Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in April.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I am 42 and my wife is 39.

We’ve been married for 12 blissful years.

As Warren Buffet has said, his greatest investment was an engagement ring.

Do you have kids/family (if so, how old are they)?

We have two beautiful children, ages 7 and 8.

They continue to be a joy for both my wife and I, seeing them grow up and sharing in all their new experiences.

What area of the country do you live in (and urban or rural)?

We live in a suburb of a large northeast city.

What is your current net worth?

It still shocks me to this day that it’s $9 million.

I remember my net worth exceeding $1 million for the first time at age 30 and it took forever. The next $8 million flew by.

Some well-timed and very stressful investments during the Covid lock down in early 2020 added about $2-3 million to my net worth.

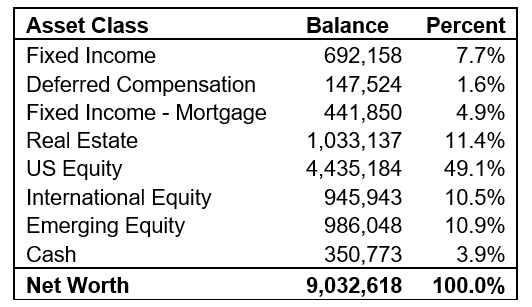

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

Below is a breakdown of my net worth by asset allocation. All numbers throughout this interview are as of 1/31/2023.

I have a 600k mortgage against my primary residence but that is netted in the real estate figure below.

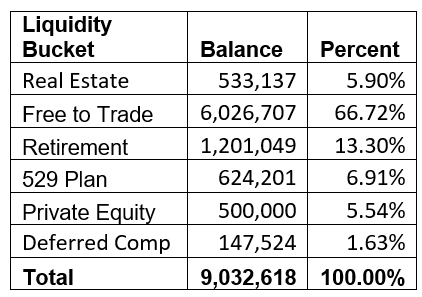

Below is another breakout by liquidity buckets.

For example, the ‘Free to Trade’ bucket is mostly stock index funds in taxable accounts that I can sell tomorrow and convert to cash.

Private Equity is a multi-family Opportunity Zone fund (grouped into Real Estate above) that I plan to hold for 10 plus years to achieve the maximum tax benefits.

The retirement bucket is a combination of 401k and various types of IRAs such as Roth, Traditional, and an Inherited IRA (about $280k in value).

EARN

What is your job?

My wife is a care giver for our children, a severely underestimated job. She should be making the big bucks.

I am a Senior Vice President in the investment field.

I have been on a trading desk for most of my career. It certainly has its pros and cons.

The pros are the high income, intelligent conversation with many market participants, and what is likely to be both a pro and a con, the excitement of the ups and downs of the market.

The negatives are the stress and long work hours in the first half my career required to get to my current level.

What is your annual income?

My annual income fluctuates based on my workplace portfolio returns.

It typically has averaged $600-700k total compensation over the past ten years, but I had one exceedingly good year at $1 million.

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

In my 20s I worked long hours, but with the long hours came rapid career advancement and salary growth. My total salary for my first year was $62k in 2003, the following year it jumped to $140k and stayed in the $125k-200k range for the next 5 years.

In 2009 it jumped to $450k then to $700k the following year.

As mentioned, over the next 10 years or so it’s averaged $600-700k. In the early years, my tax accountant was always shocked when my salary would double. It was always fun to see his reaction.

What tips do you have for others who want to grow their career-related income?

I was told early on that the best way to make yourself valuable to a company is to make yourself irreplaceable. You must remove the words “No, I can’t” from your vocabulary. I recall in my mid-twenties that I wrote some visual basic code for an excel model. I taught it to myself with a lot of web searches and trial and error over the course of a few evenings. People value innovation, the ability to stand on your own two feet, and simply to get the job done. Because I feel it is so important, I will mention it again, you must replace the phrase “No, I can’t” with “How can I?”

Always look for ways to improve yourself and your work. I have read every single annual letter by Warren Buffet, no small feat at 1,000 pages of tiny print, and many articles and books about Berkshire Hathaway. Charlie Munger and Buffet said that there are a few qualities that make investors stand out and surprisingly it’s not intelligence. It’s the ability to control your emotions and to constantly learn new things. If you always read and strive to know more than the guys sitting across the table from you, the money will follow.

What’s your work-life balance look like?

Today it’s 8:30 am to 5:30 pm, Monday through Thursday and I leave around 4 pm on Fridays.

It’s relatively short hours in my industry but I am not motivated by the money anymore. My time is far more precious, and I love to be around my family.

I am considering a career switch, but I struggle to find a suitable next move. I could retire but I am fearful that I will be bored and lack purpose. While I know many have praised retirement, I also know of others who have struggled.

But the good news is that I am focusing more on living life and actively seeking what’s next. As opposed to mindlessly stacking more money onto the pile.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

Yes! A matter of fact I do and I am quite proud of my diversified income stream.

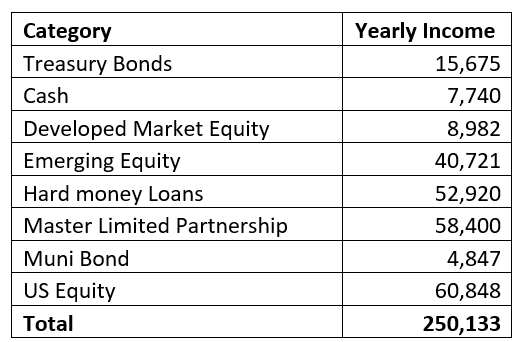

I currently earn about $250,000 a year from my investments, not including any appreciation in value.

Below is a breakout of the sources and explanations of some of the buckets.

The categories treasury bonds through emerging equity are bond interest, money market interest, or stock dividends.

The hard money loans are 12-month loans for the purpose of buying, fixing, and selling real estate (commonly referred to fix and flip). I lend to a developer/friend of mine who has spent his entire career in the space. While the returns of fix and flip loans can be attractive, I would caution people to do your homework before trying to make such investments. There is unfortunately a lot of fraud out there and this type of investment takes a lot more leg work than just buying an investment on a brokerage account.

Master Limited Partnerships or MLPs are a tax efficient way to invest with taxable dollars. The distributions are treated as a return of capital and therefor are tax deferred because they write down your basis. Some google searches will do a better job of explaining the pros and cons of such an investment, such as it requires investors to file K1s. It’s worth researching if you are unfamiliar with the investments.

Muni Bonds and US equities are bond interest and stock dividends.

I devised this investment to be tax efficient. The hard money loans are done through my self-directed IRA and equity index funds distributions are qualified dividends in my taxable accounts. I strongly propose index funds for a variety of reasons:

- Extraordinary low fees. As the saying goes, returns come and go, but fees stay around forever. You should target expense ratios of less than 0.25% or 25 basis points.

- I found that when investing in individual stocks it was hard to put large amounts of money to work. Since the chance of an individual stock going to zero is so high, it was always a small amount of my net worth. In 2020 when the markets were at their lows, I felt justified investing 10% of my net worth at a time since the entire S&P 500 going to zero is a very small chance. If it does go to zero, money will likely be the least of your concerns. At work, we call this high conviction trades. It takes a lot of work and research to feel confident about an investment and its long-term return rate. Those moments don’t come very often. You may only experience 10 of these moments in a lifetime. When it happens, you need the ability and confidence to invest large amounts of money.

SAVE

What is your annual spending?

First off, I don’t believe in budgets. I am a strong proponent of the pay yourself model.

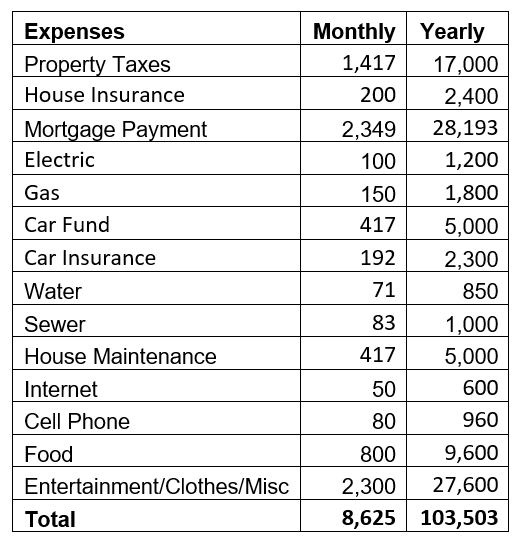

Below is a sample budget that I follow to know how much I need available. Using the below numbers, I know that I need $8,625 a month and any dollars in excess of that amount should be swept into a dedicated savings account for investment in the beginning of the month, not the end.

In my case, my salary is derived in two parts. Base salary and bonus. My base salary is $175k a year. I will live off my monthly base salary and invest my entire bonus.

As for the spending, it’s always been easy for me to keep spending in check. I grew up in a cost-conscious family where everything that was purchased was on sale. I didn’t even know what the acronym MSRP (manufacturer’s suggested retail price) was until I learned that a co-worker that I met in my 20s paid it.

Who pays full price?! Clothes were bought at the outlet mall. Today, food is purchased on sale by looking through the weekly flyers. We have a clothes swap with families in town where we give away clothes as the kids outgrow them and take them from other families who have children older than ours.

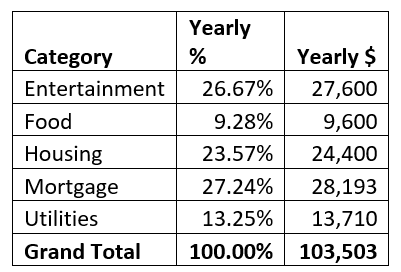

While the below may seem like a large budget, it’s mostly because of the expensive housing cost where we live. My high paying job is in an expensive city. To have a reasonable commute, homes are expensive in the suburbs. If you exclude the first three housing items, the yearly budget is $56k a year.

On a side note, I don’t see my mortgage payment as an expense. I refinanced into a five-year arm at a rate of 2.125%. I then took that equivalent amount of money and invested into treasury bonds at 2.75% that will mature when the ARM rate increases, thus making my mortgage profitable in a low-risk investment. In hindsight I should have waited longer for rates on treasuries to increase, but investing doesn’t come with a magic fortune tellers’ ball.

What are the main categories (expenses) this spending breaks into?

See below. If I were to retire and pay off my mortgage as I plan to, my health insurance would likely be in line with my mortgage payment, thus this budget would represent a retirement budget as well.

Do you have a budget? If so, how do you implement it?

I don’t have a budget per se, more of a guideline.

My wife and I have been living within our means for years and we are careful not to increase spending as my income rises.

Our spending picked up significantly once we had kids, mostly due to moving to a bigger home.

I strongly suggest a pay yourself model by moving money into a retirement account then a separate investment account to maintain discipline.

What percentage of your gross income do you save and how has that changed over time?

Great question. I used to think about this more when I was younger, but since I have been on auto-pilot for many years living within my means I have lost sight of this fact.

Doing the math, I am typically saving 80-85% of my gross W2 wage. If you consider that my living expenses are below my investment portfolio income then I am saving more than 100% of my gross income, not taking taxes into account.

My wife and I have been debating spending more money for the past year but struggle to do so. We started taking the kids skiing this past winter to local mountains and doing some local trips with hotel stays.

It’s interesting, as my wife and I have started spending more, it has added stress to our busy schedule. It takes time to plan trips and to go on them. While it’s fun and creates great memories, we have noticed that we have less time to decompress and enjoy our home. We are actively working on finding the right balance.

What’s your best tip for saving (accumulating) money?

Pay yourself first. Period. That is the most important thing anyone can do.

There have been very few investors that can beat the market, but saving a large part of your income by sweeping money into a savings account before it hits your spending account is well within your control. Simply take that money and invest it into a broad based index fund such as VTI. It really is that simple.

What’s your best tip for spending less money?

Spend time outdoors. Enjoy the simple things in life as I have found them to be the most rewarding.

An outdoor hike, time at a beach, teaching your child how to play baseball, or building a snowman with the kids. To me those are the greatest memories.

What is your favorite thing to spend money on/your secret splurge?

I am currently attempting to spend money on things that will save me time, such as hiring a lawn treatment service to do weed control and fertilizer.

It’s a catch 22 for me, since I enjoy working on my own house and fixing the various items that always need attention, but time is my most precious commodity now.

INVEST

What is your investment philosophy/plan?

When I was younger it was to be smarter than the next guy by researching stocks and other investments. I learned the hard way that it is difficult to outperform the market.

I now invest in broad based index funds and concentrate my energy elsewhere.

My advice to people early in their saving and investing career, you will see far greater returns by investing time in your career and being prudent in your spending than you will by trying to outperform the market.

Focus on the E and S of ESI, the investing part just takes discipline.

What has been your best investment?

- Engagement ring.

- House to create memories with my family.

- Education, equally formal and informal by constantly reading books and researching online.

- My health.

- I bought $400k worth of an energy focused ETF at the end of 2020 which is comprised of oil and gas companies. It quickly went to $300k in a matter of weeks. Talk about gut wrenching, how to lose $100k in less than a month! It then grew to $957k by early 2022. Wow, I still can’t believe it. At the time there was so much uncertainty, and the world economy was shut down. I figured people are going to start driving again at some point and when they do, they need gas. The diversification of the ETF holding many companies gave me the confidence that I would not lose 100% of my investment, it was simply a matter of holding on until one day when the ETF would go back to its pre-pandemic level.

- On March 20th, 2020 I decided to invest 10%+ of my net worth, wow was I nervous. I invested $600k, super funding my kids 529 plans with a $150k investment for each kid and the other $300k into my taxable account. The following business day I invested another $100k. That $700k doubled in 2022 when the market hit its all-time high. How did I pick the 2020 bottom? It’s better to be lucky than good. But I wasn’t trying to pick the bottom, for me it came down to using the S&P 500 cape ratio (more on this later), which estimated that the next ten-year stock return will be 5-7% annually. Since my conservative plan of a potential early retirement only used a 2-3% safe withdrawal plan, I took the plunge and invested.

What has been your worst investment?

I lost about $60k buying a single name stock. I purchased largely on the fact that a well-respected private equity fund bought the company. I assumed they would turn the company around and make it a success. To my dismay, the private equity company issued a lot of debt in bond offerings and additional stock sales. When there was nothing else to sell or finance, they filed bankruptcy that wiped out the common equity.

Ever since then I learned to stop trying to beat the market and just invest in the market. It’s far safer. While it was an expensive lesson, it gave me the confidence and discipline to invest larger sums of money in 2020 which turned out well for now.

I also lost $50k on a fix and flip project that went wrong in many ways. Again, an expensive lesson but I don’t regret that one as much as it was initially based on sound logic, just unfortunate execution and market timing.

What’s been your overall return?

I keep close track of this. Since I am in the investment field, I enjoy calculating returns, especially when it’s a return on my decisions.

The below is inclusive of my savings from my income, thus they are not purely investment returns. It’s a combination of earning, saving, and investing.

At the end of 2022, I am proud to have kept my net worth flat in the market downturn, thus the 0% in the 2023 line.

I did that with some active trading and selling my oil and gas ETF investment and investing the gains into an opportunity zone fund to defer the long-term capital gain tax until 2027.

My savings from income in 2022 also helped offset losses.

How often do you monitor/review your portfolio?

I do a deep dive once a year, but I am always monitoring the market and making decisions accordingly.

I keep most of my investments in a separate brokerage account and rarely check it. I have the password hidden away. It’s a chore for me to log into that account. This helps me stay disciplined not to overact in a market downturn.

There is nothing more painful than checking your brokerage account daily in a market downturn and seeing it drop by thousands if not tens of thousands a day. This is my trick for overcoming those negative effects that can come from panic selling.

NET WORTH

How did you accumulate your net worth?

I grew up in a blue-collar family. While my parents were financially responsible, worked hard, and did a fantastic job at saving, they knew nothing about investing. Without realizing it, I was following in their footsteps in saving and not investing.

Then in 2017 I started my own financial blog, which has since been hacked and I let it shut down. I was only 6-9 months into the blog and I have all my articles saved, but it was sad not to be able to go to a website anymore and review my work.

The reason I mention this blog is because up until that point I only read investing books but never “taught” investing. The act of writing how to invest really helped me develop a plan. Prior to 2020 I felt that stocks were expensive given the long market run up.

Again, I use the S&P 500 Cape Shiller measurement as my guide, which I learned in the book “A Random Walk Down Wall Street” which I have read 2-3 times. Luckily, I stayed disciplined and was sitting on a lot of cash when 2020 came.

While investing most of my net worth in 2020 turned out great for me, I did the math, and I would have made more money if I would have invested into VTI consistently every month for the prior 10 years.

What’s the lesson? Pay yourself first by investing monthly into a broad-based index fund. Over the course of 10-30 years, you will be a wealthy person.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

Likely the earn, followed by the save.

In hindsight investing is easy if you do it consistently monthly and don’t try to time the market.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

I didn’t necessarily hit road bumps, but I did endure a lot of stress and long work hours in my 20s.

It’s important to not only focus on work but all aspects of your life. I luckily learned this in my 30s and not in my 60s.

What are you currently doing to maintain/grow your net worth?

I monitor my portfolio and trade here and there for fun, but I leave 80-90% of it untouched. Like the old infomercial for rotisseries said, “Set it and forget it!”

The fix and flip loans that I make take a lot of active work but that’s with a friend and we both enjoy working together.

The active sale of the oil and gas ETF I mentioned before was largely because I did not enjoy having so much of my net worth in oil companies given the environmental concerns. While I am not an ESG investor, I am still conscious of companies that may be harmful to our environment.

Do you have a target net worth you are trying to attain?

When I was younger it was $20 million, but that was before I knew that you could live on much less and still be very happy.

I am happy with my net worth right now. With my goal of being financially independent complete, my next project is to figure out what’s next.

My goal was always to create an income stream to retire but I never gave much thought of what retirement would entail until the past couple of years.

Part of the reason why I am writing this interview, away from hopefully helping others, is I am doing something different in hope for some insight. I always use the following quote by Albert Einstein as a guiding principle, “The definition of insanity is doing the same thing over and over and expecting different results.” From this interview I hope to learn from others who have become financially independent and what they have done next to have a purpose.

How old were you when you made your first million and have you had any significant behavior shifts since then?

I made my first million at thirty years old. My behavior did not change.

For my lifestyle one million is not enough to retire, I fall into the Fat FIRE camp.

What money mistakes have you made along the way that others can learn from?

I wish I had invested consistently in index funds monthly from the start. I wasted a lot of time, energy, and money trying to pick stock winners.

Remember a loss is not only on investments that you make, but also on investments that you don’t make or when you sell too early.

Stick to index funds and never sell them.

For every home run stock that you read about (Amazon, Tesla, etc.) there are countless money losers. Concentrate your time on earning and saving, the investing is far easier than you think.

What advice do you have for ESI Money readers on how to become wealthy?

Never stop learning.

FUTURE

What are your plans for the future regarding lifestyle?

I am debating that now.

I have researched retirement a lot and I don’t want to make the mistake of being bored in retirement. I like the idea of a semi-retirement — getting a less stressful job, with less hours, that has an impact and purpose that I can be proud of.

On one hand, people may say that it’s a poor example for your kids to not see you work hard. I am leaning towards the camp of what a great role model I will be spending more time and being present with my kids. Afterall, what type of role model is never home?

I am contemplating a few areas of work post my current career, ranked in order of my top choice being first.

- A Registered Investment Advisor (RIA) where I can help people build a responsible financial future. Many friends and family often ask me for financial advice, which is a nice vote of confidence. How great it will be to teach and help those who need it most to avoid all the pitfalls of consumerism. Do any readers have advice on career satisfaction in this line or work?

- Becoming a teacher on financial literacy. Like my goal of helping people as a RIA, I can teach people at the high school or college level before they even start their work careers.

- Fine woodworking. A big contrast between my first two choices. I worry about this field as it may be solitary and will get more difficult on my body as I age, but I loved working at a cabinetry shop in high school and college. Perhaps I will leave this as an awesome hobby.

- Some type of business owner involving the outdoors. Perhaps owning a winery.

- Maybe even starting a blog again, this time with better anti-virus software 😊.

What are your retirement plans?

My kids will certainly keep me busy since they are still in elementary school.

But I am a planner, and the kids will grow fast and 10 years from now won’t need my time as much. Thus, I am trying to find a social and purpose filled way to occupy my time, as listed in the previous response.

Any other ideas on careers where I can help people will greatly be appreciated in the comments.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

From a financially responsible sense, my concerns are health care, but I have enough income where I can buy expensive health insurance if that will alleviate my fear of having inadequate insurance. My family and I are healthy, it’s just the unknown that I am trying to solve for. Semi-retiring into another career can alleviate this.

My biggest concern is being bored in retirement and leaving an interesting and high paying career. Although the stress of my current career is not good, and I will likely be healthier and sleep better doing something else.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

I have always loved investing. I bought my first stock as a teenager that quickly went to zero after they filed for bankruptcy. I used to watch the financial ticker on TV to see stock updates.

During college I took every finance class offered and post college I read financial books in my spare time. My financial knowledge of retirement planning and investing is largely from the books that I have read, while my financial discipline on emotions is from my work career and temperament.

Who inspired you to excel in life? Who are your heroes?

My grandfather grew up during the great depression and taught me at a young age that price and value are separate components. Price is what you pay, and value is what you get. My father and mother have incredible work ethics that they instilled in me. This combination of hard work and focusing on value has gotten me to where I am today.

Away from family, Warren Buffet has taught me a lot about investing and life. Most people only see Buffet’s financial lessons, many do not see his life lessons. Just to name a few he has always lived in the same house, loved his wife intently, and did not give in to lifestyle drift (at least for a multi-billionaire). Warren praises others while taking little credit for himself and he spends his time on what he loves.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

I have many, but to narrow it down, it’s all the popular ones that most have already heard about. Most are financial discipline 101.

- Rich Dad, Poor Dad – The author’s definition of rich vs poor can also be used to define financial independence. The poor work for their money and the rich has their money work for them.

- Random Walk Down Wall Street – Many great lessons including asset allocation, passive vs active investing, and projecting equity returns 10 years out using the S&P 500 Shiller CAPE Ratio.

- The Simple Path to Wealth – Written by a blogger. For those who want a comfortable retirement one day but don’t want to learn about investing, this book is likely all you need.

As a bonus, Poor Charlies Almanac by Charlie Munger offers perspective from Warren Buffet’s partner at Berkshire Hathaway. While Buffet may get the spotlight, he would not be in the top 10 richest people without Charlie Munger. The book is a compilation of speeches and writings from Charlie that are insightful on a lot of different topics. The book is equal parts investing and psychology.

I also recommend people learning about Stoicism as a form of a life plan. There are many books on the topic. The intent of pointing this out is that you can’t just focus on your finances, life’s relationships with other people and yourself are far more important.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

I do give to charity, but not as much as I should.

I have been so focused on becoming financially independent that donating a large amount of money will delay my goal. I do hope to give back in retirement in ways discussed above, by teaching others.

I have also held various volunteer positions in my community where I have given my gift of time. I enjoyed learning the concept of the three T’s years ago when it comes to charity. The gift of Time, Treasury, and Talent.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

I don’t plan on leaving a lump sum to my kids. It will either be a small amount with the rest going to charity or perhaps the inheritance will be phased over some certain metrics. Such as a trust that matches dollar for dollar on their savings at certain ages, so I can continue to teach financial prudence after I am gone. This would apply if I passed at a younger age, but the concept may apply to grandchildren.

The book “Die with Zero” has an interesting viewpoint on inheritance. One should distribute their inheritance while they are alive and when children or others need it most, such as a down payment on a house, vs a lot of money when they are in their 50s and don’t need it. This plan will be a work in progress as I get older.

An incredibly well articulated and comprehensive journal of your journey! Thank you for sharing so many details.

Congrats to you and your wife!

Thank you so much for the kind words. I have always felt that writing was a weakness of mine and your positive comment means a lot.

Should look into becoming an RIA.

After I retired, someone suggested to me to get Securities Licenses, which I did, but I only offer Syndicated offerings; no stocks and bonds; it appears you can offer all and HELP a lot people out there, that’s what I’m doing now and I don’t have an office, just work from home.

Hi Pete, Thank you for reading the interview and providing feedback to my question. Does being an RIA offer you enough social and rewarding interactions as you want? Can you elaborate on syndicated offerings? Are you independently a RIA or through a company? Also, what is your time flexibility like? Apologies for all the questions, but as noted it is an interest of mine. Much appreciated!

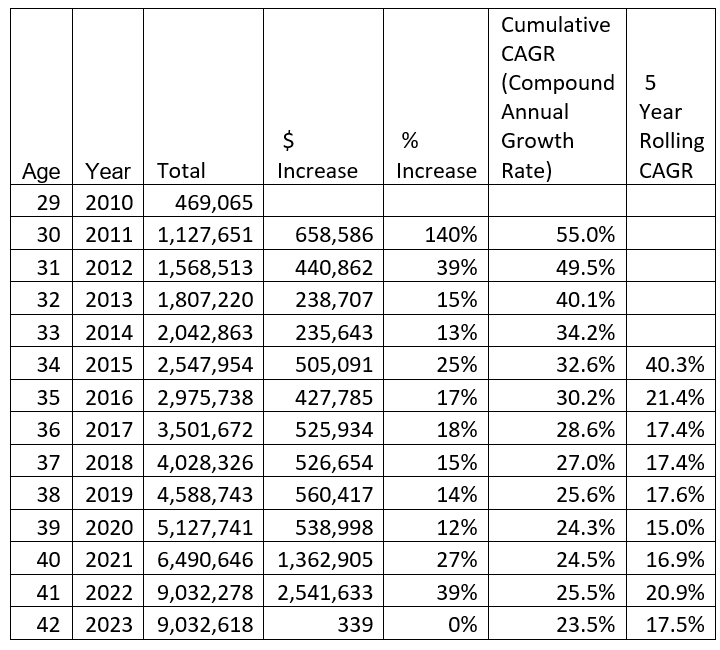

How did you go from $6.5mil net worth to $9mil from year 2021-2022? I must have missed that detail in the interview.

Yes, I’m interested in the answer too. Part would be your salary, and your energy ETF, but the remainder was the market? Was there some timing of the market there? I didn’t go back to analyse, but I didn’t think the market at that time would make up the difference?

Hi Stan and Clay,

Thank you for reading and commenting. First, a slight error on my part. The year 2021 net worth should be 7.5mm. In my sheet for that year I was including the potential tax liability on my unrealized gains.

Let’s ignore 2021 and focus on my gains from 2020 (5.1mm) to 2022 (9mm). I have the 3.9mm gain over two years accounted for as follows.

Bonus (after tax cash) = 750k

Equity Gains (pre-tax) = 2.35mm (largely because of dip buying during covid lock down and strong equity gains that followed)

Dividends and Bond Interest = 242k

Gains on Real Estate = 185k (this is conservative)

Mortgage Interest Received from Fix and Flip Loans = 240k

That leaves about 130k unaccounted for. While that seems like a substantial number to not have identified, let me please remind you of my investment philosophy. I have learned over the years that focusing on every detail has increased my stress level and not necessarily my returns. I focus on the medium/big picture and devote that extra capacity on items where I will get a greater return. Thus my ‘lose’ accounting in this case. Also, it is for my personal records, not like I am posting this for the whole internet to see….

Thank you again for commenting.

fantastic interview and very, very impressive numbers. Even at such a high salary those balances are quite strong.

re buffett, clearly the man knows how to allocate capital and turn a penny into a few billion, but i’d be careful about lionizing his commitment to his wife too much. The dude openly cheated on his wife and embarrassed her right out the door.

https://www.businessinsider.com/warren-buffett-marriage-wife-2017-10

he’s also a big fan of you (and me) paying a massive inheritance tax, while carefully structuring his own estate to ensure he never pays a penny (granting the bulk of it to bill gates foundation so as to avoid the very inheritance taxes he’s so passionate about the rest of us paying.

that aside, congrats on a truly impressive net worth and for remaining as grounded and family-focused as you have. as someone roughly a decade older than you who retired last year, I can tell you that if I could have at your age i would have. The time is so much more important than that next/tenth million dollar stack. well done sir.

Hi MI-121,

While I have no personal connection to Warren Buffet and I only know about him from his writings and interviews, my recollection is that Warren’s wife left him. She wanted to pursue a singing career and told Astrid (his new wife) that she should move in with Warren to take care of him. His former wife had said that Warren was incapable of changing a light bulb and needed someone to look after him. While I hope am correct as it would be upsetting for a man that a view in such high regard to have cheated on his wife, I do not know the real answer.

Separately, thank you for your kind words and advice. I have heard many times (through reading and firsthand) how people wish they would have retired earlier. One of my greatest weaknesses is a fear of making a mistake, thus my cautious approach to actually retiring. Understood I can always go back to work, but in my line of work it may not be that easy.

On the estate tax. The Patagonia move was very interesting. The guy will be no tax and get to retain full control.

https://www.bloomberg.com/news/articles/2022-09-15/patagonia-billionaire-who-gave-up-company-skirts-700-million-tax-hit

Thank you again for commenting and the congratulations! It feels great to set goals and achieve them.

Great work! While you are quite calm in your descriptions of the moment, I can only imagine how stressful some of those bigger bets were at the time. While I doubled down on a few things during Covid, I didn’t have enough cash on hand to go as big as you. I somewhat wonder if I would have had the conviction level required for that.

Fortune favors the bold, and you have EARNED the opportunity to reflect. Given your background, you are far beyond ever needing more money at this point, and I suspect you know that deep down. It is sometimes easier to make a leap when you are the master of the environment, such as when you established your investment positions. It seems you are experiencing the other side of that coin when you can’t (with certainty) know what will make you feel purpose and happiness without work.

It’s a big leap, but I haven’t yet met someone who wasn’t happy to have taken it. I hope you enjoy the opportunity in front of you and use it to the fullest of its potential.

Congratulations!

Hi MI-296,

Thank you for your congratulations. Yes! Quite stressful. While I felt confident in my conviction, that did not take away the trauma level amount of stress I felt. Who knew that just a single mouse-click on a little ‘confirm’ bubble on your screen to put in a trade can cause so much tension. I feel sick to my stomach. But you are 100% correct, my trial and error of prior years of both losses and forgone profit of inaction gave me a different level of stress. The stress of NOT doing anything. I learned from earlier downturns that the pain of NOT taking that leap into investing lasts much longer than the pain of momentary losses on your investments.

I believe I just inadvertently fell into a metaphor on retirement. Perhaps the pain and loss of NOT retiring will be far greater than facing the unknown of actually doing it. When the kids eventually leave home, how comforting will it be to know that you maximized every teaching moment, shared in all the wins and losses, and was just there to talk.

I recently read an article on the difference between quantiy vs quality time with your kids. Exceprt and link below.

https://www.focusonthefamily.com/family-qa/quality-time-vs-quantity-time-in-parenting/

“It’s important to realize that it’s not always possible to plan meaningful interactions between parent and child. Such serendipitous moments can’t be cooked up and crammed into a few minutes of “quality time” every day. Many critical opportunities to teach or model moral values may catch you off-guard and will be gone in the blink of an eye. You can’t seize the moment if you’re not there to do the seizing.”

Similarly, I read an article not too long ago that stopped me in my tracks. While I don’t recall where I read it, there was a statistic that stated something to the effect of “By the time your children leave the home to pursue higher education, you will, on average, have spent 90% of the lifetime amount of interaction you will have with them”.

Just made me freeze on the spot.

You seem to be in a phenomenal head space, and KNOW that you can continue to build on your financial freedom even without an income from someone else. I hope knowing that helps you “do the seizing”.

My suggestion for a less stressful “career” with impact and purpose is to volunteer in a local school. Become a coach of the math, science, or future business leaders club. You can be there for your kids and still show them hard work and dedication. I’m four years into retirement, volunteer 10-20 hours a week, and fully done with my career. No regrets.

Hi Steve, Thank you for suggestion. This has been one of my options that I am considering. Reassuring to know that you successfully put it into action. I thought I can start at the high school level and dabble with an adjunct professor role. Perhaps even go to school for my post grad degree and become a professor full time.

MI-365

Phenomenal job— congrats! Thanks for providing a comprehensive lens about your financial journey.

You mentioned VTI —but due to expense ratio why would you not buy the Admiral version?

Proud of your pursuit of life balance!

May blessings continue—

VTI has an expense ration of 3bps (0.03%) vs admiral share VTSAX is 4bps (0.04%). What am I missing? Also, VTI which is an ETF is more tax efficient than the mutual fund version VTSAX.

Thank you for the well wishes!

Hello again, apologies if my previous reply was short. I was rushed for time. To further clarify, I believe admiral shares only apply to mutual funds, not ETFs. Mutual funds have the benefit of setting up automatic buys and sales, which is great for dollar cost average or automatic withdrawals once you start drawing down on your savings. The negative to the convenience is a slightly higher expense ratio and also slightly less tax efficient, when compared to ETFs. Either VTSAX of VTI or excellent choices, it’s a matter of are you dollar cost averaging (buying on a monthly basis) or investing a lump sum. I own both in my portfolio. If you have further questions I encourage you to call Vanguard as they have excellent customer service. Also, Fidelity has some 0 cost index funds that are good choices. But the debate between Fidelity and Vanguard can be a whole blog post on its own. I hope this helps.

You are still young, have a prestigious title in an industry you love, earning a phenomenal salary and are financially independent. First of all, a giant congratulations! Walking away from such a position will be very difficult, not just because of the money, but also the satisfaction of achievement.

If I was in your shoes, I would learn to control the stress of your job better and ride that train as long as I could. Just knowing that you can walk away at a moment’s notice without hurting your family financially should be a good stress reducer, it was for me. Maybe you can redefine your job some to spend more effort mentoring and helping your employees, that should somewhat scratch your itch to teach. You obviously have a talent for investing, otherwise you wouldn’t be paid as highly, I would hate to see that wasted on woodwork 🙂

I fully understand your desire to spend more time with your children, I just hope that if you do quit but resent it later, that it wouldn’t sour your relationship with them. All the best for you and your family, well done MI-365!

Thank you for the thoughtful reply. I have been given similar advice from a former boss and that is what I am currently doing. I am taking on less responsibility at work and have dramatically reduced my stress. Thus, I have worked two years past my self-declared FI date. I will likely continue to do so, just knowing myself, until I am confident on what I am running to. Making my salary and enjoying most nights and full weekends with my children is something I would have been envious of when I was younger. I don’t want to be shortsighted of how good I have it. But education and exploring my options is always a healthy exercise.

I enjoyed your woodwork comment, but a perfectly mitered joint with a natural varnish finish is sure satisfying! 🙂

Congratulations on your investment success! Are there particular ETF/Index funds that you would recommend for us to research further? Are you investing in AI companies or funds? I appreciate the book recommendations and will check out A Random Walk Down Wall Street.

Thank you SMB116. I have not invested in AI companies. All of my investments, absent 2 or 3 very small positions, are broad based index funds. There will always be a hot sector or hot stock that will make people bucket loads of money, but I decided years ago to stick with broad based funds. They let me sleep better at night and likely give me better returns.

A Random Walk Down Wall Street gives great suggestions for index funds and asset allocation. The book was recently revised for its 50th anniversary. I suggest taking it out at the library (save a few bucks) and at the very least reviewing the funds and allocation charts towards the end.

Here are some funds I suggest, but they are all broad based. I’m not giving up any secrets with these funds, just reducing your fees.

Fidelity: (0 cost funds)

FNILX – US Large Cap

FZIPX – US Mid/Small Cap

FZROX – US – All Stocks

FZILX – International Stock

Vanguard (the below are also available as ETFs)

VFIAX – US Large Cap

VEXAX – US Mid/Small Cap

VTSAX – US – All Stocks

VTIAX – International Stock

Ishare ETFs:

IVV – US Large Cap

ITOT – US – All Stocks

IXUS – International Stock

Thank you so much! I will definitely check it out of the library. Also, I very much appreciate your recommendations on the above broad based funds. I definitely have my research cut out for me. I really enjoyed reading your interview and wish you all the best!

I always wondered how a professional investor invests their own money. It seems you have been true to the traditional recommendations of broad-based indexing with attention to fund fees.

I was in your same boat. However, once our net worth hit 8 figures (roughly 2014), I wanted atypical results (enhanced compounding). I allocated a portion of my assets to double and later triple leveraged broad based mutual funds/ETF’s, having seen 12-month periods of 50-100% returns, which more than make up for the fees.

I am 8 years your senior, if my returns continue as the past 9 years have, i should hit 8 figures in our retirement accounts alone within the next 4-years. I risk no more than 25% of my total net worth at any time to this, and am ready to sell on a dime if I feel we are no longer in secular bull market – current date suggests to me that won’t be for a while, but circumstances can change quickly.

This is for someone who has a big cushion, likes fundamental and technical analysis, and has devoted time (in my case almost 2 decades) to learning and standard investing experience before engaging these investment vehicles. The reward is very good when done right given the magic of compounding but can be very difficult when done incorrectly. I am also heavily diversified outside of the markets to include my business, commercial real estate and a 20% NW position in CD’s/savings accounts at roughly 5% returns currently (this serves as an insurance policy for my cash flow dependent business and real estate).

Wish you continued success. Spend time with the family and travel. I have had the same challenges with time and have made and continued to make significant changes to focus time and energy on the family. Hence an increasing focus on our passive income.

Hi MI-119, thank you for the kind words and congrats on your success. The one item I have on your “how a professional investor invests their own money” comment is that I am a professional in my niche area of the market. Most professional investors invest on behalf of large institutional clients in a specific strategy, which is very different for the average person. The average person can do better than the “professional” investor without much effort and a bit of education. It’s a shame that the simple concepts discussed here are not more broadly taught in school.

Could you provide an assessment of the CAPE Schiller Ratio? I.e it is around 30 right now but what does that mean to me? It seems high historically but are there other factors that need to be considered against historical baselines. TIA.

From someone not close to FI/FIRE or retirement, this was an encouraging read as a “boring investor” myself. Congratulations!

Hello RSPatts, sorry for the late reply. The CAPE Schiller Ratio is around 31 right now which indicates that you can expect to earn 3.5 to 4.5% return over a 10 year period, based on historical observations.

You are correct that there are many other factors at play, such as interest rates, ones view on EPS growth, P/E multiples, and other macro views. I like to keep things simple and compare risk free returns on treasuries in the 4.25% to 5.25% range (depending on 1yr or 10yr maturity) vs equity returns. In my opinion, you are not getting paid enough on equities at the moment. I hope this helps.

Great interview! Many similarities to out path…just plan and simple stick to the index funds and never sell. Now i am jumping back to MMM to comment on your “20 Year Career At a Crossroads” post. https://forums.millionairemoneymentors.com/t/20-year-career-coming-to-a-crossroads/9912