Today I have an update for you from a previous millionaire interview.

Today I have an update for you from a previous millionaire interview.

I’m letting three years pass from the initial interviews to the updates, so if you’ve been interviewed, I’ll be in touch. 😉

This update was submitted in January.

As usual, my questions are in bold italics and their responses follow…

OVERVIEW

How old are you?

I am 62, my wife is 61, and we’ve been married for almost 39 years.

Do you have kids?

We have 3.5 children. When I tell people that I always enjoy seeing the mental gears get jammed up as they attempt to process the half-child.

And then I explain: he is a Chinese exchange student who lived with us for a couple of years about ten years ago. He has become very much a part of the family since then.

We share him with his Chinese parents so we consider him half ours, although we get to see him far more often since he still lives in the States. He is here on a student visa and is pursuing a PhD in computer science.

Two other kids are out on their own, one of them married with our one grandchild, and one boomerang kid who is now living back with us (temporarily) during the divorce process.

What area of the country do you live in (and urban or rural)?

We live in the suburbs of a larger city in the upper Midwest. ESIMoney’s old stomping grounds.

For the last few years, we have “lived” in an RV in January and February, usually volunteering somewhere warmer than the upper Midwest.

Retirement has afforded us the opportunity to travel extensively, often for many weeks at a time. So the definition of “home” is sometimes rather fluid.

What was your original Millionaire Interview on ESI Money?

I am MI-241, and the interview was published on April 30, 2021.

NET WORTH

What is your current net worth and how is that different than your original interview?

When the original interview was written, our net worth was $2.8M. It is now $4.2M.

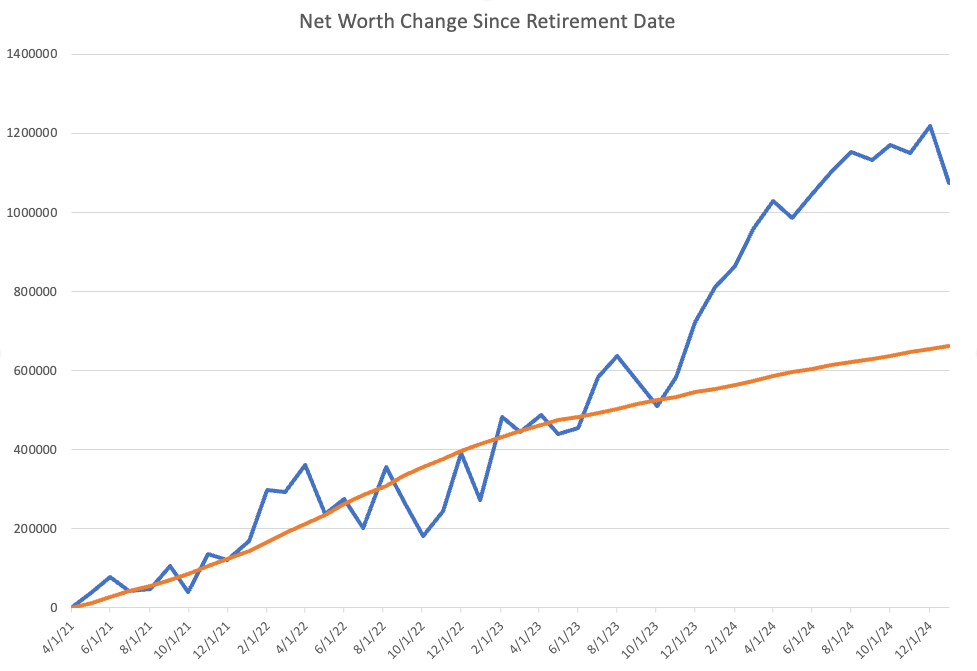

The original interview was written several weeks before my retirement date of April 1, 2021. Since then I have plotted our net worth monthly and the graph looks like this:

The blue line is our net worth, normalized to my retirement date. So this line represents change in net worth since then.

The orange line represents a scenario that just grows by the rate of inflation each month. My wife tends to worry about inflation eating into our spending power, so I added this to help allay her fears.

I have to tell her to keep in mind that expenses are baked into this number so we can take approximately $120K in expenses each year and still, the chart has risen rather significantly over the last four years.

What happened along the way to make these changes?

The Good:

We’ve developed sources of passive income to offset expenses. A stretch goal is to cover expenses entirely with passive income, and we’re nearly there.

Passive income covered 98% of expenses in 2024. Sources of passive income include:

- Rental property. We have one rental property which nets about $25K per year.

- Real estate syndications. We have several real estate syndication deals, most of which have stopped producing income because of the challenging interest rate environment. If all of these deals were performing as originally promised, our passive income would be above 100% of expenses (this probably belongs in the “bad” paragraph).

- Real estate debt funds. We’re invested in a couple of funds which do hard money lending. These funds are consistently returning about 10%.

- Raw land. A couple of deals in raw land and industrial park development are returning 10% to 11%.

- Dividends. A rather large amount of company shares from the last job pay out a steady dividend.

We’ve received two inheritances, totaling about $200K.

Sale of rental property. We sold a rental property in 2021. Originally purchased in 2011 for $170K, it sold for $600K. Nice boost to the bottom line.

The last two years have seen a nice run-up in stock prices. Just under 40% of our net worth is invested in broad market index funds so this has helped cover losses elsewhere.

The Bad:

We piled into real estate syndications over a few years starting in 2020. While we had one go full-circle and return a nice profit, most of those deals since then have stopped paying their preferred returns.

One of them recently was forced to sell and resulted in a complete wipeout for the limited partners. Another appears to be close to that point.

Others are floating the spectre of capital calls and/or have used preferred equity to bolster their cash positions.

My one dividend stock is mentioned above. After a couple of quarters of disappointing news, the price of the stock dropped significantly.

I did manage to donate a bunch of shares to my donor-advised fund near the peak price point several months back, but the drop has impacted my tax strategy for this year. Since my federal income is near zero due to lots of passive activity losses and charitable donations, I did a bunch of capital gain harvesting of this stock: selling the shares to realize the gains, then immediately buying them back.

I’m still good with the capital gains harvest, but the repurchased shares now show a rather significant loss.

Rental Property: Revenue was significantly lower this past year as we had one tenant that was several months behind on rent and finally moved out. About that time the electricity was cut off from that unit due to nonpayment.

When we got into the unit several days later we found a completely trashed unit with a refrigerator full of spoiled food. Several weeks and a few thousand dollars later we now have a new tenant who gets to enjoy all new flooring, repaired and painted walls, and a refreshed kitchen and bathroom.

We also did a complete kitchen remodel in another unit earlier this year.

What are you currently doing to maintain/grow your net worth?

We’re rotating out of some of the real estate syndications where possible. Most of these have lockups of 5 years or more so not a lot we can do, but one operator offered to buy out our position in a deal if we placed the funds in their income fund.

We jumped on this, intending to exit the fund after the one-year commitment.

We’ve bought into a couple of hard money lending funds, which pay out a consistent cash flow around 10%.

Other than that, it’s stay the course. We’ll continually tweak this over time but right now, in spite of the underperforming syndicates, we’re still doing OK.

EARN

What is your job?

I retired in April 2021, shortly after completing the original MI-241 interview. Since then, other than a short consulting stint, I have not done any paid work.

I worked for 36 years as an electrical engineer, a very enjoyable career, but I’m glad to be done with it and have never looked back.

What is your annual income?

We just did a review of 2024, and our passive income came out to just under $120K for that year.

How has this changed since your last interview?

Back in early 2021, we had a few sources of passive income including the first of several real estate syndications and two multi-family rentals (11 doors). At the time of retirement, passive income was about $70K.

We started developing additional sources of income about 18 years ago when we bought our first rental property. We acquired a total of three rental properties during the heady years of 2006 through 2011.

Two of them needed significant rehab which gave my teenage boys some decent work for a number of months. We sold one of the properties and branched out into syndicates a couple years before the last interview, and additional syndicates since then were part of the same plan.

Have you added, grown, or lost any additional sources of income besides your career?

Between the original interview and now, we have sold one of the rental properties, picked up a few more syndicate deals, and have put additional money into some debt funds. We agonized over the decision to sell a cash-flowing rental property for a while, since that would reduce our yearly cash flow by $25K, but prices were high and we sold at the top of the market.

We used the funds to buy into a couple more syndicates, a debt fund, and to raise our cash position. In retrospect, the rental property cash flow was better and more consistent than the syndicates that succeeded it, but some work at the rental property put me in the Emergency Room, so we considered that a fair trade.

We’ve been focusing more on cash flow lately so investments have been mostly in debt instruments that pay out consistently.

SAVE

What is your annual spending and how has it changed since your interview?

Annual spending is in the range of $120K to $130K. This has changed relatively little since the original interview.

While the amount has not changed much, the mix has. Taxes used to be far and away the top expense, now it is probably somewhere around number six.

Since nearly all of our income is passive and we can claim passive activity losses, we have been able to bring our Taxable Income down to near zero the last couple of years. Charity has always been near the top, now it is number 1.

Travel was somewhere in the middle, now it falls only behind charity, as we have taken many extended road trips since then.

What happened along the way to make these changes?

As an engineer, I have taken a data-driven approach to planning, saving, and investing. I developed several spreadsheets to track income, taxes, expenses, and the like, partly to satisfy my own need for a good representative picture and partly to convince my better half that we are, in fact, doing OK.

She leans to the more pessimistic side of things and so needs to be reassured when our net worth drops by $150K in a month that we don’t have to start living like paupers. As a result of having this kind of data, we have been able to increase our travel expenditure greatly and still know we have a comfortable margin above pauper-ville.

And when syndicates start to go belly-up, the data shows that our effective withdrawal rate is still less than one percent, far below the 4% metric that is widely used in financial and retirement circles.

INVEST

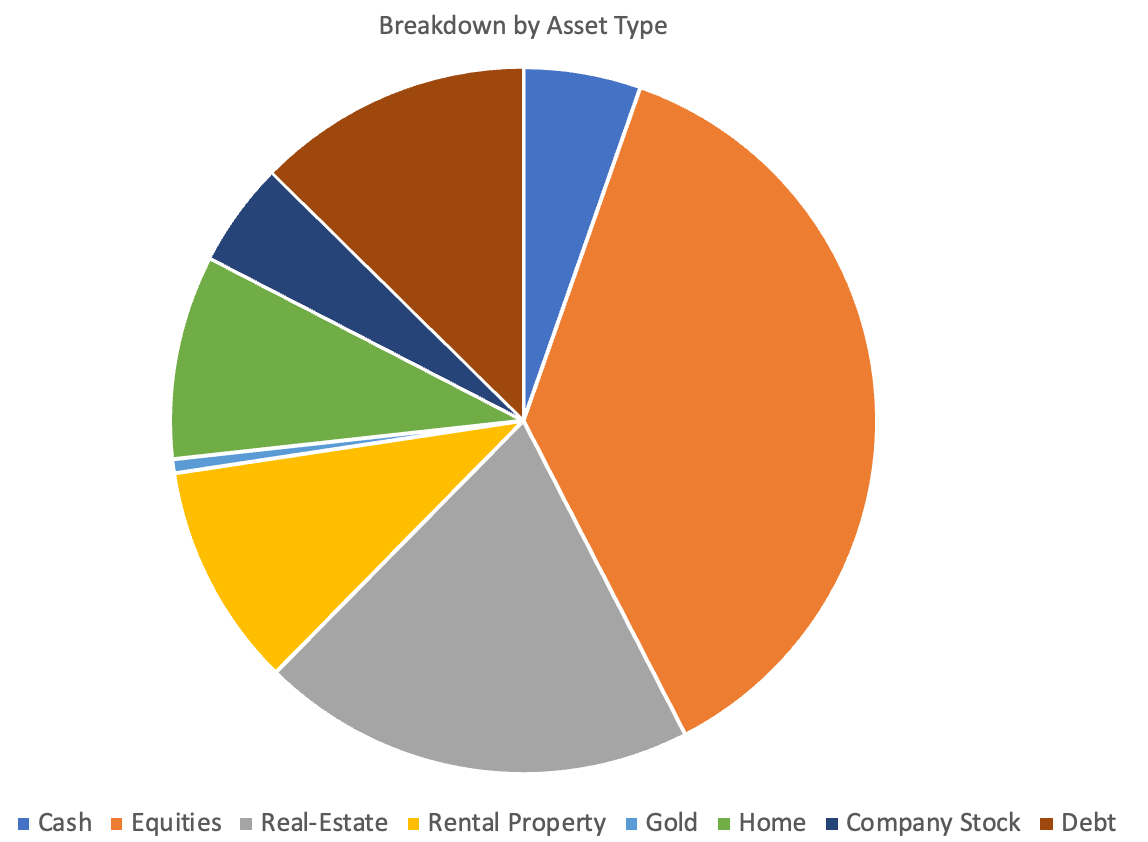

What are your current investments and how have they changed over the years?

We are spread out into a few major asset categories:

The largest of these is Equities (stocks) held in a broad-market index fund. The run-up in the stock market the last couple of years has enhanced this nicely.

Next is Real-Estate, composed of several real estate syndicate deals. It’s a little tough to value these so they are in here at original purchase price.

I would imagine this slice of the pie may shrink somewhat to reflect deals in distress.

Debt is composed of a few hard money lending funds, and investments in raw land and business park deals where I have no equity stake in the asset.

The yellow slice represents our six-unit rental property. Valuation of this is based on the city assessor’s value, however it would probably still sell for a significant premium over that.

I’ve included our home in this chart. Some may choose not to do so.

Company stock has shrunk almost by half since its peak. May need to re-think our position here.

Cash represents about 5% of the picture. We try to maintain a decent cash position as a buffer and as dry powder if something comes along.

Years ago, we bought a few gold coins. Back then we were thinking of some sort of inflation hedge, now they are just pretty metal which is a tiny fraction of the pie.

It’s rather fun to watch, however. I bought it at about $350/ounce about 20 years ago. Now, at the time of this writing, it is just over $2600/ounce.

We’ve increased our investment in debt instruments. As of the last interview, we had almost nothing, now it’s 13% of the pie. This is part of our effort to increase steady cash flow.

We have also shrunk our holding in company stock. So it’s not just the price that has made the piece smaller. This has been our main source of funds for our donor advised fund as most of the company stock is highly appreciated and donating it doesn’t result in a taxable event.

And, looking back at it, real estate syndications are probably a piece of the pie that’s too big.

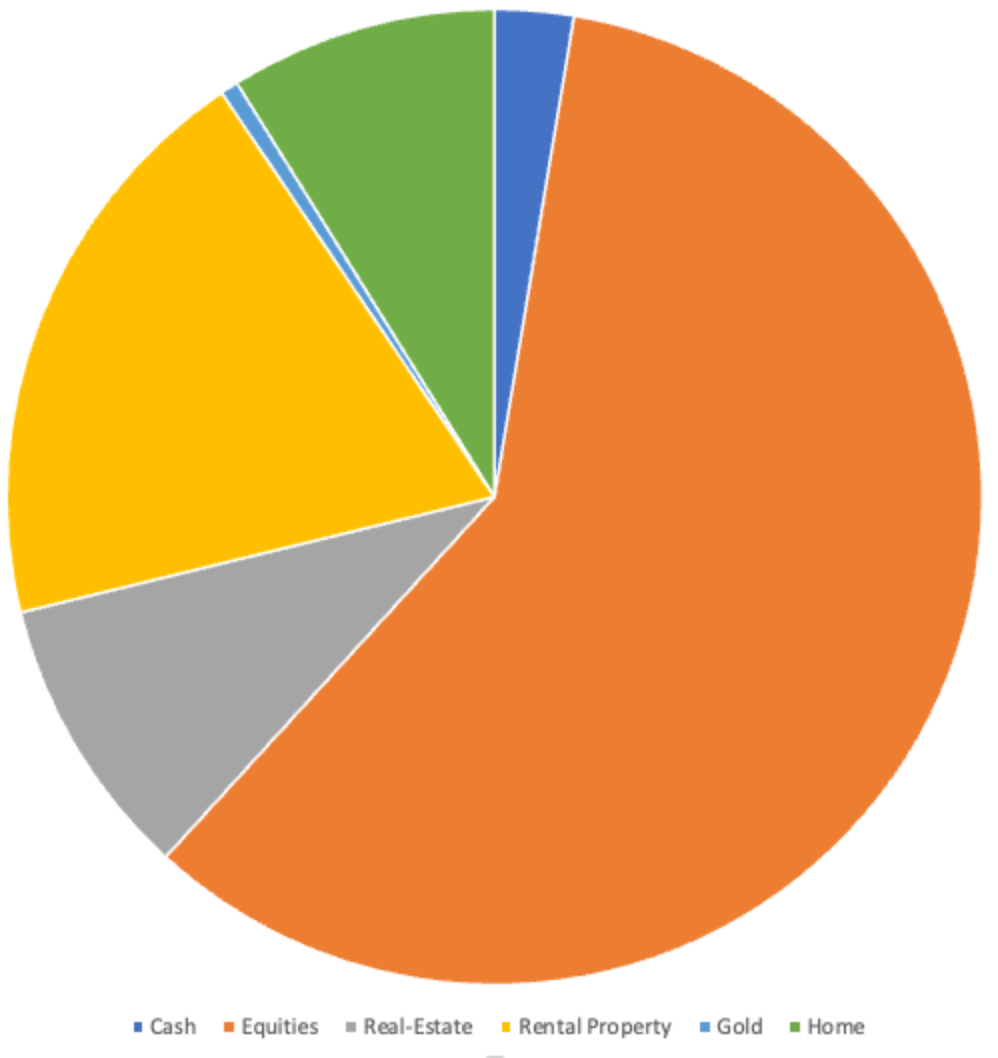

This allocation has changed from 2021, when it looked like this:

Back then, stocks were a much larger piece of the pie as most of our assets were being managed by a financial planner. I was just starting to rotate some funds out of stocks and into syndications.

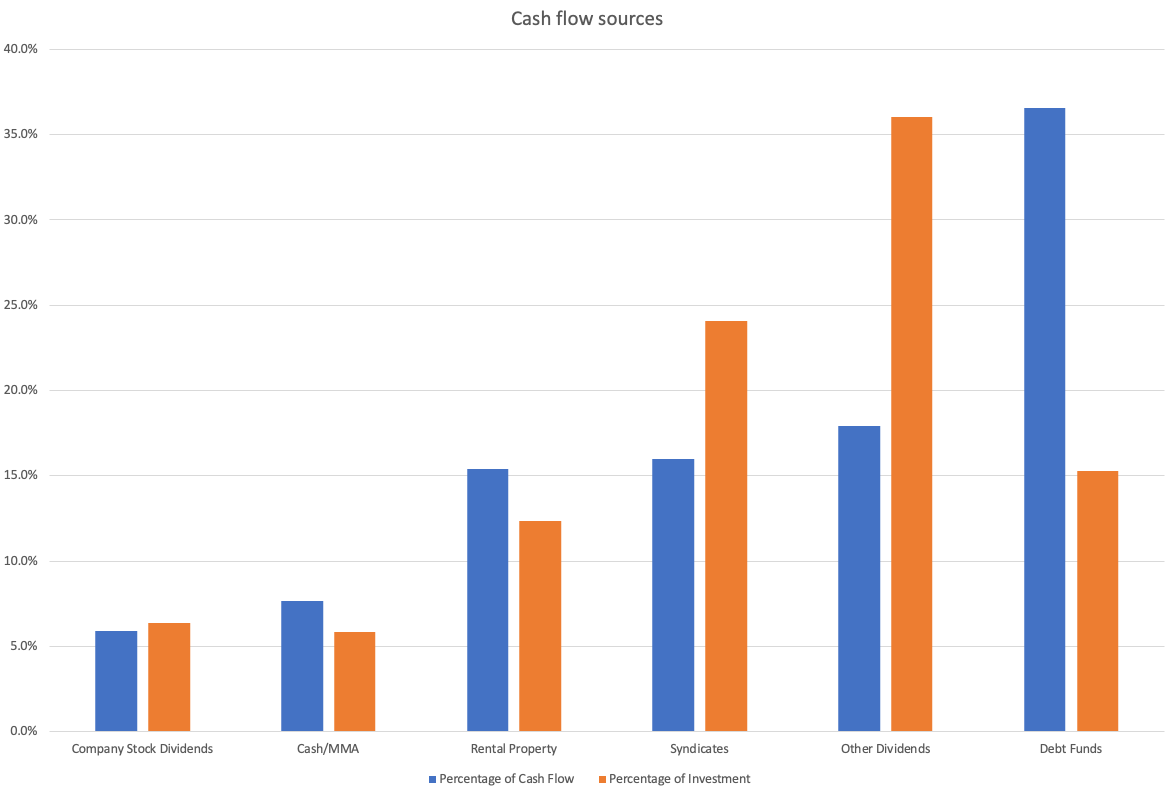

When all this data is contained in a spreadsheet, some interesting stuff can be observed from it. I looked at all our sources of cash flow and graphed the percentage of assets contained in each asset type alongside of the percentage of cash flow generated by each asset type.

The result looks like this:

The orange is the percentage of the total cash-flowing assets that this one represents, and the blue is the percentage of the total cash flow that this one generates.

So, for my holdings of company stock, the holdings represent about 7% of the entire pot, and it generates about 6% of the total cash flow. So, pretty even.

Most of our available cash is in money market accounts, representing just under 7% of the pot, and it generates about 8% of the total cash flow. When it gets really interesting is on the other side of the chart. Debt funds represent 15% of the total investment, yet generate 37% of the total cash flow. For “Other dividends” (from stocks, mutual funds, etc), the equities represent 36% of the total investment, but generates only 18% of the cash flow. What this doesn’t show is capital appreciation so the stocks will have additional benefit when they are sold.

Looking at this result, we will probably make some effort to reduce investments in company stock and syndicates and place those funds, when available, into debt instruments.

What happened along the way to make these changes?

I realized I was moving funds out of the realm of our financial planner and doing more myself, so I ended the relationship and took on the entire task myself. And suddenly the sixth largest line item in the expense list disappeared.

Over the next several months I rotated all the assets out of the accounts he was managing and into either index funds or alternative investments. He had me in a bunch of individual stocks and ETFs, and unraveling these without creating too much of a tax hit involved donating the ones with the highest appreciation and selling the rest over a couple of years.

The end result was more diversified and included more investments that generated a cash flow.

MISCELLANEOUS

Overall, what’s better and what’s worse since your last interview?

Since my last interview occurred approximately around the time of my retirement, some of these items may be more related to retirement than anything else.

Better:

- The bottom-line net worth figure: $2.8M at the last interview, $4.2M now. Even if we take some impairment due to under-performing syndicates and knock a few hundred grand off of this, a runup of a million bucks in four years, after expenses, is pretty incredible. If I were to translate that into an effective wage, that’s a quarter million dollars per year. Quite a bit more than I was making in my W-2 job.

- Taxes: not having everything come in as ordinary income allows for better and more creative tax planning, so taxes have been reduced significantly.

- Time: not exactly a financial thing, but it does allow me to do my own financial planning as I have the time to do this. I also do my own taxes and those of a few family members.

- Wisdom: It is said that the school of hard knocks is the best teacher and we certainly have paid our dues to that school. We’ve learned what investments to make, and, more importantly, what investments not to make.

Worse

- Real-estate syndications: In 2021, interest rates were low and it was easy to make the numbers work well on many large commercial or residential real estate deals. Take those same deals that were financed with variable-rate debt, crank up the interest rate to double or triple the original amount, and suddenly things don’t look so hot. We have some deals in trouble, even from our most trusted operators, with at least one showing a complete loss of the $50K we put into it.

- Taxes: Another downside of some of these real estate deals is the complexity of the tax picture. K-1 forms often come in late, requiring us to file extensions. They also can span multiple states. Tax returns can span hundreds of pages. I’ve been finding that retail tax software such as TurboTax is not up to the task. I’m a DIYer but have jettisoned TurboTax for software that the pros use. And TurboTax just nickels and dimes you to death. By the time I’ve added state products and e-files and upgrades because the version I have doesn’t do such and such, and the business version, I’ve spent just as much as on Drake Tax, which is what I am using for 2024.

What are your plans for the future?

Financially, continue to execute the plan. Tweak the investments towards a more consistent cash flow.

Rotate out of many of the real estate syndication deals when possible. We do have some deals that are performing well and will probably continue to work with those operators.

Work on automating and simplifying investments towards consistent mailbox money—a check each month or each quarter. Keep the withdrawal rate low (currently below 1%), and, as a stretch goal, develop enough income to drive the withdrawal rate to zero.

Maintain enough of a financial margin to meet any challenges that come our way: sudden medical needs, giving opportunities, bucket-list travel, purchasing a new car/RV, etc. Simplify the tax picture while still minimizing taxes.

In areas other than finances: Travel more. Give more. Volunteer more. Use our resources to buy experiences rather than things.

Given that you have a bit more wisdom and experience, what advice do you have these days for ESI Money readers?

Do your due diligence when researching investments, make your decision, then, if things still go bad, realize that good decisions can sometimes still result in bad outcomes. Build enough margin in to allow those bad outcomes to happen without jeopardizing the plan.

Seek like-minded people to share the journey with. If you are married, your spouse is a great start.

My wife and I bounce things off each other often and we will sit down in the situation room once a month and go over the numbers and make any necessary tweaks. It’s likely that spouses will have a different approach to financial matters, retirement matters, or just about any matters. And that’s a Good Thing.

My wife is the more cautious one and sometimes it seems like I have my foot firmly on the gas and she has her foot firmly on the brake. And then we’ll talk the particular financial matter through and arrive at something that is probably better than each one of us could do alone.

Like-minded people can also be a small group of trusted friends. I and two other guys I know will often trade emails about a particular investment or strategy and we can be rather honest and open with each other because we know each other well.

Like-minded people can also take the form of an internet forum. MMM comes to mind.

Although I haven’t been able to participate much lately, I have gleaned some good ideas and advice from the folks on MMM.

Although this is a lot about finances, much of this advice can be applied to non-financial stuff also. Due diligence also is a good thing when researching a vacation destination, looking for a job, and even looking at a new restaurant for dinner (although the stakes (steaks?? [hahaha]) can be far different for each of these).

Seek like-minded people for many things. We’ve gone on camping trips and vacations with a like-minded group of friends for over 30 years.

Money is a means to an end, not the end in itself. Figure out what that end is.

Speaking from the other end of nearly four years of retirement, financial independence and early retirement has allowed travel opportunities and volunteer opportunities that we otherwise would not have had while still working. It has also allowed the flexibility to come alongside of family members when in need.

What is your end, your purpose, your calling? Now spend the money to make it happen.

This was a good one. Honest with no pretensions as some are.

Thank you kindly

Congratulations on your success! I am considering investing in hard money loans as I have not been doing well with investments. Would you share what companies you would consider worth checking out based on your experience?

We’ve bought into a couple of hard money lending funds, which pay out a consistent cash flow around 10%.

There are a bunch of them out there, and a couple names have bubbled to the top of my list as ones to invest in. This is by no means a recommendation, you have to do your own due diligence and go with what’s comfortable for you. I’ve invested in funds from Boomerang Capital and Indicate Capital, both funds that do short-term fix-and-flip loans and construction loans, mostly in the residential space, mostly in the states of Colorado, Utah, and Arizona. So far, they have been fairly consistent in their returns.

Thank you!

Hi from MI32. Thank you for sharing your update and I have a few questions as I’m a few years behind you but planning on my exit in 4 years. I have passive income from real estate and a similar amount of money in retirement funds. Can you share cost of medical benefits and how you are obtaining. Is it ACA exchange as u am budgeting $2500 per month to buy for family of 3 years midi g wife and one of mi kids. Also I plan to have a

Similar budget. So is your fed tax rate around 15%. Thanks again

I don’t understand your math. You spend $130K out of $$4,200K. To me, that’s a (very respectable) 3 per cent WR, but not less than 1 per cent.

Hi seclawyer,

It’s fairly simple: I have several investments that generate cash flow. Spending is offset by cash flow coming in. If I spend $130K in a year but have $120K in cash flow income, my effective portfolio draw-down is only $10K, making my withdrawal rate just a fraction of 1%.

Thanks for your comment.

The $130K that you spend annually is the amount withdrawn from net assets of $4.2M, which is a 3.2% annual withdrawal rate. Most personal finance experts, Big ERN for example, would consider that “safe” (although maybe not perpetual). So I say you look good. But a 1% withdrawal rate and a $130K spend would imply a $13M net worth. Cash flow has nothing to do with it. All best wishes.

I would respectfully disagree and say cash flow has everything to do with it. If I have $130K in expenses and $130K in passive income, my withdrawal rate is zero. Increase the cash flow to $140K and the withdrawal rate goes negative. In my situation, my cash flow last year was $120K, so the actual withdrawal from principal was $10K, making the withdrawal rate 0.2%. Ignoring incoming cash and sticking to a simple withdrawal rate calculation (expenses divided by net worth) puts you at risk of way over-accumulating.

Whether or not this is “safe” is a different discussion.

Thanks for your comments

I respectfully disagree as well with using cash flow in addition to the SWR calculation. It’s already factored in when you estimate future returns.

This sentence is misleading “ And when syndicates start to go belly-up, the data shows that our effective withdrawal rate is still less than one percent, far below the 4% metric that is widely used in financial and retirement circles.”. Any cash flows are added to your net worth and then the % is the total spend as a percentage of the net worth. Otherwise my withdrawal rate is significantly below zero. I don’t even spend the dividends my shares generate.

I agree with the way you look at it. My pension will cover all my planned expenses the rest of my life. I don’t plan on taking any money out of my retirement funds making my withdrawal rate 0% as well.

I think he’s saying that his $130K spending is covered by passive income (let’s say that’s $90K) plus 1% WR ($40K).

The 4% rule, or any other financial planner recommendation on safe withdrawal, is NOT calculated like that AFAIU. So I think he’s comparing apples with oranges when considering this 1% in comparison to normal SWR advice.

Hi RJ,

I would consider this more of an apples to apples comparison, perhaps comparing the Northern Spy apple to a Honeycrisp apple. They are both apples but are used for a different purpose. The oft-misused 4% rule was meant as a rule of thumb to evaluate how much retirees can safely withdraw from their investment porfolios without running out of money over a 30-year retirement. There are some assumptions attached, such as a 75/25 stock-bond mix, but it actually IS calculated using expenses divided by portfolio value (net worth)

And, yes, I am misusing the 4% SWR calculation to some extent. I am not applying it to a 75/25 mix, and I am drawing any income as cash flow and using that to offset expenses. So the effective withdrawal rate will be somewhat different in a true SWR calculation than what I am using. But the net result is still the same: a number that can be used as a first-line indicator of financial health. It’s kind-of like the check engine light in your car. The light doesn’t say what’s wrong, it just lights up to say you need to look into something further. As long as the withdrawal rate stays significantly below 4% (and it’s another discussion why I am using 4%), the light is off. If that rate pops upward, it’s time to get out the diagnostic tools and figure out what to do about it.

Thanks for your thoughts.

Hi from MI32 and thank you for sharing your update. I’m a few years behind you and planning my exit in 4 years at age 61. I already have income from rental properties which I have owned for over 20 years and without any debt attached. I have a family of five but when I retire it will be down to 3 for medical benefits. I am budgeting $2500 per month and plan to purchase through the ACA website. Can you share how you are getting medical benefits and their cost. Once my working income is gone I’m hoping to qualify for subsidy too.

Hi MI32,

We weighed a bunch of options when planning this out and eventually settled on a faith-based health sharing ministry to fill the gap until Medicare is available. It’s hard to plan for medical issues and emergencies, so coming up with a monthly number is mostly a finger-to-the-wind exercise. Since this particular plan handles benefits per medical “event”, we figured six events in a year and added the deductible for those events into the overall cost. Also, routine wellness, things like colonoscopies and mammograms, dental, vision, and the like are not covered, so we estimated this also and added that in to achieve a final number. Actual base cost runs about $750/month for the two of us, and costs with everything included probably is somewhere around $1200 to $1400.

You can probably qualify for subsidies when your income is gone as ACA subsidies are based on numbers from your tax return. Our federal tax rate last year was zero as all of our passive income was offset with passive activity losses and there was no W-2 income. You can get more creative tax-wise when the W-2 income is gone.

Thanks for your comment

Congratulations! You’ve done really well. It must feel pretty awesome to have your net worth go up that much!

One thing I wondered about when I read this, and I often wonder as well with many comments in the MMM forum, is whether it’s worth it to go to such extreme lengths to generate “passive” income.

I must admit I say this is someone who has about $130,000 a year in net rental income! 😂

But what I mean, is people often have a portfolio of dividend paying stocks, and then just try to live on the dividends. You described a few other ways in this interview.

It sure seems like it would be simpler, much less complex, less risky, and perhaps result in overall higher long-term returns to just invest in a broad index and harvest the gains as you go.

I assume this is a psychological thing. Is that right? Do you just just like the idea of generating income that comes from the asset, without ever having any risk that you would use up the asset?

I know I love that about rental income. The rent comes to me every month, and the asset is still there slowly growing, usually at least at the rate of inflation.

But I often wonder if I might be better off just selling everything, paying the taxes, and then putting it in something like VTI, and then just living on a fixed draw off of that. It seems like it would be simpler, definitely less work, and perhaps more likely to result in the highest long-term return.

If you don’t mind, I wonder how you think about these questions?

Hi M206

Thank you although I may not be popping the champagne corks yet. After this interview was written and submitted, one of the operators that I am invested with announced some rather extreme austerity measures, including pausing all distributions. I have some other real estate syndications that have circled the wagons and stopped distributions, so several sources of passive income have dried up. I’m still doing OK, but if I remove those investments from the overall picture (kind of a worst-case scenario: assuming a total loss), then net worth comes out to more like $3.3M. Still respectable, considering four years of expenses and a net worth still higher than on my retirement date, but not as stellar as it may seem.

And you bring up some great points: is the extra complication worth the effort? I’m a bit of a numbers geek, and I had the time and motivation to dig into a lot of these things, even automating wherever possible. However, the side-effect of all this is increased time spent tracking and managing these alternative investments, and particularly the tax complexity. K-1 forms usually arrive late, requiring extensions and resulting in final filings in May or June rather than April 15. Tax returns can run hundreds of pages long. I do my own taxes (yeah, probably another subject) and have come to realize how opaque the tax code really is. The pros get paid what they do for good reason.

While I’m not ready to completely swear off alternative investments, I will be simplifying as some of the existing investments exit, either through completion or bankruptcy, either of which could take a while.

You’re right, there is a psychological thing about covering expenses with cash flow income. Steady cash flow insulates you from the wild gyrations of the equities market but, as has happened lately, it is not guaranteed.

There is an attraction to keeping it really simple and just placing everything in something like VTI, however, even VTI lost nearly half its value in 2008/2009, so I will continue to seek some alternative investments.

I’m probably rambling a bit, but those are my thought processes. Thanks for asking.

Thanks for sharing! Your charitable giving comments excite me as my number 1 expenditure is giving for gospel ministry of evangelism, disciple-making, and helping the needy. It is also interesting how you developed and draw passive income.

Thanks for your comments. Dave Ramsey often says “live like no one else so later you can live and give like no one else”. Some people love Dave Ramsey, and some people don’t, but I think he is spot on with this one.

Thank you for sharing your journey. My husband and I will be retiring in the next year. Can you share where you found your volunteer opportunities in January and February with your RV? This is something I have had a hard time finding information about. Also do you travel with any RV groups? I appreciate your time.

Hi Mary,

Great question! We have a group of friends that we have caravanned with on occasion. We have gone camping with them for 35 years or so and we all have eventually migrated from tents to RVs. I have not sought out any RV groups, other than a Facebook group dedicated to our particular RV model. There’s probably one for just about any imaginable model out there.

As for volunteering, we are part of a faith-based organization called SOWERs, which has over a hundred projects going across North America at any time of the year. Some people do this full-time, we are more at the one or two projects per year level right now. We’ll spend three weeks on a project, and then another few weeks just wandering about, exploring the area (usually Texas or Florida in the Winter).

You can also volunteer at campgrounds, serving as a campground host. US Army Corps of Engineers manages some of this. Habitat for Humanity does building projects that RVers can participate in. Take a look at Volunteer.gov or just search the web for organizations, there seems to be plenty of them out there.

Well done fellow engineer! Enjoyed both your update and your original interview.

Chuckled as I realized we have both traveled similar journeys – maybe even the same cities. No desire for management here – nothing wrong with that – just realized I was not fit for it. As Dirty Harry said, “A man has to know his limitations.” Yes, the technical track can lead to FI.

Best wishes in your retirement!

Thanks for the comments and wishes. Always great to hear from a fellow engineer!