Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in March.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you?

I’m 51 years old and have been married for 22 years.

My spouse is 50 years old. We’ve known each other now for 32+ years.

Do you have kids?

We are the proud parents of 2 boys, ages 19 (soon to be 20!) and 17. My oldest is finishing his 2nd year at a public in-state university and will hopefully graduate early with a BS in Bio-Medical Engineering (Dec 2027).

He wants to go on to medical school and is studying for the MCATs. His first attempt taking the exam will be in May 2026…so fingers crossed!

My youngest is a high school junior and still trying to figure out what he wants to do. There’s a good chance he will do 2 years at a community college to get his basic courses out of the way and then transfer to a public university for a STEM degree.

My parents and siblings as well as my wife’s parents and siblings still all live within 30 mins of us. My wife’s parents are currently dealing with some health issues so we’ve been helping out with that.

What area of the country do you live in (and urban or rural)?

We still live in the same major urban city in Missouri, the Show Me State and in the same house from my original interview.

What was your original Millionaire Interview on ESI Money?

I am Millionaire Interview 348.

Is there anything else we should know about you?

That getting up the nerve to actually call it quits and retire is HARD, at least to be able to do it on my own terms. Even seeing the health issues that my in-laws are currently dealing with and knowing that my healthiest day is today, quitting work is a mental mind shift that I can’t seem to do.

I do want to retire but I just can’t seem to pull the rip cord! Behavioral Financial Psychology is real!

NET WORTH

What is your current net worth and how is that different than your original interview?

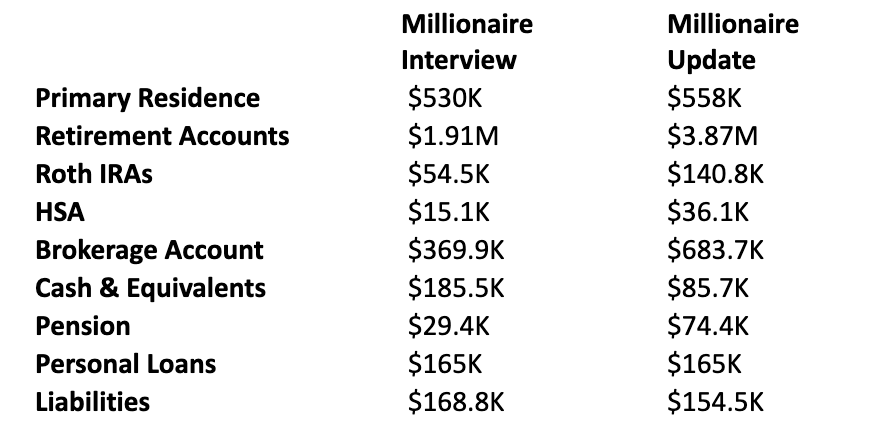

In my original Millionaire Interview, I wrote that at the end of July 2022, our current net worth minus our primary residence was $2.56M. If we add in our primary residence, based on Zillow’s estimate, it was $3.09M.

Fast forward to March 4th 2026 and our current net worth minus our primary residence is $4.21M. Adding in our primary residence, based on Zillow’s estimate, puts our NW at $4.77M.

The net worth numbers do not include cars, the 529 account or anything else of value.

What happened along the way to make these changes?

We’ve done nothing different since the original interview.

Aside from my wife and I continuing to work, the increase in NW is mostly attributed to the continuing bull market and re-investing the interest and dividends received.

What are you currently doing to maintain/grow your net worth?

Looking at the numbers from my original interview and comparing them to what they are now, most of the retirement accounts have grown due to the continuing bull market and re-investing the interest/dividends. Since I am still working, I add just enough to my current employer’s 401k plan to get the full company match but it’s not that much.

My spouse and I also have separate HDHP at work so we try to max out the HSA accounts. Roth IRAs, we both contribute if income limits allow for it.

As for the brokerage account, I put anything extra that we don’t spend into that account. My wife continues to work, so the pension amount is just the current value based on what’s she put into the account.

This will either convert to a monthly lifetime pension amount or we will be able to take that amount as a lump sum. This will all depend on how long she stays at her employer.

The liability is just our remaining mortgage on our primary residence which will just continue to slowly drop as we make our monthly mortgage payment.

We also have an $69K 529 account set up for the boys that we do not include in our asset total. We’ve started to draw down on this to pay for anything that scholarships don’t cover for our oldest.

EARN

What is your job?

I was working as a consultant in a business analyst position (fully remote since March 2020) when I originally did my millionaire interview but was laid off at the beginning of 2024. I knew the company was going through some tough times, and people on the bench were being let go.

At the time, I was safe since I was on an assignment. Lo and behold, my assignment ended at the end of 2023.

I still thought I was safe as I figured I would have at least a month or 2 of them trying to re-assign me but that would not be the case. Not even 2 weeks of being on the bench and updating my resume, I got an email for a meeting with a manager.

Now, I’ve never even talked to this guy before, so I kind of had a hunch this was it. When I got on the video call, there was someone else on the call as well and then I realized it was an HR person.

The manager said there was another round of layoffs and that I would be included in that round. No apologies given, no remorse, no emotions.

He was in and out of that meeting in less than 5 minutes, and I was left with the HR rep. She then goes through her spiel regarding cobra, PTO payout, and severance.

I’m kind of half-listening. She then says I’m getting 12 weeks of severance…UHHH HOLD ON??

I ask her to repeat that again. Here I’m thinking that I would get 2-4 weeks at most for severance.

Now I have a sh*t grin on my face. The call ends and I talk to my wife about it. She asks me if I was planning on looking for another job. I said I had no plans to do that.

I honestly thought that would be the catalyst for me to retire early. Apparently, that was not in the cards because not even a week into my early retirement, a buddy of mine reached out and asked if I was interested in doing quality assurance testing.

Next thing I know, 2 weeks after being laid off, I started a contract position at another company.

What is your annual income?

- My current annual income – $130K

- My wife’s current annual income – $65K

- Personal loans – $11K

- Pension – $1K

We also had about $151K in dividends/interest/capital gains last year from all our various accounts that automatically get re-invested.

How has this changed since your last interview?

My salary hasn’t really changed; in fact, looking at it now, it may have actually dropped if you take inflation into consideration. I believe I’m compensated fairly well for what I do, and I have no desire to move up in the corporate world.

If I don’t like something or how something is being handled, I have no problem speaking up. I’ve been told once or twice to settle down…

My wife got tenure and a promotion where she works since the millionaire interview, so that’s why she got the bump in pay.

The dividends/interest/capital gains increased from the millionaire interview because we don’t spend that money. It just gets reinvested and you know what happens when compounding takes over.

Have you added, grown, or lost any additional sources of income besides your career?

I don’t have any other sources of income other than what was mentioned above.

SAVE

What is your annual spending and how has it changed since your interview?

We still use Quicken to track our expenses. I finally broke down and paid for the Quicken software again so that we could get the latest updates and be able to download transactions from banks, credit cards and investments.

It has changed drastically since 2021. Back then, we spent a little over $67K for our family of 4.

For 2025, we spent a little of $101K. If I include some of the one-time expenses, that amount increases to $168K. This would include $42K (car), $22K (Down-payment Screen Room), and $3K (Permanent Lighting).

Our main categories of spending are:

- Food – 16.5K (Includes groceries & eating out)

- Insurance – $10K (Includes home, auto, life, medical, vision, umbrella)

- Mortgage – $8.6K (principal, interest)

- Property Taxes – $7.9K (for our primary residence)

- Household stuff – $1.1K (home maintenance, toiletries, HOA dues)

- Vacation – $17.5K

- Gifts – $7.6K

- Cell Phones – $2K

- Entertainment – $3.7K (internet and anything fun goes in here)

- Utilities – $5.9K (electric, gas, water, sewer, trash)

- Auto – $11.K (Gas, Maintenance, Repairs)

- Medical – $2K (Doctor co-pays, medicine, glasses/contacts)

- Clothing – $2.6K

What happened along the way to make these changes?

We still use the EveryDollar app for monthly budgeting. I think a lot of the increase in the various categories is due to things just costing more than they did in 2021.

I believe food cost increase is mostly due to that. I don’t think we are eating any better or worse than before.

Vacation is much higher because in the original interview, things were still recovering from the pandemic, so what we are spending now is probably better aligned with our spending for vacations going forward.

Gifts increased because we decided to do more for our families since we can (pick up the tab when we go out etc). Auto spending increased because we did maintenance on 2 of our older cars.

INVEST

What are your current investments and how have they changed over the years?

Our current investments have not changed over the years. We still hold mostly mutual funds in all our brokerage, HSA, and retirement accounts.

I have started to buy some VTI (the ETF equivalent for VTSAX).

Currently, we still save around 30% of our gross income. This is less than what we were doing back in 2021.

This includes 6% for my 401K to get full company match and my wife’s public school retirement account. We still try to fund Roth IRAs for each of us but the last 2 years have not been successful due to high income.

We also automatically invest $1000 into our brokerage account every two weeks. Anything that is left after budgeting our monthly expenses, goes into our emergency fund.

When the emergency fund gets too high, then we transfer a set amount into the brokerage. My aim is to keep 2-3 years in the emergency fund.

What happened along the way to make these changes?

We already have close to $4M in retirement accounts and more than likely that will just continue to increase due to compounding. Unless we can get some Roth conversions done, we will face some major RMDs when we turn 75.

The biggest change or challenge has been to put less in the 401K and more in the brokerage account and emergency fund, so that when we end up doing Roth conversions, I will have money to pay the taxes on that conversion as well as money to live on as a bridge until we turn 59.5.

MISCELLANEOUS

What other financial challenges or opportunities have you faced since your last interview?

My financial challenges are knowing when to retire so that I can do Roth conversions and do what I can to minimize the taxes that I have to pay in the future.

But as a wise man once said, if those are the financial challenges that you face, you’ve essentially won the game!

Overall, what’s better and what’s worse since your last interview?

My work-life balance is still great! It’s great to see the net worth continue to grow but what makes it ‘bad’ is that I still can’t get myself to quit/retire.

I don’t get stressed out when Sunday night rolls around, knowing I have to work the next day. Work’s been pretty easy but I do get frustrated when I’m working with some of the stuff I get to see and deal with and at times, it shows, especially in meetings.

This makes me unmotivated but then I take a deep breath and remember that I’m the one that ‘wants’ to be here and that I don’t need to be if I don’t want to. I have to remember to let things go and not give a crap.

What are your plans for the future?

In my millionaire interview, I said we might purchase a lake house and use it for our home base. We have decided against this, at least that is our current thinking.

We just figure that if we want to spend some time at a lake, we can always rent. We still like the idea of visiting all the national parks. That has been on our bucket list.

I know I’ll retire sooner or later, hopefully sooner rather than later. But in the meantime, I’ll continue to work and do what I can to ensure my kids don’t start life in a huge hole.

Given that you have a bit more wisdom and experience, what advice do you have these days for ESI Money readers?

My advice is roughly the same from my millionaire interview. I’ve included it here again.

Get a good paying job and learn to live within your means, below your means is even better. Whatever money you save, invest for the long term. That is the key!

Without investing the money you save, rarely will you ever become wealthy. The easiest way, with minimal effort, is to invest in a total stock index fund and make it automatic.

Invest when the market is up, invest when the market is down. Slow and steady wins the race but remember to enjoy your life along the way as well.

It’s ok to enjoy your good fortune, just don’t go crazy!

The only thing I would add is to make sure that you are investing in a 401K, Roth IRA, and a brokerage account. ALL THREE!!

Don’t think that just because you max out your retirement account, you are set for life. You want to invest money in a brokerage account as well.

This is the account that will bridge you from the time you retire until you can easily access your retirement accounts, especially if your goal is to retire early or just want to get out from the daily 9 to 5 and do your own thing.

Great post and good thoughts on contributions to all three: 401k, Roth and brokerage. I was late to the brokerage game and wish I had a do-over on 401k v Roth. Converting now and hope to get most out of 401k and into Roth by 60.

When I was younger, I didn’t even give Roths a 2nd thought. I just figured everything is in the 401k, why stop…I was naive.

You mentioned being above the income limit for Roth IRA contributions. If so you could consider putting $8,600 each (since you are over 50) into Roth IRAs via the “backdoor Roth” method. It’s a tiny bit of a hassle but will have less tax drag compared to your brokerage account.

Thanks for the response. I’ve looked into doing this backdoor Roth a little bit but need to do more research on it.

At 51 and some college tuition ahead – I doubt I would retire with $4M – and I am very pro early retirement. I would work 2-3 more years and see how your day doe see are looking. I was somewhat naive in my thinking that child related expenses end around age 22 – they don’t.

Thanks for the response! I know child-related expenses don’t stop. I look forward to helping my kids beyond age 22 if I’m able to do so! I’d rather give with warm hands than cold ones.

I’m just a few years older than you (54) and retired a year ago. I highly recommend it! As long as you’re enjoying what you do, have at it …. just knowing you can walk at any time reduces the stress immensely. And you can just laugh at the chaos swirling around.

Thanks for the update.

Thanks for the comment! Just knowing that I can walk away is awesome. No stress!!

Shout out from the Lake! Thanks for the update!

Thanks DT!

At this point, your money makes more money than you do. You have all your expenses and reports dialed in, how do you measure the amount or joy/sense of accomplishment/pride you and your wife get from work besides “remembering not to give a crap” 🙂 ? What will you do when you do retire?

What will I do? I’ve been trying to figure that out for 50+ years!!! haha

Lots of volunteer work.

Thanks for sharing the update! I liked your comment, “I know I’ll retire sooner or later, hopefully sooner rather than later. But in the meantime, I’ll continue to work and do what I can to ensure my kids don’t start life in a huge hole.” Proverbs 13:22 speak of a good man leaving an inheritance to his children and their children. I believe this speaks to examples of godly spiritual, lifestyle, and financial beliefs and practices that one provides while they are living that also overflows in the children’s lives once the parents are gone.

One of a few things that finally convinced me to retire early…

A coworker, Engineering Mgr, came early into work with a severe headache. Before the first meeting of the day he died of a brain aneurysm. He was a nice guy, left behind a wife and two kids. It hit me hard.

At the next round of layoffs, I recalculated our numbers. I volunteered for the severance package and just crossed the threshold to fully vest a modest pension.

Tomorrow is never guaranteed.