Today I have an update for you from a previous millionaire interview.

Today I have an update for you from a previous millionaire interview.

I’m letting three years pass from the initial interviews to the updates, so if you’ve been interviewed, I’ll be in touch.

This update was submitted in March.

As usual, my questions are in bold italics and their responses follow…

OVERVIEW

How old are you?

I am 53, and my spouse is 48.

We’ve been married 18 years.

Do you have kids?

We have two kids together who are 16 and 14. They both enjoy sport a lot.

One plays tennis and one plays cricket, both at representative level. We spend a lot of time traveling about with them.

I also have two older boys from a previous marriage who are in their late 20s / early 30s and independently established.

What area of the country do you live in (and urban or rural)?

We live a couple of hours from one of the large capital cities in Australia in an urban area on the coast.

It’s a very nice part of the world with beautiful beaches and national parks nearby.

What was your original Millionaire Interview on ESI Money?

I was Millionaire Interview 315.

NET WORTH

What is your current net worth and how is that different than your original interview?

Our net worth in Australian dollars is $5.5 million. With the current exchange rate, this works out to be $3.9 million USD.

From past experience in US, I observed that prices for most day-to-day items in the US are very similar in dollar terms to prices in Australia although denominated in a different currency. Thus, something that costs a hundred Australian dollars in Australia will cost a hundred US dollars in America.

Accordingly, I think our AUD net worth of $5.5M would buy a lifestyle in Australia similar to what USD$5.5M would in the States.

Having said that, I will report the rest of the figures in US dollars. Overall, our net worth has grown since the original interview.

The changes are as follows:

What happened along the way to make these changes?

The growth in Retirement Accounts and Brokerage are primarily due to investment returns as we have made limited contributions. The retained earnings are the build-up of a surplus in my new consulting business (more about that below).

One negative is that the Australian dollar has depreciated about 5% since the last interview, which reduces our USD denominated-holdings somewhat. The depreciation was closer to 15% until about 6 months ago when the USD has started sliding, so things are just starting to improve on that front.

Over a 10-20 year timeframe the Australian dollar can move in a range of $0.50 to the USD at a low point, with a high water mark of $1.10 to the USD. It most commonly fluctuates between $0.65 and $0.80. At the last interview it was $0.75 and today it’s about $0.71.

This is a case of swings and roundabouts, and given we measure our wealth in AUD, we don’t worry about this at all.

Another seeming negative is that my income has dropped. However, I don’t describe it as a negative because the drop in income has coincided with a very large drop in my hours worked, commute time, and stress levels.

I now work around 20 hours a week, based in my home office 99% of the time and I have a much freer lifestyle. This is as a result of resigning from my management role in 2023 and commencing a new, one-person consulting company.

What are you currently doing to maintain/grow your net worth?

I’ll keep rolling with my consulting business at least until the kids finish high school. It’s a good flexible option.

At a minimum, I’ll ensure I cover our costs to let our investments keep compounding. Depending on how motivated I feel about chasing new work, I may make a surplus as well.

Apart from that, I am just leaving our funds in the market and letting them compound over time.

EARN

What is your job?

I am an IT management consultant working in a one-man consulting company.

I have six clients on retainer. I do ad hoc consulting projects as well

What is your annual income?

The annual income earned in my consulting business has fluctuated between $200,000 and $280,000.

How has this changed since your last interview?

This is lower than I was earning in the corporate role that I had when I did my last interview. At that time, I was earning $350K – $500K, depending on the size of the short-term and long-term incentive.

Despite the drop, I think I am making a good level of income for part-time employment of around 20 hours per week which is also largely stress-free.

In my last interview, I spoke about my ambition of transitioning to consulting work. I have now done this, although I found it very scary making the leap, even though I thought the time was right.

I was very tempted to extend for one more year. At the time I made my change, I’d been with the organization for nearly eight years and I was well respected in my role.

To give it all up in order to start a consulting company with no known clients and no known work prospects seemed foolhardy from at least one perspective.

To try and ease the transition, I saved 18 months of living expenses into cash in advance of making the move. Despite this, I had many sleepless nights in the days leading up to my resignation.

I gave my company six months’ notice. There were two reasons for this. I enjoyed my full-time role and did not want to leave the company or my boss in a pickle, so I wanted to give them time to recruit a replacement.

At the time I resigned, I also hadn’t started exploring potential consulting opportunities because I did not want word to get back to my employer. However, once I did hand in my notice, I did use the six month notice period to start putting some feelers out.

Making this change has been the best thing that I ever did. I’m so glad that I overcame my fears and pushed through to make the change.

If I hadn’t done this, we would be in a better position financially, but our quality of life would have been significantly worse.

The consulting business has done quite well. I’ve managed to find work and enjoyed acquiring new skills in business development that have been required to get the business established and keep it in continued operation.

I’ve also had some good holidays. Since starting the business, we had a five-week European holiday 18 months ago, and I just had six weeks off over the Australian summer from mid-December till the end of January 2026.

Despite this and despite the part-time work, I’ve still been able to make enough money to more than cover our costs, which has allowed our investments to continue compounding.

My spouse was retired at the time of the last interview, and she is still retired!

Have you added, grown, or lost any additional sources of income besides your career?

No real changes. I left my corporate job, and I started the consulting company.

Apart from that, everything else is largely the same.

SAVE

What is your annual spending and how has it changed since your interview?

We spent about $145K in 2025, which included replacing the carpet and blinds in our house. In 2024, we spent about $140K, which included a 5-week European holiday.

Last time I indicated that our base spending is $75K, but that we might spend anywhere up to an additional $100K depending on the size of the bonus.

Accordingly, I think we are spending at similar levels to previously, and it doesn’t feel like we have tightened our belts at all. If anything, we are possibly spending a little freer.

What happened along the way to make these changes?

I am not getting the big annual bonus that I used to. This has reduced the gap between what I earn and what we spend.

However, our net wealth is continuing to grow. Despite the lower savings, our higher investment balances has still seen us make decent progress in absolute dollar terms.

We are happy to pay the price of slower wealth accumulation in return for the additional time and freedom that we have been afforded.

INVEST

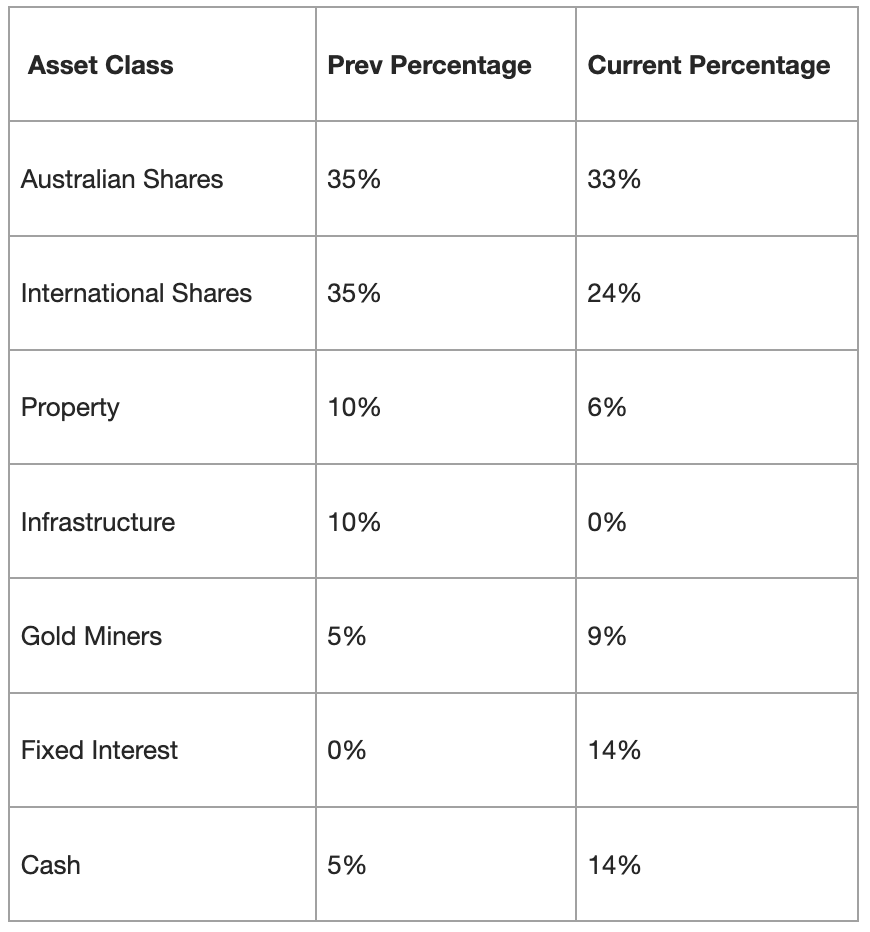

What are your current investments and how have they changed over the years?

Current investments are as follows:

What happened along the way to make these changes?

The portfolio has been tilted to a more conservative basis to protect against sequence of return risk in early retirement. At the time of the last interview, I had 95% invested in growth assets, whereas this has now reduced to 72%.

This has primarily been achieved by reducing holdings in infrastructure and property, and reinvesting dividends from Australian and International Shares into Fixed Interest. This has seen Fixed Interest build up from nothing to 14%.

Cash is also quite high, with a primary driver being the surplus that has been built up in my consulting business. With equities fully valued according to many estimates, I am not in a hurry to deploy this cash at present.

My international exposure is via an ETF that tracks the top 100 companies globally on the Australian Stock Exchange. It’s called IOO and that has been a very good performer over the last several years.

I’ve also maintained a 5 to 10% exposure to gold by investing in three gold miners over the past decade. Despite trimming these holdings recently, they have also done very well.

Performance has been especially good in the last 12 months, but even over the last 10 years that I’ve held them, they’ve been very good investments (7- or 8-baggers so far).

The share price of one holding (CSL.AX) has dropped from $300 to $145 over the past 12 months, but given I bought it for $65, it’s still provided a decent return (~9% per annum over 12 years). It’s a legacy holding (I’m primarily invested in ETFs now) and I took profits on the way up, so my remaining shares are only worth about $10K, so this drop has hardly moved the needle.

Apart from that, I haven’t really had any bad experiences over the last three years.

MISCELLANEOUS

What other financial challenges or opportunities have you faced since your last interview?

I’d been an employee my whole life until starting the consulting business a couple of years ago. Once I started the consulting business, I was surprised how much I enjoyed it. I never really thought of myself as the entrepreneurial type, but I can see that I do have some skills in that area.

One of the big questions that I’ve had to juggle is: Do I actually want to try and grow the business into something bigger? I’ve had opportunities where I could have built a team or taken on more work.

I did wonder whether I could get aggressive and try to build a decent company over the next decade. I think the answer probably is, “yes, I could”, but I’m comfortable with where my life is at now and I have decided not to follow that path.

I’ve made the decision that I ceased my corporate career because I wanted a simpler life and so I’ve generally resisted the urge to engage employees or subcontractors or look for additional work when the books are full.

On the flip side, I’ve also thought about stopping work altogether. Over this last Christmas break, I had six weeks off, and I decided to use this as a mini-retirement experiment.

I wanted to see how I would go with no work tasks and no structure in front of me (although we were still quite busy with kids’ sporting activities).

By the end of the six week break, I came to the realisation that I am still happy doing some work, and my 15 or 20 hours a week provides some structure and challenge which I enjoy. At this point, I am not going to pull the retirement trigger, but I will still keep ticking along at my current rate.

Overall, what’s better and what’s worse since your last interview?

The thing that is much better is the balance in my life. I’ve gone from working longish hours with a 90-minute commute each way on 3 or 4 days of the week, to part-time hours with zero commute.

This has helped me to introduce more purpose and balance into my life.

It’s nice to be able to spend time with the kids each morning before they go to school. I also usually do an activity between 8 and 10 with my wife.

This could either be a game of tennis, a long walk, or a workout in our home gym. I’ve also picked up several volunteering activities.

This includes recording an occasional segment for Christian radio, visiting an elder member of the community and becoming much more involved in my church than I was previously. I have also re-commenced competitive sport (cricket) to augment my casual running and tennis.

All of these have been great changes in my life and much more rewarding than the non-stop hustle and regular stress that came with a senior corporate role.

What are your plans for the future?

At this stage, I’m planning to continue in a similar vein for the next few years. My youngest child still has three and a half years of high school to go.

I don’t think it makes sense to fully retire before he finishes school because we would not be able to travel much anyway.

I think the part-time nature of my work is enough to give me some structure and challenge while also giving me the opportunity to practice hobbies and other volunteering as I move closer to retirement.

Given that you have a bit more wisdom and experience, what advice do you have these days for ESI Money readers?

“One more year” syndrome doesn’t just apply to full-on retiring, but it can also apply to any significant change, such as when I made the leap to start my business. It’s very scary to make changes like that.

But if you’ve thought it through, your spouse is on board, you’ve made appropriate plans such as preparing an adequate financial buffer and considered fallback options, it is definitely worth taking the risk if there is something you have long dreamed of doing.

The worst that can happen is that you need to enact your full-back plan (for me, that may have been getting another job if our savings ran low), but if your desired change works out the way you anticipated (or even better), it’s a blessing and not something you would want to have missed out on because of fear.

The other thing comment is that during the early years and the middle years of earning, saving, and investing, when you seemingly don’t have very much to show for it, it’s very important to stay the course.

Although progress may feel slow in the early days, once you do have a little nest egg built up, it can provide tremendous flexibility and options to live your life in different ways. Although the investment growth may not seem so significant in the early years, you’re planting the seeds and watering the sapling that will become a large tree and provide shelter for many years to come.

Kudos on your career courage and financial success. Do you have a target net worth or time line/age where you will plan to pull the plug towards full retirement?

What a fantastic result for your risk of leaving employment and starting your own business. It’s wonderful that it covers living expenses and allows investments to grow, but at least as wonderful that it is giving you back so much time, and the work is something you are enjoying and basically at your own discretion. Should make a perfect pathway to keep it as long as you like, and whatever level you prefer, and retire entirely if/when you choose to. That’s control over your own life.

Thanks for sharing, I love these 3 yr updates.

Thanks. I don’t have a target net worth at this point. The market will have more say in this than anything I contribute so I am just along for the ride. In terms of timeline, I am planning to keep the consulting going to some extent for the next 2-4 years, probably until my youngest completes school. It may become slower and slower over time.

Thanks for sharing the follow-up story! I like your comment, “This includes recording an occasional segment for Christian radio, visiting an elder member of the community and becoming much more involved in my church than I was previously.”

We have something in common. We also lean heavily on our intimate relationship with Christ. Started well before retirement and by the His grace will last until we leave this earth. Being a part of His body, the Church, gives us plenty of things to do that have great purpose and meaning for our lives and allows us to positively and eternally affect other people’s lives through our volunteer efforts. We also augment this with other fun things like vacations and get-togethers with friends and physical activities to keep us exercised and energized.

May the Lord continue to bless you richly as you follow His plan!