Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in April.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I’m 58 and my wife is 55. We’ve been married 28 years.

Before we got married, we dated on and off (mostly on) for 8 years in a long-distance relationship. We finally lived in the same city after marriage.

Do you have kids/family (if so, how old are they)?

We have one son who is 19 and one special needs daughter who is 18.

What area of the country do you live in (and urban or rural)?

We live in a suburban area on the west coast.

What is your current net worth?

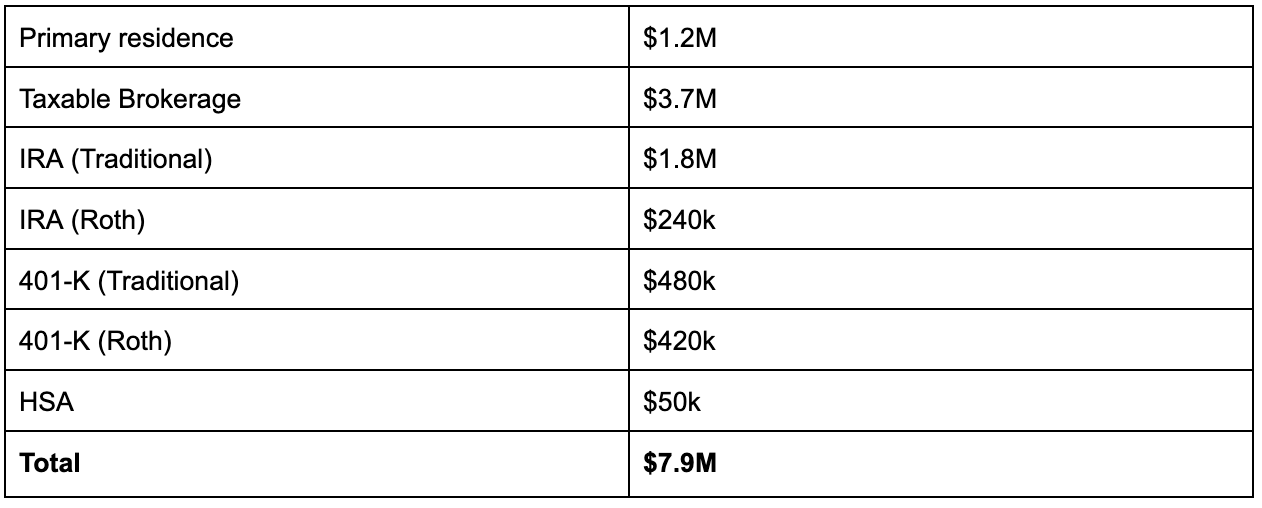

Our total net worth is roughly $7.9M.

During the worst of the tariff tantrum, it was down over $1M from our peak. It’s come back a bit.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

The basic breakdown of our assets are as follows:

Our primary residence is ~$1.2M. Zillow values it at $1.4M+ but I’m discounting it to reflect what I think I would net if I sell it after fees, capital gains taxes, and improvements.

I use Fidelity “Full View” to track investment net worth. Since I need my Fidelity login credentials to access it, I feel safe supplying my non-Fidelity investment account information on the Fidelity platform so I can “safely” see all my investments in one place.

Much of our Roth contributions came from mega-backdoor Roth contributions while employed. During peak earning years, I typically contributed the 401-K max using pre-tax money to lower taxable income and my employer allows in-plan conversions of all mega-backdoor contributions to a Roth.

It’s hard to predict in advance whether I should have done more Roth contributions vs traditional but for most years, it wasn’t even an option as plans were not as flexible 10-20 years ago. I expect to do lots of Roth conversions now that income is lower.

Not included are our son’s UTMA and 529 accounts as we see this as his money.

We have no debt. Home, cars, and all other assets are fully paid for but other than the home, are not included in the net worth figure.

We paid for our home in cash back in 2003. It wasn’t an investment optimal decision but the joy of not having a mortgage all those years more than offset the additional investment gains that would have been earned.

EARN

What is your job?

I just got laid-off but was a Product Manager at a Fortune 50 tech company.

My wife works part time as a Physician Assistant

What is your annual income?

My last full year of income was $230k in salary and bonus. It has been on a gradual decline the past few years due to my “quiet quitting” ways, whereas new equity grants were not forthcoming.

My wife works part-time and averages roughly $45k per year. Investment interest, dividends, and capital gains are on top of this.

Being laid off, I’ll collect unemployment through October. Starting next year, my wife will likely drop to one day a week so she will pull in about $30k per year.

She likes working part-time and wants to keep her skills up. The State just started allowing me to work taking care of my adult special needs child and will pay me roughly $1600 per month so between both incomes, we will likely bring in $48k/year.

I would care for our daughter for free as we won’t make her a ward of the state. Our daughter will also likely get SSI soon which will add another $950 a month.

Our daughter will live with us as long as we are able to care for her.

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

I grew up in a middle-class family on the East Coast. I studied engineering and worked as an electrical engineer for three years at a big tech company before pursuing an MBA.

Upon graduation, I landed a plumb but grueling job as a management consultant. That lasted three years until I parted ways and joined various tech companies.

Jumping from tech company to tech company, sometimes by choice and sometimes because the company was about to sink, I worked as an individual contributor or as a low-level manager and earned around $100k in the late 1990s and pretty much plateaued.

A few years ago, I peaked at around $270k in salary, bonus, and equity but this is primarily due to competitive industry increases for my job skills and increasing RSU share value and not promotions and substantially increased responsibilities. I never hit it big with employer equity-like some folks in tech have.

My spouse obtained a nutrition degree but after getting married, we jointly decided she would pursue a physician assistant master’s degree. She then worked full-time for 5 or so years, took time off to raise 2 kids before they were of school age, and then went back to work part-time.

Her earnings ranged from $60k – $100k back in the early 2000s, then dropped to about a third of that level (after adjusting for inflation) when she went back to work part-time. We earned decent but not stellar pay from our W-2 jobs.

What tips do you have for others who want to grow their career-related income?

My success and advice is for early career moves. I plateaued mid-career so am not the best person to offer insights beyond the early years.

If you are going to school or going back to school, seek a school and major that demonstrates you are one of the best. Employers probably don’t care what you learned in school.

They see school as a way to quickly filter who is good and who is mediocre. My first boss told me he didn’t expect me to learn anything useful in school for my job.

Maybe 2 or 3 days of a couple of classes might be relevant to my job but engineering school simply glosses over broad areas. In the engineering real world, your job is much more specialized and on-the-job training is the only efficient way to learn what’s needed to deliver value to the employer.

I did my MBA at an “Ivy Plus” school. On-campus recruiters flocked to recruit graduates since it was a target school for management consulting firms, tech companies, and banks.

The “halo effect” of my school’s brand name opened some doors post-graduation.

Become a difficult-to-replace, high-impact contributor. I was usually pretty quick to figure out what needed to be done to do my job well with minimal direction from my bosses.

I would self-learn, find and solicit help from a wide variety of sources, and figure out solutions for my boss with the goal of making my boss’s job easier. Deliver quality work as early as possible and proactively solicit feedback early and often to ensure and increase work quality.

Bring a positive attitude regardless of the situation or challenge at hand. I’m not the best at doing this but have found (sometimes the hard way) that negative or hopeless attitudes are usually frowned upon by management.

I’m terrible at corporate politics, don’t suck up to bosses, am not the fastest on my feet in meetings with the bosses, and am quite introverted. My personality doesn’t scream “leader”.

So over the years, I’ve been stuck as an individual contributor and have tended to be pigeonholed in my various jobs mid-career. Sure, there were many things I could have done to improve these skills but I didn’t feel it was worth the effort and frustrations.

I’ve seen younger peers do this and some even eventually became my bosses. I also believe that like sports talent and book smarts, there is also born political and social talent whereas I’m in the low percentile rank.

It would have been hard work for me to bring myself up to a decent skill level just to claw my way up to middle management. I don’t think I would have been skilled enough politically to reach senior management just like I don’t think that even if I practiced all the time, I’d be good enough to make a Division 1 college soccer team.

What’s your work-life balance look like?

In my early 40’s, I lost the lust to climb the corporate ladder. I crossed the $1M net worth mark at around 40 and was on the CoastFIRE path well before I ever heard of the term.

For the last 15 years, I’ve decided that working a 40-50 hour week (not necessarily working all the time, sometimes just face-time hanging around the office) with the aim of preserving employment being the primary goal.

Working at home part-time was also part of the arrangement with post-covid work being 100% remote. I never missed a kid’s sporting event due to work even if the games were in the afternoon as I simply took my phone with me to work/respond to anything urgent.

During my last 2 years of employment, my productivity really dropped. I was pretty much checked out at work and only doing the bare minimum.

I declined business travel when possible and tried to “hide” from bosses and work when I could. I was ready to quit but a smart colleague of mine that I confided in told me not to quit but to wait for an exit package.

Large tech firms are always laying off folks and I guess I was unproductive enough compared to my colleagues that I made the list. So in April 2025, I got let go with a modest severance package.

My work-life balance couldn’t be better now that I’ve been laid off. I’m still in my honeymoon retirement period so life is grand. I still have to figure out my next chapter but I’m building my list of things to try now that I have lots more time.

Do you have any sources of income besides your career?

I have no side hustles other than what was previously mentioned. I do play new customer credit card and brokerage account promo games.

For new brokerage accounts, I have a five-position portfolio with a bit over $1M of index funds (and one stock, AAPL) which I flip in-kind every year from broker to broker to collect $3k – $5k of promotion money per year. I also apply for new credit cards for the bonus points and close them out after a year to avoid the second-year annual fee.

Me and my wife each apply separately for cards and once the minimum spend to collect the bonus is done for a card, I file it away and apply for the next. It drives my wife crazy since she does most of the shopping but it earns us another $2k per year worth of points.

I’m running out of cards to apply for but have a new avenue since our special needs kid is 18 and now an adult. We’re applying for SSI and once approved, we can charge her rent as an adult living in our home so I now have an income-generating side business.

So I should be able to start collecting business credit card promotions pretty soon.

SAVE

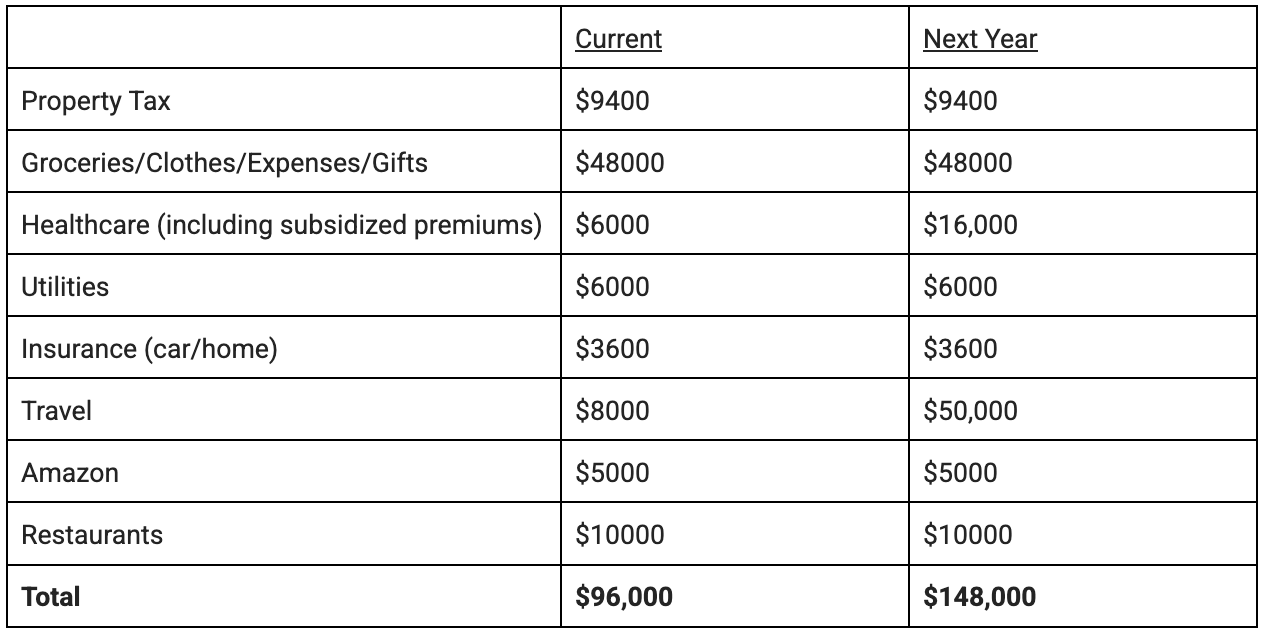

What is your annual spending?

Our spend is roughly $8k per month or $96k per year.

What are the main categories (expenses) this spending breaks into?

Breakdown is roughly:

Because of our special needs kid, we get healthcare premium reimbursements from the State for all of us. That will change now that I’m retired as there is a cap which will be greatly exceeded now that I’m on COBRA.

So it’s going to increase to $1200/mo once the company stops paying for my COBRA as part of my severance. Looking into our State’s healthcare exchange, we made too much money this year to get a better price than COBRA but that may change next year.

Groceries/Clothes/Expenses are what’s dumped on the Fidelity and Costco credit cards which average around $4k/month. All Amazon purchases are done with the co-branded Chase card to get 5% cash back and is typically other crap that my wife buys.

We’re reasonably frugal so I don’t watch our spending that closely. As long as there is a healthy savings rate and we don’t go overboard on expenses, I don’t sweat the details.

Next year with both mostly retired, we plan to dramatically increase our travel. Assuming we don’t get a subsidy, health insurance will also dramatically increase but we should still get some premium reimbursements from the state due to caring for our special needs child.

Our post-tax dividends and capital gains distributions along with any Roth conversions will likely knock us out from collecting any Obamacare healthcare subsidies. With this assumption, next year’s projected spending will likely be close to 3% of investable assets after including income taxes.

Bringing in $48k in income will bring it down to roughly a comfortable 2% withdrawal rate of investable assets.

Our oldest is in college but I don’t include his expenses. A while ago, I set up a 529 and UTMA account for those expenses.

It turned out, he managed to earn a full 4-year tuition scholarship at the State University along with other ad-hoc scholarships. So he’s been able to self-earn a lot of his expenses.

During his high school junior and senior years, I encouraged him to apply for scholarships and said that any surplus 529 or UTMA money is his to keep once he graduates. I wanted him to feel that the money was “his money” so the incentives to win scholarships were fully “reimbursed” for his efforts.

At the time of graduation, he had about $170k combined in his 529 and UTMA. He had a choice of going to an Ivy (but not his top choice Ivy) or going to a State school.

I told him we would fund his Ivy undergraduate education even though it exceeded $170k by quite a bit or he could keep any money we’ve saved for school. He chose State U.

Because he took a lot of AP classes and a few community college courses in high school, during his second year in college he is already taking senior-level computer science classes and on track to graduate in 3 years. He’s also just picked up a part-time and full summer intern job at a FAANG company.

So between the unused college fund and earnings from his job, he will probably graduate $200k in net worth. He’s taking as much as he can of his earnings and dumping it into a Roth IRA and mega-backdoor Roth IRA.

This kid will be 20 and already CoastFIRE! Additionally, we’re still trying to figure out how to burn more of the 529 money as scholarships have covered most of his expenses.

We will likely take advantage of the new 529 to IRA rollover option when available but we still may have excess. It’s a great problem to have.

Do you have a budget? If so, how do you implement it?

We don’t have a formal budget. I monitor every credit card bill line by line mostly to check for fraud but it helps me understand if we’re spending responsibly or not.

I keep all receipts and map receipts to each line item on each credit card bill so I always get a paper bill from the credit card company. If any charge looks high, I’ll read through the receipt. The usual suspect is Costco.

What percentage of your gross income do you save and how has that changed over time?

We saved about 40%. Without a mortgage for over 20 years, it’s pretty easy to do with our income when first maxing out pre-tax 401-k savings.

To get to 40%, the rest went to post-tax 401-k, HSA when allowed, and post-tax investments. 40% got a bit harder to maintain when my income didn’t rise and eventually declined while inflation continued to grow.

What’s your best tip for saving (accumulating) money?

Maximize and automate contributions to tax-advantaged accounts including 401k, mega-backdoor IRAs, and HSA accounts.

Any after-tax savings should be invested in diversified index ETFs (usually better tax efficiency than mutual funds).

What’s your best tip for spending less money?

I use a “point of sale” method of budgeting. Before every purchase, I ask myself 1) Do I need it? 2) Is it a good value?

Most of the time, it’s not a need. There is so much unnecessary crap for sale that if I think about it for just a few seconds, I can envision it (clothes, gadgets, adult toys) just piling up in the house without good use.

Sometimes waiting can yield good sales and waiting before making purchases may help you realize that your original idea wasn’t that great (anyone else re-thought that motorcycle or land yacht purchase?). My wife tends to buy and return.

Costco is the typical culprit. I don’t sweat it too much and just build in a few hundred extra into the monthly “budget” to keep the peace since we can afford it as they typically aren’t expensive purchases.

What is your favorite thing to spend money on/your secret splurge?

We eat out a lot. Neither of us likes to cook due to lack of time.

We will spend on takeout (can be a pain to eat in with a special needs kid) at various favorite restaurants out of convenience. It’s about $1k a month but a splurge we can afford.

INVEST

What is your investment philosophy/plan?

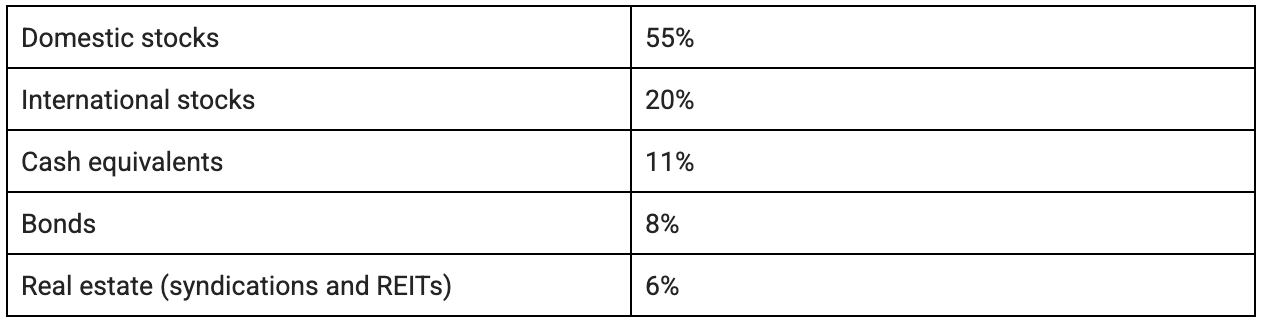

Our overall investment strategy is to maintain a diversified portfolio with a high share of risk assets. We are employing a “barbell” strategy with lots of safe spending assets on one side, and a bunch of risk assets on the other side with little middle-risk bonds and similar assets.

We are targeting:

- Enough “safe assets” to pay for essential expenses and provide a comfortable living for 5 years.

- Additional investment bucket allowing for roughly 3 years of drawdowns of bond assets.

- Invest the rest aggressively in ETF equities, REITs, and alternatives which is 80%+ of investable assets.

- If markets do well, take some profit and use it for extravagant extras like high-end travel, home renovation, new car, etc.

- Maintain between 20%-30% international assets.

- Maintain sector diversification across all equity types to be close to the entire US market and world market as measured by the Dow Jones U.S. Total Market Index (because Fidelity Full View gives me an instant breakdown of this so it’s easy to monitor).

- Allow for 5% – 10% of risk assets as “play money” to scratch the itch of investments in the most aggressive asset classes like individual stocks, real estate syndication projects, angel investments, secondaries, private equity offerings, and/or other opportunities.

Our current portfolio breakdown looks like:

I’ve tried various free calculators with Monte Carlo simulations and they all seem to generate similar results. They all roughly say that if we withdraw a little over 3% of investment assets annually, we have a 90%+ chance of not running out of money before we reach 100.

For this blog, I’m using Fidelity Investment’s calculator since I’m a client and they offer a free calculator that is good enough for me.

My baseline spending assumptions:

- $10,000 per month spent, increasing with inflation every year.

- Both spouses collect social security when we turn 70. Older spouse collects $2,000/mo. and the younger collects $1,500/mo. (Likely much less than what we actually get, even if social security is cut)

When running the calculator with “conservative” assumptions, the numbers look fine with well over 90% chance of not running out of money at age 100 for either spouse. And this did not include social security.

Apparently, the Fidelity calculator reduces your assets by 17.5% upon retirement in their “significantly below average” scenario. I don’t know why but I’m guessing they used some back-testing and statistics on the sequence of returns to come up with that number.

I won’t overthink this since any calculator is only used to give you a ballpark idea of what your spend-down profile might look like.

Looking at our expenses for the past few years, we spend roughly $8k per month. It helps to have a house that’s paid off.

If we have to include self-pay health care insurance, that may add up to an extra $24k / yr. which will bring us up to $120k/yr. I don’t expect the tax rate to be that high since most of the income will be taxed at the long-term capital gains rate until RMD kicks in.

This level of spend is also consistent with other bloggers similar to our situation who are retired and publish their spending rates.

My “free” Fidelity financial planner also agrees this is a typical spend rate for households like us and he has several clients who are retired with around $3M in their portfolios and are doing fine. We have double this so we should be fine spending a bit over $200k per year.

What has been your best investment?

I’m no stock-picking guru but got lucky buying AAPL over a decade ago that is my only 10 bagger. I have a “play money” account that allows me to invest up to 10% of investable assets in more speculative ventures.

My AAPL $10k investment is over $160k now and offsets a number of less-than-stellar bets (like ZM and AAL which I bought during the pandemic after they dropped).

What has been your worst investment?

My worst investment was the purchase of private shares in a startup stem cell research company where my brother is a member of the advisory board. Although the minimum investment was $100k, I was granted an “exception” due to my relationship with a board member.

That was a red flag. Apparently, they were desperate for money and accepted me at $20k.

The investment went to $0 and the former CEO was accused of financial malfeasance.

What’s been your overall return?

It’s been a couple of percentage points below the S&P average for a number of years. This is due to my exposure to international stock, REITS, some bond/cash holdings and mid/small cap holdings.

Recently, reversion to the mean is starting to happen so the gap is closing.

How often do you monitor/review your portfolio?

Sometimes every day. I have a Scrooge McDuck in me that likes seeing my net worth go up.

But when the market is down, I play ostrich with my head in the sand and don’t look at my portfolio and net worth as often. I’m pretty good at sticking to the financial plan so there’s no need to look at it often.

I rarely sell and continue to keep the automated buying on autopilot.

NET WORTH

How did you accumulate your net worth?

Some of the biggest factors that boosted our net worth:

- Got college degrees in lucrative fields and got those degrees early. This included me encouraging and supporting my spouse to get an advanced degree in a better paying and more interesting field early as well.

- Got out of debt as fast as we could. We paid off our expensive private school loans quickly and lived cheaply to do so.

- Paying off an 8% interest student loan is the same as getting risk-free after-tax returns of 8%.

- We always save and pay for our cars in cash. We drove used ones until we could easily afford new ones which we treated as luxuries. We also paid off our mortgage quickly.

- Lived below our means and invested all our savings. Investing early got us a longer time horizon to let compound interest do its work.

- We primarily invested in low-cost, diversified funds and subsequently ETFs. Individual stocks are limited to “play money”. We limited real estate investments to REITs/syndications but may look into expanding this in the future.

- Had kids later in life and are not “overspending” on them. Kids are expensive so saving and subsequently investing that extra money prior to having kids had a huge impact on our eventual net worth.

There are many personal trade-offs here and doing this just to have more money may not be smart. We chose public school for our kids since our school district is decent (not stellar).

You can’t always afford the “best” for your kids and private school for 2 kids is a huge expense that we didn’t think was worth it.

Looking back at our game plan, none of it is earth-shattering and any decent personal finance blog or personal finance book will tell you the same thing. Our key to success was consistency, patience, and perseverance.

Hiccups happen. I was laid off during the dot-com bust and was unemployed for over a year before having to relocate to pick up a new job, causing my spouse to look for new work.

I joined a failed start-up and got laid off. My spouse left work and then shifted to part-time work 1-2 days per week to care for kids, including one with special needs.

But we stayed on track the best we could and were fortunate to ride two great bull markets over the years without panic-selling during the down years including the dot-com bust in the early 2000s and the housing “financial crisis” in 2007-2008.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

In my early years, it was earn. I was on a path to potentially make Partner at a prestigious global management consulting firm.

Real-world employment then hit and I learned that good grades and a resume full of potential isn’t enough to get you to the next level. In the later years, saving and investing dominated increasing net worth.

Our lifestyle creep was contained. We bought our house with cash and never upgraded in 20+ years allowing us to save a lot of income.

Although we bought new cars, we kept all of them for 15+ years. Since housing and transportation are typically the two biggest household expenses, containing those expenses helped us save a lot.

We invested those savings primarily in diversified stock funds/ETFs and never sold during big downturns including the dot-com bust, the great financial crisis, COVID, and now the tariff tantrum.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

Our biggest financial setback is caring for our special needs child. My wife stepped back from full-time work to carry the majority of the load of caring for our two kids with the intention of going back to work once the kids started school.

The demands of caring for our special needs child took priority and we likely lost over $1M in potential wages which would have more than doubled over the years if invested. We deliberately decided to have children later so she could go back to school and establish some work experience before taking time off.

It is much easier to go back to the same or similar clinical healthcare job after leaving it for a few years compared to technology jobs. Evolution of the human body is much slower than tech and clinical techniques don’t change that quickly so it’s a good profession if you want to take years off and then go back to work.

But carefully laid plans can easily go out the window when life happens. That said, we have more than enough now so it’s all good.

What are you currently doing to maintain/grow your net worth?

We’re sticking with our game plan that has worked thus far. One could say we’re taking on too much risk after “winning the game” but I’m comfortable with a $600k cash buffer and $500k bond buffer.

This leaves over 80% in high-risk assets. $1.1M is close to 10 years of “essential expenses”. I don’t like leaving too much money on the table.

Do you have a target net worth you are trying to attain?

I’ve heard your target net worth is double what you have now. But I think we’ve just hit our sweet spot of $8M.

I’m still targeting $10M since it’s a nice round number.

How old were you when you made your first million and have you had any significant behavior shifts since then?

We hit $1M when I hit 40. It was a ballpark estimate since half of our net worth at the time was our house so it’s unclear when we actually hit the 2-comma club.

We both self-funded graduate degrees at expensive private schools so that caused a big drag on wealth accumulation both in tuition and living expenses as well as foregone earnings. Both our graduate degrees enabled us to more than double our salaries post graduation so they were well worth it.

What personal habits and/or traits have you developed that have made you successful at growing your net worth?

Discipline and consistency were the key for us. The ability to spend below our means and consistently invest the savings through thick or thin did it for us. It really was that simple.

I will add that my mother served as a good role model. My dad never earned 6 figures as a professor and my mom earned much less as a research lab manager at a university.

Yet they raised 3 kids and my mom now has a net worth of over $7M using the same investment strategy and discipline we use.

What money mistakes have you made along the way that others can learn from?

No real money mistakes other than my worst investment mentioned earlier.

What advice do you have for ESI Money readers on how to become wealthy?

Make a plan and stick to it. I mentioned earlier that our biggest wins came from perseverance and patience in sticking to the plan.

Make intelligent trade-offs and stay balanced. In hindsight, I may have been too fixated on our financial progress and lost out on some of life’s joy by trying to save money but now I try to spend more mindfully in our journey through life.

What’s right for us may or may not work for you. You can factually analyze most of the financial aspects of retirement planning but in the end, an enjoyable (and hopefully early) retirement is about having the freedom to do what you want without worrying if you have enough money.

How much is enough is a state of mind as much as it is an actual net worth, cash flow stream, and set of risk probabilities. How you view different factors of risk, what lifestyle you want and how much work and sacrifice you’re willing to put in to achieve a certain FIRE lifestyle are all highly personal.

It’s more than the risk of running out of money. It’s also the risk of working too long or hard and missing out on life’s joys.

You need to figure out what you want balanced against the sacrifices you are willing to make that best fit your own unique self.

Good personal finance blog sites are the best sources of information for me. I think blogs are more timely than books. Also, I’m not a book reader.

I think just about anyone can find a few bloggers that are in similar situations to them such that their advice and experiences are relevant and meaningful.

FUTURE

What are your plans for the future regarding lifestyle?

I’m just entering my 3rd act so I plan to do a lot of experimentation. For the most part, getting laid off was the plan and I burned some bridges being a slacker to the point that my bosses wanted to get rid of me and gave me a severance.

I don’t recommend this plan unless you’re absolutely sure you don’t plan to work in your industry again.

What are your retirement plans?

I’m just starting to formulate my new set of hobbies and activities. I’ve taken to heart blogger Fritz Gilbert’s (Retirement Manifesto blog author) advice to keep experimenting until you find what you like.

Extensive slow travel is definitely in the cards when my wife will step down to limited part-time work next year. I plan to increase gym time to 3-4 days a week and am making new friends there.

I’m looking into various volunteering activities that have a mentoring/teaching component to them, want to try my hand at cooking, pick up keyboard/piano again, perhaps try some songwriting, try some pickleball, maybe join an old man’s soccer league and try a variety of other stuff to see what sticks.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

Healthcare and health care concerns. Cost-wise, it’s probably an irrational concern as we can likely absorb very high healthcare costs.

And although we’re both generally healthy, healthspan is always lurking as we age. I’d like to think we have a good 30+ years of healthy living where we can still run/walk and do things independently but small health issues like rotator cuff injuries, and minor knee and back pain have peaked our concerns.

So we want to prioritize participating in more active hobbies and activities sooner vs later.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

I think compound interest and investing in a diversified set of stocks started to click at age 14. At that age, my mom gave me and my brothers each some shares in a mutual fund as a Christmas gift to introduce us to investing.

I’m somewhat mathematically inclined (Dad was a math professor) so compounding interest was not a hard concept. And during the go-go ’80s, stocks were all the rage.

Seeing those funds grow much faster than savings accounts kicked off an early entry into equities investment. When young, I was also already a saver and cheapskate, typically choosing to save my money. (That Members Only jacket is too pricey.

Let’s buy at the station with the cheapest gas on my standard routes. I’ll eat for free when I get home instead of buying a burger).

Who inspired you to excel in life? Who are your heroes?

I don’t really have any heroes. I do like to observe and learn from all sorts of people but no one really stands out.

For example, I’ve been reading about Stoicism lately as I move to the next phase of my life and am seeking direction on the best way to live life but Marcus Aurelius and Epictetus aren’t my heroes.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

I’m not a book reader but I read a lot of blogs. Many money blogs say the same thing in different ways but I still like reading them.

A few of my favorites include Big ERN’s Early Retirement Now, Morgan Housel’s posts at the Collaborative Fund (not so many these days), White Coat Investor, Ben Carlson’s A Wealth of Common Sense and of course the ESI millionaire interview series.

I also like reading comments in online communities such as Boglehead forums, Reddit Fatfire, and private real estate investing and high net worth communities. I’m looking forward to reading and contributing to MMM in the future as I now have much more free time.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

I’m a Scrooge McDuck. Writing checks to charity does not give me much pleasure.

Call me selfish. It’s probably true. So when I die with piles of money, I hope that my wife and son will live longer than me and find the pleasure in giving our excess money away to worthy causes.

Now that I’m retired, my interests should involve volunteering in the near future. I’ve been told by numerous folks that I’m pretty good at teaching and explaining things.

I plan to seek volunteer work, helping the underserved in a teaching/mentoring capacity. I hope this works out and if this becomes a passion mission, I’m sure monetary donations will follow as I can see joy in helping these causes.

I tried writing checks to food banks, churches, and other charities. It just doesn’t do it for me.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

We will likely leave a sizable sum to our kids. Our son will likely manage the special needs trust for our daughter that should be set up once we pass.

We’re targeting $2M for our daughter (today’s dollars) as this should be enough for her lifetime. Although he probably won’t need it, we’re targeting about the same for our son as well to be fair but he will get all that we have over the $2M we give our daughter since she won’t have the need or mental capability to know how to spend it herself.

In the event we piss away all our wealth, we will simply tell our son that the $2M for our daughter is from grandma (my mom), as this is the likely amount we will eventually inherit from her. In all likelihood, we will pass along more than this $4M figure unless at some point in our life, we want to start giving it away.

Only time will tell if I/we find a worthy cause. My son is a kind and practical kid so if he chooses to build a legacy or contribute it to worthy causes, that’s up to him.

At the moment, giving our kids any unused wealth gives me the greatest joy out of all the alternatives I currently see.

Since post-graduate degrees improved your and your wife’s earnings, perhaps your son can use the 529 funds for a master’s degree.

We’re certainly encouraging our son to do this. Given his current credits, if he is accepted to the Masters program at his current college, he could finish that as well under scholarship, hence still leaving a balance. We’d love to see him go for a PhD, but he doesn’t seem interested. But do 20 year olds really know what they want? Maybe he’ll come up with some pioneering idea that he’ll want to pursue in the future. I hinted at how Google’s founders followed that path as a possible model. That said, PhD students typically get RA stipends. There’s a slight chance he might go for an MBA like dad and may of his aunts and uncles. Going that route, the 529 money will definitely help.

I loved the honesty in this post. Thank you for sharing your life’s journey so far. I do hope you find that passion mission to help with making your retirement journey a fulfilling one.

Thanks for the kind words. I was concerned my cheap/selfish ways regarding charity might bring on the hate but it’s honestly how I feel. At work, I may not say or do the politically correct thing. Rather, I did what I thought was the right thing to do and slow-rolled the BS work asked of me. I think it may have contributed to my lack of advancement in my later career. I

This is one of the best ESI millionaire write-ups that has been published IMO. Very candid & introspective- especially about the trade offs ya have to make to get ahead – or not – in the hierarchical status-obsessed corporate jungle. But just the fact that the author has ESI’d his way to a third act shows that he & his wife have won the game. Enjoy that 3rd act! Make music, get fit, read great books and drink reasonably priced wine!

M24, you are too kind! Just trying to be helpful and honest. I’m certainly looking forward to our 3rd act. I love that I’m now fully in charge of my destiny.

Congratulations on being such a successful saver! Really enjoyed the read, thanks so much for sharing so openly. A lot of lessons here!

Many thanks! Looking forward to checking out MMM (I’m assuming you’re a member) now that I have lots more time and get a “free” membership. I suspect there’s lots for me to learn there (from you and others) and hopefully offer some meaningful insights as well.

Looking forward to seeing you on the forum. There is so much great material there. We all definitely learn on a regular basis. Scott

Thanks for sharing! I liked the comment, “Bring a positive attitude regardless of the situation or challenge at hand. I’m not the best at doing this but have found (sometimes the hard way) that negative or hopeless attitudes are usually frowned upon by management.”

Management’s playbook says you need to shuffle deck chairs on the Titanic with a positive attitude. It makes perfect sense. It keeps the troops focused, may give some poor lost soul some hope and has zero downside consequences vs panic, hopelessness and despair. Over time, I’ve learned to keep my mouth shut in these situations but couldn’t force myself to drink the Kool-Aid

Truly enjoyed the openness and honest write-up. Very practical strategy of balancing high-risk assets with a solid cash and bond buffer. Many nuggets of wisdom from discipline, savings and investment concepts. Thank you.

Thanks for your kind comment. Curiously, during my “free advisor” Fidelity consultation, the advisor asked why I was still being so aggressive with over 80% in equities. Most folks going into retirement would move to a more conservative portfolio to reduce risk and preserve their wealth, especially if they “won the game”. He asked if I was building a legacy or plan to contribute to charity with the likely excess. If that wasn’t important, then I should make the classic move to de-risk. It just didn’t feel right to me as I feel like I’m leaving money on the table. Even if I don’t use it, someone down the line will. I hope it will be for some charitable cause that could really use the money. I’d rather they get it than the greedy financial institutions and corporations (because I bought more conservative investments enabling them to extract the risk premium instead of me).

Surprised you don’t have the Robinhood Gold card. Would make your life much easier with P2. Either use the new card you’re working on or Gold card for straight 3%. EZ. Park 2k in SGOV to unlock 1k in free margin included with Robinhood gold. Margin can also be invested in SGOV. That covers most of the Robinhood gold annual fee.

A little more complicated but Bank of America premium rewards (park 100k in Merrill) will get you the best cash back ecosystem with BofA platinum honors. They also currently have a bonus % based sign up bonus on a couple of their cards that stacks.

Another thing to look at is cashing out Membership Rewards points to Schwab via the Schwab Platinum card. Good way to liquidate Business Platinum sign up bonuses. Ideally triple dip the Schwab card. Sign up mid/early December and cancel at 1yr+~20/30 days. This will give you 3 calendar years of cash out ability for only 1 annual fee. Amex refunds annual fee if you cancel within 30days of it posting. Main advantage here is Schwab cash out to Roth is not coded as Roth contribution, it’s coded as brokerage bonus. I am not your accountant though. Cash out is limited to 1mm points per calendar year though(11k) in the Schwab account at 1.1x transfer rate.

If P2 is already annoyed with your credit card shenanigans though I would simplify and just do RH gold card as backup card and whatever sign up bonus you’re currently working on.

Those cards are good (probably better) options than my Fidelity/Costco cards but I haven’t pulled the trigger as I’m more focused on card promotion awards as that’s where I see the bigger bang lies. Spending $2k – $4k on a card and collect 60k – 100k in points yield me more than an extra percent (or fractional percent) on purchases. So I’ll do a promo in my name (Say Venture X) then my wife, do a another card (Say Capital One) then my wife, etc. I keep rolling to more and more cards to collect promos. I deprecate or cancel the cards at the end of the first year. I got lots of unused cards in a locked drawer. I’m at the point where I’m scraping the bottom of the barrel with Delta points on AMEX (Delta has a number of flights out of our area, we’ve already done Alaska and Hawaiian). I don’t care about the temporary credit score hit as I don’t have any other need for my credit score and it never dips much below 800 anyways (Vantage Score) before it recovers. With so many open cards and unfrozen credit, I know I’m putting myself at risk so I should probably cut this out at some point, take up your idea and freeze my credit. At the pace I’m going, I’ll probably be out of good cards to apply for pretty soon and move on to that strategy and get a life.

Regarding Schwab, I’m looking out for the next good promo to flop over to them. Timing hasn’t worked out yet as to when my current brokerage promo expires and Schwab is offering something good. Once I flop to Schwab, I like the other card/point bennies you mention. Will likely get to that at some point.

Regarding parking money in SGOV, I absolutely do this. Most brokerage accounts offering promos have sweep accounts with 0% interest. So any money that isn’t in positions are in SGOV. I think that’s a very good practice to keep.

Great ideas! Thanks!

Love the writing style and honesty. As parents, sounds like you’re doing a good job. Enjoy the time with family and enjoy and hobbies you may find.

Thanks for the kind words. As parents, all we can do is the best that we can and love them, whoever they are and become. Gotta go hobby hunting now (well after I hit the gym and maybe a nap).

Very at-length interview, thanks for taking the time to answer so thoroughly and candidly. I know you’re not a book reader, but Die With Zero may be one exception (or maybe an audiobook now that you have more free time?) It also helped me with planning how to add more time in my life and not be so frugal. Looking at your spending and net worth, and doing that add just a few thousand per year in income for you, you should have no issues passing money down to your kids.

Thanks for the suggestion! I’m assembling a list of a few books to acquire. I’m looking at cruises and read that wifi can be sketchy (unless you buy the really expensive plans) so want to queue up some books to read. Die With Zero is a good one to try (I heard Perkins speak). I also want to read Psychology of Money (Morgan Housel) and Key’s to a Successful Retirement (Fritz Gilbert).

This is one of my favorite interviews and really appreciate your honesty. It sounds like you and your wife have done a great job navigating life and being able to save along the way. Thanks for your tips on switching brokerage firms, credit cards, etc. I will have to look into some of these. I too bought AAPL back in early 2000’s and it has been one of my best investments. If you can share some of the ETF funds you invest in for stocks, I would appreciate it.

Thanks for the kind reply. There are a number of good blogs that post the most recent promos and credit card bonus deals. You can Google for those as I find the best sources can vary depending on when they update their articles. I’ve been gravitating towards low cost broadly diversified ETFs. Of course, there’s VTI and VXUS. I also diversify by “sector” so that I have more flexibility to sell when I need cash (e.g. I get a choice to sell the whole market selling VTI/VXUS or sell a sector that I think is at a high price). Some key ones include VTWO for mid/small caps, IGV for tech SW (I’m bullish on SW and will pay the 0.41% fee to get that concentrated sector … but you do you), REET for international real estate, SPDR ETFs for sectors (XLF for financial, XLE for energy …), VNQ for domestic real estate and SGOV as cash holding. I favor low cost, broadly diversified ETFs. Not a big fan of bonds.