Today I have an update for you from a previous millionaire interview.

Today I have an update for you from a previous millionaire interview.

I’m letting three years pass from the initial interviews to the updates, so if you’ve been interviewed, I’ll be in touch. 😉

This update was submitted in March.

As usual, my questions are in bold italics and their responses follow…

OVERVIEW

How old are you?

I’m now 37 and my husband is 38.

We’ve known each other for 8+ years and married for 5.5 years.

Do you have kids?

Yes! Happy to report that since I last participated in this interview (in 2019) – we now have 2 boys (1st one turning 3 in April; and 2nd one just born on March 21 2023).

It’s been a challenging few years, given that the first child was born at the start of Covid (April 2020) and we were moving countries at the time. It was tough; especially since borders shut before my husband could enter (he’d stayed behind to sort out moving logistics) and he was stuck in another country for 6+ months whilst I gave birth alone in another country with no family or friends allowed to be with me at the hospital. It didn’t help that I also had birth complications and baby came a few weeks earlier than planned and had emergency C-section.

We were isolated from family for 6 weeks — with no one allowed to come see me or the baby as a result. It also took 5-6 months of constant petitioning to the national immigration authorities where I had to make multiple trips to various different government offices during the height of Covid in order to get my husband into the country; and he finally managed to see his firstborn about 5 months after the baby was born.

Fast forward 3 years, Baby #1 is now a rambunctious toddler and we’re just now welcoming Baby #2!

What area of the country do you live in (and urban or rural)?

Currently based in a large South East Asian city (urban).

What was your original Millionaire Interview on ESI Money?

NET WORTH

What is your current net worth and how is that different than your original interview?

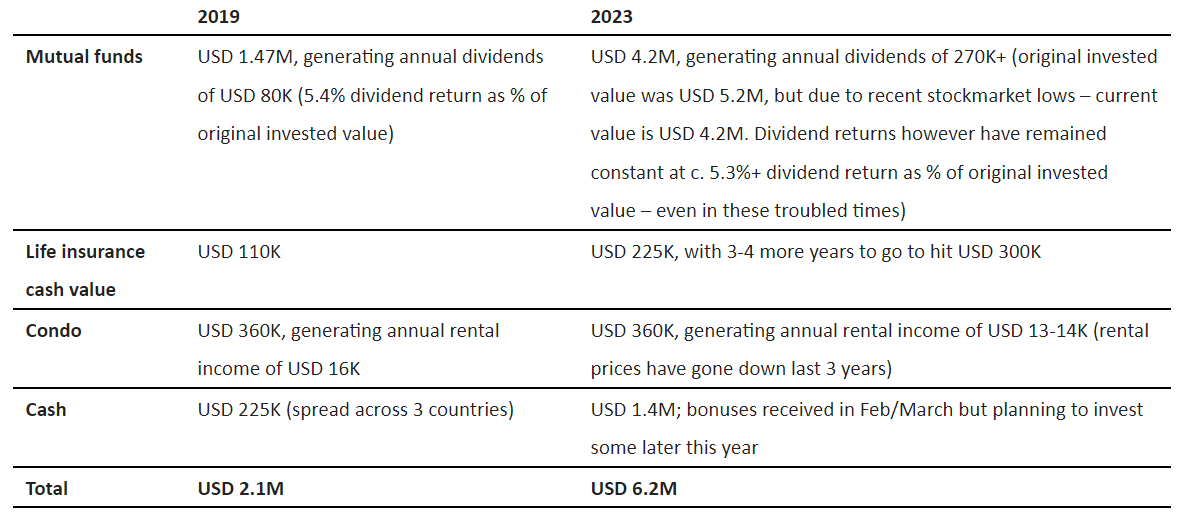

Current net worth is $6.2 million, not including pension / employee contributions (which I now have accumulated in 3 different countries – and left as-is).

The largest pension contributions of the 3 countries have about $620K in pension contributions which also provides 5-6% dividend returns y-o-y; which I could theoretically only withdraw upon retirement or up to a 30% of total balance for health /education expenses for myself, spouse or kids.

The other 2 countries’ pension contributions are much smaller – around $250K in total, but difficult to withdraw as am no longer a resident nor citizen of those countries; so might just have to leave it where it is.

Previously it was $2.1 million, so have increased by roughly $4 million in the past 4 years.

What happened along the way to make these changes?

Not too much has changed.

We have continued to earn, save & invest.

The good: Despite the pandemic; had a few good earning years with big bonuses which added substantially to my NW in the past 4 years. This was also when I shifted to part-time work (4 days a week) to spend more time with my firstborn. Majority of bonuses basically went straight into investments, despite the recent stock market lows; as well as a started a cash stockpile as a safety buffer.

The bad: Looks like the good earning years are coming to an end – as am facing some changes at work; and also the fact that I’ll be hitting my FIRE target soon in terms of reaching $300K annual dividend income. So will be re-evaluating my plan for the next 5 years.

Comparison of (revenue generating) asset breakdowns below:

Also bought a new car in cash last year (not counted in the above since it’s a depreciating asset that doesn’t generate any income) since we’ll now have 2 kids and it’s getting harder to move around without a reasonably sized car.

No credit card debt, loans or mortgages outstanding.

What are you currently doing to maintain/grow your net worth?

Same as before:

- Earning, saving & investing into dividend generating funds

- Setting aside some funds for my children’s education

- Funding a cash buffer in anticipation of FIRE

The growth in my net worth in the coming years will likely slow and plateau as I hit my FIRE target; and the shift will move from ESI to ISE where the focus would be less on earnings maximizing and wealth accumulation and more on maximizing time spent with loved ones and figuring out what I want to do outside of work.

EARN

What is your job?

Partner in a consulting firm.

I have been in the industry for close to 15+ years now; having worked in Europe & Asia.

What is your annual income?

Varies as it depends a lot on firm’s performance plus whether I hit/exceed my sales targets.

Currently annual income is about $380K+ base with variable bonus (which can be anywhere from zero to 2-4x base) depending on firm’s performance & whether I hit/exceed my sales targets.

In the past 4 years; have made on average $1-1.4 million a year total comp pre-tax (not including deferred bonuses).

Also – have passive income of $270K+ in dividends and $13-14K in rental income. I am the main breadwinner as my husband is currently the stay-at-home parent and doing a fantastic job with the kids.

How has this changed since your last interview?

Not much has changed – other than having a few great earning years as a partner.

But there’s some recent changes at work at play which is forcing me to reconsider my timelines for FIRE. Given the birth of my second child recently, it’s also time to re-evaluate our priorities as a family.

Have you added, grown, or lost any additional sources of income besides your career?

As you’ll have seen from the above table – I’ve not added any new sources of income; but have significantly grown some portions, e.g. have increased dividend income from $80K to $260K per year.

My FIRE target is to hit $300K+ in dividend income; which would more than cover our annual household expenses (currently $75K for family of 3; projecting that to increase to $100K for family of 4).

This would actually happen later in the year; once I’ve invested the spare cash from bonuses received earlier this year.

SAVE

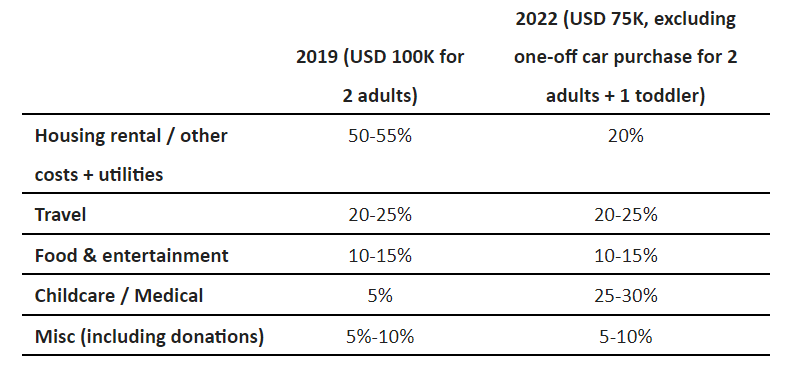

What is your annual spending and how has it changed since your interview?

Annual spend is $75K for family of 3; which is actually lower than previously.

In my previous interview during 2019 I estimated potential annual spend would be $70-75K, but in reality – we hit $100K due to various moving costs and travel in 2019.

During Covid (2020-2021) – it dropped to about $60K for family of 3; but that was largely due to the fact that we didn’t eat out or travel much with the various lockdowns that occurred. As countries have relaxed travel restrictions, this has now increased to $75K for 3 (2022); and likely will increase to $100k for family of 4 (plus increased travel).

We also bought a new car last year to cater to our increasing family size.

In terms of spending categories:

What happened along the way to make these changes?

Reasons for the changes would be:

- We moved countries and moved from a HCOL city to a lower cost of living city, so cost of housing dropped by more than 50%. Taxes however has increased; so you win some, you lose some. However – we are now living close to my family, which has been a huge help especially in terms of having grandparents nearby to help with our child.

- Costs of childcare plus a number of unexpected medical emergencies cropped up; so that increased by 5-6x relative to previously.

- Travel was significantly lower during Covid; but we started traveling again in 2022 – so that went back up. Even though the number of trips have dropped; the number of family members and costs of travel have increased – so the percent spent on travel was roughly similar to pre-Covid.

So in terms of household spend (excluding taxes); that has remained fairly constant at about $75K despite our family increasing from 2 to 3. However, as mentioned, am expecting an increase to $100K due to increasing from 3 to 4 plus increased travel.

INVEST

What are your current investments and how have they changed over the years?

See prior table above in terms of investments / assets. Not much has changed.

I’ve always planned on hitting FIRE using a dividend fund based strategy as way to generate passive income; and am currently on track.

What happened along the way to make these changes?

No changes.

Just keep plugging away at it until I hit my FIRE target. 🙂

MISCELLANEOUS

What other financial challenges or opportunities have you faced since your last interview?

Key challenges faced:

- Moving countries and having kids during Covid was pretty tough – both financially and emotionally/physically! Cost of childcare and medical care has gone up drastically as had some medical complications at birth and some health issues for my firstborn when he started playschool has landed him in hospital a couple of times. My husband also had some medical issues which also landed him in hospital a couple of times. And unfortunately neither is fully covered under my company insurance; so had to pay a fair amount out of pocket. Luckily we had the financial means to do so – but that caused me to start stockpiling a significant sum of cash set aside for such emergencies. Will also have to start investigating alternative forms of insurance coverage – given that my company insurance has such poor coverage (doesn’t cover maternity/child-related costs and v. limited spousal coverage).

- Stock markets have faced challenges in the past 12+ months; and given the bulk of our net worth is invested in the market – that has taken a big hit. I am currently down $1 million ($4.2 million vs. $5.2 million). Haven’t sold any positions – but have added instead; as my strategy is to “Buy & Hold” in dividend funds – but it still was nerve-wracking to watch the markets continually drop for the last few months. Was lucky to be able to offset most of it with increases in income (which I funneled straight into investments); but as mentioned – that looks like it’ll be coming to an end soon as well.

Key opportunities/benefits:

- Living closer to my parents has been a huge benefit – both financially, emotionally & physically. Given the lockdowns and daycare centers/schools constantly having to shut due to Covid/flu/etc. – having my parents nearby to help look after our child was a godsend! We’d originally planned it 4 years ago; with the birth of our first – but we really only realized how lucky we were and how amazing my parents have been during Covid. And also it’s been a joy seeing our son interact with his grandparents and other relatives and spending this precious time with them. I’ve seen on the MMM forums that time spent with loved ones is one of the most precious commodities that you can never get back – so it was a blessing for us in that respect.

- Have also started drafting up will(s) to ensure that my husband and kids are well covered if anything happens. This was something that I’d learned from the MMM forums; the importance of estate planning. It’s a bit more complicated since our assets are split across multiple countries; and apparently it’s easier to draft up a separate will per legal jurisdiction. We’d never really thought about it in the past; but having kids and some recent medical emergencies do bring it closer to the fore.

Overall, what’s better and what’s worse since your last interview?

What’s better:

- Living closer to family has helped significantly, especially with children!

- Moving countries, having kids and living through a pandemic has definitely brought my husband and I closer. It’s been tough and we’ve both been tested at times – but at the end, I think we’ve come out of it having a greater appreciation for each other and being more willing to overlook each others’ faults and to lean in when needed. He’s also been a fantastic dad and supportive husband – and I hope to be able to reciprocate in the future when we consider what to do post-FIRE. 🙂

What’s worse:

- Whilst I’d been able to manage a reasonable work-life-balance during Covid due to work-from-home, it’s now getting increasingly hard to manage as countries reopen and travel restarts. Our clients are increasingly expecting us to be back on-site; although this does vary by client – and that makes it harder for me to manage. With our first, I already feel that there’s not enough time to spend with him, family and also for myself. With a second now – it’ll be even more challenging.

What are your plans for the future?

As mentioned; we’ll be hitting our FIRE targets soon – and am currently evaluating what our plans would be for the next 5 years.

Whilst we don’t have a clear idea as yet; we do have the following considerations:

- I’d like to be able to spend more time with my children, as these are the formative years in their lives.

- Due to Covid, we’ve not been able to travel – so would like to take the opportunity to do more travel whilst the kids are not yet in school (e.g. before they hit 6 years old); as our idea of travel is less spending a few weeks here and there but more “slow travel” where we can spend a few months in a country to really experience what it’s like. Plus given that we’ve not really figured out where to settle in the long-term; would be a good way to experience different countries and see what it’s really like once the “holiday sheen” has worn off

- The past 5+ years we’ve been very focused on my career as we agreed that would be the fastest way to hit our FIRE target. My husband has had to step back in terms of his career / other desires and spend time being the primary parent as a result. Now – I’d like to take turns prioritizing his career/future desires in the next 5 years whilst I spend more time with our kids

Given that you have a bit more wisdom and experience, what advice do you have these days for ESI Money readers?

Besides ESI, I would also strongly urge others to review their overall life plans and targets every 3-5 years to see if they’re still relevant. For a lot of folks (including myself) – the focus on wealth accumulation can be an all-consuming goal.

The question is – if you’re starting to reach it or if life no longer feels worth the grind; is it worth powering through for the next few years or taking the foot off the pedal to enjoy life a little bit whilst coasting comfortably to your goals?

Also – life is short; I’ve seen quite a few people pass away during Covid to realize that time spent with loved ones is infinitely more precious than trying to earn more $$.

Great update – You are killing it – congrats! My wife stepped back from a lucrative engineering career when our daughter was in 2nd grade. Wife still says it was the best decision!

Thanks – hopefully we think the same too!

Thanks – we hope so too!

Congratulations on such a high NW at a young age! I am curious as to what Mutual Funds have you invested in?

Congrats! Yes, I would be interested in the dividend Mutual funds details as well. Thank you.

To caveat: I know that mutual funds have higher expense ratios than ETFs or stock indices, but I am in a country where I have limited access to either and also not taxed on dividend income.

The ones I’ve invested in are: Pimco Global Income funds (5.5% dividend return), First State Dividend Advantage (3-4%) Allianz Income & Growth Funds (7-8%), JP Morgan Income funds (5-6%), Morgan Stanley Global Multi-asset funds (5-6%). There’s a couple others which aren’t doing so well, so haven’t put in any more money there.

Congrats on your success and family! I need to revisit the dividend strategy. Thank you for sharing!

Can you please share more on your FIRE plans. If you are already making $300k per year in Dividends you should have more than $240k post tax to spend. With expenses of $100k, why don’t you have enough to retire today?

Hi Mark

Thanks for your question.

Originally the plan was to retire at 40, with the aim of having an even bigger margin of safety since we’d be retiring with 2 young kids and we planned to fully fund their education / healthcare / etc, which can be quite costly. Plus we plan to buy a place somewhere once we’ve figured out where we’d settle in the longer term.

Also – we’d need to ensure what we have keeps up with inflation as well and needs to last us for at least 40-50 years in addition for kids, which is far longer than the typical retirement scenarios of 20-30 years.

However have decided to pull the plug since work was becoming more challenging and preventing me from spending as much time with my kids as I’d like.

The current $300k target is so that there’s some allocated for ongoing investments to continue to build the nest egg even in retirement to ensure we don’t run out of money over the next 50+ years.

Congrats and great job reaching your goals so quickly! You have the same target I had, $300k income in retirement without touching the principal. It’s a great target in my opinion but totally not necessary. Having been retired 9 years now I’ve realized a life well lived costs nowhere near that much. So good news is you and your family are going to be fine even if you pull the rip cord tomorrow. I would suggest giving it a few more years as well as 37 is about the age you start to feel that pull to walk away, but it’s awfully young, and unless you’ve got a plan for what’s next I think you’d not get the most out of early retirement. But use the next few years to formulate what you want the next 20 to look like.

Congrats again, I love reading stories like this of young people crushing it out there!

Thanks for your kind words!

My husband and I have spent some time since this was written discussing our plans for the next 3-5 years, so I think we do have a plan for how to enjoy our early retirement. Or mid-career break if that’s more palatable to folks 😉

I’ve also taken up some coaching certifications so as to prepare for my next career pivot, executive coaching – which would allow me to have the flexibility that I want plus still some engagement with the corporate world on my own terms.

If I do get bored, can always go back into the corporate world- but for now I want to spend time with my kids when they’re young and want to be with us. When they’re older and in school, then things would probably change