Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in November.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

By the time this interview is posted, I’ll be 59 and my spouse will be 56.

We met when I returned to college to finish my degree, and we’ve been together for 34 years, married for 32.

Do you have kids/family (if so, how old are they)?

We have two daughters in their late 20s.

We’re fortunate that they live about 10 miles from us.

What area of the country do you live in (and urban or rural)?

We live in a suburb of a southern US state capital.

We relocated here in the mid-90s after living in the Washington, DC area for two years.

What is your current net worth?

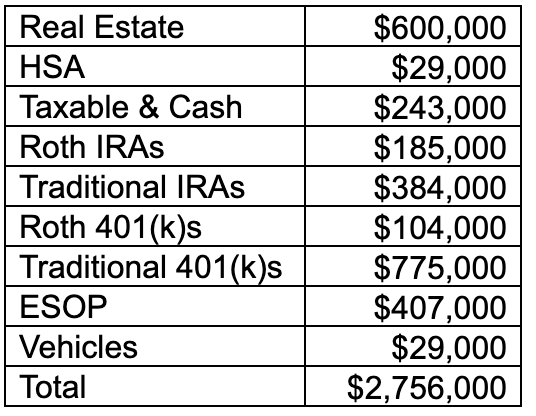

As of September 30, 2025, our net worth was a little over $2.7 million.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

The bulk of our assets are in retirement and taxable accounts. The only real estate we own is our residence.

The ESOP plan is from my husband’s job, and over the next few years, we can start moving a certain percentage to other investments each year. Our mortgage and cars are paid off, and we pay off our credit cards monthly.

We currently have more cash than usual because we’ve got some home repairs coming up, and my husband is considering buying a new vehicle. We may continue to hold more cash in 2026 if we decide that I’ll retire when I turn 60.

EARN

What is your job?

I work as an administrative manager in a large financial institution.

My husband is an executive at a professional services firm.

What is your annual income?

My base income is $92K, and with a generous 401(k) match, total compensation is $101K. My husband’s base salary is $175K.

He gets a 2% match on his 401(k) and a contribution to his ESOP that varies annually, based on profitability. He’s also eligible for a profit-sharing bonus, and this year he got $20K, plus he received an additional $2K for a successful project.

Normally, I’m not eligible for bonuses, but since we received conservative raises, there’s talk of a bonus or a potential salary increase in early 2026. I’m not counting on it, and it will be a nice surprise if it happens!

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

My first job as a teenager was as a typist for a word processing company, and I made $5 per hour (over minimum wage!). My husband’s first job was delivering newspapers, and he doesn’t remember the pay.

He was undecided on his major when he started college, but after he worked a summer job in a meat-processing plant, he decided that he wanted to graduate from college, so he didn’t have to work manual labor jobs.

I worked at a bank the summer after I graduated high school, and I enjoyed it so much that I almost changed my major to finance. However, everyone told me I’d be a great engineer, so I started college as an engineering major, and I stuck it out for two years before taking a break and re-evaluating my goals.

In my early 20s, I worked full-time at a bank for three years. Even without a degree, I was promoted from being a teller to Assistant Manager, before I decided to return to college to finish my degree in Finance.

I worked for the same bank in a different role for two years after graduation, until we moved to our current area. While we were in the DC area, my husband worked for a federal-adjacent agency. Our salaries were in the low-to-mid-$20K range.

Once we moved out of the DC area, we both worked temporary jobs for about 9 months before getting permanent jobs, and our salaries were in the high-$20K range. I worked full-time until we had our first daughter.

Then I worked part-time at night for about 3 years until my husband took a new role and had to travel more.

My husband has been the main breadwinner during our marriage because his career took off with the job he got after our move from DC. He started out in a Marketing role at a salary in the low-$30K range.

Then he moved to IT support, eventually replacing the IT manager, and getting a $20K raise, which allowed me to stay home with our girls. He worked for that company until 2004, when most of the managers and executives were made redundant after a merger.

He’s been with his current employer since 2005 and progressed from Marketing Manager to a VP in charge of several business units.

I worked part-time jobs during most years from 2004-2017, first as a Training Coordinator for a financial institution and then as an assistant to a real estate agent. I could have had higher-paying jobs while my daughters were growing up, but we felt that it was more important for me to be home so that they could participate in activities.

Also, there wasn’t as much opportunity for flexible schedules or working from home during their childhoods.

I didn’t have a job from summer 2007 to fall 2010. My mother was diagnosed with cancer in 2007 and passed away in 2009.

It was a blessing that I was able to spend time with her in her final days and help my dad get through the first year without her. I was the executor of her estate, and it was helpful to have the flexibility to handle all those tasks without another job.

I was also unemployed for part of 2017-2018, and I was able to take care of my dad when he had knee surgery and help my mother-in-law after my father-in-law passed away.

In 2018, I took a job with a $33K salary to get benefits and my foot in the door. In the past 7 years, I obtained some financial licenses and designations, and I was able to increase my income to over $100K.

What tips do you have for others who want to grow their career-related income?

Both my husband and I have a strong work ethic. Doing what you say you’ll do, along with under-promising and over-delivering, helps to get you noticed.

We both became the go-to person for our departments, and promotions and raises followed. If you’re doing the work and not being recognized, it’s time to find another role where you’ll be rewarded.

What’s your work-life balance look like?

Work-life balance is good for both of us, more so for me than for my husband. I never have to check emails after normal work hours, and I only need to log on in the evenings a few times a year to test after updates that must occur after hours.

Occasionally, my husband is required to work on weekends for conferences or when there is a technology upgrade or emergency. Overall, it’s better than earlier in his career when he often had to travel at the last minute because of IT emergencies.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

We don’t currently have any side hustles. My husband has contemplated selling items that he’s made from woodworking or other projects, but he hasn’t parted with anything yet.

My main talents are related to what I do in my job, and I’m not allowed to have a side business that uses those licenses and designations.

SAVE

What is your annual spending?

Total spending in 2024 was roughly $114K from income of about $273K.

What are the main categories (expenses) this spending breaks into?

The main categories of the spending were (to the nearest $1K):

- Taxes – $54K

- Groceries – $10K (including alcohol)

- Insurance – $10K

- Medical – $8K

- Utilities $8K (including cell phone & internet)

- Auto – $5K (gas & repairs)

The best expense of 2024 was about $1,000 for lawn passes to the local amphitheater to see a spectacular line-up of concerts. My favorite was Hozier, and we also saw Foo Fighters, Red Hot Chili Peppers, Chicago, Joan Jett, REO Speedwagon, Dave Matthews Band, Robert Plant & Allison Krauss, Alanis Morissette, Doobie Brothers, Earth, Wind & Fire and many others.

2025’s top categories will be similar, but insurance will be higher because we took out long-term care insurance, and our auto, home, and umbrella policies all had substantial increases.

Travel will likely be the 6th highest expense because of the trips we’ve already taken, plus we have a trip planned in November and more travel to see relatives during the holidays.

Do you have a budget? If so, how do you implement it?

We don’t have a formal budget anymore.

When we made less money, we had targets for expenses, and we had a discussion when a big purchase was planned or if something needed replacement. We’re both frugal and averse to spending unnecessarily, and this has helped us to save money and avoid conflicts.

What percentage of your gross income do you save and how has that changed over time?

When we were younger and my earnings were minimal, we started saving 12% of my husband’s income and increased the percentage from there. Some years when I worked part-time, I contributed to a Roth IRA, but not the max every year.

Since I started working full-time in 2018, we’ve maxed out my 401(k) contributions, and we try to max my husband’s contributions every year. Because he’s a “highly compensated” employee, sometimes partial contributions are returned to us.

These amounts were between $900-$2,400.

During the last five years, we’ve also been maxing Roth contributions for both of us since both daughters finished college. Currently, we’re saving over 30% of our gross income between retirement and taxable accounts.

What’s your best tip for saving (accumulating) money?

Automate savings so that you aren’t tempted to spend the money.

Out of sight, out of mind, helped us to keep contributing to our savings and increasing the amounts as our incomes improved.

What’s your best tip for spending less money?

When possible, wait at least a day to make a purchase. If it’s a big-ticket item, try to wait at least a week.

Sometimes the impulse goes away, or maybe the item will go on sale once you decide you want to buy it.

What is your favorite thing to spend money on/your secret splurge?

Our biggest splurges have been good ingredients and tools to make food and cocktails at home. We eat out more often when we travel, and then we try to recreate meals and drinks.

We are also bourbon enthusiasts, and we’ve been to many of the large distilleries on the Kentucky bourbon trail.

Travel is another splurge that had to go on the back burner the past couple of years. We spent more in that area this year, with a couple more trips planned before the end of 2025, and we have one trip booked already for summer 2026.

INVEST

What is your investment philosophy/plan?

My investment philosophy is to keep it simple. We currently have more investment funds than I’d like because of the options available in our 401(k) plans.

Once we retire, we’ll consolidate more to manage asset allocation.

What has been your best investment?

My best investment was returning to college to complete my degree, with a bonus of meeting and marrying my husband. For financial assets, we’ve never owned individual stocks, so there’s not any single asset that’s had a substantially higher return than others.

We also had good timing when we purchased our house, because within the next five years, prices in our neighborhood increased by almost $100K.

What has been your worst investment?

My worst investment was keeping some of my husband’s IRA money in a fund that was too conservative.

What’s been your overall return?

Looking at our current accounts, returns have averaged 8-13%, cumulatively.

How often do you monitor/review your portfolio?

I look at my 401(k) balance weekly because I have a credit card through that brokerage.

Otherwise, we look at our accounts monthly to quarterly.

NET WORTH

How did you accumulate your net worth?

We’ve accumulated assets from income from our jobs. I got $5,000 as an inheritance and used the funds to help pay for college.

We may inherit some assets when our parents and other relatives pass away, but we’re not considering those in our retirement plan. It will be bonus money if we receive it, and we may also pass some of our assets to our daughters, depending on how much we inherit.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

Our greatest strength has been Save. We’ve only become higher earners in the past 5-10 years, so we prioritized saving what we could.

Invest is second because we’ve mainly invested in moderately aggressive funds for the long term. Our parents all made it to at least their 70s, and we both had grandparents who lived into their late 90s, so we wanted to ensure we grew assets as much as possible.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

We graduated from college in the early 90s when the job market wasn’t great, and we eventually found jobs that had lower pay than we hoped. We did better after moving out of the DC area to a more affordable location.

Another bump happened when my husband was laid off about a year after we bought our current (more expensive) house. I was working part-time and was able to increase temporarily to full-time hours, so we were able to meet expenses, but we couldn’t save during that time.

Then, during the recession in 2007-2008, my husband had to take a pay cut, but at least he kept his job. We continued to live within our means, and fortunately, none of the bumps lasted too long.

What are you currently doing to maintain/grow your net worth?

Since we’re still working, we continue to contribute to retirement accounts, an HSA, and taxable accounts. We’re gradually moving some of our portfolio to less aggressive investments.

Once we stop working, we’ll structure some Roth conversions to take advantage of lower tax rates and set up accounts for a better transfer of wealth to our daughters.

Do you have a target net worth you are trying to attain?

I would like to get to $3-3.5 million in investable assets.

I would never have imagined that figure a few years ago.

How old were you when you made your first million, and have you had any significant behavior shifts since then?

As a result of some changes with my husband’s ESOP, we had to answer a questionnaire that included our net worth. That was when we realized we had crossed $1 million in invested assets, and it probably happened at least the year before.

We were in our late 40s/early 50s at the time.

The most significant change is that we’re able to save more now, because our incomes have increased since then, and our daughters finished college. We also don’t stress as much over meals out or paying for other time savers.

What personal habits and/or traits have you developed that have made you successful at growing your net worth?

We are both good at delayed gratification, and that has cut down on unnecessary expenses, allowing our assets to grow over time. My husband has been able to handle a lot of repairs around the house and with cars, and that has also saved us money.

I’ve cut my husband’s hair since early in our marriage, and that’s saved us over 30 years of that expense.

We’ve owned fewer vehicles than most of our friends and relatives, and we typically keep cars for 12-15 years. We have also spent less on furniture than most of our friends because we bought quality pieces, and we don’t keep up with the latest trends.

What money mistakes have you made along the way that others can learn from?

While not technically a money mistake, I wish we had traveled more when our daughters were younger. We still go on trips together, but it’s hard to coordinate when everyone is working full-time.

Although we have spent more on experiences in the past few years, I still struggle with spending on “non-essentials.” I’m working up to prioritizing travel and other active pursuits before my “go-go years” are over.

What advice do you have for ESI Money readers on how to become wealthy?

Invest in yourself and be a lifelong learner. Being able to adapt can help you grow when others are stuck in the past.

Be willing to postpone some wants so that later you can have more freedom. Live within your means and define your priorities.

Periodically evaluate whether your daily activities and your monetary spending match your priorities, and if they don’t, either your priorities have changed or you need to realign.

FUTURE

What are your plans for the future regarding lifestyle?

I’d like us each to stop working at 60, but that would mean five years before Medicare on an individual health plan for my husband and two years for me.

After I retire, I may start my own financial coaching business, and I would plan to work 15-20 hours a week. My current job doesn’t allow me to use my licenses and designations to earn side income, so I’d have to leave before starting that type of business.

For now, we plan to stay in our home, but we’ve learned to “never say never” to the possibility of living somewhere else or other changes we may need to handle regarding plans in retirement. I’d like to consider a second home in a cooler area because I’m having trouble handling the heat and humidity during the summers here.

We would likely rent before buying to ensure that we really like the area enough to commit to ownership.

What are your retirement plans?

My husband likes to make things, and he’s never short on hobbies, so I’m sure he’ll have no trouble finding things to do after he retires. Since I’m an only child, I’ve been keeping myself occupied my whole life.

I like reading and yoga, and I’ll likely participate in more group exercise once I’m no longer in the office or logged into a computer for 8 hours a day. I’m also going to join a mahjong group soon, and I hope to meet new friends there and increase playing time in retirement.

I may also get into travel hacking once I have more bandwidth to keep track of the promotions.

We each have one living parent, and we’ll likely have to provide care for them during the next 5-15 years, given how long their oldest parents lived. We don’t live near them, and while our current jobs provide flexibility for temporarily working remotely, we may end up taking a leave of absence or retiring early to help them.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

Healthcare in the US is the main reason we aren’t retired already. Both of us have had health issues recently that make us wary of leaving employer health coverage.

How the government decides to prioritize health insurance subsidies will play into our plans for when we decide to retire. We may have to cut back on other expenses during the years before Medicare eligibility to pay for healthcare.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

I was always good at numbers and helped my dad add up receipts when he managed a gas station – I was about 8 at the time. My grandfather would let me watch him pay bills and give me old checks to “practice” paying mine.

I never really had the urge to overspend, and it didn’t take long to get back to a positive net worth after college.

I learned what not to do from my mom – after she retired, she continued spending like she still had her full salary and ran up a large amount of credit card debt. I had to juggle expenses for my dad for a few years after she passed away.

Who inspired you to excel in life? Who are your heroes?

When I was in college, I was assigned A Random Walk Down Wall Street, and while the book wasn’t the highlight of the course, the professor gave lots of good advice. He was able to retire early and teach for fun, and he gave me hope that I might be able to retire early one day.

I won’t be as young as he was, but I’ll be able to stop working before age 65.

My maternal grandparents are my heroes. They kept me while my mom worked, and I spent weekday afternoons, summer days, and many nights at their house.

They taught me so many life skills that kids today don’t get to learn as easily. Although I’m not a fan of gardening, I could do it to grow my own food.

I know how to make simple repairs because my grandfather let me use his tools. They didn’t buy a house until they were in their 50s because my grandfather was a farm manager.

Despite low earnings and my grandmother never working outside the home, they accumulated more than $100,000 before my grandfather’s death in the late 80s. Neither of them graduated from high school, but they had common sense and were so kind.

They were well-loved, and friends and relatives visited them often. I wish that my husband and children could have known them.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

The books that helped us the most came out in the early 2000s. The Millionaire Next Door started us on the path to wealth with the recommendation to save more than 10% of our income.

I’m not sure if it was in that book, but I remember hearing or reading that saving 12% of our income for at least 12 years would give us a good start towards saving the amount we would need in retirement.

The Automatic Millionaire by David Bach gave some straightforward tips on automating savings and other financial transactions to help meet goals with less effort and temptation.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

We currently give limited dollar amounts to charity, supporting mainly local food banks and PBS. I donate a few hours per month for pro bono financial counseling, and my husband occasionally joins his coworkers in volunteering.

We’re just starting to develop a plan to make more substantial donations, and we’re both getting back to more in-person volunteering.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

We plan to leave an inheritance for our daughters, and we may help them by gifting funds or assets while we’re still alive. I’m an only child, and my husband’s sibling doesn’t need the money.

Our daughters say that they don’t want to have children, so we may not have additional family members to inherit our assets. Depending on how everything plays out, we may also make plans to support charities – still a work in progress.

Thank you for sharing your story! I like your comment, “Doing what you say you’ll do, along with under-promising and over-delivering, helps to get you noticed.” This same practice helped me move from entry level worker to state government administrator during the course of my career. Even when I thought no one was watching or caring, department leaders and our clients did and it paid off handsomely for me and my household versus where I otherwise would have been position and salary-wise.

Thank you for your comment! I’m glad to hear that you were able to grow your career and gain salary increases along the way.