Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in August.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I’m 43 (for 8 more days). My husband is 45.

We’ve been together since 1999 and we got married 15 years ago in 2008.

Do you have kids/family (if so, how old are they)?

We have two daughters, ages 14 and 12.

Our older daughter is an aspiring artist. Her skills are impressive and I’m hopeful she can find a successful career that aligns with her interests.

Our younger daughter is outwardly giggles and goofiness, but inwardly contemplative and compassionate. She has a great work ethic that we think will serve her well.

Both girls daydream about the future and of course we think the world is their oyster.

What area of the country do you live in (and urban or rural)?

We live in a small town in the Philadelphia, Pennsylvania suburbs.

It’s the cutest square mile of a community with a bustling main street, and it happens to be a tiny bit of a tourist destination.

What is your current net worth?

At the time of this interview, our net worth is $2.23M.

We don’t usually include our estimated home equity in this number, but I understand most people do, so I included it here. The estimated value is from Zillow. I’m not sure what that means to people, but it’s just the easiest source. I don’t think it is out of line based on recent sales in our neighborhood.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

- My Pre-tax Retirement Savings: $638K

- Husband’s Pre-tax Retirement Savings: $390K

- My After-tax Retirement Savings: $322K

- Husband’s After-tax Retirement Savings: $146K

- Joint Taxable Brokerage: $309K

- Kids’ 529s: $145K

- Kids’ Taxable Brokerage: $12K

- Cash: $88K. Credit Card Balances: ($33K) All at 0% interest. I dabble in the points and miles hobby, so we happen to have multiple cards running promotional interest rates. With cash being worth something these days, we’re doing a little interest rate arbitrage. Net Cash $55K

- Estimated Home Value: $609K. Remaining Mortgage: $(391K), at a sweet 2.75% interest. Net Home Equity: $218K

EARN

What is your job?

I currently work for a global non-profit as a Finance Manager.

My husband works at a nearby state university as a Research Assistant. His position is grant funded and we are kind of surprised they keep having the money to pay him.

What is your annual income?

I earn about $145K, and my husband earns $45K, so our combined household income from employment is $190K.

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

I would categorize my income story to date into 3 “Eras.” (Any Swifties out there?! Our teenage daughter is obsessed. I’m a casual fan by proxy.)

Era 1: 2003-2007, a time of quick and substantial salary increases, $36K to $80K in 5 years

My first “real” job was a staff accountant for a regional public accounting firm earning $36K. While in that role, I sat for the CPA exam and passed all four sections on my first try. I stayed in public accounting for just a little over a year before making the switch to private accounting for a better work-life balance.

I was happy to find that the CPA credential was highly desired by employers outside of public accounting. It is a challenging test to pass. So I did a lot of job hopping a lot pre-kids. 5 employers in 5 years, each one willing to pay more than the last, and by 2007 I was earning $80K, all in a variety of accounting positions.

Era 2: 2008-2019, a hiatus and a time of slight stagnation, $80K to $98K in 12 years

We got married in January 2008, then enjoyed our honeymoon adventure for the next 4 weeks.

Days after we returned home, we found out I was pregnant! We already lived simply and frugally, so we spent the next 9 months living on his salary and saved mine. We always thought he would be the SAHP, but I disliked my job at the time, and he was enjoying his.

I left my job when my maternity leave was over to be a SAHM. It didn’t make financial sense, since he was making $27K managing a small vegetable farm and I was making $80K. But we had savings to fall back on. I had come into the marriage with a NW of around $150K and his NW added another $23K.

Ultimately, we didn’t need to dip into any savings. I was very proud of our finances that year. We decided to use our excess cash to pay off his student loans (they were “only” 10K) that year. We also took advantage of a low-income year and corresponding lower tax rate to convert my pre-tax 401K to a Roth IRA.

When our daughter turned one, my work break was done. My husband became a SAHD, and I returned to my career.

The job market was terrible in 2009 when I returned to work, but I wasn’t stressed about it. I took a contractor position for 3-4 months while I searched for a permanent role. I ended up with a salary of $80K in early 2010, got small raises in the next few years, breaking into $90K in early 2014. But by then I was not happy with my job. The environment wasn’t great, work-life balance didn’t exist, and I didn’t like what I was doing. Also, I had asked for a raise, was denied, and was mildly offended about it. My empathetic and comedic husband got me a cake that said “Nice Try!” on it, though, so at least some good food came of it.

Ultimately, the rebuffed raise request left me feeling negatively toward my employer and turned into a catalyst to move on. I jumped ship in 2014, taking a pay cut to $85K for a senior accounting job in what looked like a much healthier environment. (Their offer was $80K, I asked for $85K, they said okay. That was my first time negotiating a salary. It was so easy; I should have asked for more.)

Annual 3% raises followed, and by 2019, my salary was $98K. But I was growing weary of the same work after 5 years. As if they’d read my mind, my supervisors put me on a special project in 2019. It was a great surprise, engaging, and just the change I needed.

Era 3: ~2020-2023, a time of career growth, $98K to $145K in 4 years

When the project was about to wrap in late 2019, my supervisor surprised me again, offering me a newly created role for 2020. It was a great opportunity and I made the switch to the new role in late 2019, bumping my salary to $110K.

In January 2020, the standard 3% increase came in on top of the recent raise, bringing me to $113K. The work was new territory for me, so my employer onboarded an externally hired manager to show me the ropes. He was probably one of my best bosses ever.

In January 2021, another 3% raise was handed out, making my salary $117K. Then my beloved boss was whisked away by someone in his network to a director role in late 2021. I was nervous about getting a new boss after having such an exceptional one, but he convinced me I was ready for the manager role. I feigned confidence and told his boss I was ready for it. Then I waited.

My annual raise (4% this time!) came at the beginning of January 2022. My salary was now $121K. And I waited a little more. By the end of January 2022, I had officially landed the manager role, and my salary was bumped to the $135K I requested. (Too easy, I should have asked for more! Again!)

In January 2023, I got a 4.5% raise to $141K. Two weeks later, I was notified that due to a “compensation data review” I was getting bumped to $145K. I guess they decided I was underpaid. I have looked at salary surveys and I do believe I’m well compensated given my limited experience. Whatever their reasoning, I’m grateful and I will take what I can get.

Not my Eras: He earns income, too!

My husband’s earnings, when he has been working full time, have ranged from $18K-$45K over the years. He has a degree in psychology and I think is happiest when he is creating, but the stars haven’t aligned for him in terms of work interest and opportunity to produce a salary like mine. Which is fine, I earn enough for our family, and he contributes in many non-monetary ways to support our goals.

He’s earning his highest salary currently, in his University Era, which started in 2017. One of the biggest eras in his life (and our family’s) has been his time working at a local coffee shop from 2013-2017. He was still our SAHP at the time, and he thought it would be cool to work 5-7 am, then come back home to be with the kids when I left for work. He added hours as the kids got older and spent more time in school. That really grew into a career in coffee and a welcome entanglement into a small community of coworkers. He is still in touch with many of them; I can’t say the same for most of my coworkers.

Prior to the Coffee Era was the Agriculture Era. He took opportunities that worked around our family’s schedule and aligned with his prior experience in agriculture. Packing CSA shares at a local veggie producer with the kids in tow. Running a small beekeeping business. Being a cowboy. (For real, rounding up Angus cattle on a pasture, just like in movies, but on a bicycle instead of horse.)

Prior to our marriage, he worked a lot of various jobs. He was a zookeeper, prep cook, substitute teacher, bookseller, music store manager.

What tips do you have for others who want to grow their career-related income?

Be proactive with your job and stay engaged! You’ll enjoy the work more if you do, and you’ll do a better job if you enjoy the work.

Recognize your worth and your needs in a role and move on if there are gaps in compensation or other aspects of the job.

What’s your work-life balance look like?

I think it’s pretty good! My husband will tell you I work too hard these days, but I have a lot of flexibility since I work 100% remotely.

He has less flexibility with his job and needs to be on site to do physical work. But he can manage his hours around family needs most of the time.

We are both lucky.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

Maybe $5K in dividend income annually. As previously mentioned, I do dabble in the points and miles hobby, and it offsets some of our travel expenses, but I’m not sure if I should report on what I earn or use here. There are people that really go nuts with this hobby. I am less invested and do the hobby at a slower pace than most.

My parents, immigrants to the US, have done well for themselves, and they are generous with cash gifts. It amounts to around $6K annually. I think my dad feels an obligation to take care of his children very much still, even though we are all adults. It’s sweet. I always tell them upon receipt of such gifts that they are never needed and always appreciated.

SAVE

What is your annual spending?

I think a fair number for annual spending now would be $80K.

In 2022, our total spending was $102K, and that includes $26K for a new roof, new gutters, and a deposit on a solar array we had installed in 2023.

So if you exclude that, we spent $76K. Perhaps it’s foolish for me to make these exclusions. We finished the solar project in 2023 ($23K).

And we also need to replace one of our two vehicles this year. And we want to build a deck. (The quotes are outrageous. We need to do it ourselves.)

The point being it seems like something always comes up, which is why we are still working.

Our spending used to be much lower before home ownership and recent inflation. Our annual spending in the 5 years prior to the home purchase was around $57K annually. We bought our house in July 2021. PITI is about $10K more each year versus our old rent, which was a steal.

I worry about what the next thing is that might change our spending. In 10 years, will I say, “our spending was much lower before event XYZ. We used to only spend $80K a year.”? This is one reason I continue to work and save, despite declaring a retirement date and having it come and go, time and time again.

What are the main categories (expenses) this spending breaks into?

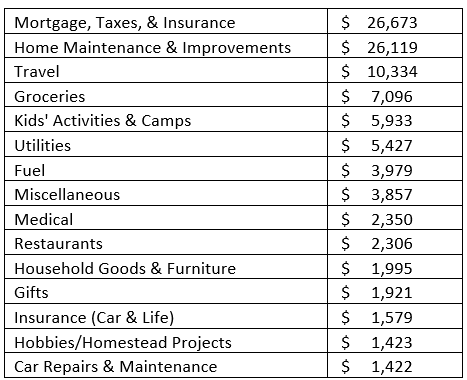

In YNAB we have 30+ spending categories, and I’ve cut it down to 15 in an attempt to simplify the view.

Here is our actual 2022 spending:

Do you have a budget? If so, how do you implement it?

Yes, we use YNAB Classic. I love YNAB, but I don’t want to switch to the SaaS version for multiple reasons.

My husband does his part by entering transactions, and I handle all the rest.

I’ll have to find a replacement, as it is now unsupported and likely will not work forever. If anyone has any suggestions, I’m listening!

I also wonder if I’ll find myself in a position where we no longer feel the need to budget. But one step at a time.

What percentage of your gross income do you save and how has that changed over time?

It’s around 50% these days. It’s always been close to that, which is hard for me to wrap my head around given my recent salary increases. I wonder how we are spending so much.

Using YNAB, the answers are right there, but seeing them still doesn’t make it make sense! I guess the good thing is we are still saving more than ever.

What’s your best tip for saving (accumulating) money?

Live well below your means. Try hard not to spend your raises. In years past, I would have said “just don’t spend your raises.” But now we are in a position where our lifestyle changed due to a home purchase, and we are spending my raises, at least some of them. I really thought owning versus renting wouldn’t have much of an impact beyond PITI, and I knew I had to account for maintenance costs, but I didn’t really predict the timing of it very well.

For the most part, we try to be value-ists. I know that’s not really a word, but we really consider if whatever $ we’re parting with is providing the value we personally want. Also, automate and simplify as much as possible!

What’s your best tip for spending less money?

My best tip for spending less money is to move it out of your view before you can even think of spending it, and only spend it if it brings you true value. Moving it out of your view is easy to do if you automate it.

Know what you value and don’t be fooled into thinking you value what other people value.

I haven’t read it (because our library doesn’t have it), but there’s a book by Luke Burgis called Wanting: The Power of Mimetic Desire in Everyday Life. The concept is that beyond biological needs, we only want things because we see that other people want them. Just be aware of what your true desires are and behave accordingly. I think most people reading this will find that they really don’t want much.

What is your favorite thing to spend money on/your secret splurge?

Travel, for sure. We love to explore and we love to have fun. We use points and miles to mitigate our travel costs. Still, last year we spent over $10K on travel. That got us a couple of overnight city getaways, a ski weekend, a couple of weekend getaways to a regional amusement park, 5 days at the beach, 9 days at Disney, and a week visiting family in California.

We loved Turks and Caicos when the kids were younger. We thought Disney would be a one and done deal, but 2022 was our 4th trip. Yellowstone and Grand Teton parks were amazing. The kids really enjoyed London and Paris. We just spent 3 weeks in Hawaii, visiting the Big Island, Maui, and Oahu. (We left Maui about a week before the devastating fires occurred.)

Looking forward to more travel with our family as we close in on the final years of us parents declaring what happens in during our children’s summertime lives.

INVEST

What is your investment philosophy/plan?

Keep it simple with low-cost index investing.

Be aggressive with high risk tolerance in your early years. IDK that we are still in our early years, but our portfolio is still very aggressive at about 93% equities.

Invest as much as you can as soon as you can. As they say, time in the market beats timing the market.

We just like to make sure money goes in one direction, into investments. We trust time will take care of the rest.

What has been your best investment?

I’m going to go with a figurative answer here and say education. I don’t mean my bachelor’s degree, I mean my continued efforts investing time to learn.

Continuing my informal education, mostly through a lot of reading, has been a huge benefit to my life, financially and otherwise.

I didn’t always make the smartest financial choices. At my first job, I only contributed a small percentage (recommended by the HR lady) to my 401K. I was living at home at the time and did not need much of my salary. At one of my early jobs, I didn’t contribute to a 401K simply because there was no match. I should have contributed something! Also, in another one of my early jobs, I decided to invest in a handful of funds that had the best returns in the last 5 years.

Obviously past performance is not a reflection of future performance, so that wasn’t the best idea. Our financial behaviors have changed as a direct result of learning.

What has been your worst investment?

Peerstreet Pocket.

I had long admired those in the financial independence community that have gotten there with real estate investing, but that hasn’t been our path. Eager to find a palatable substitute, I turned to crowdfunded real estate investing. Peerstreet only allowed accredited investors, and I will admit it made me feel special that we qualified. I invested in only a couple of Peerstreet loans before deciding I wasn’t comfortable with it. So I stopped and pulled our money out. The account sat dormant for a couple years.

Then, when interest rates were rising in late 2022, I decided to move a small amount of cash from our savings account to Peerstreet Pocket, which was yielding maybe 1% more than the savings account. It touted monthly liquidity, but that came to a sudden halt in January 2023. Peerstreet filed for bankruptcy this Summer. I have about $900 tied up with them and I’m not sure I’m going to get it back. I’m not holding my breath, and if it’s gone, that’s too bad and I’ll feel stupid.

But in the grand scheme of things, $900 obviously will not break us. I’m glad it wasn’t more. I have heard of folks that had 6 figures tied up in Peerstreet Pocket. For me it’s just an expensive lesson, not a disaster. Don’t invest in something you don’t completely understand!

What’s been your overall return?

We don’t have great records for this, but we estimate returns have been roughly 10% annually.

We don’t pay that much attention to this because it is largely out of my control. We are not chasing returns, we do our part to earn, save, and invest, and then we let the market do its part.

How often do you monitor/review your portfolio?

I monitor balances sporadically. Sometimes it will be daily for a month straight, sometimes I will ignore it for a week or so. I do look at least monthly. I inform my husband of any notable changes, it’s not on his radar to look at it regularly.

There isn’t much upkeep to do with such a simple approach. I am guilty of not rebalancing annually, but again, there isn’t much to do since our portfolio is very equity heavy.

Also, I typically just adjust contributions to correct ratios. We have sat down with a financial advisor or two in the past, but we’ve ultimately decided we didn’t need their services. I really believe that nobody will take care better care of our money than we will.

NET WORTH

How did you accumulate your net worth?

Our earnings have been good, but not great. I can see how families that earn similarly to ours end up living paycheck to paycheck. I wouldn’t even say we invested particularly well, since heavy equity indexing is such a run of the mill strategy in the FIRE community.

The key to our net worth growth has mostly been aggressive savings.

We did recently inherit $60K from my MIL, which is certainly nothing to sneeze at, but in terms of our current net worth, it is not a game-changing amount. We still appreciate it very much.

My parents are financially secure and probably have more money than they will spend in their lives. This means they will likely leave me and my three siblings an inheritance. I have a differently abled sibling, and I will absolutely take care of the family I grew up with before we pad our accounts with any of those funds.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

This is not a hard choice for me. Our strength has been saving, hands down.

Our earnings are fine but not extraordinary.

Our investment choices are typical for those in the FIRE movement.

Nothing special with the E and the I, so it’s gotta be the S.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

I think I can say we have not have any road bumps. It’s been smooth sailing for the most part.

Not to say life has always been easy, there are always challenges. But nothing major has hindered our path.

What are you currently doing to maintain/grow your net worth?

Not touching those investments, shoveling more savings in!

After our home purchase, I decided we didn’t need such a large emergency fund and kept cash balances low. So when we wanted cash for needed home maintenance in mid-2022, we didn’t have much available. I know timing the market is a no-no, but that was not a great time to be selling, and I really didn’t want to do it.

Ultimately, we didn’t touch our investments. Between a short-term loan from a family member (mutually beneficial!) and a 0% intro rate on a credit card, we were able to handle the expense without cashing out any of our invested assets. It would have been okay if we had to sell, but I’m happy we were able to keep money flowing in one direction.

Do you have a target net worth you are trying to attain?

This is tough and probably the biggest uncertainty in our finances.

When I started this journey, I thought we would be able to retire with $1.2M. That became $1.4M, then $1.8, then $2.0M. And it keeps changing. Right now it is $2.5M.

I think we are in our 1st year of one more year. But we might be in our 3rd year of one more year. I do fear that once we get to $2.5M, I’ll want $3.0, and it’ll just never stop.

How old were you when you made your first million and have you had any significant behavior shifts since then?

In 2018, our NW reached $1M. I was 38, and my husband was 40. It was like a non-event.

I was watching it closely, waiting to see it cross over that threshold. And when it finally happened, it was not super exciting. I think most people will agree it doesn’t feel any different. Given that we understand what $1M is worth from a retirement standpoint, our behavior did not change.

Between August 2018 and March 2020, market swings took us out of and back into millionaire status 3 times. We’ve now seen this happen twice with our $2M since reaching that milestone

I feel there have been some behavior and/or perspective shifts since our home purchase. It was a perfect storm of parting with the biggest check of our lives, the sudden increase in inflation, and a raise and promotion. I felt like money was just flying out of our hands and I couldn’t control it, and even if I could it didn’t even matter that much.

I part with money more easily these days than I used to. In some ways it is good, and in some ways it is bad. I’m not sure what to make of it. It’s a relatively new phenomenon still. Perhaps this has been a road bump on the way to $2.0M, or will be one on our path to the next milestone.

What personal habits and/or traits have you developed that have made you successful at growing your net worth?

I’m always trying to be better and do better. I’m not anything special; I’m an average person, but there’s always room for improvement. We are all works in progress.

I view myself as a lifelong learner, and I try to read a lot. I’m on track or maybe a wee bit behind on my goal of reading 52 books this year. If I can get at least one useful takeaway from a book, that’s great!

I read Never Split the Difference by Chris Voss. It’s about negotiating techniques. This was maybe a couple years before we bought our first house. I ended up using techniques from that book to negotiate our mortgage interest rate down from what our lender originally offered. The result is 10K less in interest over the life of the loan. It was a lot of back and forth negotiation via text messages. I was getting push back, but I pressed on, using the tactics I had read about. In the end, I got what I asked for, and then asked for more, and got that, too! I was so proud.

This is not a trait or habit I developed, but I must acknowledge the role of luck in my success. I was privileged to be born to a solidly upper middle-class family in a well-developed country. I had nothing to do with the fact that I had access to a great public education and had a family situation that allowed me to pursue almost anything I wanted. That landed in my lap. I’ve had so much privilege in my life.

On top of that, I am just strangely lucky. We had amazing luck buying our house despite a ridiculously competitive market in 2021. Even when it seems like unlucky things happen, it almost always turns out to be good for me when all is said and done.

What money mistakes have you made along the way that others can learn from?

I would have maxed out my 401K at some of those early jobs. I worked for 5 years before I started maxing out my 401Ks.

And, referencing the Peer Street debacle described earlier, I would have avoided that, of course.

Look to see what others are doing for ideas, ensure you are doing the best for yourself, but consider strongly before you stray from your plans and try to copy someone else’s path.

I read about people using low-rate margin loans strategically, then opened an account with Interactive Brokers thinking we were going to take advantage of these loans. I moved our assets to IB, but never pulled the trigger on the loans, which turned out to be a good thing with the rise of interest rates. I moved the assets back to my preferred custodian, but I had previously completely closed out that account, so it’s an annoyance now that I have a new account number and cannot view the account history of the previous account very easily. I also have some administrative work to do still to close out the interactive broker accounts.

I basically wasted time trying to copy someone else’s actions. In fact, the Peer Street debacle was also a product of trying to emulate what someone else was doing.

What advice do you have for ESI Money readers on how to become wealthy?

Be content with what you have. Don’t buy junk. There’s this hilarious tweet from writer Paige Kellerman “Not everyone realizes this, but if you clean the pile of receipts out of your purse and stack them together, it makes a teeny tiny book about why you’re broke.” Don’t let that teeny tiny book exist!

Keep track of your savings and spending. You don’t need to have a detailed budget, but you need some data or feedback that tells you whether your behaviors are supporting the results you want.

Pick your spouse wisely. I know it appears that I’m the heavy lifter when it comes to my family’s finances. But our life as we know it is only possible because we chose one another. We share it all and we like it that way.

I know this will be a divisive statement, but if you are married or otherwise in a lifelong commitment, just put everything together! I know some couples that keep finances separate, and honestly it seems so complicated! I think it helps that we both feel an obligation to be good stewards of our shared financial resources. If I waste a ton of money, I’m not just jeopardizing my financial future, it will impact our family.

Having shared goals and a shared vision will go a long way in shaping behavior to facilitate growing wealth.

FUTURE

What are your plans for the future regarding lifestyle?

We definitely want to retire early, and that’s been a long standing theme in our financial goals, but the detailed timing of when is tricky.

I wouldn’t mind if my husband left his job in a year when he’s 46. His job provides minimal income and I think he and our family would be better served by having time to tend to things at home, including himself. Self-care is hard to prioritize when you work full time. I’m better at making time for this, even if it limited to not-daily-but-somewhat-frequent meditation. He thinks we should both retire next year, or at least thinks that he shouldn’t retire until I do.

I’m probably not going to stop working until our NW hits at least $2.5M, and I hope this happens before I’m 46, just because 45 seems like a nice number to call it quits. I am open to a reduced workload, maybe even before we hit $2.5M. I worry that part time work will just mean squeezing a full-time job into a slightly abbreviated work week, while taking a 50% pay cut. Nobody wants that.

What might be more viable is moving to contract or consulting work. Full time for 6 months while the kids are in school, and then taking a 6 month break. I think there are opportunities like this in my field, but I’ve yet to delve into them.

What are your retirement plans?

When we do retire, I expect we will draw down around $80K annually for expenses, but I want to be able to stretch that to $100K. Planning for spending of $100K and a corresponding NW of at least $2.5K puts us solidly in fatFIRE territory. I almost can’t believe it, because I feel like we live so simply, except maybe the vacations.

When we finally retire, I imagine we will have amazing self-care and healthy habits, like going to bed at a reasonable hour and meditating and exercising every day. Our health and happiness will be our priority.

As it is now, working full-time is a big drain on our time. I know that technically there are still more personal hours than working hours, but it doesn’t really feel like it. Also, household management will be a snap since we’ll have time to make sure everything is running smoothly. We’ll eat splendidly because we will have time to follow those ridiculously specific Cook’s Illustrated recipes. We will have time for leisurely and active pursuits. We’ll have time to act and advocate for changes in our community, locally and globally, that we want to see.

Then, when the girls are away at college, we will have the flexibility to travel in off-peak and shoulder seasons!

We’ll love Mondays because everyone that isn’t retired will have to be back at work, and the world will be at our beck and call. Or is it that we will be at the world’s beck and call?! In other words, our lives will be perfect!

Of course, I know perfection cannot be achieved. But without the stress of work and the additional free time we will have, I know we will be happier. I’m not sure what retirement truly holds, but I imagine we will love it.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

I am worried that the days will waste away and I won’t get enough done, but that is not any different from how I feel now.

We also need to investigate health insurance, but I know there are decent options out there for us. I’ve priced them out before, but things change, so I’ll revisit closer to when we will be retiring. We haven’t really planned fully around this need, which is one of the reasons we wait one more year.

We also worry about running out of money. I would like to read Die with Zero, but I suspect they don’t mean that you inadvertently run out of money at death.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

Like most people, I was never formally taught anything about finances, but my parents had it mostly together when it came to this stuff, so I learned from them.

I’ve always had a saver’s mindset and been interested in finances.

I can pinpoint a “click” moment in my youth, though! My mom explained investing and compounding to me when I was a teen, showing me a graph that illustrated how starting investing even a small amount early on would yield big results in time. At the time, I wasn’t thinking about retiring early. I was just wowed by the idea you could have a million dollars at 60 by saving a small amount annually starting at 20.

In my young adulthood, before I had heard the term FIRE, I read “Your Money or Your Life” https://esimoney.com/the-best-personal-finance-books-of-all-time-your-money-or-your-life/ by Vicki Robin and Joe Dominguez. A lot of the investing advice is now outdated, but the concept of financial independence made an impression on me.

Who inspired you to excel in life? Who are your heroes?

My parents.

I’m wowed by the audacity and risk tolerance it takes to move halfway around the world to tackle life in a new country. My dad had some family that had moved to the US, so he wasn’t going at it totally alone, but I still am inspired by their paths.

Both of my parents are college educated, but an overseas degree isn’t the same as a US one, or it wasn’t when they arrived in the US, at least.

My dad’s first job in the US was waiting tables. He had a degree in civil engineering and he was a waiter! My mom has a degree in nursing and was able to come to the US because there was a shortage of nurses here, so she was able to jump into her career immediately.

They dreamed big and worked hard for me and my three siblings, and I’ll be forever grateful for that.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

- Your Money or Your Life by Vicki Robin and Joe Dominguez. A classic introduction to the truth- you trade your life for money. How much of that do you want to or need?

- The Millionaire Next Door by Thomas Stanley. The basics. Millionaires are regular people, it’s not hard to get there by living below your means.

- The Psychology of Money by Morgan Housel. This is a newer favorite. It reinforces a lot of what I’ve learned over the years. And it makes an attempt to hammer in ideas I’m still trying to accept, like what is enough.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

We do give to charity and we have a small budget for it. It is rolled into the miscellaneous category in my answer about spending. But major philanthropists we are not. Yet.

We are interested in starting a donor advised fund, but before we do that, we want to be comfortable that we have enough. I am confident we will get there, it’s just a matter of time.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

We would be happy to leave an inheritance to our daughters!

We hope that when that time comes, they will have already established self-sufficiency and their own savings. We want any inheritance to be icing on the cake for them, not something they are relying on.

Our collective futures seems bright and we’re excited to see with it brings!

Nice interview!

Thanks Philip!

Try Everydollar.com. It’s a great budgeting app. Super easy to use.

Thanks Amy! I have looked into it before and it seemed promising, but I need it to have the balance sheet side of things, which it lacks. It’s all income and expense, but no assets or liabilities. (My accounting background is at play here, clearly.) The reality is I uncover transactions that were forgotten or otherwise need correction when I do the account reconciliations in YNAB, plus I use it to track a lot of credit cards for my points and miles hobby. Without that, I can’t be certain that my data has been tested for occurrence, completeness, or accuracy. (And there’s my audit background making an appearance!)

I also wonder if I will feel comfortable enough to let go of data perfection here at some point, in which case everydollar could be a decent solution. I’d have to move credit card tracking elsewhere, but it could be done. Maybe one day even stop budgeting/tracking all together. (Gasp!)

This interview was extremely well written and very enjoyable to read. The teamwork between you and your husband sounds extraordinary in terms of equally valuing both financial and non-financial contributions to the family. Great Job!

Thanks Scott, I appreciate the comment! I’ve always liked writing and this interview was a fun exercise in deciding what I wanted to convey and how I wanted to say it.

We do pretty well with the partnership around here, but of course there’s always room for improvement!

Wonderful interview. I love how you are the primary breadwinner and talk so fondly of your spouse, suggesting he retire before you do to take care of himself. You’ve given motivation that even with a household income under $200k and raising two children, you can become a millionaire well before retirement age! Well done, look forward to the update.

Thanks! Also, he is a couple years older than me, so he’s been working longer than I have, which supports him retiring sooner, right? That’s what I tell him, at least.

And it isn’t really spelled out, but it is only the last 5-6 years, since my husband took the university job, that our combined income has been anywhere close to that ($140K-$190K). Before 2017, we were essentially a one income family with my salary averaging $85K. And one of those years I was a SAHM and we only earned $27K! We hit our first million in 2018, so most of it done with one (relatively) modest income.

It’s amazing how much a little simple living can do for your future!

Excellent interview – great storytelling and love the positivity that comes through it. Congrats on your success thus far, and thank you for sharing!

Thank you! As an avid reader, I enjoy a great story, so this comment made me smile!

I do lean towards positivity; life is just nicer that way. I also try to balance that with being realistic. We can’t be positive and happy all the time. Positivity has its bounds, and sometimes in the most dire circumstances, can be really hard to find.

Love your story! Many blessings as you forge ahead.

Aw, thanks, I love our story, too! Upward and onward!

Loved this interview. The teamwork and “equal yoking” (though contributing in different ways) between wife and husband is inspiring. Saving is an underrated skill! And it can obviously work miracles.

I also really appreciated that this woman was so clear that her privileged upbringing- upper middle-class family, solid public education, parents who taught her well and were good examples – is a big part of her success, as is pure luck. So many seem to believe it was they and they alone who achieved success on their own. Hard work often needs a lift to lead to this kind of achievement. Kudos to this remarkable woman, and best wishes on reaching your goals!

Thanks Polly for sharing your thoughts! It’s nice to hear was resonates with readers.

I didn’t always understand the role of privilege in my life, that’s something I’ve learned in the last 10 years or so. Once my eyes were opened to it, its presence was so obvious.

Nice interview – I liked that you have kept it very simple and amassed a nice NW in your mid 40’s.

In terms of the target $2.5M net worth before retiring, is that outside of your home equity or including it?

Our goal was to have $2.5M excluding home equity.

In the 6 months between the completion of this interview and it’s publication, our liquid net worth has grown to $2.478M. So we are nearly there.

However, we are now aiming for $3.0M. I want to have a bigger buffer because some of these assets are earmarked for the kids, not for our retirement. I still have concerns about SORR. I just don’t feel ready to leave my job. Part of the hesitation is that I am still struggling with the concept of enough. But also there are projects and goals at work I really want to see through to completion.

$3.0 outside of home equity would give you enough of a buffer. The last 6 months have been amazing, another year of such returns and you could almost RE 🙂

Thanks for the reply and good luck on your journey. Will look forward to an update whenever you post it in the future.

Wanting is an excellent book. I listened to a podcast where Luke Burgis was the guest (I can’t recall which one) and enjoyed it. I bought the book when it came out. Mimesis is an interesting concept.

I was also informed about it via podcast! The one I listened to was Paula Pant’s Afford Anything. I’m a big fan of hers in general. She is also one of the reasons I feel pushed to real estate investing. This, coincidentally, is a good example of mimetic desire!