), monitoring cash flow. With that as a key tool, we were able to slowly accumulate enough savings for our first home at age 30, then upgrade to our current home at age 37, save more than enough for college for both children, and now to retire early.

Always being aware of your cash flow and, as Millionaire 280 recently said, knowing what gives you joy and applying your time and money in that direction, is essential.

FUTURE

What are your plans for the future regarding lifestyle?

We retired early (October 2020 and June 2021)!

My wife is really enjoying it, as she has her musical interests.

As for me, I’m in the early phases of figuring out how to enjoy my freedom.

What are your retirement plans?

I look forward to lots of travel – I was waiting to retire and excited for the end of the pandemic in June, but unfortunately the variant has raised its ugly head and we are still limited in our activities.

While we are young and healthy, I want to do a lot of travel, volunteering as well as just fun stuff.

We have also taken up birdwatching and pickleball.

We both will take Social Security at age 70, as we want that 8% increase/year. We will live on savings until then.

And at age 72 when the Required Minimum Distributions (RMDs) kick in, we will be forced to withdraw from our tax-deferred savings way more than we need – so have to figure out how to be more generous with our favorite non-profits, children, family etc.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

My wife and I have different “travel cadences”, and we will have to work through how to enable me to travel A LOT (monthly?), and she would like to travel domestically once and internationally once annually, plus local car trips. Of course that is truly a “first world problem” and I’m sure we’ll figure it out!

Others have mentioned Healthcare as a concern, and before I dug into ESI Money, I assumed that we needed to wait until age 65/Medicare to retire.

(1) We are able to use the Affordable Care Act to cover us until Medicare, which was a big (and most welcome) surprise.

(2) I am “anti-insurance”, and so we do not have Long Term Care insurance but will be self-insuring and have allotted dollars for our last three years of life for a senior living facility as well as extended care during the last year or so. It’s sizeable ($700k for the first year, and $1.1 million for the last year), but given the growth of our portfolio, we more than have that waiting in the wings.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

I have been frugal all my life, due to my working class background. In fact, one of my nicknames was “moneybags” as early as junior high.

I have always saved for large items in advance – for example, we paid for our first car via a loan (interest free), but since then, we have always paid cash for them with pre-allotted savings.

This may not be financially sensible, but emotionally, my wife and myself are delighted to always be debt-free.

We also would pre-save for large vacations so we would not be surprised by the credit card bill afterward (paying it off with savings when we get the bill).

Who inspired you to excel in life? Who are your heroes?

My mother never had much money, raising two children as a single mother, but taught my brother and me to always pay off credit cards, save for large purchases, buy quality items so they will last, etc.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

What Color is your Parachute in Retirement was very helpful in having me look not just at the financial aspects (do we have enough money) but also the social, emotional, soft aspects (what will we do with our time).

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

We are big givers, in both time and money, to our church, neighborhood groups and schools and are looking to increase our giving to have more international impact.

We enjoy using our Donor Advised Fund (DAF) to support many political and social causes (it makes us feel like Santa, without impacting our “operating accounts”. (We heard about the DAF on ESI Money.)

We have donated 10% in the past, but now will aim for 15% at minimum, for financial donations. Time-wise, we each volunteer 4-8 hours per week.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

We plan to give both children significant contributions to their down payments, given how expensive home ownership is for the coming generation. This will be in the next decade. We don’t want them to inherit the lion’s share when we die, as that won’t be helpful for them in their later years.

When we die, our children will inherit our home. We may remain in our current home, or downsize. Our plan is to stay in this same region, but that will depend on where our children settle, especially if grandchildren appear.

Great interview! Love seeing the “bootstrapping” from working class to FI. It is always nice to see someone achieve success without having to have had an “over the top” household income.

I hope you have many fine adventures. Egypt is a very cool place. I spent about 3 weeks there, just prior to covid, for a work project. (FYI; worst food poisoning I ever got was from a dessert from the Cairo Hilton room service.) The Saudi German Hospital is not too bad, though, if medical ever becomes necessary while traveling there.

Cheers,

TWW

What a great interview! I love hearing from people who have just put their heads down and saved, while still living a balanced life. Congratulations to you and your wife!

I loved reading your interview. Congratulations on amassing such a nest egg on incomes that were not in the stratosphere and lives with balance.

Great interview. Love when working people build wealth like this when so many people say and think you cannot! Best investment, your wife, never really looked at mine that way but she is, we are so on the same page and that makes things so much better!

Congrats on your retirement from a fellow Californian. I’ll be in retirement in less than two years. You are correct with ESI and MMM forum helping to talk to others about finances without jealousy factor. I have used the MMM forum to gain more confidence to retire at 54. Enjoy figuring out your time in retirement, should be a blast with your wife!

Wow, 54!

Thank you for featuring a same sex story! I wasn’t sure you were open to this and it has given me renewed energy to explore the site and find it relevant.

Agreed! I’m a lesbian and plan to share our story very soon. 🙂 Thanks to ESI for the (and everything), and to all of you who have commented nicely (i.e. no homophobia).

I’ll keep my eyes peeled for your story!

Yea!

Thank you for sharing so many of your details. Congratulations to both of you retiring and figuring out the next phase of your lives. Travel being curtailed was difficult for a few years, but time to start planning again. We are a bit like your wife, no international travel until next year but lots of USA travel. Planning trips is a huge part of the enjoyment and then the actual travel date starts.

I have enjoyed the Road Scholar travel organization as well. My mother and I completed several trips with them before she went to heaven and now I am repeating the trips with my husband. Only this time, I don’t require RS assistance. We did also work with another travel company called Gate One to travel to Australia and New Zealand February 2020. Covid was starting in China but still new. We were lucky we were able to fly back to the USA before Australia was closed. Fabulous trip and great travel company which we will use again for international trips. This year: Sedona, Grand Canyon, South Lake Tahoe, Vegas, Myrtle Beach, Hawaii for 4 weeks and several others. YAY to travel. Be happy and enjoy life.

So excited to have a few trips (mostly domestic but Egypt in the fall, as mentioned in my story) on the calendar. We really love Road Scholar. Take care.

Egypt is on my bucket list. Both of you will have a great time. Glad you are planning USA trips as well.

Congratulations, and job well done! I really enjoyed this interview. You two have done a fantastic job.

Bravo!

Thanks!

What a fantastic story. It is incredible how much wealth you’ve been able to build through persistent saving. As I mentioned in a prior comment, I am also a lesbian and plan to post soon about my family’s journey. Part of my hesitation was fear of homophobic comments, but your story, along with the positive comments, have allayed my fears. Just out of curiosity, are you in North or South CA? I long to move back to CA but the cost of living is intimidating (I’m in the midwest now). Thanks for your post!

Happy to hear from you. I am in Northern California, and it’s not getting any cheaper (it’s ridiculous!). I hope to hear about you in a future ESI Millionaire story. Hearing from you and a few others was precisely why I wanted to write my story. It was also fun sharing it with a few others – but I wasn’t comfortable sharing with the vast majority of my community (whether GLBT or not), unfortunately, due to the envy factor.

My husband and I also thrift. We recycle a lot and donate a lot to charity. Does not matter if we are buying a home, car or hard or soft goods. It always amazes me how we find most anything we are looking for in new or near new condition for pennies on a dollar. It is way too fun meeting other wealthy (millionaires) while “treasure hunting”. I will check out the Frugalwoods blog you mentioned… Thanks.

Yes a wealthy life can be isolating. We also have just about no one to talk to. (I so enjoy reading ESI.) Although, we do enjoy our “stealth wealth”, it give us a lot of freedom. Unfortunately, even when we are asked how we amassed our life style, the reactions are less than desirable. We do hide a lot of our wealth. Otherwise, I’m afraid that the family and friends we have left will never talk to us. We are frequently faced with sarcastic remarks and anger. I do believe it is just not everyone’s cup of tea or desired life style. Loved ESI’s “If you want what I have you have to do what I have done” blog.

Anyway, I’m glad my husband and I are enjoying our lives and have since we were the 15 year old sweethearts in the projects, some 50’ish years ago. Our lives are self made and owned by us… no regrets what so ever.

Best wishes on your endeavors!

Wow, inspirational! You’ve been together even longer than me and my wife! Consider contributing your “millionaire” story in the future here with ESI!

I am so glad and am looking forward to maybe seeing your story featured in the future! That’s exactly why I wanted to contribute.

Great story and wanted to comment Connie but all these readers are so spot on! I have been saying for many years and there is always a common theme of self made millionaires and that is the basic blocking and tackling AKA live well but live below your means. My favorite words today, minimalism, downsizing, dividends and well, Coffee.

God Bless you and your wife.