Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in April.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I’m 36, turning 37 next month. My husband recently turned 42.

We are just shy of our 5-year wedding anniversary.

Do you have kids/family (if so, how old are they)?

No kids.

We live close to my husband’s family, two sisters, brother-in-law and his mother.

My parents & two siblings are spread across the mid-West.

What area of the country do you live in (and urban or rural)?

We live in the Northeast, about ~30 minutes from a major city.

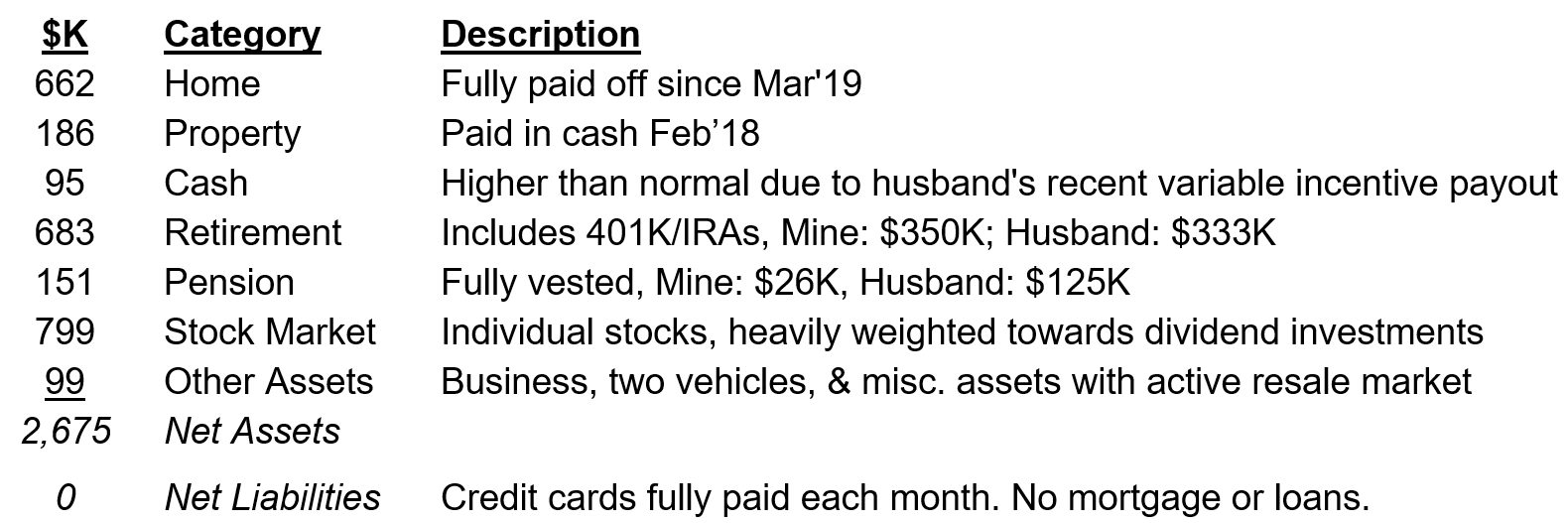

What is your current net worth?

Our current net worth is $2.675M (as of March 31, 2022).

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

I error on the side of conservative and I hold back on the valuation of our primary home, second property and some of the other assets (i.e., Zillow values our properties an additional +5%).

EARN

What is your job?

I’m a Corporate Finance executive at a Fortune 100 company.

My husband is an IT executive at a Fortune 200 company.

What is your annual income?

My current total compensation ~$360K, which is a base salary of $209K plus variable incentive and long-term retention incentives. This is up significantly from $220K last year due to recent job change.

My husband’s total compensation will hit ~$385K in 2022, but varies quite a bit based on value of equities and variable incentives. His base salary is $204K.

We also started up a small business a couple years ago, this operationally is break-even, but has been a nice tax shelter for the past couple years.

We also have dividend income of ~$50K per year based on our current portfolio, which is fully re-invested.

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

I started babysitting around 14 years old for ~$5/hour.

During college, I worked an average of ~35 hours a week between a local bakery making $8/hour, tutoring high school students $20/hour, working with special needs kids, and researching for a college professor. Looking back, I’m not sure how I managed a full course load and the schedule of four jobs, but I made it work.

Being the youngest of three, by the time I went to college there wasn’t any financial support for me so my small income went to tuition. I lived at home with my parents to save on room & board and commuted to campus 4 days a week.

When I graduated college, I had accumulated a small amount of debt (~$15K) primarily during the time period I studied abroad.

When I graduated college, I went to work for Fortune 500 company in a finance leadership development program. I started out earning $48K. The program required me to move every year, which resulted in ‘one-time’ relocation benefits each year of an additional $15-20K. I spent 6 years with the same company, changing jobs and locations every year, increasing my income to around ~$80K.

Unhappy about my location and wanting to move closer to friends/family, I took a role with Fortune 100 company making about $90K. I crossed the $100K threshold 15 months later when they promoted and relocated me to their division headquarters. The job market got tighter and my company instead offered variable incentives instead of base salary increase. For almost two years my base salary did not grow much, despite working hard and taking on more scope.

I worked up the nerve to complain to my manager about my lack of meaningful compensation increases. To my surprise, he got me an extra $35K. In retrospect, I was just grossly underpaid for my contributions, but learned a valuable lesson…the squeaky wheel gets oiled as my husband likes to say!

I found a bit of a niche when my division got divested. I received a one-time incentive to stay during the transition for ~$30K. I ended of staying at the spin-off company for three more years, as I had some autonomy to write my own job description and work on the projects I enjoyed. My base salary went up to $165K + variable incentives, but I was unhappy with the leadership at the new company.

Unexpectedly, an old boss recruited me back at my previous Fortune 100 company. I’ve been there for about 6 months and increased my base salary to $209K. To my surprise, one month in the company announced another big spin-off. The good news for me is it’s resulted in a fairly substantial 3-year retention agreement to support the spin.

What tips do you have for others who want to grow their career-related income?

Lesson # 1: Don’t undervalue yourself

Ask for more than what you think you’re worth. You don’t want to ask for more than what makes sense for the role, but you also want to get compensated fairly and on the higher end of the salary range the employer is already expecting.

If you’re working with a recruiter, usually the company already has a range in mind and they can share that information with you. If you’re not working with a recruiter, do your homework. There is a lot of readily available information about average compensation for a given area through Glassdoor or recruiters who work within your functional area.

Lesson #2: Don’t be afraid to negotiate

When I accepted a role with a new company, the job was posted without relocation. When they made me the offer, they said if I wanted relocation, they would have to re-post the role and it would delay the hiring process by 2-3 weeks. I naively accepted the role sans relocation.

In retrospect, I should have negotiated for more salary and secured relocation benefits. I was so impatient and excited about the next steps that I cost myself probably $10-15K of additional incentive.

Lesson # 3: It never hurts to ask

Women especially seem to have a hard time asking for more and feeling as though they’ve earned it. If you want to be paid more, first do more then ask for more.

In one personal example, I had been running on fumes for months at work. The perfect storm – I had a new boss, the business was recently divested and acquired by another company, and we had significant turnover in my department. I had received a retention bonus during the year of the transition and an increase in my variable incentive, but my base salary had not been raised for over two years due to a salary freeze implemented company-wide.

During the transition, I had taken over two other people’s roles on top of my existing job. My role was never re-scoped to account for the additional work. Afraid to make waves, my husband encouraged me to say something to my boss. I didn’t have a formal plan – but after I explained the situation to my boss, he took action. I thought at best I’d get a 10% raise, but he came back with a surprising offer. If I would write up the job descriptions, they would post for the two additional resources. On top of that, I received over a 30% pay raise!

What’s your work-life balance look like?

My work-life balance is decent now, but it was not always the case. Since I started my new role about 6 months ago, there was a big adjustment period that increased my stress-levels. My meeting schedule today is a bit more chaotic and less respectful of a dedicated lunch break.

My last gig turned into a European based company, which took almost the whole month of August off in the summer, respected your vacation time, and always took at least an hour lunch break.

During my early career, having relocated almost every year for work, I didn’t have a lot of distractions of friends & family nearby. I spent a lot of extra time in the office, including early mornings, late nights, and long weekends. I invested a lot into my career and luckily had some great mentors along the way who helped me grow professionally.

One of the catalysts to my work-life balance is when my now husband and I started dating. We lived in different cities and we were commuting to see each other almost every weekend. I negotiated to work remotely on Friday’s and return late-morning on Mondays to the office so we could spend our weekends together. After putting 30K miles on my car in a year, I had enough.

We were about to get engaged and move in together so I told my employer that I needed to be full time remote or I was going to leave. Working remotely was very unpopular with my division at the time – they had just spent beaucoup money to co-locate. They accepted me being full-time remote, with the exception that I spend 16 weeks a year at the headquarters and they would split the cost through a quarterly stipend.

After a year of that, I started a role with a new manager who was more flexible. I slowly decreased my travel time to shorter and less frequent visits, which were fully funded by the company. Then when COVID hit, my travel went down to zero.

In my new role, I am full time remote and likely will not travel much. Technology has been a blessing as well, as my entire division is remote, video conferencing is much more common and I’m able to get the ‘in person’ experience without the travel. I spend about ~50% of my workday virtually on camera.

My husband has also been remote for going on three years now. When possible, depending on our meeting schedules, we try to have three meals a day together. I try to take 30-60 minutes each day to make lunch. I enjoy cooking so it’s a nice break in my hectic work day.

We also try to wind down work at a reasonable hour and spend at least 30 minutes a day exercising. Over the past few years, we expanded our home gym so we have weight equipment and treadmill / exercise bikes so there is no excuse. When the weather is nice, we live close to a park and we’ll do 5-10 miles on our mountain bikes around the lake.

We haven’t had a real meaningful vacation in a couple years due to COVID, but we make more of an effort in general to “disconnect” from work when we are off.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

We have been slowly building up our dividend portfolio the last couple years, we have ~$50K/year of dividend income which we currently fully re-invest.

We also started making wine together as a hobby. I’ve always dreamt of owning a vineyard – so when my husband suggested we turn our hobby into a small business it sounded like a brilliant idea.

Much to the credit of my husband, we were able to get our winery endeavor up and running. We completed a one-year commercial winemaking program together, which was an invaluable way to make connections in the industry. We filed our licensing paperwork late-2019 and got approved in early 2020.

We were traveling in March of 2020 to a winery expo to connect with vendors and solidify our equipment purchases. Despite the uncertainty of Covid, we launched our business. We got started in our basement with some minimal equipment investments. However due to Covid, we were never fully able to pivot into our original business model.

Though we enjoy aspects of the winery, the realities of the earning potential versus our day jobs hit us and the time commitments seemed daunting. We would need to open a retail location and invest more of our personal time to really make the business a success. Our passion for the business fizzled.

In the two years of operations, we broke about even when you factor some of the tax advantages. With significant supply chain constraints in the wine equipment market, demand is high so we’re able to recoup all the original costs on our equipment plus a small mark up.

SAVE

What is your annual spending?

Being in Finance, I track our all of our expenses in detail each month. Our expenses vary dramatically year-to-year; however, we average ~$120K of expenses after taxes.

Since we both have executive corporate jobs, we have income in high federal tax brackets. Our blended federal tax rate is ~24%, state & local taxes at another 4%, plus Medicare and Social Security.

What are the main categories (expenses) this spending breaks into?

Our core expenses are ~$85K:

- $20K Home (property taxes, utilities, insurance, internet)

- $20K Groceries & Toiletries (… we don’t skimp here, we buy almost exclusively organic and fresh produce. We both love to cook and we host family/friends for dinner often)

- $10K Home Maintenance (our house is ~25 years old, we typically do a few upgrades each year in addition to expanding & maintaining our garden, plus my husband is a ‘do-it-your-self’er and likes to have the right tools for every job)

- $8K Healthcare/Fitness (employer healthcare insurance, fitness gear, peloton membership, supplements, and out of pocket expenses)

- $4K Car Expenses (normal maintenance, car wash, insurance, gas)

- $4K Dining Out (we eat out at high-end restaurants a handful of times a year plus 1-2 times per month we go out with family/friends)

- $2K Electronics (typical 1-2 devices are upgraded each year)

- $2K Lawn Services

- $4K Retail Purchases (clothing, shoes, fitness accessories)

- $1K Pet (premium dog food, supplements, and vet expenses)

- $4K Sundry/Gifts

- $6K Second Property – property taxes & HOA plus minor maintenance & repairs as needed for my mother-in-law’s townhome that we own

Our “Entertainment” bucket is ~$35K:

- $7K for Season Tickets for professional football

- $3K Concert Tickets / Events

- $10K Vacation (usually trips to see my family, Vegas, and 1-2 weeks beach vacation)

- $10K tied to other activities we enjoy, last year we bought new mountain bikes & kayaks and my husband upgraded his weight lifting equipment

- $5K Wine/Liquor…my husband is building a bourbon collection & we both enjoy high end champagne, not to mention we host family/friends often who also partake

This last year, we also spent another ~$30K to proactively replace our roof, gutters, and upgrade some of our kitchen appliances.

Do you have a budget? If so, how do you implement it?

As I am a finance nerd, I track all of our income & expenses every month down to every last Amazon transaction. We do set a target budget at the beginning of each year to rough out our spending, but we use this more as a guideline.

In the past, every month I summarized our spending by category and review it with my husband and set a budget for the following month. However, our income and our spending varied a lot month to month.

Now we spend a bit more freely as we’ve shown ability to save each month. I’m naturally a bit more frugal and rarely buy much outside of normal groceries & toiletries. I can talk myself out of almost everything. My husband on the other hand always finds something he’s keen on upgrading or a new project around the house.

My husband does much more of the day-to-day finance management and manages our investment portfolio. He also is responsible for paying our bills and manages the cash flow between our numerous accounts.

In lieu of a budget, once a month we talk in terms of our net worth, our ‘accessible funds’, and investments (mostly stocks) that we’re interested in pursuing.

Our accessible funds have been the key point of interest for us as my husband is interested in pursuing some career changes outside of corporate America…we would like to have more of a cushion of liquid funds to rely on in case he wants to start up or acquire a business.

What percentage of your gross income do you save and how has that changed over time?

We save between 55-75% of our take home pay.

It obviously helps that we both have big incomes, but we made it a point the last couple years to live on the take home pay of the lower of our salaries. Each month, we send money to our retail investment account.

We also save 100% of our variable incentives which is a large part of our total compensation.

In addition, I automatically contribute 8% of my salary to 401K while my husband contributes 6%. I receive 7% match from my employee (4% throughout the year and 3% at the end of the year as a one-time incentive). My husband now receives 6% employee match as they recently suspended his pension benefits.

What’s your best tip for saving (accumulating) money?

Spend less than you make (obviously!), plan for the future, and find the right financial balance for your lifestyle.

The one area we excel, unlike many others we know, is we like to plan ahead. We are looking at the long game, trying to accumulate wealth now, invest, and be ahead of the curve for retirement. Inspired by the FI/RE movement, we are very motivated to have our ‘financial independence’ and for us that means not relying on our big corporate paychecks.

In the past, we tried to “cut back” our spending to the point we were both just unhappy. We always bought the cheapest option and were never satisfied with the quality. Instead, we try to be practical, we live on one base salary, invest 100% of our variable incentives, max out on our employee 401K matches, pay off our credit card and send money to our investment portfolio every month.

Although it didn’t feel like we could afford it at the time, we bought our house which is ~1x our annual gross income and paid it off in less than 2 years. As a rule of thumb, I’ve heard your home should be ~5x your annual income so we could probably afford to upgrade. Though we dream sometimes of a bigger kitchen, an “in-law suite” when my parents come to visit, or a vacation property, we’ve been able to talk ourselves down. We like being able to live comfortably & know we can maintain our house properly over the long term.

What’s your best tip for spending less money?

Though we’re probably not the best couple to model as an example of frugality, I would say that we have always lived well within our means. In my early career still recalling my hourly rate at the bakery, I would still calculate how much time it cost me to make a purchase. That prevented me from a lot of unnecessary spending.

Since I am not much of an ‘impulse’ buyer, I usually tell my husband what I’m in the market for and he helps me research prices to get the best deal. Even when I’m at a store and like an item, I always check to see if I can get it cheaper online.

My only other advice – don’t feel like you have to be ‘pressured’ into conventional spending. My husband and I are very deliberate about where we spend money. For our wedding, we took a less conventional approach with only ~18 guest, opted out of frills like a wedding cake and an expensive wedding dress, and instead invested our money into renting a beach house for a week to share with our guests.

What is your favorite thing to spend money on/your secret splurge?

We definitely have an affinity towards fine wine and in particular champagne. I was influenced early into being a lover of wine, having traveled and visited vineyards in Switzerland, Spain, Italy and France. We had the fortune of visiting the Perrier Jouet champagne house in Epernay a few years ago with my husband’s family – a very treasured memory! There is nothing better than drinking bubbly with friends & family!

In addition, I got the travel bug early in my life. I spent a few weeks in France at 15, then a summer in Switzerland at 19 years old, studied abroad in Finland, backpacked through Europe after college, sailed in the Caribbean, and worked abroad…there is so much world to see! I don’t travel nearly as much as I would like today especially with Covid, but hope to reach financial independence early to help share my love of travel with my husband.

INVEST

What is your investment philosophy/plan?

I’ve historically been a buy and hold investor of the broad market index. My husband and I have errored a bit more on the conservative side the last couple years, we went to cash in our 401K right before the Covid market crash as we felt like to market was overvalued.

We have been easing back into to market, but mostly on specific stocks we want to own for now and those that have strong cash flows and historically paid dividends.

My husband follows the market & reads quite a bit of the market news. He often will bring investment ideas to the table. We often talk through companies and I review their annual report and some of the key financials, dividend payout ratios, cash flow, etc. We are definitely trying to build our retail portfolio of long-term investments we would like to hold onto and think there is a potential for future growth.

In my 401K, I prefer to hold a broad market index, putting in funds every month and will likely continue that path for my retirement savings.

What has been your best investment?

Hands down, marrying my husband.

He offers the best ROI on the market. 😉

What has been your worst investment?

I had put about 5% of my portfolio into one of my previous employer’s stocks, whose stock price tanked shortly after I left (….unrelated to my departure).

I sold it at the bottom and took a big hit to my 401K.

What’s been your overall return?

Personally, mostly being buy & hold investor in my personal 401k portfolio, I would say fortunate to have held on in the bull market over the first part of my career so roughly ~10-15% annualized return.

My husband is much more the catalyst of some successful investing…we recently bought into some energy dividend stocks before the big oil spike and have seen ~30%+ investment return over the last year + dividend income.

How often do you monitor/review your portfolio?

Formally, we review our portfolio once a month.

Both my husband and I watch the market daily.

NET WORTH

How did you accumulate your net worth?

I would say I’ve always been diligent about managing my money, keeping debt low, and living below my means.

During college – I worked multiple jobs, made sure I graduated within 4 years, applied for numerous scholarships and stipends, and saved money by living with my parents. I recall actually receiving a lot of judgement from some of my more privileged friends, who relied heavily on their parents for day-to-day living expenses and tuition, for not participating more in the college experience. Since I had to put in the work both in class and monetarily to get my education, it ensured a got the value out of the experience and not just the social aspects of college.

When I started my career, I did not save much. I contributed ~5% to 401K contributions to get my employer match. While I lived within my means and did not carry much debt, I prioritized experiences like dining out, nice apartments, and traveling instead of saving.

I did pay off my student loan debt 6-years after graduating college, but it was minimal as a result of working while in school. I always drove a used car. Over time, I started upping my 401K contributions to ~15% after each pay raise and slowly started building up an emergency fund.

When I met my husband, I had accumulated ~$150K in net worth. We merged finances early in our relationship. Finding a like-minded partner definitely helped create a compounding effect on our combined net worth.

The real crux of our net worth accumulation has been continuing to grow our earnings exponentially faster than we’ve grown our expenses. We live off of one base salary income and save 100% of our variable incentives or used it to pay off our house in less than 2 years.

My husband did inherit ~$120K from his dad’s estate when he passed about 6 years ago. We used that money later to buy a townhome for his mother. They were divorced and she was paying ~$1,300 a month on rent and working into her 70s without an end in sight. We wanted to ensure she always had a roof over her head and something we knew we could afford in she couldn’t pay rent. Thankfully, we had the foresight as when Covid hit, her business struggled and all her supplemental income dissolved with no ability to cover any rent. Other than that, we will not have any other inheritance and likely will need to support some of our families over time.

I also have a financial model that tracks our monthly net worth since we combined our finances over 7 years ago and projections by month for the next 3 years based on conservative assumptions around income, spending, investment growth, dividend income, and inflation.

Being in finance, I like to understand the ‘sensitivities’ of certain scenarios and what actions we can take to improve our financial position. Based on our current trajectory, barring any major lifestyle changes or market crashes, we should hit $4M in net worth by end of 2024.

You can see while our retirement funds go up every year, our current goal is to ensure our ‘accessible’ funds (retail investments & cash) grows substantially over the next three years. This is to ensure if we do leave our corporate jobs, we have access to enough funds to live until we can access retirement accounts.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

I always told myself earning wasn’t a big priority for me and cared more about the work experience than the compensation. In the past 5 years, I’ve really made moves to grow my earnings by networking with key players, building leadership skills, and working on projects that deliver results.

I’ve found the best success with automating my savings – putting a fixed amount to 401K each paycheck and now we direct a fixed amount to our retail investment account each month in additional to the full amount of our variable incentives.

I’ve been a fairly ‘passive’ investor most of my life, but I am certainly trying to educate myself more in this area.

As we look to the future, we would like to rely less on earning & saving and rely more on our investment strategy to return passive income.

My husband on the other hand has always been first a strong earner, he’s almost always had some side-hustle and has helped encourage me to grow my earnings. Though, in the past year or two, he has turned down multiple promotions offers at work to ensure he maintains some semblance of work life balance and keeps his stress levels manageable. He’s also a savvy investor and has always lived well below his means. Together, we’re a pretty great team.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

I’ve been fortunate that I’ve never much struggled with money. When money was tight, I’ve always buttoned down my spending to adjust to my incoming cash flow. I’d say our biggest struggle is dealing with lifestyle creep and balancing living in the now vs. the future.

As for lifestyle creep, there was a certain amount of stress it carried in the early part of our relationship. When we moved into our current house five years ago, I remember thinking what 31-year-old buy’s their first house for over half a million dollars!? Having relocated a lot for work, I had only ever rented. At times, the weight of a big expensive house and the upkeep felt daunting. As our earning went up and we didn’t increase our spending and aggressively paid off the mortgage, it created enough room where we now feel comfortable and don’t stress about money.

We also dabbled in starting our own business, but the time investment outweighed the benefits. We’re in process of liquidating the business and getting out break-even. While certainly we didn’t hit a home run, I learned many valuable lessons about what is takes to start a small business.

What are you currently doing to maintain/grow your net worth?

I’m committed to my corporate job for the next three years – due in part to the large long term incentive offer. There is also some room within my company to get promotion in the next 6-12 months so I will continue to work to grow my income.

We’ve also been working to invest all our extra earnings into some ‘passive income’, which largely consists today of dividend investments. We also constantly look at real-estate opportunities or are considering some real estate syndication deals in the future. My husband has quite a bit of success before we married buying and renting properties, but it doesn’t feel like to right time to enter the rental property market just yet.

Do you have a target net worth you are trying to attain?

Targeting three million in early 2023 (2.5 years after our second million).

Targeting four million end of 2024 (1.5 years later).

I will be comfortable when we hit ~$2M in liquid assets and ~$1M in retirement assets, which we are on track to get there by end of 2024.

My husband would also like to leave his corporate job, but isn’t yet ready to ‘retire’ from some type of work. He is much more of an entrepreneur and would like us to hit $10M Net Worth.

How old were you when you made your first million and have you had any significant behavior shifts since then?

I was 32 and my husband was 37 when we made our first million.

We initially buckled down for a while to tighten up our spending to try to get to the next million faster. We cut the cord with cable, started price shopping on groceries, dining at home vs. dining out….but found as our earnings and investments continued to grow so cutting costs to save was less of a priority.

We hit our second million (three years later) at 35 and 40 respectively.

What money mistakes have you made along the way that others can learn from?

Most of my mistakes have been around the ‘earning’ side. I’ve always been a hard worker and probably lacked some confidence in my abilities. I was underpaid for a number of years – but didn’t do my due diligence to even be aware of how underpaid I was. I would strongly recommend (even if you’re happy in your job) to network with recruiters and apply for jobs to get a sense for the market.

I now subscribe to market reports about salaries that are updated annually to help me be aware of the benchmarks. I’ve found a lot of success staying with companies for a long time, but I have jumped companies 2x in my career. There are pros/cons to changing companies, I would strongly recommend building some credibility somewhere first and having a strong professional network rather than being a job chaser.

What advice do you have for ESI Money readers on how to become wealthy?

I would attribute a great deal of success just on having a strong foundation – I appreciate the value of a dollar and have been somewhat conservative about money my whole life. I’ve never carried credit card debt and I’ve aggressively paid off all my major purchases early (cars, student loan debt, and mortgages).

Secondly, my net worth is largely attributable to being with an equally minded and strong contributing partner, my husband. We’ve been together 7 years and you can see we’ve gone from $0.5M to $2.7M with a path to $4.0M in the next few years.

Though we are not competing, I’ve had a successful benchmark in my husband (5 years my senior) to try to hit earning milestones in line with his career path. We are able to challenge each other to earn what we’re worth and support each other to make career moves because we have the backstop of the other and live on less than one of our base salaries take home pay.

FUTURE

What are your plans for the future regarding lifestyle?

The future feels a bit uncertain….as I am on the younger side. I’m committed to stay for another 3 years through the end of my retention bonus in my corporate America job.

My goal is by 40 to feel ‘financially independent’ enough so neither of us feel obligated to work.

I would like to continue to increase our annual dividend income (or passive income) to ~$100K to ensure we felt like we could easily cover our expenses without having to substantially change our lifestyle.

I assume neither one of us will stop working completely in the near term.

What are your retirement plans?

Being that I’m only 36, retirement is not an immediate goal of mine. I probably wouldn’t be happy being idle in the near term without something meaningful to contribute.

My husband doesn’t have a restful bone in his body, so there is almost no chance he’ll ever really stop hustling, even if he ‘retires’ from his corporate job.

I enjoy evaluating investment deals and preparing financial models. My husband thankfully is always coming to me with potential small business ideas, rental properties, or companies to invest in or evaluate. Eventually, I think we’ll find the right fit for us that will allow us to feel more comfortable about leaving our corporate jobs and we’ll pivot.

Our main priority over the coming years is to have more autonomy over our time.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

Our biggest concerns surround our aging family and our health. As my husband’s father passed from lung cancer not long after retiring, we are always reminded of how precious life can be. Time is the big uncertainty.

We’ve made some changes in the past few years to improve our health by managing our weight, prioritizing working out, eating better, and managing our work stress. We used to have debilitating stress in our careers – but we’ve really taken meaningful strides to improve our work life balance & reduce our stress.

The biggest wildcard for us is probably providing for our families…neither of our families will retire with any substantial financial backstops. We are already partially subsidizing my mother-in-law’s living expenses and we worry none of our siblings have invested much in the way of retirement plans.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

My mom used to joke that in my youth, my favorite activity was managing the cash register during her annual garage sale. Given my career ended up being in Finance, numbers and money always seemed to make sense for me, even at a young age.

Being the youngest of three kids, my siblings seemingly grew up without some of the realities of money. While my siblings got a car when they turned sixteen and a paid for college tuition bill, my parents treated us on a ‘need basis’. I didn’t always qualify as the most pressing need – especially when it came to money matters. It absolutely made me a more responsible financially self-sufficient individual than my siblings.

Who inspired you to excel in life? Who are your heroes?

I am incredibly grateful for my parents for treating me as an individual and fostering my talents differently than my siblings. Although my father grew up with some privilege, my mother was not well off growing up. I got a good balance and work ethic from both worlds, an appreciation for the value of money and also value in the finer things in life. I’m very thankful to my parents for giving me such a grounded upbringing.

I also am well balanced by my sister, who is a very generous and the yin-to-my-yang so to speak. She may have grown up believing in the laundry fairy, but she makes magical moments out of the everyday. She’s one of the most precious gifts in my life.

I am also always inspired by my incredible husband. He is dependably honest, hard-working, and my very best friend. He is my moral compass, who has an impenetrable belief about right and wrong. He is also an over achiever – someone who also challenges me to rethink what is possible and always strives to be better. I am incredibly fortunate to have found my soul mate in someone who amazes me every day.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

- The Millionaire Next Door

- Rich Dad, Poor Dad

- The Little Book of Common-Sense Investing

I would say reading about different approaches to building wealth and different investment strategies have been helpful guidepost for me as we really started to accelerate our net worth growth. It’s always good to see different perspectives and keep balance your strategy until you finding the right “fit” for your situation.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

While I enjoy giving back, we don’t give to charity very consistently. Every now and then, we might donate to worthy causes as we see fit but we don’t have a definitive strategy around financial donating.

We have provided some ‘life coaching’ to friend’s children who are approaching college. We’ve shared our perspective of good college majors, realistic job & salary expectations post graduations, and realities of cost of living & retirement planning.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

We haven’t really discussed this yet given our age and we do not have any plans for children. Right now, our beneficiaries are listed as each other.

My sister is the only one of our siblings with children, so likely they will inherit some of our estate. Something to consider down the road…

great job crafting a fabulous lifestyle in a high cost region. Love the way you’ve worked on making sure you’re paid what you think you’re worth. Also, the consciousness to minimize and basically live debt free at such young ages is admirable. Any plans to leverage an HSA, if eligible? Great write up! thanks for doing it.

Thank you for your kind words.

While at some point we likely will take advantage of an HSA – at this particular moment we wanted to focus on building up accessible funds for us to consider some future investment opportunities that may require capital we can easily access.

Very nice story and chock-full of common sense moves that have really energized your savings and investments. I did have one question about your federal tax bracket. How are you managing to stay in a 24% bracket with combined incomes over $700K? You must really be creative with some of the deductions to get it that low.

I wish I had some crafty tax advice to share…

Primarily – we were fortunate last year as a result of some paper losses on our small business venture. We will feel some pressure this year as we will have a gain on the sale of the business which will result in tax burdens.

Also not discussed in my write up, but my husband had 4 weeks unpaid as part of company wide MULA during the pandemic which resulted in some lower than normal take home pay last year.

OK, but the 24% tax bracket ends at around $330,000 so you would have needed some pretty significant write-offs if your combined income was over $700K. It doesn’t really matter. I was just curious how you could be in such a low tax bracket with such a large income. My guess is you were most likely in a higher bracket and may not have realized it.

One other thought just crossed my mind. I am talking about your marginal tax rate and you may have been referring to your effective tax rate.

Congratulations! But I’ll admit, I’m puzzled. If your career is in finance, and you track your budget monthly as well as watch the markets…how do you not know your investment returns to the dollar? I don’t budget, but I track our investments and keep the data on a spreadsheet with less than an hour effort per month.

To be perfectly honest – I see my investment in stocks & 401K as long term so I’m not as concerned about the annual returns as a metric at this moment particularly with the recent market volatility. We’ve been focused on measuring some key areas we want to control. I have been more focused on building up balanced portfolio for our risk tolerance and building up some dividend income. Certainly something to consider for future – but really my measure of success is watching my net worth grow every month and ensuring I build up strong foundation of long term assets.

congrats on what appears to be a well crafted, intentional lifestyle. how did u go about paying off a house in two years? what actionable steps you took in doing so? Large down payment then bonuses? I would love to learn. Also, no debt so young is admirable for sure. Any thoughts on using leverage to reach your goals faster, especially considering a stretch networth goal of 10M if I interpreted that correctly? Seems extremely debt adverse at young ages, but you guys ultimate number is still pretty high. Can you comment more on this. I think you guys are crushing it and will get there w time.

For the mortgage – we put down 20%. Part of our move was covered by Corporate relo, so we put some of the excess funds towards the mortgage. We put 2x towards the payment every month until it was paid off. At this time, we were not earning as much, but it was important to us to feel weighted down with debt. We also took 100% of our bonus payments including my retention bonus and our variable incentives towards the mortgage. For those major contributions- we also recasted the mortgage which lowered the overall interest we paid.

Your observation about us being debt adverse is fair! This likely stems from some of our family dynamics – my husband didn’t grow up well off and our families & friends have been classic examples of using debt in excess to fund an unsustainable lifestyle. It was a milestone for us – a goal to work toward and feel like we had control over our financial future.

In regards to future leverage, we are setting ourselves up to have access to large amount of capital in the next couple years if needed. We have an equity line on the house and access to margin in our retail accounts – we will lean into some leverage when we find the right investment, as we have considered acquiring a business at some point down the road or a multi-unit investment property.