While deciding when to take Social Security (SS) is still some time off for me, it’s been on my mind recently.

While deciding when to take Social Security (SS) is still some time off for me, it’s been on my mind recently.

As I’ve been reading the Retirement Interviews it seems there are a disproportionate number of comments and thoughts around how the retirees address Social Security.

I’m interested in this as well because it’s 1) a complicated subject and 2) something I don’t know much about.

Then in the midst of my wondering about SS, a reader sent me his thoughts on the subject (unsolicited) in a few detailed emails. Add to this that I’ve been reading a couple books on it (highlighted below).

So, needless to say, it’s been on my mind.

In particular, I’ve been intrigued by the conventional wisdom around taking Social Security. As you might imagine, I’m not big on conventional wisdom when it comes to money, so I’ve been considering alternatives.

But I’m getting a bit ahead of myself. For now, let’s start with the basics…

The Social Security Rules

The rules for SS are vast and complicated, so we’ll deal with basics or this post will be 2,000 pages long.

Here are the highlights from the Social Security Administration (SSA):

You can start your Social Security retirement benefits as early as age 62, but the benefit amount you receive will be less than your full retirement benefit amount.

If you start your benefits early, they will be reduced based on the number of months you receive benefits before you reach your full retirement age. If your:

- full retirement age is 66, the reduction of your benefits at age 62 is 25 percent; at age 63, it is about 20 percent; at age 64, it is about 13.3 percent; and at age 65, it is about 6.7 percent.

- full retirement age is older than 66 (that is, you were born after 1954), you can still start your retirement benefits at 62 but the reduction in your benefit amount will be greater, up to a maximum of 30 percent at age 62 for people born in 1960 and later.

If you work after you start receiving benefits, we may withhold some of your benefits if you have excess earnings. However:

- we have a special rule that applies to earnings for one year. The special rule means we cannot withhold benefits for any whole month we consider you retired, regardless of your yearly earnings.

- after you reach full retirement age, we will recalculate your benefit amount to give you credit for any months in which you did not receive some benefit because of your earnings.

One term that we’ll use a bit in this post is full retirement age (FRA) and is detailed here:

It varies by when you were born, but the basic ideas are:

- If you retire at your FRA, you get 100% of your retirement benefits.

- If you retire before your FRA, you get less than 100% of your retirement benefits.

- If you retire after your FRA, you get more than 100% of your retirement benefits.

These are the basic choices we all have and the crux of what we’ll be discussing today — when is the best time to take Social Security?

The Best Time and Conventional Wisdom

Given the above, the choices are to take Social Security early, on time, or late.

For the purpose of this post I’ll define “early” as “as soon as possible” and late as “age 70”.

Given these options, which is best?

As with almost every personal finance question, the answer is “it depends.”

It depends on a whole host of factors that are unique to each person. That’s why this is one case (like taxes for me — when I use a CPA) when you might want to get some advice that takes into account your life circumstances, goals, etc.

But for today we’ll generalize and try to get an answer (or at least a close estimate) that works for most people.

That said, there is certainly a pretty standard answer of when to take Social Security by most, so much so that it qualifies as conventional wisdom.

I knew this was the case but to prove it to myself I went to Google and typed in:

“is it better to take social security early or later”

Here are some of the top responses by a who’s who of American financial entities…

From CNBC:

Financial advisors generally recommend that you hold off on claiming as long as you can. Admittedly, that can be a gamble.

“You’re always betting you’ll live longer and get more money,” said Geri Eisenman Pell, CEO of Pell Wealth Partners at Ameriprise Financial. “The government is asking us to make a calculated risk decision on something we’ve been mandated to pay into and take a risk on the back end.”

It only makes sense to put in for benefits early in limited circumstances, said John Piershale, wealth advisor at Piershale Financial Group.

“If you’re going to take it at 62, if you’re single and you’re terminally ill and you know you’re not going to live very long, then you might go ahead and file early,” Piershale said.

Most other situations don’t make sense to claim early and take that permanent reduction, according to Piershale. Say you know you won’t live a long time, for example. If you’re married, claiming early could lessen the amount of benefits your spouse will have access to once you’re gone.

From Schwab:

If you have a choice and are in good health, think seriously about waiting as long as you can to take your benefits (but no later than age 70).

For retirees in good health, a long retirement, coupled with uncertainty about markets and inflation, are the biggest risks. Delaying Social Security, if you can, is effectively an insurance policy against those challenges.

From Bankrate:

Optimum strategy: put it off. Generally, it’s best to postpone Social Security benefits at least until you reach full retirement age, which is determined by the Social Security Administration.

There are instances where taking early benefits pays off despite the reduced monthly check, Neiser says.

“No one can predict how long you’ll live, but if you’re facing a potentially significant reduction in life expectancy and are short of income, taking Social Security early may be appropriate,” he says.

From Fidelity:

If you claim Social Security at age 62, rather than waiting until your full retirement age (FRA), you can expect up to a 30% reduction in monthly benefits.

For every year you delay past your FRA up to age 70, you get an 8% increase in your benefit. So, if you can afford it, waiting could be the better option.

Health status, longevity, and retirement lifestyle are 3 variables that can play a role in your decision on when to claim your Social Security benefits.

BTW, Fidelity has this very slick widget that can help you decide what to do. I put in my assumptions and it told me to wait, with the difference in earning being almost $300k for waiting.

The Washington Post:

The conventional advice about when to take Social Security is try as hard as you can to wait. Don’t take it at 62, many experts say. If you can hold off, don’t even take it at your full retirement age. Delay until you’re 70, and you get more money every month. And since many people are living longer, the extra money might be needed, most likely to pay for health care expenses not covered by Medicare like long-term care assistance.

In Get What’s Yours: The Secrets to Maxing Out Your Social Security![]() they list the following as #1 in their “three general rules to maximize your lifetime benefits”:

they list the following as #1 in their “three general rules to maximize your lifetime benefits”:

Rule 1: Be patient. Take Social Security’s best deal by waiting to collect for as long as possible — taking much higher benefits over somewhat fewer years when it pays to do so.

In Your Complete Guide to a Successful & Secure Retirement![]() they say:

they say:

You can file for retirement benefits as early as age 62. However, there are significant reasons to wait.

I could go on and on, listing one name brand site after another recommending that it’s generally almost always best to delay taking Social Security for as long as possible.

But not everyone thinks that…

The Take It Early Camp

A few have broken ranks with convention wisdom and suggest that taking SS asap is the best option.

Back to The Washington Post piece noted above:

My husband and I are in a great debate about when to start collecting Social Security.

I want to delay getting benefits until we are 70. We both reach full retirement age at 67.

“Nope,” my husband says. “I’m going to take it early at 62. Why wait all those years when we could use the money to travel or do whatever we want during our healthier years?”

My husband did a spreadsheet and it showed that while delaying until 70 would net us more money every year, the break-even point — where we would catch up to all the cash we missed out collecting early at 62 — was about 79.

“Tomorrow isn’t promised,” he argues. “There’s no way to tell about our vitality at that age.”

Then there’s the Motley Fool:

At first blush, the extra amount that can be received by waiting to claim until 70 appears to make waiting the smartest decision. However, it’s important to remember that the amount that is paid out in benefits over a lifetime is calculated to be the same, regardless of what age you claim.

Therefore, delaying when you claim until 70 may produce bigger checks than claiming early, but it also results in the typical recipient collecting fewer checks in their lifetime than if they claimed early. Obviously, if you have longevity in your family tree, waiting could allow you to come out ahead, but assuming the average person’s life expectancy, collecting more, smaller checks might be best, especially if you can invest some of that money.

For example, the following chart shows the various break-even points associated with claiming at 62, 66, or 70 for someone who is set to receive $1,000 at their full retirement age of 66. Waiting until 70 doesn’t break even with claiming at age 62 until the recipient hits their late 70’s. If someone claims at 62 and invests some of their benefits, this break-even point could get pushed even further back.

Hmmm. Now this is getting interesting.

Take It Later…Or Early

The nice, short, informative book Social Security Made Simple![]() bridges the take it early versus take it late debate by offering the following general guidelines…first for taking it later:

bridges the take it early versus take it late debate by offering the following general guidelines…first for taking it later:

The longer you expect to live (or the more worried you are about running out of money if you do live to have a long retirement), the better it is to hold off on taking benefits.

They also offer this pertaining to married couples:

From a breakeven perspective, for it to be advantageous for the higher-earning spouse to delay his/her retirement benefit, only one spouse needs to make it to the breakeven point. As you can imagine, this often means that it’s a very good deal for the high-PIA (primary insurance amount) spouse to wait until age 70 to claim retirement benefits.

On the other hand, the book offers this as a potential case for claiming early:

The higher the after-inflation rate of return you can earn on your investments, the better it becomes to take Social Security early, so you do not have to spend down your portfolio as quickly. As a result, if inflation-adjusted interest rates are very high, you may be better off taking the money early.

The book notes that the total life expectancy at age 62 is 82 for a male and 84.8 for a female. This makes the breakeven investment return to take SS early between 1% and 3%.

Food for thought.

Take It at FRA

Not to be outdone, I was sent the following by Bob Johnson, an ESI Money reader, who suggests Social Security should be taken at FRA.

His thoughts:

Here is an idea to consider if you are still working as you approach full retirement age (FRA) for social security.

Take advantage of the loosened rule for earnings in your FRA!

Most of us still working as we approach FRA are doing so because we have to. We are not yet in a position to retire comfortably, and the earnings restrictions imposed on social security before FRA are draconian: for every $2 earned above $17,640 (in 2019), $1 of our social security benefit is reduced. So we keep working.

The rule changes for the better in the tear of FRA: For every $3 earned above $46,920 (in 2019), $1 of our social security benefit is reduced.

Most of the chatter on the internet implores us to delay our social security benefit for as long as possible, touting the extra 8% per year the benefit will increase. What these well-meaning bloggers fail to appreciate is that most of us are not in a position to deplete our savings for 3 – 4 years to gain an extra 24% – 32% in our ultimate social security payout. We are painfully aware that we will be receiving $0.00 in social security for that same 3 – 4 years.

These two stark choices are where the discussion ends on the internet. However, there is another strategy to consider. It works best for people in the following circumstances:

- Still employed

- Planning to work through FRA

- In a position to save extra money rather than spend it

- Eligible for a tax-sheltered savings plan (401(k) 403(b), 457, etc.) at work

While you are still working in your FRA before you reach your birthday, you are eligible to earn up to $46,920 (in 2019) without disturbing your social security eligibility.

Here is the idea:

- Start receiving social security in January of your FRA — This will involve a permanent reduction in your benefit of up to 6.1%

- Roll an amount equivalent to your monthly social security payment into your 401(k) program – You will be allowed to contribute up to $38,000 to your savings plan in your FRA year,

- Continue this through your birthday, or even beyond.

Most of us who are still working at this point need to make, spend and save the money we earn. An extra amount in our tax-sheltered savings account would be a meaningful boost to beginning retirement.

Internet blogs are usually disdainful of the practical monetary needs of retirees. It is a hardship for the average retiree to forego the average monthly social security benefit for any period of time. It is also difficult for the average retiree to accumulate any meaningful savings. This makes whatever savings a person is able to accumulate before retirement that much more important.

We are discussing a modest, rational trade-off: creating a savings account at the expense of a small percentage of the retiree’s monthly benefit.

Example:

So you have another choice to consider. It requires some active money management on your part – get used to having to do it!

Only you can decide whether to enhance your savings at the expense of social security cash flow. But now you know how to, if you so choose!

Good luck and best wishes for your retirement!

Getting Professional Thoughts

In addition to the research and thoughts above, I wanted to get some advice from people who deal with this question every day.

I happen to have two good blogger friends who are financial planners (don’t gasp!) and manage this issue quite a bit.

So I sent them a note asking them to contribute.

I asked them to send me the following:

- Your answer to the question “When is it the best time to take SS?” You can say “Early in this case but later in these cases” if you like, just don’t say “it depends and leave it there with no explanation — tell us what it depends on and how to decide.”

- Your thoughts on the concept of taking SS early, investing it, and letting it compound. Could this be as good as (or close to) waiting until much later to take it? Why or why not?

We’ll begin with thoughts from Fred Leamnson who writes at Money with a Purpose:

I’ve been a financial advisor for over thirty years. I work with people who are nearing or in retirement.

One of the things I help retirees with figure out is when and how to claim Social Security. It’s something too many people take lightly.

The best time to claim Social Security depends on many factors.

1. Marital status:

- If you’re married, you want to see if you qualify for spousal benefits. If you do, you should consider using it. A spousal benefit is ½ the primary workers PIA (primary insurance amount) if started at full retirement age (FRA). To qualify, the primary worker must have filed for benefits. The file and suspend option is no longer available. The spouse must be at least age 62. If he/she files before reaching FRA, a reduced benefit will apply. There are no delayed credits on spousal benefits.

- Divorced – If divorced, you may qualify to draw a spousal benefit (as described above) on your divorced spouse’s benefit. The same rules apply as on how to apply. Additional rules apply. You must have been married for ten years, or more, the spouse receiving the benefit must be unmarried, the ex-spouse must be at least age 62. If the divorce was longer than two years ago, the ex-spouse does not need to have applied for benefits.

2. Financial condition:

One of the most legitimate reasons for claiming Social Security early is out of financial need. Many people have to retire before they are ready due to their jobs getting eliminated, health, and many other reasons out of their control. In that case, claiming early may be the best option.

That said, you should still analyze your options, especially if you’re married. You may be eligible for spousal benefits. It may make sense for your spouse to apply and for you to wait. Don’t rush to make the decision. Look at all of the options first.

3. Life expectancy:

We are living longer than ever. When we’re planning for income in retirement, we should take that into consideration. My advice to clients is to always calculate living several years beyond what the life expectancy tables say. Why? It’s much easier to adjust income up than down. If we plan for a shorter life expectancy, set up an income based on that timeline and live longer, we may run out of money.

Healthcare expenses increase as we get older. Maximizing income so it lasts beyond what we expect allows us flexibility in our later years.

The Social Security claiming decision is an important part of the calculation. If we delay claiming until, say, age 70, our benefit increases by 8% each year. If our FRA is age 66 and our PIA is $2,000, waiting until age 70 increases our benefit to $2,640. The number does not include inflation. If inflation continues (which it historically always has) the benefit continues to increase every year with inflation.

Social Security is one of the few guaranteed income sources that keeps pace with inflation. The extra potential income that comes from delayed filing can tens of thousands of dollars of additional income during your lifetime.

Claiming Early

The idea of claiming early and investing the difference is popular. It can make sense of one has the discipline to invest the money, rather than spend it. In my experience, most people do the latter. I have retired friends who claimed early to do just that. They’re wealthy, living off their pensions (in some cases) and retirement assets. They viewed their Social Security as extra spending money.

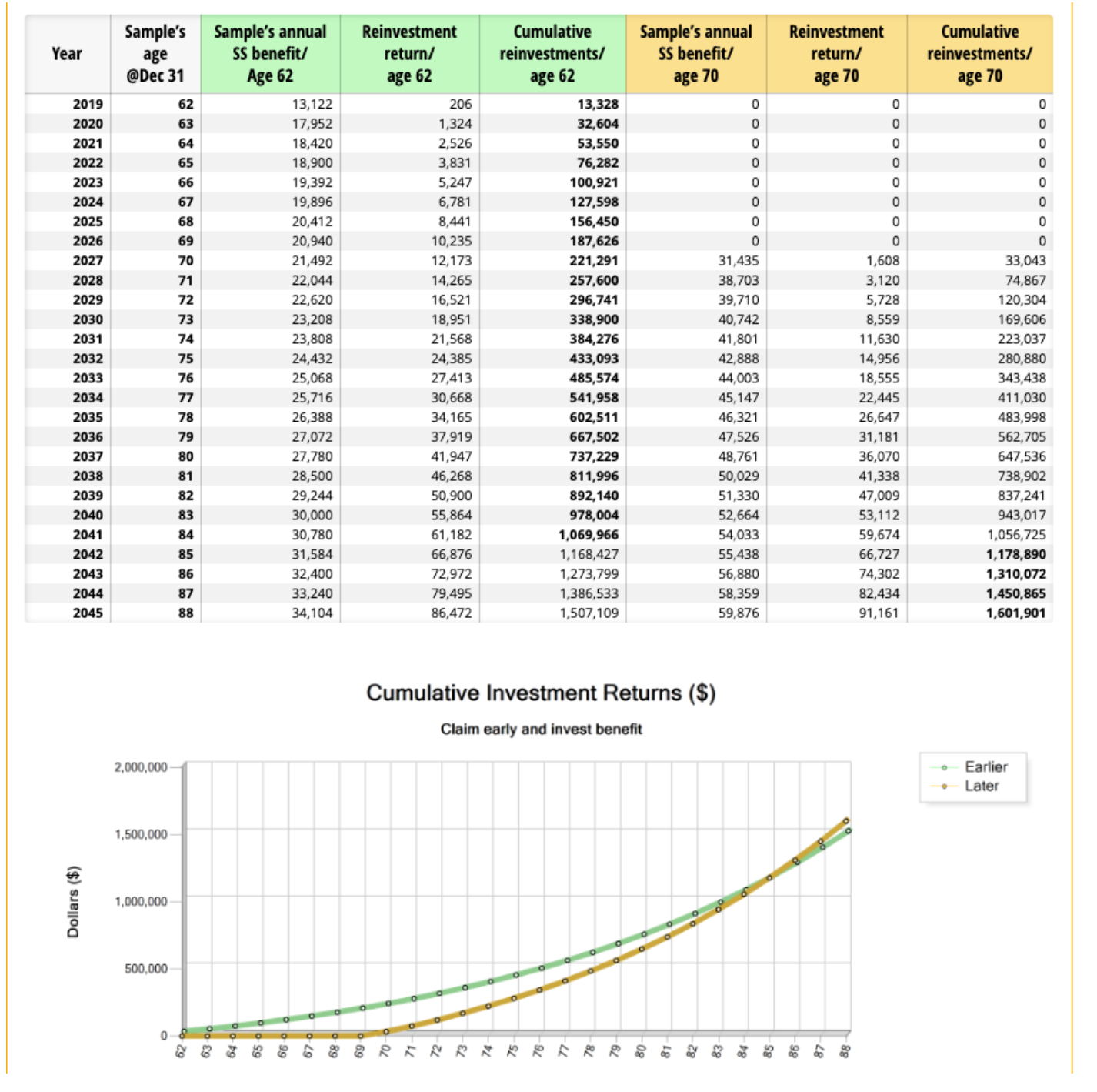

To calculate whether it makes sense to claim early and invest we need to find the breakeven point where one has advantages over the other. I’ve run an analysis to offer an example.

Here are the assumptions:

- DOB: 02/10/1957 (age 62)

- FRA: Age 66 + 6 mos.

- PIA: $2,000

- Life Expectancy: Age 95

- Investment return: 6.00% (nominal)

- Inflation: 2.6%

Below is a chart showing the numbers:

You can see from the chart the breakeven point is age 84. Living beyond that means waiting to claim is better.

If the investment return is 4%, the breakeven point is age 81. A 6% return extends that to age 91.

There are a lot of variables to consider. Life expectancy, rate of return, and risk are the top three. If you are a disciplined saver and investor, claiming early and investing may make sense.

If you are a more conservative person who likes the sure thing, waiting to claim may be a better decision.

When claiming, people want to look for a simple answer. Like most things relating to financial planning, there is rarely a simple answer. I hope you can see from this discussion whey it’s so important to carefully analyze the claiming decision.

——————–

The second response is from Michael Dinich who writes at Your Money Geek:

I have worked in the financial services industry for the last 20 years where I assisted clients with their retirement planning. We would often discuss with clients, the best pensions options for their situation, the timing of electing social security benefits, and estate planning.

Currently, I hold a certificate with the NSSA (National Social Security Association) and have conducted workshops on social security benefits throughout the southern tier of New York and Northeast PA. In the last 20 years, I have attended numerous training sessions regarding social security benefits as part of my professional continuing education requirements.

I’m not trying to suggest I am the leading expert in social security benefits or dazzle you with my resume, but I have trained under the leading experts for numerous hours each year and have the t-shirt to show for it. Instead, I am sharing this to provide some background into my experience and the ultimate truth I have realized. The financial services industry and the financial media does not want you to take your social security benefits early.

Every course, book, lecture, seminar, etc., I have attended has always led the audience to one conclusion, you are supposed to wait until age 70 to take your benefits.

Now, since you are a reader of ESI Money and astute with your money, you can probably think of one, and more like a few dozen ways it may make sense to take benefits early.

I can relate.

I was a young advisor steeped in the libertarian counter culture of Gen X had the exact feelings you probably have upon hearing you must wait. What about if you take the money early and invest, or similarly what if you claim benefits early and delay withdrawing your own funds? “Surely, you can beat the growth of delaying benefits!!!”– I would protest, as my broker dealer’s compliance person starred at me sternly willing me to drop the issue.

The more analytical will point out that the math suggests you will receive more money from social security by waiting until your 70 years old and then living a long time. None of the social security maximization calculations ever consider the time value of money, the opportunity cost of investing the money or the cost of consuming your assets to facilitate delaying social security benefits.

Once we consider that decisions concerning social security do not happen in a vacuum, the situation becomes complex. This is exactly the type of case the financial services industry and media should be helping you navigate. However, the response is usually the same, wait until age seventy if you want the most money.

The reality is it’s not an issue of mathematics or economics; illustrations can be run to show almost any scenario in a favorable light. However, all we can do is forecast; we don’t know what your longevity will be, how the markets will perform, or what the rate of inflation will be. We don’t even know what future benefits will look like; how will benefits be taxed in the future, how will cost of living increases (if any) be calculated?

The truth is it is an issue of liability; the fear is if a journalist or advisor talks you into claiming early benefits and you lose all of your money in the markets then you will sue them. I wish there were more to it than that, but at the end of the day it boils down to liability.

If you delay taking your benefits until age 70, and then the government increases taxes, implements means testing, or you fail to live your actuarial life expectancy, you can’t blame the author of a book, blogger, or financial advisor. Well, hopefully, you can’t, because who could have possibly predicted any of that happening?

The industry’s stance regarding claiming benefits early is “caveat emptor” (buyer beware). If you want to take your benefits early, you won’t be doing it with the blessing of the industry, and you will be expected to bear the consequences of getting it wrong.

I have run thousands of fancy detailed reports showing clients the differences in claiming benefits early and delaying, and overwhelming clients have chosen to claim early. Many times, clients claim early despite overwhelming data that suggests they should wait. The two most cited reasons clients tell me they are choosing to take benefits early:

- They don’t believe they will live as long as the projections suggest.

- They don’t trust the Government won’t alter the programs to their detriment.

Most of the families I have met with cite non-economic reasoning for choosing when to elect to receive payments. As much as we like to be rational, most people make decisions for emotional reasons and then try to justify their decision math. There is nothing wrong with deciding for psychological reasons; you need to be prepared to be responsible for the result.

If taking your social security benefits early and investing the money make you happy, go ahead and claim your benefits early. However, if anyone asks, you didn’t hear it from me. 😉

My Thoughts

I haven’t run the numbers for our family yet or thought deeply about all the issues as we’re a ways off from a decision and I have time.

But I have some preliminary thoughts to share with you.

Overall, I’m currently leaning towards taking SS early, but as you’ll see I’m going a bit back and forth. Here are my general thoughts on the issue to date:

1. I don’t really need the money.

When you take the financial issues out of when to claim SS, it makes things a lot simpler.

We have more than enough to live on throughout our lives, so SS is just a bonus for us. In fact, when I began blogging in 2005 I used to say things like, “I’m counting on zero from Social Security.” And that’s what I planned for.

That said, I do want to get a “good deal”. I paid in the maximum to the SSA for most of my working years and would like to be compensated for that.

But whatever I do, it’s not going to make a material difference in my finances.

2. I can invest the amount and earn more.

Since I don’t need the money, I can take whatever I get, invest it, and watch it grow.

Of course no one knows what the markets will do, but with even a fair assumption of return rates (as noted above), I would be able to push the breakeven well into my 80’s.

As for the “discipline” issue noted above, I think I’d have the discipline to invest (versus spend) it if that’s what I decide to do.

3. I’d rather be in charge of my money.

I’m not a big fan of the government managing my money, so I’d rather be in control of it sooner rather than later.

In addition, it’s clear that something will eventually need to be done about the liquidity of SS and this likely means reduced benefits and/or higher taxes on those of us with higher incomes in retirement.

This leads me to think getting as much as I can as soon as I can is a good idea.

4. There’s something to be said for having more money when you’re younger and able to enjoy it.

Even if I blow the money completely with an extra extravagant vacation each year, I’d rather do that when I’m 62 than when I’m 82.

Who knows what shape I’ll be in later in life — no one knows.

As one person said above, tomorrow is not promised.

5. I think the averages say it doesn’t matter when you take it — it all works out to be the same amount.

We heard this above, but let’s go back to Your Complete Guide to a Successful & Secure Retirement![]() where they say:

where they say:

It is actuarially true that if you live to average life expectancy, taking benefits at any age should provide roughly the same cumulative amount of benefits.

There. That takes the pressure off a bit, doesn’t it? 😉

6. I am the high earner, so I should be careful about taking SS early.

Especially since my wife eats so well she’ll probably live to 120!

And since only one of us needs to live a normal lifespan to make delaying worth it, this tilts the scale towards waiting.

7. I will need to investigate strategies for my wife and I working together to maximize our benefits.

It may be she can claim early (or at least at FRA) on either her benefit or spousal benefits while I wait.

As I noted above, we will need help figuring this out.

In the end, there are so many uncertainties (life expectancy, tax rates, income and RMDs, future benefits of SS, investment return rates, etc.) that it’s almost impossible to make the “best” decision. We each need to factor in our own circumstances and plans, make a decision, then hope the uncertainties don’t stack up against us to make our decision the worst possible outcome.

Then again, if you don’t need the money and consider even one penny of it a bonus, then the worst possible outcome is way better than you expected/need. 😉

Anyway, those are my thoughts on the issue. What’s your take?

Excellent breakdown.

Where I really think SS calculators/advisors/analysis needs improvement (particularly with younger generations) is in regards to two working spouse couples and strategies, particularly if one/both are relatively high earners and thus likely to get nearly a top SS payout.

I’m a high earner (at least so far – knock on wood). Wife is less of a high earner, but certainly makes a very good salary and has done so for a number of years. Wife probably has longer life span on her side given family history than I do (my dad died at 76, my mom has serious self-lifestyle inflicted health problems at 67; wife’s grandparents all made it into their 90s and two are still alive in 90s and her parents are both 70 and doing well other than back/knee issues).

My thought is I should almost certainly wait until 70, just because that gives my wife the option to switch to my (likely higher) benefit when I (probably) die before she does. But when does she claim? And should I just claim at FRA if family history says I might die pre-80 (although, I do think I take better care of myself than my parents/grandparents)?

It’s all hard, and probably the best bet is to run a ton of scenarios when we get closer to retirement/FIRE and decide what makes the most sense.

Yep. We’re going to run a gazillion different options when we get to that point. There are just so many variables that it becomes quite complicated.

Eye opening discussions, decision’s, revisions, and doubts abound. As a disabled veteran, retired military on a small pension, taking SS early was a no-brainer. Learned to live within our means, and managed to save over 30% of SS for the last 16 years. Am now a widower, and live comfortably. Personal financial decisions often come with risks. Weigh those and whatever decisions you make are yours to keep. This was worth reading and hopefully good advice to some who are not certain about their future financial situation.

“Personal financial decisions often come with risks. Weigh those and whatever decisions you make are yours to keep.”

GREAT advice!

Really outstanding post John and one that makes you really think through the options.

It is true that convention says waiting till 70 is the preferred method because of the 8%/yr increase for every year above FRA. And honestly I was probably leaning along that line of reasoning until I read this post.

Now I have to give it a bit more thought. I am in a similar position as you are in that I likely will not need SS and see it as a bonus payment (I also calculate it as if I am not getting anything in my current FIRE plans). The fact that who knows what will happen to benefits also makes it tilt towards early claiming if you can (bird in hand philosophy).

I read so many articles saying the exact year I turn 62 the reserve fund will be depleted. I think I will take at 62 for multiple reasons. The depleted part means in theory the fund will have issues paying 100% of what I should anyway, so I’m already likely going to receive less than our statements say.

That said my largest concerns are RMD’s and wealth preservation. If I wait till 70 than I would be spending money I have already saved minimally from 62-70. I would be spending down my retirement capital for just a chance that I may do better if I live past 85 ? No thanks. If I pass before 85, my kids win a large inheritance. If I live past 85, based on the investment returns of 23 years (85-62) I like my chances more than if I waited. I think waiting until 70 when you add on RMD’s at 70.5 or 72 if this new legislation passes, could become a problem for many good savers.

Some good points to consider…thanks for pointing them out.

TL;DR

1. SS will never be eliminated.

2. SS benefits will never be reduced for the vast majority of current AND FUTURE beneficiaries.

3. SS may one day get means tested for the highest earners.

Too many people worry about social security “going broke” or getting drastically reduced benefits for all recipients (like the common threat about it only bringing in enough money by 2033 to pay out 73% of benefits – This is currently true but irrelevant. Congress will raise taxes, print money, increase debt, allocate from the general fund, etc). This apocalypse has been predicted for almost 2 decades now and the whole time I have advised people all the exact same. Namely, this is never going to happen. SS benefits will never be reduced (probably be increased) for everyone except possibly the most affluent.

If you have plenty of means to take care of yourself without SS, then it is very possible that one day it will get means tested and you may get less or nothing. For everyone else there is zero chance the benefits will be reduced by a single dollar. It is political suicide and no majority will ever vote for it. Republicans have been threatening to lower SS benefits for decades. They have had complete control of all branches many times during those years. They never once even brought the topic up for a vote after all their talk because if they did anyone who voted for it would lose their seat.

If they means test it, it is less likely they will change the benefit for someone who has already started drawing. So that may be an argument for drawing early. However if legislation is ever brought up to means test it you can likely get in front of it and start your draw before it passes.

SS is the most popular govt program in existence. It cannot be touched for 95% of the voting base.

See here for one candidate’s current plan just out today to raise taxes and expand SS.

https://www.cnbc.com/2019/07/29/how-joe-biden-plans-to-increase-americas-social-security-benefits.html

This won’t happen yet but the cry is building. I expect something like this to eventually happen. Taxes go up (on the wealthy, or everyone, or who knows), benefits go up at least for those on the bottom of the SS scale, and more votes are purchased.

There is no viable politcal path to go the other way.

How can we keep paying for this stuff? Not nearly enough people care. They will run the country into the ground to pay for it before they ever touch SS benefits.

It is complicated but most people are better off to delay until 70. Take earlier only of you need the money and have a short life expectancy.

My situation:

1. I’m truly FI – I can live on my cashflow from pensions, dividends, interest, rental income and my wife’s SS. No need to tap my IRA or non-qualified investments so let those investments grow.

2. My wife took SS at 66 (FRA), and when I turned 66, took ½ of her SS. I’m currently 69.

3. I keep my Taxable Income just below $78950. That way my $30000 in long term non IRA dividends are tax tree. Worth $4500 (15% of $30000) annually. Claiming SS would negate that opportunity.

4. If I took SS earlier than 70 then I would be in a higher tax bracket. Why do that earlier than I need too. So staying in 12% bracket instead of 22% on incremental income if I had to take SS.

5. Waiting till 70 earns 8% more per year for 4 years, plus the annual inflation increases.

6. If I predecease my wife, she would then get my higher stepped up SS.

7. I expect to live well past 80.

8. In March 2020 I will start my SS at age 70.

M22

So starting at 70 you will be in the 22% bracket or more from here on right? Especially when RMDs kick in too.

Chris – Yes. With or without SS I will be in the 22% bracket when RMD’s kick in . But only 85% of my higher SS will be taxed, and some of that (small amount) will be in the 12% bracket.

This is a great post to highlight the complex decisions all Americans are being asked to make. Bottom line, there are no simple answers. However, I have a high degree of confidence that people who are active on this site will be okay. For us, this is a good intellectual exercise. But, as we all know, a lot of people (most?) have their head in the sand when it comes to anything financial. Seems like another crazy burden to put on people.

So true. We are at least aware of how complicated it is and are trying to make rational decisions based on what we know. Many Americans have no clue about SS (like most other financial decisions) and probably give it very little thought before deciding one way or the other.

If “we are aware” and still can’t agree which is best I’m guessing it won’t matter much to everyone else. Maybe it will…

What burns my A$$ is that it always feels like the more you ‘contribute’ to gov’t the less you are likely to ever get back. I contribute the max per year to SS (and have for a long time) and yet if I’ve done well on my my own- I’ll likely just pay more taxes on it or receive less.

Pathetic that I’ll likely have to hire a tax attorney to help figure this out.

If you take SS early and use the money for your daily living, this would help grow your investments that you have already built up. It is not necessarily about investing the SS money that you are getting every month.

Let’s say you get $2000/month of SS, that is $2000 less you have to take out of your investments(assets) that you have been building up for the last 30-40 years. The investments would continue to grow with compounding gains and dividends.

So at 61, you were taking $70,000/ year out of your assets. At 62, you claim SS early. You receive $24,000 from SS, now you only take out $46,000 from your assets. You didn’t have to take out the $24,000 from your assets that has been compounding for years.

This is assuming you are disciplined to do this and not increase your spending.

I didn’t see this thought in the article, but I may have missed it. Also, it could just be a crazy idea.

I like it. Worth thinking about for sure…

I’ve spent a lot of time on this subject, and appreciate this post. Here are a couple of related resources ESI readers may find of interest…

Taxation of Social Security Benefits This will be handy for those who have a substantial IRA balance to drawdown. Delaying S.S. and IRA Required Minimum Distributions will push more income into higher brackets in later years. At this time, 85% of Social Security is taxable at Federal rates, above $44K for married couples. As ESI’s post states, “…decisions concerning social security do not happen in a vacuum.” Realizing income in lower amounts over more years allows maximum after-tax retention.

S.S. calculator for Present Value, and married strategies Came across this recently, and it is a revelation. In the course of working with my parents’ estate, I see how this calculator can be valuable for forward-thinking personal finance with regard to both Cashflow and Net Worth.

So what’s the right answer? 😉

Ummm…”that’s not in my purview!”

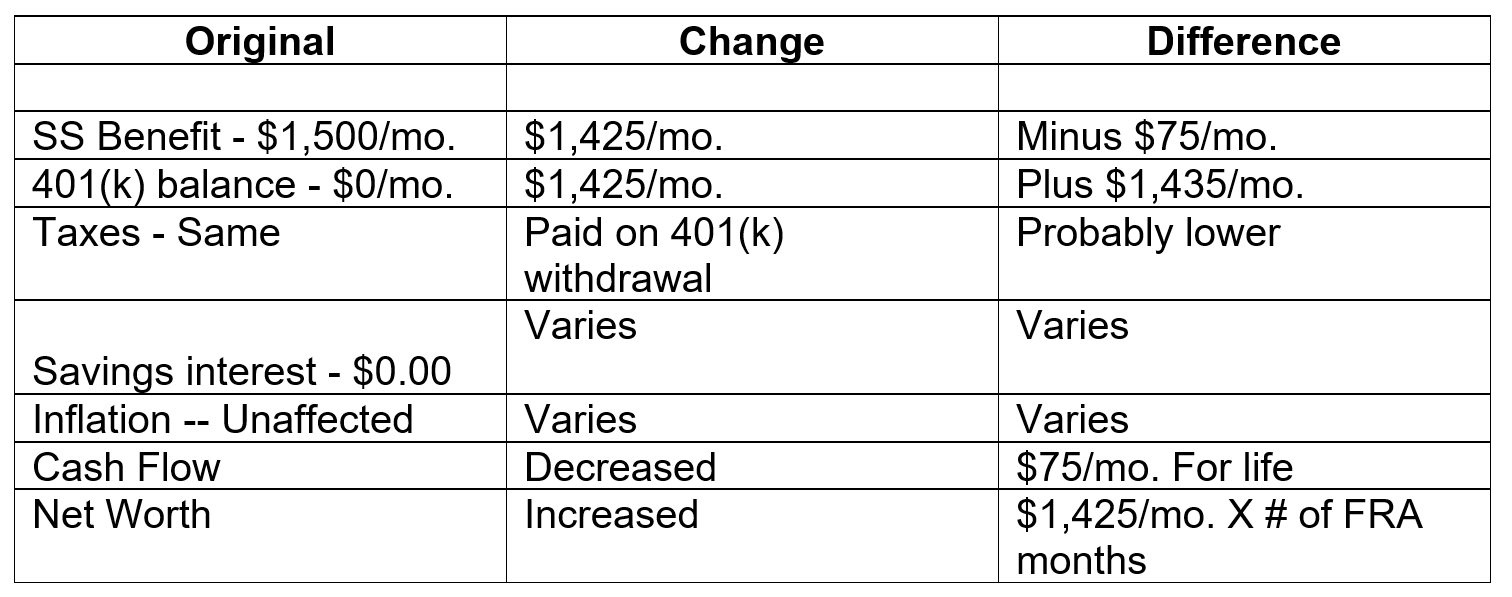

A few years ago I helped my mother with this question. In her case, she was trying to decide between taking the benefit now vs a year from now. If she took it now, it was $1500/mo. A year from now it would be $1600/mo.

I realized a reframing of the question was in order. Let’s just consider the $1500/mo starting now as a given. The first option means doing nothing. The second option is equivalent to taking that $1500/mo and using it to purchase an annuity which would yield $100/mo starting in one year.

So the question became, was this an annuity you would be interested in buying? IIRC, it took a long time before the annuity was worth it.

In any case, hopefully this reframing of the question is helpful.

Very nice thought process IMO.

ESI, I’m surprised you’re leaning towards taking SS early as you have plenty of after tax capital you can “safely” spend down until age 70. As you noted, most “experts” cite an overall better payout statistically by waiting until 70 for those in good health. Since you are taking care of yourself, you are positioning yourself to live a long life. If you do die prematurely, then you heirs get a little less. Is that an issue?

I’m in a similar situation and am strongly inclined to wait. Seems pretty clear/easy for me. If we die early, my kids get less but I’m OK with that.

At this point I’m just thinking out loud. I like challenging conventional wisdom at least to see if it’s “conventional” for a reason. As noted above, there are enough people on the “take it early” side to at least warrant a deeper discussion.

In the end, we’ll probably do a very deep dive with an advisor and see what he/she thinks. That’s still a ways off.

That said, I will be talking to my CPA later this year about planning for RMD’s and will throw in a few questions about SS to see what she thinks.

I’ll be 65 in March 2020 —- my wife will be 63 in August 2020 (she plans to retire) —- we’ve talked and talked about this very issue for years.

Final decision and behind door number 2 :

Drum Roll. 🥁

We plan to WAIT to age 70.

Yes.

For those with good sized pre-tax investments, another consideration for delaying SS is extending the time to rollover those investments into Roth IRAs at a lower tax bracket between 62 and FRA or 70. This assumes you have taxable accounts/pension or other that covers living expenses.

My husband and I both retired early 7 and 6 years ago, respectively. We both discussed whether to take our SS early or wait. Our decision rested on a factor we considered which I haven’t seen in your discussion…hopefully leaving an inheritance for our sons. Not knowing what their financial future may hold, we wanted to make sure they didn’t struggle in retirement. While we have some significant savings and could have waited to take our SS benefits, we figured by waiting, we’d be burning through a chunk of our money first with no guarantee we’d even be alive to collect SS at FRA or even 70. While we both are in good health, that doesn’t always guarantee a long life. Since we did not want to take out Long Term Insurance, we also needed to reserve our savings to cover a nursing home for one or both if needed. Therefore, we decided to spend some of our savings when we first retired and take our SS each at age 63. With our monthly SS benefits and a small pension each, we live pretty frugally and have been able to manage our expenses without having to touch our investments. That’s what we thought was best for us on when to take Social Security.

Looking for good sources for running the calculations when there is a wider age difference between spouses. My wife and I are 10 years apart so trying to evaluate what will be the right claiming strategy – we are still several years away from claiming. I put some basic info into the open social security calculator and it advised to have the younger person claim at 62 and the older person claim at 70. Thoughts?

I’m guessing that the older person has the larger SSI at full retirement and this is why the calculator picked 70 for the older person and 62 for the younger. The reason is that the younger person is more likely to outlive the older person and will be able to (upon their spouse’s death) collect the older person’s larger SSI (their SSI at FRA). There is no reason for the younger person to defer collecting to get a higher amount on their own since the younger will most likely eventually be collecting the spouse’s larger SSI anyway.

What the calculator doesn’t know is that by taking a discount at 62, the same discount will also apply to the older spouse’s SSI that the younger spouse would get upon their death. So I think the optimal solution is actually for the younger spouse to wait until FRA (Full Retirement Age) to collect.

MI 60,

This is exactly the scenario I have been trying to nail down for years and cannot find a definitive source. Do you have a reference for the statement above?

Namely if it doesn’t reduce survivor benefits my plan has always been to have my spouse draw early (her benefit is probably about half of mine) and then I delay to FRA or 70 and then she switches to taking 1/2 of mine as a spousal benefit with the presumption she would get my full benefit when I kick the bucket. I have been leery that this is too good to be true and I think I have heard some thing about it causing some reductions but again have never found any source that said one way or the other.

Here is an example of what I would plan to do if there is no future reduction.

1. age 62 my wife draws her early benefit which will be say $,1000 per month. (she is 7 months older than me).

2. At age 70 I draw my extended 124% benefit which will be say $4,000 per month.

3. She switches to draw 50% spousal benefits at that time or $2,000 per month.

4. Thus we have a total combined draw of $6,000 per month at that time.

5. At some future age (I am loath to put an actual number on it. 🙂 I die.

She then switches to my full benefit as a survivor benefit of $4,000.

For someone with a high earner and a moderate earner of similar age (within a few years) I consider this to be the best draw option.

However as you seem to state above the downside would be that in step 5 above when she switches to my full benefit you are saying she would not get my full benefit but would get a reduced benefit based on what my benefit would have been at age 62 which would probably be about half of the $4000.

As I said I am leery that there might be a catch in my plan but this would seem a bit odd that she could draw 50% spousal benefit off my full benefit while I am alive but then would get reduced to my age 62 early draw benefits if I were to die.

So all of that is to say I would really like to find a source that would nail this down for sure. So if you have a source for your statement could you please share a link to it. If not how did you come to that understanding.

Thanks!

Her own benefit, her spousal benefit and her survivor benefit are all different animals.

1. She can take her own benefit at 62 with the stated reductions.

2. Her spousal benefit will never be more than 50% of your FRA benefit (no credit given your your delayed credits) and will only be 50% of your FRA benefit if she claims when she reaches FRA and you have reached FRA and filed.

3. Her survivor benefit at her FRA or above will be equal to benefit you would have received or were receiving at your death.

Thanks Wilkop,

This is the first I have heard of spousal benefits being limited to 50% of FRA benefit, thus not getting any spousal benefits for the extra delayed credits. And also that drawing her benefits early would then also limit spousal benefits even more. I was able to verify that is in fact true. So thanks for pointing that out.

I had also been able to find information that taking benefits early did not reduce survivor benefits just as you said in item 3 above.

Thus the plan I laid out above does not work, not because it reduces survivor benefits but because it reduces spousal benefits. It actually makes good sense as that is how it should be done from an actuarial stand point.

However, given that she cannot participate in the delayed credits after my FRA for her spousal benefits, that reduces the benefit to waiting to age 70.

I will certainly need to give it more thought, but FRA is starting to look pretty attractive.

This is likely the plan we’ll end up with:

1. Wife taking her SS at 62

2. Wife switching to 50% of my FRA at FRA

3. Me taking SS at 70.

One caveat to be aware: wife can only take that 50% spousal benefit, AFTER the husband officially starts SS (anytime between 62 and 70)

That’s going to be a complicating factor — she’s 3 years older than I am.

Ugh. Back to the drawing board. 🙂

My wife is 5 years older than me, so aware of the rules. If she takes earlier than 66 (FRA), then that reduction in benefits would also apply to any future spousal benefits. My recommendation is she take at 66 and you at 70, and then she apply for spousal benefits if higher than her benefit on your 70th. If you predecease her she would then get your 70 benefit.

Along these lines also be aware that if you wait until 70 to start your draw, she cannot start her spousal benefit until she is 73, and she will not get 50% of your age 70 benefits, she will only get 50% of your FRA benefit which is the benefit you would have gotten at age 67. So in that case you would get 124% of your FRA benefit but she would only get 50% of your FRA benefit, not 62%.

Given that she would have to wait until 73 to draw the spousal benefit if you wait until 70 and that her spousal benefit will not go up at all during those extra three years, my suspicion is that the best course would be for you to draw at FRA so she can switch to her max benefit at that time rather than waiting for 3 more years to get that money when the 3 years won’t increase her draw at all.

That’s the way I am now leaning after what I learned here from Wilkop. Obviously it will take more analysis but that is seeming like one of the better options at this time.

Also be aware that as Wilkop pointed out, if your wife draws at 62 then she will get a reduced portion of her spousal benefit. She can only get 50% of your FRA benefit if she waits until her FRA to start her draw. If she draws at 62 she will only be able to draw 32.5% of your FRA benefit as a spousal benefit regardless of when you start your benefits.

Given your wife is 3 years older, an option to consider instead would be for her to wait until her FRA and start her draw, then three years later when you reach FRA and start your draw then she can switch to 50% of your FRA draw.

As I am now understanding, when one starts a draw at 62 it reduces everything that person does from there on (except survivor benefits). Drawing at 62 comes with serious penalties it would seem.

Since she is 3 years older you may decide that getting her benefit for longer is worth her only get 32.5% of your spousal benefit, but that is a calculation you will have to make being aware that she will not get 50% spousal benefit if she draws her benefit early.

Yep, I think this is sounding like the right course.

Dave and Apex

I am not sure where I read the article that gave the SSI collection strategy I wrote about (I’ve read a lot of them), but I know it is a common theme and it affects me too. I tried to find the rule about “if taking a discount at 62, the same discount will also apply to the older spouse’s SSI that the younger spouse would get upon their death” and looked at social security web page and I can’t find such a rule – so I must have got that wrong. Sorry about that. I even see ESI chiming in that his wife will be taking SSI at 62.

This interesting discussion affects how my wife and I will be filing – she just turned 62 and I am 67. Our situation is complicated by the fact that we have a disabled son. He gets SSI right now and is eligible for a larger SSI amount and Medicare (he already is on Medicaid) once one of us files for SSI. Now I am thinking that she should file right away based on her income history and I will wait until I am 70. There is also a family maximum SSI (per account) that we would bump up against if we do too much SSI claiming based on my earnings.

We’ve already had a couple of visits to the social security office to try and get things ironed out and all our questions answered. They are very helpful with questions but are also careful not to give advice.

Hi MI 60,

Thanks for the response. I think with the other people responding here we have nailed down the rules.

Namely, if your spouse draws early at 62 that would reduce her spousal benefit that she would draw off of your FRA SS. Namely instead of being able to draw 50% of your FRA amount she would only be able to draw 32.5% of your FRA amount (that might be a slightly different number given that you were both born before 1960). However she would always be able to draw your full amount as a survivor benefit regardless of when she starts her draw.

So the drawback to an early draw for her is if she would get a much bigger draw in spousal benefit based off of your earnings then that number will get much smaller if she draws early. However if you would bump up against the family cap that would change things too.

That is what throws the wrench in having the lower earning spouse draw early because it will reduce her spousal benefit, but not her survivor benefit.

One observation for couples with a lower earning spouse is the benefit of deferral of 8% per year is only from your early retirement age to your full retirement age. The benefit rate declines to 5% per year between your full retirement age and 70. A good compromise could be to take SSI at your FRA and have the lower PIA spouse take it early.

The real question is how much does the value of money decline as you get older. This is a personal question everyone need to answer based upon their specific circumstances.

Unfortunately this is incorrect information. It’s actually exactly backwards.

It is actually from age 62 to FRA that we only get 5% increases. After FRA then we get 8% increases up to age 70. For those of us born after 1960 we can only get to 124% of the benefit. Those born before 1955 can get to 132% of max benefit because they have 4 years after FRA while we only have 3 before age 70.

See here for details from the ssa.gov site.

https://www.ssa.gov/planners/retire/1960-delay.html

https://www.ssa.gov/planners/retire/1943-delay.html

https://www.ssa.gov/oact/ProgData/ar_drc.html

My comment was in the situation where you spouse gets a portion of your benefit (i.e. the spousal benefit is greater than your spouses PIA). When I looked at the tables, if I took SS at 62, I receive 70% of PIA & my spouse gets 32.5% (I was born in 1964). At FRA, I get 100% & my spouse 50% and at 70, I get 124% but she still gets 50%. So the growth from 102.5% to 150% over 5 years is 7.9% per year and the growth from 150% to 174% is 5% over 3 years. Numbers will vary depending upon your circumstance, especially if your spouse can take benefits in excess of spousal portion of your benefit.

Packer

You did say couple above, but I didn’t know the part about spouses being limited to 50% FRA for their spousal draw so looking at the percentage charts it shows the opposite.

However your point is exactly valid when considering that the spousal benefit is reduced so drastically to 32.5% when drawing early and is then not increased past 50% of FRA when the spouse waits until age 70 to increase their draw. This changes all the math when looking at it from the stand point of the increase in draw for the couple versus just the increase for one person.

Thanks for explaining what you were referring to and pointing out those differences. It certainly changes the math and your point is very valid. The total draw for a couple increases more considerably from age 62-67 than it does from age 67-70.

Very fortuitous to happen upon this great article today. Have been mulling this over for a few years, as the OCD planner, yet worrier in me, keeps soaking up information like a sponge.

Divorced, still single. Contributed for years into SS, but was unaware until too late of the ‘substantial’ income requirement. Taught for 23 years, so have Public Employees Retirement Assoc for retirement income. Despite working 2 jobs ( teaching and not contributing to SS but just PERA) as well as SS jobs, there is a windfall provision which greatly reduces the amount I am eligible to receive from SS, as they consider it double dipping. Not quite sure how that works since I was working 2 jobs, and paying into SS….but no matter. It won’t be changing. My parents are both nearing their 90’s and in great health, still active. I am also working full time at a SS job I have been at FT since 2011, and retired from teaching 2 years ago. Income taxes are killing mess I am making too much money. Unfortunately I have been helping my 3 adult children and their families get on their feet and paying off student loans, as the economy is much more difficult currently. I am not really concerned about income once I have no debt, however, I certainly want to make the most advantageous choices I can. I appreciate your analysis and many of those generally neglected aspects had been floating around in my head, too. It may be a few years or could be tomorrow, when I have to suddenly make a decision to move out of state, quitting my job, selling my home to take care of my parents. Current information is always very helpful. Ya just never know! I subscribed to your emails and look forward to more insights. Thanks again!

Here’s my thumbnail analysis for what it’s worth.

In the discussions for deferring the collection of SSI until 70 I rarely see what I think is the real reason for deferring – which is insurance against the possibility of outliving your money. According to Social Security, the amounts you receive at any age you start collecting are “actuarially equivalent”. That means that on the average it shouldn’t make any difference when you start taking Social Security – you’ll get the same total amount. That also implies that for wealthy people who have no chance of ever outliving their money the “age to collect” decision is (mostly) unimportant. I prefer to defer (as some others mentioned they are doing) in order to convert more of my traditional IRA to Roth in hopes of lower taxes on my SSI.

For most people, the possibility of outliving their money is very real and deferral until 70 (or as much as they can) will go a long way to insure against that possibility. Running out of money means you depend completely on Medicaid for you health care and long-term care. If you are worried about future Social Security funding, I would be 10 times more worried about future Medicaid funding when the baby boomers start running out of money in retirement.

I agree with everything stated here by MI 60.

Namely:

1. for people with enough money, it doesn’t make very much difference.

2. for people without much money, deferring to any extent they possibly can is their best protection for the future. They are the ones for whom it is most important to defer.

One other point I will add: I have discussed this topic with many people who don’t have much and will really need the money to carry them into old age but worry about dying too early and missing out on “$$$ all that money $$$” Can you see the greed swimming around in their head? They are not thinking about their future. They are thinking I want “my money” darn it and I am going to be dang sure the govt gives my my share before I kick the bucket. I always tell them the same thing (which never works by the way because logic is factual, greed is an emotion. Emotion kicks facts butt every single time!!!)

Here is what I tell them (I am still hoping for one person who truly understands this).

1. If you live a long time, the extra money you get will be critical in giving you a decent life during that time.

2. If you die early, you will miss out on some money, but guess what, you will be dead so you won’t be able to care.

As I said, it is not convincing to them, because they are going to get their dang money darn it even if it does leave them with peanuts in their elder years.

Interesting article and unfortunately no one knows if they did the best financial decision until their last days. Health is something that many of us take for granted until something changes. My mother was a very healthy person who loved to hike. We decided to claim her SS when my father passed and she was traveling and enjoying life at age 63. ALS changed her life quickly at age 71 and no matter how healthy she was, life changed for the worse.

Great article and good comments to read. I like your idea of visiting with a CPA. We have accumulated a variety of savings, 401K, IRA, pensions, etc but it is difficult to know what spend down process to consider as we continue retirement. Right now dividends and small pension pay for health care and our wonderful retirement life without touching any savings. But I don’t want to donate more than I should of savings to IRS so a CPA with knowledge will be able to guide us more. Also, inheritance could make a difference to some but we don’t have children but I still rather donate to charity and relatives than IRS. My husband wants to wait for his FRA and I want to claim earlier, so we might be mixed due to our personalities vs financial requirements.

There is one solution that is the final word on maximizing Social Security. www-dot-esplanner-dot-com/ I have noticed that PF blog commenters are notoriously thrifty (and lazy, but that is another conversation), and we all live in a culture of ‘free’. The software costs money. You won’t get an answer on a comment-board, but you will with this software. I have no affiliation, just the experience of using over a dozen COTS financial modeling softwares. If you know, you know.

Most (all?) financial planners will have access to good planning software too. I believe the two quoted above both do…

I have been using open social security & running scenarios to get the real cash flows then using the cash flows to estimate break-even times. For me the BE times assuming 4% real return are 84 & 87 for FRA and 70 scenarios. If I use 6% real returns, I get 92 & 95 for FRA and 70 scenarios. The more I do this, the more I think the FRA or 62 scenarios make sense.

Packer

I put together my own spreadsheet model for calculating the simple total lifetime value of the payments (no inflation, COLA, or rate of return), based on two variables for my wife and for me (so four total variables):

1. At what age do we each start SSA payments?

2. In what year do we each stop receiving them (a nice way of saying “die”)?

The key is to get as accurate an estimate as you can of what your payments will be. I just quit working, so I can get a very good estimate from SSA website using my actual salary history; and my wife, although several years younger, only has a couple years to go until she quits, so we can get a good number for her, too.

With these as inputs I can run any scenario I want on my spreadsheet, which includes calculating the Survivor Benefit for whoever lives longer (probably her, but not a sure thing).

The result is I can see what the maximum value of all our payments would be if we both reach the maximum age we’re using for our retirement planning.

I can then see how much of that we give up by starting at different ages. And also how all of the above plays out if one or both of us don’t live as long as we anticipated.

Doing this I now have a much better comfort level with our plan; which includes me starting SS a couple years prior to FRA, and wife starting at 62. What we leave on the table isn’t worth the risk that one of us dies early. Plus, given her younger age, we will have several years of glidepath behind when she reaches 62, at which point we’ll be able to decide whether to go or hold on her taking SS.

FWIW, I’m happy to share the spreadsheet with anyone who’s interested. Before I do I’ve been trying to clean it up a bit so it’s easier to just input your data and then get the report out. If there are any spreadsheet Yoda’s out there, I could use a little help with an Index/Match formula that will make the whole thing work much better. LMK. Thanks.

I’ve also created a spreadsheet to forecast the best option for when to start and would be happy to share mine for comparison. I can also help you with your Index/Match formulas.

I turned 60 last month and even though we don’t anticipate needing SS to meet our expenses I am leaning towards taking it at 62 for me and my wife (she is 3 years younger than me) and saving/investing it. Using the future value function my data shows there will be no advantage to waiting until age 70 if one does not need SS for monthly expenses and simply plan on saving/investing the money.

My example shows that if I start at age 62 and save the money under my mattress with 0% interest by the time I turn 67 I will have accrued $68,000. By the time I turn 70 my accrual will be $120,288. The table shows if annual compounding interest were applied to these amounts I would be well into my mid-80’s before catching up if I started receiving SS at age 67 or 70. I don’t know if or by how much I’ll live past age 80 but I’m sure at that at that point I would have got over any regrets I would have had by starting SS at age 62.

Thanks Larry. I figured out the index formula. I’ll post a Google Drive link when I’ve got it ready to share.

You make the point that you won’t need SS when you turn 62. If there isn’t a need for it, then I recommend you wait to take it because your benefit will be larger the longer you wait and that is very good benefit to consider.

I am a 62 year old, retired, single woman who has decided to wait until age 70 to collect SS because, like you, I don’t need the money since I have a generous pension. I believe NEED is the critical word here. Next year, I will begin taking out money from my 401K and spend that along with my pension. I plan to withdraw only 4% of the 401k but I plan to spend it since I saved it all these years with the purpose of enjoying it. Social Security will be used for any long term care I may need. I plan to stop withdrawing from the 401k once I begin social security and will watch the 401k grow in either the 401k account or in mutual funds which is where I plan to place the RMDs.

The nice thing is if i need LTC, I will have the pension, social security and the 401k. These three will allow me to stay at the nice LTC facility where they will wipe my drool with a golden napkin (LOL).

I’ve heard all the arguments. I’m filing at 62. If I’m still working all of it will be invested. If I’m retired, I’ll use it for living expenses. Each of us starts paying in the day we start earning a paycheck. I’m getting back what I can as soon as I can.

It’s not so simple if you are still working. If you earn more than peanuts your benefit will likely be reduced significantly making an early draw unattractive. In 2019 anything you earn over $17,460 will reduce you SS benefit by $1 for every $2 over that amount. Thus if you had a $2,000 per month early draw amount that would be $24,000 per year. So if you made 17,460 + 24,000 ($41,460) you would get your benefit cut in half. If you made 17460 + 48,000 ($65,460) then your benefit would be reduced to zero. This penalty doesn’t go away until you reach FRA. After FRA there are no penalties for earning money outside of SS.

Math is all well and good but a bird in the hand is worth two in the bush. What good is FRA if I die before then? What good is FRA if the system collapses due to the 10,000 people turning 65 each day in the U.S.?

And to top it off, the breakeven point is somewhere in your late 70’s. That could be 15 or so years of monthly income to be invested or enjoyed, whatever the amount—before the breakeven point. If the system is still intact, I’m filing at 62.

The system will still be intact and it will be so until the US collapses or until they replace it with an even more generous program. How will they pay for? No one cares. They will run the country into the ground before they ever touch social security.

My point wasn’t about whether you should draw early. The point was if you are still working and making a decent wage you won’t be able to draw early. Your draw will be reduced to peanuts or eliminated entirely if you draw before FRA and are making any decent wage at all. See my math above. It should make it perfectly clear what happens if you try to draw when you are making a decent wage. This is not about getting a bigger draw later. Your bird in the hand will be a rubber chicken because they won’t let you take a bird early if you are making your own bird from wages.

So you can say you are drawing at 62. You can file at 62. They will gladly accept your filing. And then they will calculate your reduced draw based on your wages and send you a check for $0.00

I commented earlier to Tom’s post concerning when and why I’ll be filing.

This a Google Sheet link (https://docs.google.com/spreadsheets/d/1-GwwkznHXEKzXYr7pPgyTu7DDwjUkkZ6-Ka7asYTnd4/edit?usp=sharing) I created to help me estimate break even ages.

Feel free to make a copy and change to figures for your personal use.

Very cool, Larry. I especially like the way you’ve incorporated COLA into it, as well as the ability to model different end dates and start ages.

Mine did not model COLA (or investment earnings), but I may consider adding those using your approach as a guide.

The last thing I’m working on is modeling Survivor benefit so the sheet automagically determines whether a surviving spouse is eligible for a survivor benefit, and if they are, how much is it worth.

I can do it manually, but it’s not as user-friendly as I’d like it to be. This gives me a picture of the total value of our benefits for my wife and me combined, so I can play around with when we both start, how long we both might live, and how much we give up by starting early versus both waiting until age 70. Good stuff!

Thanks!

How do I access the model?

Glen – you need to save a copy to your own Google drive before you can play with Larry’s model. File>Save a Copy

An article about consideration to raise the retirement age to 67 was what put me on the path to FI, and reading all these blogs. 3 out of 4 of my grandparents passed away by age 72. I am not going to only have 5 years of retirement! Sure, medical technology keeps us living longer, but if I make it into my 90s I don’t know that I’d go on the same adventures as in my 60s.

I’m inclined towards earlier than FRA, to reduce spend from other sources at the moment, but will evaluate as things get closer.