Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in November.

My questions are in bold italics and his responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I am 46 years old. Been married for 18+ years. A gentleman does not reveal the age of a lady! (As one of the interviewees said.)

My wife and I were born and raised in India. I went to school and college in India graduating with a Baccalaureate degree in Computer Science and Engineering. I came to the United States on a H1B visa.

We naturalized as citizens of the USA on July 4, 2010 at Mount Vernon (George Washington’s Estate).

My wife is an artist and she is now doing her own thing helping families and kids focusing on mental and emotional wellness. She holds a Masters in Arts Management.

Do you have kids/family (if so, how old are they)?

Yes, we are blessed with 3 awesome kids.

Oldest is 14, the middle one is 11 and the youngest is 3 years old.

What area of the country do you live in (and urban or rural)?

We live in Northern Virginia, essentially an exurb of Washington DC along the Dulles Toll Road.

What is your current net worth?

Our current net worth (as of Nov 4, 2020) is roughly $3.4 million.

I used to use aggregator services like Personal Capital, SigFig and Mint but over the years have grown really concerned about security and sharing our information with these sites who then use it for marketing and other purposes. I found Mint particularly annoying with constant sales pitches to refinance this, roll over that or get a credit card.

I now use my bank and investment company’s net worth tracker.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

Following is the breakdown of our assets:

- Cash and cash equivalents: $180 k – 4% of total.

- Retirement assets (IRAs, Roth IRAs, 401(k)): $1.69 million – 42% of total.

- Non-retirement assets: $850 k – 21% of total.

- Real estate assets: $1.2 million – 29% of total.

- Bullion and other valuables: $150 k – 4% of total

Liabilities (at this time):

- Mortgages on real estate: $652,520.

- Credit cards: $2,700.

Not included is educational savings accounts for the three kids which is an additional roughly $200 k in total. Expecting that education for the kids will have a significant impact on our savings and net worth.

Cars are owned outright.

EARN

What is your job?

I am Senior Solutions Architect for a multinational enterprise software solutions company.

My current role is very technical in nature, focusing on digital transformation for the business, by migrating the technical and software solutions/services to the cloud.

I have been a manager of teams before and recently opted to move away from team and people management. I am a technologist at heart and enjoy working with technology and dealing with challenging problems.

What is your annual income?

My base salary is $190k. There is a bonus component as well which is driven by individual performance as well as company performance. This could end up varying from $30k to $50k.

So, if all goes well with the company meeting/exceeding its goals even during the challenging COVID times and my performance is deemed excellent – my gross annual income could be $240k.

Now that things are taking a turn for the worse as COVID flares up again, the bonus pool is very likely to be cut significantly or entirely.

Not included here is any income from dividends, interest income or from my trading activities.

Not included also is income from our townhouse which is rented out. That income is a complete wash when accounting for mortgage, taxes, insurance, maintenance costs and management fees. The past two years our spending on maintaining that home has grown significantly. When this renter leaves we anticipate a significant capital outlay to refurbish and fix up the home.

Not included also is any income from my wife’s work as she is still working to set up her practice. My wife had started working full time after our oldest daughter was a year and half. Unfortunately, our daughter was falling sick a lot from her day care. Eventually she landed in the hospital and we decided that my wife will leave work.

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

My first paying job was a summer gig during college helping a local religious center fix their desktop computers and software programs. The software was written in a language called BASIC. I earned a grand total of Rs 400 each month then (less than $10/month).

After college, I started working for an Indian software services company, moved to New Delhi and was earning Rs 8000 per month before taxes (less than $200/month).

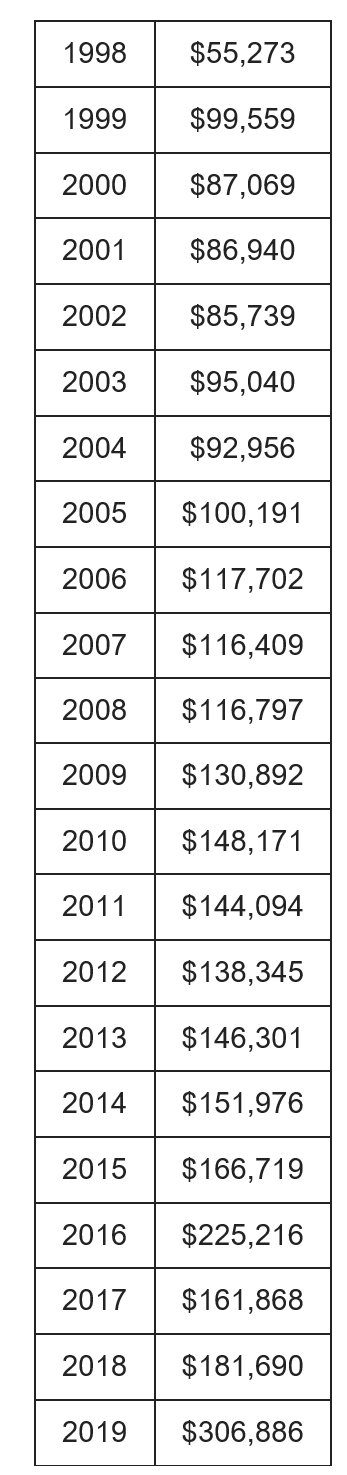

Once in the US, my income jumped to roughly $5,000 per month (in 1998) equal to $60k yearly. It took me an additional seven years to break into six figures, the dot-com crash of 2001 followed by the terrorist attacks of 9/11 left me unemployed for several months when the startup I was with folded. I took a pay cut to help me land the next job.

I never gave up though, continued learning and improving my skills. I taught myself to work with new technologies, took on greater responsibilities and worked to solve ever more challenging problems. I made mistakes too but I have tried to learn from them.

Other than technological skills, I learned to be more inclusive and to become a mentor. I also learned that it is vital to work for a supportive and kind supervisor. No matter how good a company overall is, if your immediate supervisor is an ass and a jerk, you will not enjoy your work much less thrive in it.

Income has varied through the years due to liquidity events such as stock options vesting, bonus payouts.

Below are the details of income over the years.

What tips do you have for others who want to grow their career-related income?

At least in technology, there is only one thing that is true – what you know today will be outdated soon enough.

Constant learning is the only way to excel in this environment. This may seem daunting but it’s really not. To me at least, this is exciting. There are excellent blogs and great tutorials on Youtube etc. plus online learning services which one can leverage.

One must have some liking for the line of work, for that is the only way to continue to grow and become better at it.

It is best to try out various companies and find a place that fits best for you from a work-life balance and culture perspective. Loyalty to a company is a thing of the past. When push comes to shove, corporations will not hesitate to lay off people even those that have worked for them the longest.

Your resume and LinkedIn profile must be always updated to reflect your growing experience and skills.

Build a network of recruiters and head-hunters that will bring interesting assignments and roles to you.

What’s your work-life balance look like?

It has gotten better over the years, although in these Covid times we are staying home and avoiding all activities, so no going to parks, to restaurants, to movies or to take part in cultural, sporting activities.

I used to work 60, 70, sometimes 80 hours per week but I don’t do that anymore. I used to work remotely in the past and the current work from home restrictions are just fine with me and my family.

Even if Covid restrictions are eased/lifted in the near future, I do not plan to go back to the office. I don’t see that changing when, and if a safe and effective vaccine is developed.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

We rent out our townhouse, but as noted earlier, the income from that is a wash. That townhouse was our first home that we purchased in 2004 before the housing market peaked in 2006. When the housing market collapsed taking the wider economy down with it, I was fortunate to be working for a relatively stable, large company.

We decided to take advantage of the downturn and bought our current home. While we were busy looking and buying our home, the county our townhouse was located in had enacted provisions that allowed local police to ask people for immigration documents even during traffic stops. That made the already dire housing market situation even worse. Entire families from that county disappeared overnight. A lot of homes went into foreclosure, even more than the damage wrought by the housing market crash. New lending rules meant significantly fewer people could buy.

So selling the townhouse then would have meant taking a significant loss. We decided to rent it out. Our experience as landlords has been mixed – most of the people applying are people with poor or bad credit. One renter had the money to spend on glasses costing $900 but had trouble paying the rent on time.

A former cop bailed out on his lease and left the keys on the kitchen island. We later learned he had borrowed money from a lot of people from the mosque he attended and they were all trying to find him and collect.

The home needs more upkeep now. Once the current renters leave, we will need to spend a good chunk of money to replace the carpet, appliances, get things fixed up etc.

I tried (for some time) to start a IT consulting business but decided to not pursue it primarily due to the exorbitant costs of health-insurance coverage.

SAVE

What is your annual spending?

Our annual spending is tracking around $60k on average.

This year of course, our spending is down significantly.

What are the main categories (expenses) this spending breaks into?

Following is the breakdown of our expenses:

- Housing: $40,000.

- Shopping: $4,000.

- Utilities (Natural Gas, Electricity, Water/Sewage, Internet, Mobile phone plans): $3,000.

- Transportation: $3,000.

- Travel: $5,000.

- Charitable giving: $5,000.

Do you have a budget? If so, how do you implement it?

Not anymore. We used to budget, and I used to balance our checkbooks and cross-check our monthly credit card bills with all the receipts.

We just don’t do it anymore. Our spending is a well established pattern and variations are always something that we discuss and ensure it fits our priorities.

What percentage of your gross income do you save and how has that changed over time?

When I started working in India, I was saving nothing simply due to the high cost of living in New Delhi area and the measly income after taxes. I was able to gradually grow my savings rate to 15% and it stayed that way for several years.

Last year, we put away 50% of our income as savings in different vehicles such as 401k, education plans, HSAs etc.

This year, we will likely save 70% to 80% of our income – all thanks to COVID and related lockdowns.

What’s your best tip for saving (accumulating) money?

Maximize your 401k contributions and leave that money alone.

What’s your best tip for spending less money?

Focus on the priorities.

Keeping up with the Joneses is never a priority.

For example, we chose to purchase a Toyota Sienna, a minivan when our unexpected addition to our family was on the way in 2017. Almost all our friends and neighbors were buying Teslas and Mercs. We ignored all of that and focused on our priority.

What is your favorite thing to spend money on/your secret splurge?

Nothing really. I do love good food and tech gadgets. I have never been one to stand in lines to pre-order the iPhone or iPad.

We have a lot of devices at home now, hand held devices, smart speakers, FireTV cubes, WiFi enabled TVs but almost all are several generations behind the latest and greatest.

INVEST

What is your investment philosophy/plan?

Initially it was a simple one, putting all my savings into index funds such as Vanguard S&P 500 Index Fund.

Right now though, we are going after growth stocks and investing in the companies and sectors that we understand. The plan is to transition to dividend paying stocks and ETFs as we near retirement age.

What has been your best investment?

Continuous learning and development, in other words, investing in ourselves.

What has been your worst investment?

From a perspective of investing in assets – buying into IPOs of Uber, Lyft and most recently Snowflake have been my worst investments.

I also lost all my money buying shares of Nortel back in the late 90s.

I did not do enough due diligence in these companies and essentially bought the hype when I should have paid attention to the fundamentals.

What’s been your overall return?

Overall rate of return on assets invested is around 18%.

This year alone, we are up 40%.

How often do you monitor/review your portfolio?

Almost daily.

NET WORTH

How did you accumulate your net worth?

First off, as immigrants there is no inheritance that we expect to get of any sort. Everything we have built is through hard work, living below our means and investing whatever we could as the years went by.

We have stuck to the basics:

- We have worked diligently to learn and grow our skills.

- That in turn, allowed us to seek higher paying jobs and increase our family income that way.

- We maximized our 401k deductions.

- Invested in Roth IRA (when possible), started a Health Savings Account and 529 plans for the kids.

- Consistently lived below our means, even though that meant we drove old reliable cars and never splurged on anything just because others were doing the same.

- We avoid credit card debt, unless it’s a purchase at 0% interest for a certain period which we always pay off. Credit cards and pay-day lenders are legalized usury in my view.

- We have a rainy day fund.

I want to point out two additional critical factors that helped us get to where we are:

- Debt – taking on mortgages to buy our homes to us is a smart decision. Interest rates are historically low, plus there are tax write-offs (limited to $10k in the 2017 tax bill, but still…). Money “saved” by not paying off that debt is invested and that has grown at a significant pace.

- We left our investments alone during the Great Depression and then most recently during the downturn right after COVID related lockdowns. I remember that the S&P 500 went all the way down to 900 points during the Great Depression, essentially cutting our investments to a third when compared to 2006. We know so many people who panicked and sold during that time. We did nothing, just left the money where it was. Then again during the COVID lockdowns, just one of our IRAs was down like $250k. We made that money up and then some by staying invested.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

It is investing for sure, and I believe it will continue that way.

Invest in your own self and let the compounding nature of the stock market work for you.

[Editor’s note: I would classify this as “earning” since you invest in yourself (i.e. increase in knowledge and skills) and thus your earnings grow, but I’ll leave it to the readers to decide how they view it.]

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

The usual ones – job loss due to events outside our control, unplanned and unforeseen expenses and stupid mistakes.

The big elephant in the room though is health challenges. My wife was recently diagnosed with a chronic condition which requires regular treatment with expensive medications.

For me personally, I struggled with alcohol abuse for years, which looking back now stemmed from underlying depression. I lost track of my priorities as a result. I went cold turkey in September 2018 and have sought mental health services.

Doing better now, and I want to make sure people understand that mental and emotional health is as important as our physical well being.

Health is wealth!

What are you currently doing to maintain/grow your net worth?

I plan to stay the course.

We will continue to work and grow skills, to continue earning more and continuing to invest in the stock market.

Do you have a target net worth you are trying to attain?

A few years back, $1 million seemed out of reach! $5 million seems within reach and if things go well, $10 million would be a stretch goal.

How old were you when you made your first million and have you had any significant behavior shifts since then?

I actually don’t know/remember.

If I were to guess, it was probably around 2012 when our net worth crossed the $1 million mark, so I was 38 years old then.

The only thing that has changed is that we try to live and travel well, nothing extravagant. If you ask my wife though, she still thinks I am very thrifty/frugal.

What money mistakes have you made along the way that others can learn from?

Invest in yourself and your mental, emotional and physical health.

When investing in assets, always do your due diligence.

What advice do you have for ESI Money readers on how to become wealthy?

Everything in life is a risk, even investing in the stock markets and for sure, starting your own business. Understand your risk tolerance and act accordingly.

Work to grow your income, live below your means to allow you to save and then invest it for the long haul.

FUTURE

What are your plans for the future regarding lifestyle?

Some time back, I gamed out a few scenarios using retirement calculators and tools. According to those tools, assuming an average rate of return of 7% on our current assets, a drawdown rate of 4% and accounting for taxes and life-span, we could retire in 10 years.

If we live very frugally and make an above average return on assets, we could retire now.

Our older daughter will start college in 2024, followed by the middle one in 2027 so those expenses are coming. We would like to ensure all our kids get a good start in life.

The big elephant in the room though is health and health-care expenses.

Bottomline – I don’t expect to retire until at least 65 years of age and I plan to continue working full time until such time I am able to and my contributions and experience is valued.

Once COVID is under control with a vaccine, we want to travel to Europe, Peru etc. Travel, and living well is our only goal that has evolved and allows us to consider options that I guess being ‘wealthy’ allows.

What are your retirement plans?

My wife and I plan to travel around the world.

We also enjoy going to the gym, playing golf and performing arts.

Along with our activities, we also expect to be playing supportive roles in our kids’ lives.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

We look at health care as the single biggest risk to our financial well-being.

Health care costs are the reason that I will not take the risk to start a business, it is the reason I know a lot of other people either don’t start a business or are unable to keep it going. Health care costs are also a big reason most people continue to work in dead-end, soul sapping jobs.

All of our political leaders are too craven and beholden to the insurance companies to make the decisions that will actually provide the basis for more job creation in this country.

Our goal is to save and grow our HSA to half a million dollars or more over time. For that goal, we contribute the max to our HSA and we actually do not use it for our current medical expenses. At the same time, we are actively trying to maintain our physical, mental and emotional health.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

I remember my father talking to my brother and I during our college years about the need to learn how to manage money. He would often say that as important as it is to earn enough to meet your needs, it is as important to learn how to save and manage your money.

He built his own methods and while he was and to this day is quite risk averse, probably due to the various scandals and scams in the Indian stock markets – I see those conversations with him as getting me started on this path.

My first few years in the states, living all alone, no family or friends to help/guide me, I had to teach myself everything. My very first paycheck in 1998, I had no idea what all the various deductions were – I just remember being shocked at the take home / net pay.

When I had to file my tax return, I had no idea that one could go to preparers. I had no idea what H&R Block was for example, and I filed my tax returns on paper, hand filling the forms myself and doing all the work to figure out my taxes by reading IRS publications end-to-end.

Who inspired you to excel in life? Who are your heroes?

That would have to be my parents. My father is the first one in our family to go to college in the family, then worked to build himself and the rest of the family up – he gave me and my brother a much better start in life.

Some of the teachers I had also instilled the values of hard work and to strive to be the best.

I have also been inspired by Gen. Colin Powell’s life story.

In technology, I have looked up to the usual suspects – Steve Jobs (Apple), Brain Kernighan & Dennis Ritchie (Bell Labs).

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

The Millionaire Next Door![]() and its sequel The Millionaire Mind

and its sequel The Millionaire Mind![]() helped crystallize the basics, and then I read a lot online.

helped crystallize the basics, and then I read a lot online.

I also regularly read Warren Buffet’s letters to his investors.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

The short answer is yes, but the long, nuanced answer is that this is still a work in progress.

We take some care to look for public disclosure forms for the charities we give to since we have known some charities misuse funds.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

Expect to yes.

If all goes well, we expect to have a net worth of $10 million or close to it. We expect to leave some chunk of assets to our kids.

Life in America is becoming tougher and tougher for working people. Work is still looked upon as good and glorious but our tax policy favors the wealthy and capital. I personally expect taxes to go up in the near future, plus the cost of health-care and education to continue climbing. Housing is becoming out of reach for a lot of people in places like NYC, San Francisco, etc.

I hope and expect that our kids will do well in life, but we are also fully prepared to help to ensure that their quality of life is good.

Nice read and congratulations on being able to turn your high income to savings and investments.

> The software was written in a language called BASIC

10 A number of similarities with our background — CS, software engineering, immigrant, and saver. I’m SFI9 and MI238 (coming out soon, I guess)

20 BASIC was my first language too. I started writing code when I have 11-12 years old, and did build software for a local grocery as a teenager.

30 Based on your heroes, I’m going to assume that you were into C as well — K&R.

> This year, we will likely save 70% to 80% of our income – all thanks to COVID and related lockdowns.

Great to see that you’re able to save that much. I’m curious how you’re able to do that considering you have kids, mortgage, etc. Personally, I’ve been only able to historically save 40% which is why I’m always curious of what people do (hacks) or not do to have above 50% savings rate. Care to share?

Congrats again!

You and I are brothers! 🙂

Yes, taught myself to code in C, COBOL, C++, then Java, Python and dabbled in Android and Swift.

As far as savings go in the past more than a year, the answer really is simple – increased income, specifically vesting of stock options and bonus payouts. With gross income as a result crossing $300k, cutting out on eating out, no travel, no shopping for tchotchkes – ergo saving rate has gone up.

We recognize we are blessed.

Good job on the savings!

C++ (Linux, Windows, and Solaris) is what got me in the US as a 23-year old software engineer. I only brought two books with me to the US, the Design Patterns book and Stroustrup’s Design and Evolution of C++. 🙂

I’ve since moved on to Java, Python, C#.NET and Go. However, my hands-on these days are mostly personal and the occasional bash and python script as work.

If you’re interested, we can discuss the structure of the code I wrote for our model and simulation — https://forums.millionairemoneymentors.com/t/p-boone-countdown-to-retirement/2357. It’s in github, with unit tests, integration builds, etc. 🙂

Awesome! Would love to learn about your work. You are way ahead of some of the engineering teams I deal with at MegaCorp – those engineers look at me blankly when I ask then about unit tests, automated integration tests and CI/CD. 🙂

Thanks again for your kind words! Would love to connect if you are open to it. Pls let me know.

Thank you so much for sharing your advice.

I cannot agree more that health is wealth. My mentor once told me that you cannot enjoy your wealth if you are in bad health – and hearing that just clicked for me. And I completely agree that being healthy does not just relate to physical health, but that it also relates to emotional and mental health.

You make another great point about investing in yourself and always learning and growing your skills. Although it seems like humans naturally tend to go against change, it is necessary for us to adapt to new eras. I find one of the best ways to is by researching and learning. Try to understand what makes you uncomfortable. Typically, the better you understand something, the more comfortable you are with it.

Thank you so much for your advice and I hope your wife will feel better soon.

Cheers,

Fiona

Thank you for the kind words! One grows when faced with challenges/adversity, or at least that is the hope.

Nice work and well done! I also have a wife with health issues which puts things in perspective again. Health is definitely wealth! You are on the path to hit your designed life.

Thank you for the kind words! GOD be with you and your family as well. Despite the challenges, we recognize we are blessed.

Aside from a great job in turning your earnings into a significant sum of money, the part of this that resonated with me was coming to the US, being by yourself and having only yourself to rely on. Not only did you succeed, you excelled. I had that same background myself of being from somewhere else and arriving here in the 90s with just my hands and what was between my ears to rely on. I remember being told I could get a free free soda refill in a fast food restaurant and furtively walking up to get my refill expecting a heavy hand on my shoulder at any moment and hand cuffs next.. 🤣🤣🤣

I strongly believe that if you can be successful (defined as supporting yourself and a little more than that put to the side), the confidence you gain from this experience can form the backbone of a very successful future life in the United States. Very well done because many are not successful.

Are you expecting to spend a lot more in retirement or is it the case that the focus of your retirement is primarily as a legacy for your heirs? A $3.4 million net worth at 46 with $60k in current spending is a very significant sum of money already. Without any growth considerations, that’s $75k a year for 50 years starting today and you are still young.

Great interview

My apologies, that should be $75k for 45 years starting today 😉 $68k for 50.

Kevin – I can relate! I couldn’t believe it myself when I learnt about free sodas, $0.99 tacos at Taco Bell and gas at less than a dollar per gallon back in the late 90s.

Of that one can still get free sodas. 🙂 Travel anywhere and one can see that the rest of the world operates far differently.

I only had like $500 to my name when I landed in the US. It’s been a ride! Good luck to you and your family as well.

We do expect our spending to go up over the next several years. Not planning to retire – just yet. Accounting for unknowns, especially health related is a major factor.

Thank you for the response 😊

I think I had around a $1000 when I got here and that was also when you had to spend $300-$400 in calls a month to keep in touch with home too.

Arrived in roasting Miami Airport in Florida in an Aran wool sweater of all things..

Those were the days…lol

Calling cards – $20 for a few minutes – it would cut you off right in the middle of talking to your family!

International calling plans on landline providers would easily run $300 per month as you point out.

Interesting story here: International calling code for India is +91. North Indian cities used to have city codes starting with 1. So plenty of times, we had cops show up when all we were trying to do was place a call to North Indian cities by calling 911…

Oh Lord, I’d forgotten the calling cards from before I got a landline. +91, that is dangerous.

Posting a broader update here for all readers! Since the time of working on and submitting my interview answers to ESI, a few things changed:

1. Our NW went up to $4.5 mil+. If these trends continue (a big IF in my view) we should hit the $5 mil mark relatively soon. As is often said, the first million is the hardest.

2. I too have been diagnosed with a chronic condition, fortunately the medicines to help with my issues are cheap and generics are easily available.

3. Working on tax returns for 2020 and realizing that despite COVID, or perhaps because of it – our gross income crossed the $500k mark. The stock market, more options vesting and my trading played a major role in this uptick and this has come with a nasty surprise too – income taxes! Personally, we don’t expect this trend to sustain but still it’s been a banner year! And no, we did not invest in Bitcoin or other cryptos!

4. Refinanced mortgage on both our homes to lock in the rates for the next 30 yrs and took some cash out for repairs and remodeling. It’s just crazy in my view not to take advantage of money being so cheap to borrow, with tax write offs on top and use the money not used to pay off the mortgage to invest for the future.

For the data inclined, here are some numbers:

Total earned (1998 to 2020): $3.5 million

Avg earnings: $154,000

Median earnings: $130,000

Net worth (as of April 2021): $4.5 million

Half of our working lives, we earned less than or equal to $130k.

On average, our income is just over $150k p.a.

It really is true that slow and steady wins the race, that following the basics will get you there. If then there is just one home run, then your net worth can be more than your entire total earnings.

Good luck to everyone!

Well Done MI236. Thank you for sharing your journey. It was an awesome read. If you can please elaborate on this update as to how long did the networth take from 3.4 to 4.5 and the breakdown of that new NW. Also if you could share the break down of the non retirement assets. In general could you share the types/names of investments assets and if you try to buy low sell high or buy low and let it grow or dollar cost avg. Anyway thanks again for sharing.

Hi Stan,

Thanks for the kind words. We added $1m to our NW in six months – of course, it’s all paper wealth, so easy comes easy goes is entirely possible.

For the breakdown,

Retirement assets (IRAs, Roth, 401k, HSA): $2.3m

Non-retirement assets (Brokerage, Money Market, ESPP): $1.4m

Real estate assets: $1.3m

The uptick is driven by a general uptick in asset values including stocks and real estate valuations.

Kids 529 plans are not included. Cars and other assets are not included.

Buy low, sell high is hardly a strategy and I certainly have not succeeded in timing the markets. I don’t even try. I don’t day trade, although I do trade in stocks/companies that I know and follow.

Perhaps we can connect and discuss on MMM.

Hope that helps.

Thank you so much. I do appreciate it. Sure we can connect on MMM but not so sure if that is another fire website. I can also be reached at [email protected]. Best.

MMM is the Millionaire Money Mentors forums.

It’s a paid membership group where millionaires and those wanting to become wealthy hang out and chat about money.

Details can be found here:

https://millionairemoneymentors.com/

Thank you!

Great Story. I am also an immigrant from India and resonate with your story and life. I commend you for taking “control” of you addiction and focusing on health. I hope your wife’s condition is managed or even better she feels better. I too struggled with addiction and have worked very hard to manage it through recovery process and mental health. I focus more on mental and physical health. When you are mentally and physically healthy – your healthcare expenses can be way lower !! We have gone plant based whole grain food, no alcohol, running twice a week (6-10 miles), yoga 3 times a week, meditation 30 mins daily and reading a lot of books. Our relationships with friends, family and kids are so much more rewarding than before.

My story is M116 and that was 3 years ago. We had NW of $7M and it has grown to almost $11M. I think your goal of reaching $5M is easy and I am sure $10M is not a stretch. It compounds quickly.

Best wishes for everything and thanks for the story

Thanks for the kind words! Lots of similarities in our situation and we would love to catch up outside of this forum if you are open to it and ESI allows it. 🙂

I read your story, inspiring and motivational.

In our case, I have personally now opted to cut down on work commitments and stay in an individual contributor role, not working/traveling to execute a Director/VP/CTO level role. I actively decline LI roles that do not meet my criteria.

Let’s connect on MMM if you are present there. Alternatively, I can share my phone number here and we can connect. Pls let me know.

Happy to connect. I am not on MMM I think ! If you like share your email and we can connect from there. Thank you.

I responded elsewhere but just wanted to be sure you see this:

MMM is the Millionaire Money Mentors forums.

It’s a paid membership group where millionaires and those wanting to become wealthy hang out and chat about money.

Details can be found here:

https://millionairemoneymentors.com/

I hope you can figure out my email, trying to avoid being picked up by spammers/bots. 🙂

o b j v I v at y a h o o dot c o m

o – orange

b – boy

j – john

v – victor

I – lower case I for india

v – victor

at

yahoo.com

So many of us former techies becoming millionaires on here! There has to be something in our genetic “techie” make up. I think it’s the abstract data structure mentality that makes us all so good at personal finances! I started with Basic then Pascal, Turbo Pascal, Cobal, C, and finally C++. I’m thankful that I (finally) left the IT world for the operations side of the business world! I could’ve never kept up with the ever changing learning demands. But my IT roots served me extremely well on the business side. My hat is off to you for surviving and flourishing so long! Congratulations. Great write up. I really enjoyed the whole backstory. I can’t imagine traveling to another country by myself and sitting down to read the IRS tax codes! Hats off to you!

100% agreed. Techie here too..

Hi MI-226,

Thank you for the kind words.

Quick q – ref your transition out of IT world, I am presuming you left coding. Did you move to IT operations or business operations such as running/maintaining production lines?

It’s great to connect with like-minded folks.

As for sitting down to read the IRS code, it was the only logical thing to do given what I knew at that time. 🙂

Sincerely.

I left coding (and managing coders directly) to cross over into business operations. Specifically Supply Chain Operations (Production Planning, Distribution, Purchasing, Inventory Control). My last few years of coding were for a large medical device MegaCorp that was automating their distribution systems. I had been specializing in radio frequency and robotic warehousing systems from a previous employer (late 80’s to early 90’s). Initially, it was an easy transition to Distribution Operations for me to run and automate their distribution centers with my IT specialty in that area. I ended up setting up and running automated distribution centers around the globe. Having both the programmer mindset and the business aptitude to optimize business supply chains was a deadly combination and made for an awesome career. Longer term to senior levels over North American Supply Chain Ops in the Pharmaceutical sector. Not the typical IT career path, but it was great for me. Congrats again on a great read!

Awesome! I can see the value of an analytical mind that pays attention to detail for an effort like RF and robotic warehouse systems automation. Sounds like a fun effort and great value add.

MI236,

You mention your HSA, but don’t specifically list it in your assets.

Curious how you categorize that investment? Like you, I never use HSA money to pay for actual medical expenses. I like to look at mine as an additional retirement account and also as an additional emergency fund to my emergency fund. An HSA is bar none the best money savings tool we can have IMO.

Also, 500k seems like a lofty goal for an HSA balance when you can currently only max out at $7100 a year…. What’s your secret?

Hi,

There is no secret. It’s just a goal to try and get it to half mil by the time we retire. Let’s see if we actually meet that goal.

For now I am doing what I did to our other retirement assets, move them off of the company provided platforms/vehicles as quickly as possible and into HSA account with brokerage company so I can buy individual stocks/ETFs and not have to be stuck with investing in MFs with high expense ratios with additional exorbitant fees charged by HSA providers.

HSA is a great money savings tool but the HSA providers are ripping people off.

Sincerely.

To your specific question, HSA funds are part of retirement assets, as of now <50k in total. I started the HSA pretty late I think in 2016/2017. Definitely a miss on my part.

Wow congratulations. It’s remarkable you’ve been able to either increase or keep your income levels even during bad times such as the coronavirus pandemic, 2007-2009 crash, and 2000 – 2003 crash. Also even after getting laid off from the tech crash, 9/11.

Was it difficult to get back to the same income levels and/or exceed it? I know companies love to pay the least amount of money they can to an experienced employee.

Thanks for the kinds words David @ Filled With Money.

You will notice that in 1999, I nearly crossed the six figure income level. Then the dot-com crash and 9/11 happened and I took a pay cut to find other work and by the time I crossed six figures in income, it was 2005. So it was definitely a setback.

Still it taught me that there is always demand for good people with skills.

Like you, we rented out our “starter” house for a number of years (about 15 I think) and I finally got tired of dealing with the hassles. We were doing just better than a wash financially. When we sold it, we actually did quite well, our net proceeds were about 3 times the initial cost of the house. However, they would have been even better had we been wiser in our tax planning. I did not keep adequate records to expense on the house and as a result the capital gains really bit us. I would encourage research, either reading IRS information or consulting with a good tax accountant or attorney on rentals and capital gains. They likely can give you some direction on Preparing for the day you sell the house. As a wise accounting teacher once said, the Supreme

Court has determined that tax evasion is illegal, but tax avoidance is OK! Best of luck.

Thanks for the kind words AZ Joe!

Will definitely look that up as I am also concerned about the depreciation claimed all these years and how that will be handled. Any experience with that?

It has been some time since I dealt with that and I mostly had our accountant do it. As I remember, the depreciation is all added back in and becomes profit when the house is sold, so it becomes part of the basis for your realized gains. It is possible to reduce the basis by subtracting any improvements to the house (you added value) thus keeping good records is vital. What ever money is realized net of your cost for the house (Including depreciation) becomes the capital gains taxable amount. Capital gains are taxed at a somewhat lower rate than most income taxes, but still it is pretty hefty. Our accountant did the best she could, but we still paid a pretty big chunk in capital gains. As far as I know the only way to really beat the system is to move back in and live in the house for 2 years, thus making it again your principal residence. That makes the realized income tax free. However, we chose not to do that and just lived with the tax.

Awesome, thanks!

MI-236,

Since your townhome is purely an investment property at tis point, you might want to look into a 1031 exchange.

From the IRS: “Whenever you sell business or investment property and you have a gain, you generally have to pay tax on the gain at the time of sale. IRC Section 1031 provides an exception and allows you to postpone paying tax on the gain if you reinvest the proceeds in similar property as part of a qualifying like-kind exchange. Gain deferred in a like-kind exchange under IRC Section 1031 is tax-deferred, but it is not tax-free.”

Also, you might want to look into this:

Opportunity Zones provide substantial tax benefits to investors who move any realized capital gains into a qualified Opportunity Zone Fund within 180 days of the asset sale. In turn, these Opportunity Zone Funds may invest in qualifying businesses, real estate or infrastructure substantially located within a federally designated Opportunity Zone. Check out this interactive map of Connecticut’s Opportunity Zones and some highlighted projects.

In exchange for their investments, Opportunity Zone Fund investors may be able to decrease their federal tax burden through the preferential treatment of capital gains — in three key ways.

First, any capital gains on the money reinvested in an Opportunity Zone Fund will be temporarily deferred.

Furthermore, the taxes on those capital gains may be reduced if the Opportunity Zone investment is held for at least 5 years — and even further reduced if held at least 7 years.

Finally, any capital gains on the Opportunity Zone investment itself can even be eliminated — if the investment is held at least 10 years. You’ll find more details on how these federal tax benefits work here.

If an equity investment in a qualified project must be liquidated before the 10-year investment period is over, the Opportunity Zone Fund can reinvest in another qualified business or project.

Awesome info! Thanks for sharing MMiguel!

This forum is truly a great place to learn.

Nice story. Pretty amazing that even with your health problems you still accumulated the wealth. Re: hsa account. I have one with chard Snyder. Are you saying that it is feasible and beneficial to pull the money from chard and into say a Schwab brokerage account? I also wonder if my I change health coverage I would still be eligible for hsa. I am on cobra now. I only have some 50% of my wealth in equities. My money hasn’t worked as hard as it could have. I have had to do the heavy lifting by earning. I am semi retired and age 59, thus reason I have high cash cushion. Though I am still working a lot by choice. Thanks. Gary

Hi Gary,

Thanks for the kind words. We have been lucky and yes blessed.

I have not had any experience with Chard Snyder, but have dealt with Optum and HealthEquity and yes, they were both expensive for the privilege of investing *my HSA dollars*! They charged a monthly fee to use their investment platforms and then limited the options to a few MFs all with high expense ratios.

So yeah, as soon as there is enough, I move our money over to a HSA with Fidelity and now we don’t pay any costs to trade plus we have access to any ETF we want to buy.

I am no advisor but I don’t believe changing plans has any impact to funds already accumulated in HSA. HSA $$ are always yours.

Happy to discuss more in MMM if you are there.

Sincerely.

My HSA was with HealthEquity originally and I moved my HSA to a Fidelity brokerage account. Fidelity have one of the best if not the best HSA accounts available. It was very easy to do.

Congrats on the impressive net worth and growth. I’m always impressed by how fast it goes from $1m to doubling/tripling considering how long it took to get to that first $1m.

It always impresses me how much software coders make in the US. I remember turning down options to move to silicon valley, since at the time the USD wasn’t as strong and the incomes were similar in my own local market. Fast forward to now, and the US is making 3-4x easily, and actually changed careers in order to earn a decent income. I think a decent software developer now makes around $60k per annum here, down from $100k in 2007 due to the currency depreciation. I guess it would’ve been similar had you not made the move to the US and built your software career in India?

Well done on the high savings rates, building the net worth and achieving so much and coming into the US to achieve it!

Thanks for the kind words!

I know people who stayed in India and went on to become VPs/CTOs due to the spectacular growth curve in IT during the years I was slogging away here in the US. The dot-com crash and 9/11 caused a crash here but companies still needed good IT work which for a time was pretty much all being off-shored to India.

At the same time, the growth in India itself and the crazy up tick in real estate prices there additionally made a lot of people a whole lot of money in India.

Wealth is always relative.

This hit home:

“For me personally, I struggled with alcohol abuse for years, which looking back now stemmed from underlying depression. I lost track of my priorities as a result. I went cold turkey in September 2018 and have sought mental health services.

Doing better now, and I want to make sure people understand that mental and emotional health is as important as our physical well being.

Health is wealth!”

Alcoholism runs rampant in my family and at an early age (around 23) I decided I wasn’t going to tempt fate, so I swore off drinking. I’m now 48 and have never had to deal with the disease – which I am very thankful for. Health and finances are closely intertwined – when you struggle with one, the other is negatively affected as well.

Agreed and awesome job staying off alcohol. Keep it up!

So if I had to choose ONE THING as the catalyst to this wealth, I would say it was moving from India to the USA and getting an income increase from under 2.200/year to 55.000.

That’s a 25-fold increase.

Only in America.

If you were to have the same compounding but had stayed in India (very unlikely to have the same compounding without the 401k benefits, the amazing wage increase possibilities and the success of the US stock market) you would now have a wealth 25-fold less.

Lesson here: Move to America.

People for centuries now come to America for opportunities and to give their kids and families a better life. By all means – Move to America, but it is not as simple as saying that move to America = becoming a Millionaire.