Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in October.

This is another long interview, so I’ll break it into two parts.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I am 47 and my wife is 43.

We’ve been married for 5 years, and this is a second marriage for both of us.

Do you have kids/family (if so, how old are they)?

We have two kids from my previous marriage who are 15 and 12.

The kids split time evenly between each parent’s house.

What area of the country do you live in (and urban or rural)?

We live on the east coast in a mid-sized town.

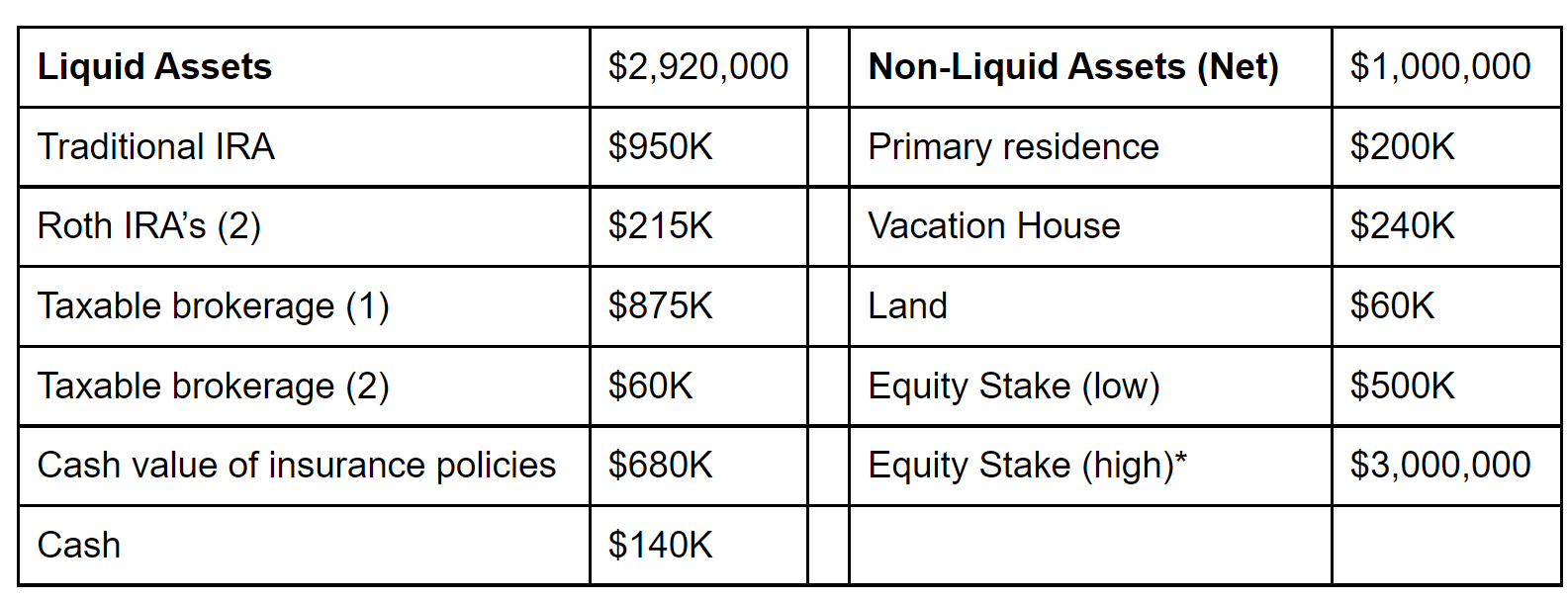

What is your current net worth?

Our Total Net Worth (TNW) is $3.9M on the low end (based on conservatively estimated asset values), and $5.5-$6.0M on the high end.

Our Liquid Net Worth (LNW) is approximately $2.9M.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

We have not yet blended many of our assets, although at some point I am sure they will become more mixed.

Part of the reason we haven’t is that many of the assets are held in a revocable trust with my wife and kids as beneficiaries, which reduces the need for day to day asset blending. There are some exceptions.

Also, 529’s for kids educational expenses are excluded, although we are close to complete on where we need to be with those.

Some of my assets have valuations that are highly variable and/or event driven, like an illiquid equity stake in my company that requires an exit for its value to be accessed.

As a result, I value employment equity conservatively as it has dependencies outside of my control. I’ve put in an equity placeholder of $500K, but realistically the full value is probably closer to $2.0-3.0M (pre-tax) assuming a mid-range valuation.

Real estate values are net value estimates (market value minus remaining mortgage) and will fluctuate. Both properties are titled to a trust primarily for probate purposes.

Our primary residence has an estimated $700K market value, and the vacation house conservatively has an estimated $500K value.

We bought the vacation property to make memories and have time together as a family, so although not truly an investment property, we are quite confident that the value will continue to appreciate as it has already done (up about 30% since purchasing). If we do choose to rent it out at some point, approximately 10 weeks of rent per year would pay for the annual mortgage.

EARN

What is your job?

I am a senior executive at a technology company.

My wife works for a human services organization.

What is your annual income?

Our income can be extremely variable based on results.

We both work full-time and have a household income dependably in the ~$500K range.

Combined, our base salaries add up to $400K, with an additional ~$300K in bonus potential annually.

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

I worked odd jobs in high school, anywhere from lifeguarding to factory work.

I had a high school summer job in a tractor part packaging factory that I thought paid unbelievably well. Work started at 5:30 am and we would work until 2 pm in sweltering heat, lifting cast iron parts laden with grease. For that, I believe I earned the princely sum of about $5.25 an hour which was $2-3 over minimum wage at the time. I remember looking around and seeing folks in their 50’s doing the same work and realized that I didn’t want to be in that situation.

I graduated from college with just one employment offer, which was to be a customer teleservice rep for a large, well known financial institution. It paid $24,000 annually, with no bonus potential and pretty dismal upside. It was so far from my hopes and dreams that I quickly realized I needed to pivot and prepare for a second approach.

I’d considered going to grad school, but had put it on the backburner thinking a couple years of experience would be more valuable. While I could argue that the job market wasn’t great when I graduated, the reality was that I wasn’t a great candidate.

I ran the numbers on grad school, and realized if I could get a job earning 75% of the average of what recent MBA graduates from this school were earning, I’d be breakeven in about 3 years. I applied to my preferred schools and miraculously was accepted to my #1 choice. I used federal student loans to pay for that education, combined with side hustles and even more loans. I certainly didn’t have the grades to get in, but what I lacked in academic accomplishment I made up for in great mentors and advocates who aided my acceptance.

Following grad school I received a couple of job offers, but took one that allowed me to travel around the world setting up a distribution network. The salary was $48K with $12K in bonus potential. I did my own “net worth” calculation on the first day of that job and my net worth was -$84K mostly with student loans, plus an auto loan for a car to get me to/from work.

Fortunately their business in my region grew 300% over the following 3 years. I wanted (and solicited) more career growth and income, but it was a very traditional, family owned business and they simply weren’t willing to change at my desired pace.

It was 1999 and I was desperately trying to get in on the dot.com boom and it was clear tech was here to stay. However, I had no pedigree in technology and it was hard to crack into tech at that time for someone with neither the educational nor professional background. I eventually was recruited into a company that needed someone to develop a specific international region, and they were willing to teach me the technology if I could teach them the ropes in this region.

They offered a salary of $70K, with earnings potential up to about $130K. While I was secretly ecstatic, I braced myself and negotiated. In the end, I was able to get the base up to $80K and total earning potential to $145K at target (with uncapped potential above target). I thought I had made it. Looking back, it was an inflection point in my life that changed everything else.

Over the next couple of years I dug in and learned the business. While every day brought challenges and opportunities, I was growing and learning and meeting some great people. Those years were the first time I cracked into six figure earnings.

In 2004, our company was acquired. The acquiring company offered me a job, but required relocation. I was young, single, and said “why not?” I moved exclusively to advance my career as the location was not an upgrade.

Importantly, it was a larger company with increased access to opportunity. As a young professional, the #1 blocker to my growth was lack of experience, and I was eager to do (almost!!) whatever would give me the experience to move up the ladder.

As I navigated the new company, the role also offered an opportunity to negotiate a different compensation package, and I was able to get to a total income of $200K. I felt unbelievably lucky as in just 5-6 years I had gone from making $65K to making $200K.

A few months later, I received a promotion and in a group meeting several senior executives were talking about compensation, and they discussed how some individuals were exorbitantly below market and debated solutions. They spoke in hushed tones, so I assumed it was confidentially about individuals in their respective organizations.

The next week I received a salary increase of $20K plus $30K incremental bonus potential. I slowly realized that I was the one they were talking about, and I was on the low end because I was the youngest guy at my level by a long shot. The next year I got promoted again, and was a VP at the age of 32. I received another raise, and was given my first “real” equity grant (meaning…more than just a few hundred options).

In the subsequent years I did well. From that point on I didn’t make less than $250K a year, and over the past 12 years the average has been over $450K with a couple of really good years ($700K+) in the mix.

In my profession, there is theoretically unlimited upside, but pragmatically its very difficult to achieve beyond a certain threshold. As a leader, it’s like owning a mutual fund of employees. One can heavily overachieve, but others will regress you to the law of averages. It really helps drive home how dependent you are on making sure your whole team succeeds.

A few years ago, I made the leap from “VP” to “C-level”. The main difference at this level from a compensation perspective is that your cash earnings start to level off, and your upside transitions more to equity realized through enterprise valuation. The equity has much higher upside potential, but because I specialize in growing small and mid-sized tech firms that are either private equity owned or venture capital backed, that equity is illiquid. The company must either be bought or IPO for equity to convert to cash. Both exit paths can carry additional terms and conditions from an employment perspective.

What tips do you have for others who want to grow their career-related income?

I think the most important thing is to make yourself valuable and ideally indispensable. What that entails changes as your career evolves.

Some follow the path of being a subject matter expert, knowing a lot about something specific and usually staying as an individual contributor.

Others grow through demonstrating leadership skills, which was my path.

But along the way even as my role changed, I knew my job and I knew what the company needed from me. I worked hard to overachieve, moving all over the world for my career and setting up offices in multiple countries. I moved my family as well, and that brought its own growth opportunities and stresses. But my leadership knew they could count on me more than anyone else to deliver, and that matters. Being trustworthy matters.

Probably the single biggest game changer for me was leaning in on the maxim of “know thyself”. I know it sounds cliche, but really, truly being honest with yourself and acknowledging your strengths, your limitations, and your likes and dislikes really makes a difference. Self awareness is a gift that keeps giving throughout your life.

I had phenomenal mentors along the way, and they were all so different.

I realized that my biggest strength was authenticity, born of sincerity and the ability to address issues head on. I was given a chance to leverage that into getting others to be better versions of themselves, and to perform at a higher level. I wasn’t the cleverest financier, the best sales guy, the smartest technologist, or the most creative marketer. I just knew how to be diplomatically candid, and build processes to improve. The secret sauce to all of that, if you will, was being honest and being myself.

It took me a while to learn that, but it has been one of the most powerful tools in my career. When you stop trying to be something that you think others expect, and instead learn to lean into who you are, everything gets easier and more instinctual.

Note: “being yourself” does not mean that you get to stop growing and evolving. It’s more that you work on your opportunities for growth from a place of self acceptance.

If you go the management route, my advice is to get as high as you can as quickly as you can either by being the best at what you do, or a consummate team player with whom everyone can work. I learned pretty quickly that I absolutely detested not having a seat at the table and not having a part in decision making. Being in middle management was painful for me, as you are stuck somewhere between the kids table and the adult table in the corporate dining room. While I certainly didn’t need to be the sole decision maker, I did need to be part of the process and the team that debated the issues.

Early in your career, the issues are all about execution. Those skills are important, and will enable you to help others as they navigate challenges. Later in your career, it becomes more about which course you determine to chart, decision making, and navigating the grey zone between black and white. Uncertainty is the home field of Opportunity.

Early in your career, seize opportunities to diversify your experience. Along the road I took many roles above my experience level because I knew breadth of experience was going to be required at the executive level. I would raise my hand to do more whenever an opportunity presented itself (and believe it or not, a layoff is an opportunity in this sense).

You don’t see CEO’s who only know how to do one thing. To be in position for those roles in your life you need to be able to sell, market, operationalize, and speak finance. You need to learn how to develop a culture of success by learning how to evaluate, hire and retain great talent. Those skills require time and opportunity to be developed, so take the opportunities when you get them. You WILL make mistakes. Own them and learn from them.

Lastly, I cannot emphasize enough the value of being positive. People like to work with, and follow, positive leaders. Show up with ideas and solutions, not just problems. Offer to help. Presume good intent.

I’ve seen so many brilliant people lose out because they couldn’t avoid the trap of seeking the problem in a mountain of gold. Be the positive wind that provides lift to those around you. EVERY team needs those people.

What’s your work-life balance look like?

My life is sometimes quite hectic.

In my profession, you go from hero to zero every 90 days, and you are only as good as your most recent performance. It’s stressful and takes a toll.

My kids are also at that age where I am basically their chauffeur from event to event. I love being a dad, and receive so much joy from this facet of my life. However, balancing their needs, my work commitments, investment in my marriage, diet & exercise leaves very little in the tank.

I have a global role which requires some early morning and late night sessions, and when we are not in a pandemic it includes a lot of travel. Over the past 25 years, I have only flown <100,000 miles annually twice (one of those was due to the pandemic). When I look at all of those miles flown, I immediately do the math on how many hours of my life I have spent in an airplane. Contextually, I have flown ~ 4,000,000 miles in my career (and probably almost a million before that). At an average jet speed of 500 mph, that equates to 8,000 hours, or 4 years of 40 hour work weeks in the air.

When you think of that time investment, its pretty staggering as most of those hours are evenings, weekends, early mornings….times when others are investing in their workout regimen or family time. I won’t even try to calculate the airport waits, taxi/uber/train rides, and hotel check ins/check outs. It would blow my mind.

My work weeks vary tremendously. I have occasional “normal” weeks (40-50 hours of work), but there are also weeks where I can work 70. You add in a trip to Europe, South America or Asia for work and you can pretty quickly take out about 20-30 hours just in travel time, often as overnight flights. When I am home however, I am very protective of my personal calendar and my time with family.

Whether real or imagined, my perception is that there is very little down time. Some of that may just be the age of my kids. I have been spending a lot of time thinking about how to rebalance life to enjoy the most of the remaining years I have with the kids at home.

Some have suggested I could just step back into a lower level/less stressful role. However, “knowing myself” has taught me that I am not very good at being lower in the food chain and I think I’m more likely to do something completely new rather than slide down the corporate ladder. My profession is not one where you can really be half in and be successful.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

Not really. Any dividends received are reinvested, and my capital gains are usually quite modest as I am buying and holding for the most part.

We don’t rent our vacation home because we invested a lot of sweat equity and don’t want to continually fix things broken by renters. That being said, we would consider it if it enabled a different lifestyle sooner.

Alternative/passive income is an area I need to develop, but with limited time I don’t want to be an active landlord.

One consideration is how to reposition some of our assets towards more income generating options if I choose to semi-retire or change professions. Real estate syndication/crowdsourcing is something I am interested in understanding better, and would welcome a conversation with any of you out there that are doing it successfully and enjoying it.

SAVE

What is your annual spending?

This one gets uncomfortable for me.

My “spending” is about $250K, but that also includes some investing.

I have kept taxes out of the spending category as I have minimal control over that portion of my income, but I do acknowledge it as the #1 expense.

Everything below is post tax, and also doesn’t include employee sponsored 401k and HSA contributions, which I max out annually.

What are the main categories (expenses) this spending breaks into?

- Primary Home: $42K (includes Mortgage, HOA, utilities, prop taxes, insurance)

- Children: $56K (child support, tuition, summer camps, activities)

- Second Home: $27K

- Groceries: $10K

- Entertainment: $5K

- Brokerage: $80K

- Family Vacations: $10K

- “Other”: $20K (clothing, doctors, vet, gas, auto insurance etc)

Do you have a budget? If so, how do you implement it?

We have come up with budgets before but ultimately don’t really follow one.

Like many others on this blog, I have lived a lot of years just automating saving at the source and living on what is left over. There are things that always pop up, but generally I try to have enough buffer to absorb those while just chipping away at larger goals.

At times I have had to dip into savings. I have luckily reached a point where my “emergency fund” is really just cash on hand to take advantage of dips and other market opportunities.

For the most part, I have about $110-130K+ of savings/investments “automated” each year via contributions to my 401k, self directed brokerage account, HSA, or financial advisor brokerage account. Depending on bonuses, that number can jump pretty decently.

What percentage of your gross income do you save and how has that changed over time?

From my first salaried job until now, I have always been a saver with the bias to invest.

Early on I couldn’t afford to put as much into my 401k, as I was servicing too much debt from my MBA. However, even then I put ~10% of income into my 401k plan and it increased over time.

As you can see above, the brokerage “expenses” are really after tax contributions to my investing regimen, and those do not include me maxing out my Roth 401k & HSA every year.

All in, I save at least 20% and in good years as much as 40-50% of my income.

Given the variability, I have a baseline built around my salary and as bonuses come in they are usually invested or used to pay down debt (all mortgage debt). That being said, I am not paying debt down very much these days as I have restructured it so that long term it is all 3% or lower, which is currently even lower than inflation.

What’s your best tip for saving (accumulating) money?

Automate.

I started small, automatically investing $100 a month. Then I made it $150. Then $100 twice a month, and so on.

The first $10K was really tough. The first $100K felt like an insurmountable mountain.

But then, you adapt, and one day you look up and you are putting $4-5K per month away and not even blinking.

I will say that the first years are by far the toughest. I put myself in a position to earn more so that I could save/accumulate/invest, not spend. I reflect on that early timeframe and I probably underestimate the angst I felt at not being able to do more at that time. I had friends who would mock my underinvestment in clothing and cars, and jokingly say things like “he only invests in appreciating assets”. However, I think I was just pursuing a different dream than theirs.

What’s your best tip for spending less money?

This one is loaded for me, and so I hope you will all forgive this answer, but here it is: marry wisely.

My first wife is the mother of my children, and a really great mother. However, she viewed my 401k investments as a waste of disposable income/potential happiness. She didn’t think twice about spending for our immediate happiness or the immediate happiness of our children. Please don’t misinterpret that as she was spending money left and right. She wasn’t at all. However, we just had different values around investing. Getting divorced was very painful for everyone involved, and was also really expensive (more on that later).

Having a spouse who shares your moral AND financial values is one of the best choices that you can make in life, and I feel blessed to be in a position where I now have that alignment. While we do spend on certain things, those things aren’t really the expensive ones.

I drive an 11 year old SUV that I bought used 8 years ago, and she drives a highly efficient small SUV she bought a few years ago. We shop at warehouse clubs, clean our own home, and I enjoy cooking. We groom our dog ourselves, watch You Tube videos on how to do auto and home repairs, and have started growing some of our own food. We are frugal, but spend in areas we feel really make a difference or that we really enjoy. We tend to invest in experiences.

What is your favorite thing to spend money on/your secret splurge?

Probably travel experiences.

We have limited windows to really go do fun stuff around the world and in our own country, so I rarely think twice about splurging on a good trip.

That doesn’t necessarily mean fancy, but getting to wonderful places can be expensive and some of the experiences cost decent money. I like to go somewhere and then get lost in that location just wandering around.

————————————-

Pretty good story so far, huh? Well, there’s lots more to come!

To read more, check out part 2!

Thank you for sharing! It sounds like your success has been all about taking advantage of your professional opportunities because you were very intentional in your decision making. You knew who you were at the time, knew what you wanted, and made your good skills great.

Congratulations on all you success.

Hi Dan, thanks for the comments. I would love to claim that my intentionality was there at every step of the way, but the truth is probably a blend of “gut” and “logic”. Decisions are steeped in the boiling water of uncertainty, and we all just try to avoid the really bad ones 🙂

This interview is already intense and resonates with me. I lost a good chunk as I didn’t marry wisely. The path from individual contributor to leader is amazing. Looking forward for part 2.

Sam,

I hope you enjoy part 2 as well! Setbacks occur on every journey, and hopefully yours prove to be as surmountable as mine have been.

I’m curious about this quote: “Also, 529’s for kids educational expenses are excluded, although we are close to complete on where we need to be with those.”

What is complete for you? What was the dollar goal you wanted to hit by the time they were 18?

Hi Mary,

In my particular case, I have been targeting around $200-$250K for each child. I recognize that sounds exorbitant, and it very well may be. However, the university I went to many years ago (not an Ivy or even close) is about $70-75K per year now, so my estimate may even be short if my kids opt for something like that. They could just as easily go to a more affordable state school and have a surplus that they could then use for any graduate studies.

My thought process was that I may not cover 100%, but it will likely cover the majority of probabilities.

Thank you! It doesn’t sound exorbitant to me. I have 3 kids so am targeting $200-$250k per child too with the hopes that they balance each other out (meaning one may pick an expensive school but one may pick a state school). Mine are almost 6, 3.5 and 1 so I have a little more time.

I sort of felt the same way. I also have the dynamic that child support will end for me (which is material) and may act as a bit of a natural hedge if I need to provide some assistance.

In part 2 I talk a little bit about how I paid off my student loans. But a little debt is not horrible if the kids require it to complete their studies.

Congratulations on your road to financial independence and looking forward to the second part of the interview.

I’m similar in age and income, also divorced and in a second marriage. That really pushed back my retirement as I am still paying child support 😂. At least I can say I experienced everything this lifetime.

Brian,

I can only say, with a deeply profound exhale, “I understand”.

You live and (hopefully) you learn. In my case, I am hopeful that others learn from my mistakes and don’t have to live them personally.

He could write a blog,book, etc. 🤓

Good stuff for young professionals.

I hadn’t really thought about that until your comment. I am probably better as a guest writer than a real blogger!

Thanks for reading!

Any time you want to guest post — let me know!!!! 😉

Would be happy to! Let me know when you are trying to tackle a specific topic and happy to contribute

I cannot do what you have done.

Your work/life balance is really skewed towards work from my perspective.

You have invested an amazing amount of time and resources into getting to where you are in your career/income level – wow, the travel… I really admire that, and I think you are wired for it.

Do you think you can sustain your time and energy investment in your career until retirement?

I always look at folks in my company who have roles similar to yours and ask myself “how do they do it?”.

At the same time, I recognize and respect their contributions, we need the leaders.

Your trajectory from a grunt to a leader is amazing and rapid. Looking forward to part 2!

Most of us would be surprised at what we can do when we have the right motivations. Working hard is part of most success journeys in some form or fashion, mine just happened to involve airplanes:). Others do the same thing rehabbing homes on nights and weekends, or investing in their business as they build it. Different paths.

I would also add that there are chapters in life for everything. I worked like few others in my 20’s to have the opportunities that arrived in my 30’s. I didn’t have a family then and it was a different equation.

As far as how long that goes, stay tuned for Part 2!

Wait did you start making $145k at the age of 24/25 in 1999?! Holy moly that’s phenomenal.

Congratulations, That’s like $250k on an inflation adjusted basis.

Keep in mind that the “target” was $145k, but almost half of that had to be earned through achieving or exceeding business objectives. Only the base salary was guaranteed.

For the company, it was “free money” if I succeeded. Said another way, they paid me $145k, but I made them well over 10x that. Most of the higher paying career opportunities come with healthy at risk components, and you have to lean in to them.

Wow poor guy. He’s got millions, sure, but sounds like a hectic and stressful life. He’ll burn out and slow down soon hopefully for him and his family it’s not too late. Sad. But there’s light if he can slow down!

Well, after 25+ years I haven’t really slowed down or burned out yet, so maybe I am a slow learner 🙂

Believe it or not, my family life is fantastic and I have coached kids soccer teams, advised youth groups, and celebrated them along the way. I am blessed in so many ways.

As I said above, there is a chapter in life for everything. I may have used mine differently than others. Certainly with each chapter I have had to learn and adapt, and my balance between work, home, faith, and health has changed over the years.

And I hope that continues!

Your cash value number is the most intriguing number to me.

In what way?