Here’s our latest interview with a retiree as we seek to learn from those who have actually taken the retirement plunge.

Here’s our latest interview with a retiree as we seek to learn from those who have actually taken the retirement plunge.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

There was no way to include every possible question in an interview like this, so if you’re wondering about something that’s not addressed, please leave your question in the comments below so the interviewee can address it.

My questions are in bold italics and his responses follow in black.

Let’s get started…

GENERAL OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

Me: 57

Wife: 61

Blissfully happily married 30 years.

Do you have kids/family (if so, how old are they)?

No children.

What area of the country do you live in (and urban or rural)?

We live in a suburb of a major Midwest city.

We also have a second home, just built, outside a coastal city in the Southwest (more on that later).

Is there anything else we should know about you?

As my story unfolds, you’ll see that I’ve done several things that ‘go against the grain’ or defy conventional wisdom.

That said, we’re both comfortable (or lucky) that these decisions have been positive and we feel good about our situation and the route we’ve taken. I’ll flag these items.

From reading just about every Millionaire Interview, we’re definitely not doing what many have done but we’re in a good place.

RETIREMENT OVERVIEW

How do you define retirement?

I know retirement is a bit like a Rorschach:

- No longer ‘corporate’ and working part-time, either at a passion or a side gig?

- Going from full-time to consulting?

- Doing a complete career change after corporate life?

- Not working entirely?

For me, I think it’s a somewhat ‘fluid’ definition.

Currently, I don’t work at all so I consider myself retired. That said, if I discovered a ‘passion’ (for example, working with food, writing etc…), I think I’d still consider myself retired. I’d no longer be working in the profession where I’d spent my entire full-time working life.

How long have you been retired?

I’ve not been working since early 2015.

I dabbled briefly with some consulting in the few months following my exit but I abandoned that pursuit and have not been working since.

Is your spouse also retired?

My wife retired about 1 year earlier than me, and her circumstances for her exit were similar to mine.

What was your career and income before retirement?

I spent most of my career in Market Research, first at a large Consumer Products Company, then several large Pharmaceutical companies. I ended my career as a department Director.

Over the last 15 years of my career my total compensation rose steadily from $110k/year to approx. $240k/year, including stock options and stock grants.

My wife spent most of her career in Information Technology for Financial Services companies.

Her salary trajectory, though more bonus-driven was similar — some years she would make close to $300k, other years a bit less.

Having changed positions and companies several times her compensation varied but on average, she brought home ~$175k/year during her last 10 working years, averaging the good and bad years.

Why did you retire?

I was fired, essentially.

I could toss it up to politics, career mis-steps towards the end (a high-visibility project that didn’t go well), ageism and a company changing priorities. I will say I was somewhat surprised as I had always been an out-performer but I did not see this coming.

Though things were not going well and I could sense it, firing was the last thing I expected — I know if one of my employees were in trouble I would’ve worked with them to improve or at the very least given them the heads-up.

In the end though, it was a blessing. The commute was terrible (my company relocated to the suburbs and I went from an easy commute by bus to a 60 mile drive on some of the busiest highways in the Midwest) and the company’s culture and expectations changed.

Upon reflection, I don’t think my skills were current for today’s world, which changes at lightning speed though not to say I couldn’t have learned — and after 15 years, from their perspective they likely needed fresh blood.

There was a bit of a purge, from what I understand and there are many new faces with fresh ideas. I can’t say I blame them.

My wife left her role under similar circumstances. Her last company was a bit chaotic, bosses changed, politics and evolving priorities all contributed.

For both of us though, we left with fair severance packages and we received our bonuses so we did not walk out empty-handed. And we were well-compensated throughout most of our career so for that, we’re grateful.

PREPARATION FOR RETIREMENT

When did you first start thinking seriously about retirement and when did that turn into a decision to do it?

Retirement came to us, not us to it!

But I had a net worth dollar target in mind and I started to target age 55 as an out-date.

From a benefits standpoint, 55 was/is a magic number as I would qualify for subsidized retirement medical benefits etc…and also, psychologically its a milestone that I would have liked to have achieved. I was 53ish but if I throw in severance and bonus that probably added another year in compensation so I fell about 1 year short.

In today’s world, that’s not bad and I consider myself very fortunate. Many folks my are escorted out earlier and/or in much more dire financial straits.

My wife was just ready. She wasn’t happy in her job and she lost the desire to find something else.

That said, when she left her company she did some consulting for 6 months or so for her former boss so that kept her busy but she really had no interest in working full time. She was done, and she just didn’t want to work any more.

What were the major steps you took from deciding to retire to developing a plan to do so?

Several key steps helped me develop a retirement plan, which evolved from my financial plan:

1) Got an Investment Advisor/Financial Planner. More specifically, we got the right advisor that understands our goals:

When I joined my last company, even at age 38 I had one eye towards 55.

One benefit from my wife’s company at the time was free access to a financial adviser. We came to the realization that we needed someone to help us develop a rigorous plan.

We had been somewhat haphazard (I had always been a saver) but it was the equivalent of a ‘messy desk’. We had plenty of ‘stuff’ (401k, some individual stocks that seemed interesting, mutual funds) but not organized and not goal-focused.

He helped us tremendously and we still use him today after almost 20 years. I like him because he ‘gets’ us. We’re conservative investors and somewhat risk-averse. He knows where we want to be and he doesn’t push us into things we don’t want.

2) Took full advantage of company benefits – 401(k), Savings/Investment plans and other benefits.

Further, my company had terrific retirement benefits and while I had done so in my previous companies I had not put much thought into it.

As early as I could, I contributed the maximum allowed, both before and after-tax into my 401(k).

I also had a good portion of my paycheck diverted to my financial adviser to invest and I also invested money each paycheck into mutual funds that I like.

I would estimate that >40% of my salary was invested in either my 401(k) and outside investments and that was something I maintained for at least 15 years.

3) Treated ’Savings’ like an ‘Expense’.

For us, monies directed through payroll deduction, automatic investing etc…were considered a bill, something we were obligated to do. The way we pay our utilities etc…we ‘pay’ our Financial Advisor, our mutual funds, our company savings plan.

I like to steadily invest — call it dollar-cost averaging, but I like the discipline of consistent investing on a schedule.

My wife has a different savings style. Where I like to steadily invest throughout the year (payroll deductions, automatic withdrawals each month etc…) she likes to invest in chunks.

Her bonus and excess cash buildup would be invested in addition to 401(k) contributions.

Slightly different means, but we end up in the same place and the good thing is, we both have the savings mindset.

4) Became educated on the finer points of personal finance.

I became a voracious consumer of financial information, through blogs, publications i.e. Money Magazine, Morningstar, Kiplinger, Ric Edelman and retirement-focused newsletters, including ESI!

This helped me to ask much more informed questions, learn from others, shape my savings and investment strategy and to focus on 4 things: cost, return, income and tax implications. Before I invest in anything, these are the questions I ask.

5) Became highly disciplined re spending, budgeting, planning and investment performance and acquired to tools to rigorously monitor.

To that, I rely heavily on Mint to monitor spending, Personal Capital to monitor performance and various of planning tools i.e. TRowe Price FuturePath tool, Fidelity Retirement Planning and NewRetirement.

to monitor performance and various of planning tools i.e. TRowe Price FuturePath tool, Fidelity Retirement Planning and NewRetirement.

Though it’s cumbersome since it’s manual, I use Morningstar for research, and Morningstar’s Portfolio Tracker. I find this tool particularly helpful to understand my portfolio’s performance, composition, mix and fund expenses, and to benchmark my performance against broader market indices.

For us, I developed a comprehensive spreadsheet/workbook in Excel where expenses are monitored, a line-item budget is set, with lots of fancy-shmancy graphs and pivot tables so I know exactly where we are and how we’re doing. Finally, once every 2 years I have my Financial advisor do a comprehensive plan for us.

It’s probably a bit OCD but I like to sanity-check against the various tools. There’s so much at stake and the tools all have features that let me model, run what-if’s etc…and that just gives me a measure of confidence that for the most part, the tools all tell me I’m on track, in addition to the modeling my financial advisor does for me.

Regardless, I learn something from each of these tools — what to consider such as impact of market changes or social security claiming strategies or heaven forbid, impact of a catastrophic event.

Overall, the biggest change for us was mindset.

Retirement wasn’t an abstract, far-off concept. It was imminent and the odds are it would happen sooner than we plan so we better be prepared.

It wasn’t an ‘if’ but ‘when’, and we focused our thinking and our investment strategy on the long term through income-generating investments, safety, asset mix so we could benefit from strong, and ride out weak markets.

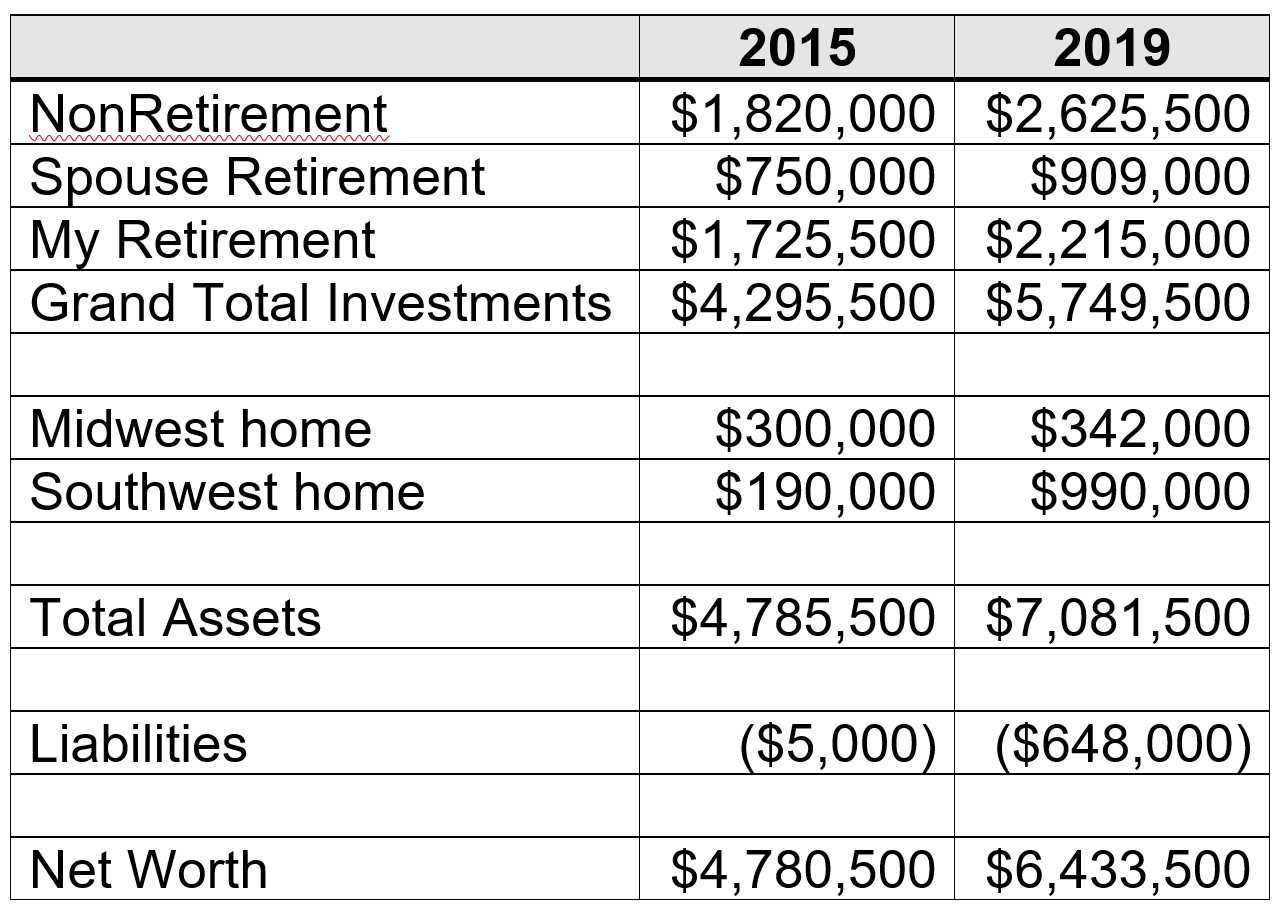

What did your pre-retirement financials look like?

Here are our financials in 2015 (retirement year) compared to what they are now:

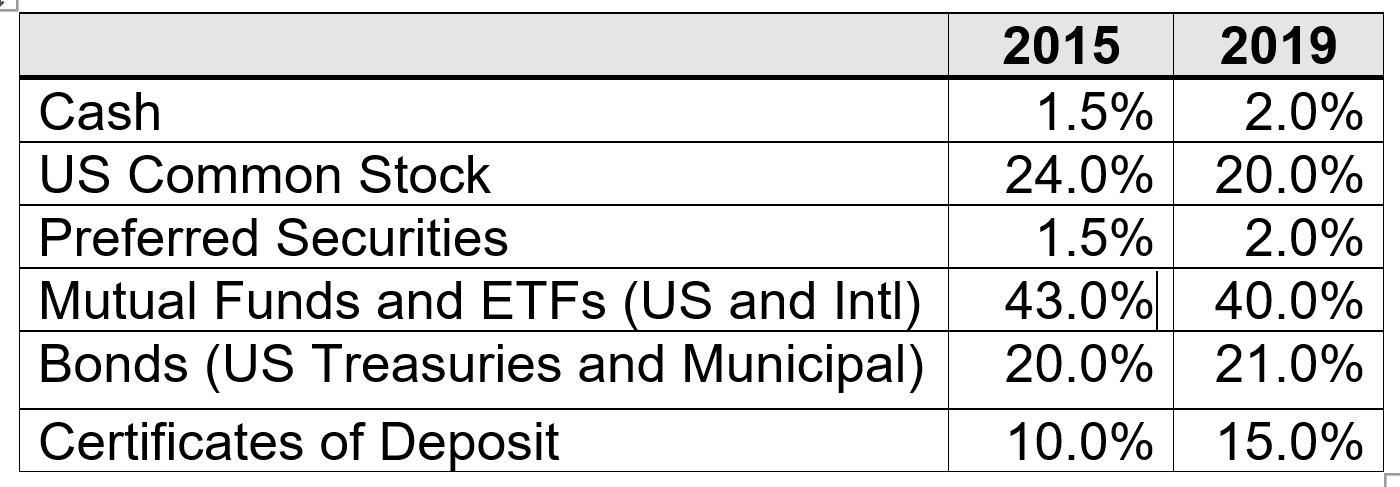

And here’s our asset allocation:

A couple of points regarding above:

1) I took a lump-sum option on one of my pensions. I wanted to have the asset in-hand, and I had done projections from when I took the lump-sum at age 54, and what the lump sum would be at age 65 and I believe I could have done better.

2) I’ve been steadily, but slowly moving to more fixed income (i.e. CDs) now that rates are ~3%. I expect some market volatility and I would like safety, particularly in the retirement accounts.

3) I was fortunate to have benefited from a tax law change in 2014 that allows for after-tax 401(k) contributions to be rolled to a Roth IRA. I had contributed to not only to the pre-tax limit, but after-tax limit in my 401(k). This was convenient forced savings for me and I was happy with the investment choices across a variety of fund types and at low cost. [Note: Roth was $325k of retirement funds in 2015 and is now worth $424k.]

What was your overall financial plan for retirement?

I’ve been obsessively, and in excruciating detail, tracking my expenses over the past 5 years so I’ve been able to establish a baseline — that is, average expenses across the major categories, allowing for the unexpected and fun i.e. travel, dining out etc…

For the past few years our spending has been consistent so I’ve been able to plan and budget accordingly.

Since 2018 was the year we built our house, one-time expenses were significant but I’ve been able to establish a baseline for average expenses — utilities, etc…on a second home.

We know what our mortgage payments (plus escrow for taxes and insurance) will be for the next 10 years and our plan is, within the next 5 years to sell our Midwest home and with the proceeds recast our mortgage so the payments will be much lower.

Our overall yield (dividends, interest etc…) is ~2.5% and our portfolio has grown approx. 7.5%/year since retirement.

We do not expect that growth rate to hold in the future, especially as we move to safer investments but we are confident that the interest and dividends will be consistent given the composition of our portfolio.

Currently, the non-retirement and my wife’s retirement portfolio throws off approx. 60% of our expense requirements:

- When I turn 59 1/2 in 2021 the combined income generated by these accounts will represent approx. 80% of our requirements.

- When bonds, preferred issues and some structured products come due throughout the year we are able to utilize these proceeds as needed to pay expenses etc…Our CDs are ‘laddered’ – that is, with maturity dates from 1 year to 3 years that we’ll continue to roll over

- My wife and I have 2 small pensions that we will take when we’re 65. My pension will be 100% joint/survivor so if I pre-decease my wife she’ll still receive income.

- We have an annuity, ~$500,000. We like the idea of a consistent income – we’ve given ourselves a paycheck every month since retirement – and this particular annuity was attractive in that it provides 6%/year. We will likely turn this on within 4 years.

we’ve modeled every combination of Social Security – both at full retirement, both early, one early and one at full retirement etc…and we’ve settled on me claiming at 62 and my wife at 66 though this may change. While many recommendations are to wait as long as possible to maximize the monthly payments - We’ve identified these claiming ages as a ’sweet spot’ – that is, our assets would not be markedly different at milestone ages – 70, 75, 80 and in some cases lower had we chosen different timing. We’re able to take the proceeds and use or invest depending on need. Waiting longer may mean a higher payout but fewer years to enjoy it.

Did you make any specific moves to prepare your finances for retirement?

Against the grain #1: We UPSIZED our home(!)

- We’ve lived in the same townhouse we bought, which we’ve owned free/clear since 2003, having paid off our 30 year mortgage in 15 years.

- We fell in love with the area of the Southwest and purchased property in 2004 with the plan to eventually build a house where we can entertain, have visitors etc…We’ve never owned a stand-alone home and we did not want to move to another townhouse or a condo. We wanted a house to call our own, built the way we like it with the features that we don’t have in our townhouse.

- For now we’re keeping both locations, maintaining ‘dual citizenship’. We have the financial means, maintaining our home and lifestyle in the Midwest is in the plan and honestly, we’re just not ready to move – we have our friends, our routine and we enjoy many of the things the Midwest has to offer. So, for the time being we have the best of both worlds but I’ve planned for us to sell our Midwest home and live full-time in the Southwest within 5 years.

Against the grain #1a: We took a mortgage(!)

I know that many retiree’s goals is to be debt free and there’s plenty written, blogged about etc…about the perils of having debt in retirement but we felt this was the right move.

We certainly could have paid cash but we’d rather have our money working for us in the market, especially since the mortgage interest rate is low — 3.75% and the interest is tax-deductible.

Against the grain #2: A portion of our equity portfolio is in individual stocks.

- I’ll give more of a breakdown of our assets later but in short, I like having these stocks and I chose those that are rock-steady and consistently pay dividends. While these holdings don’t represent the most significant portion of our portfolio, they’ve provide a steady source of income each month. And, by and large these holdings tend to generate dividends in good times and bad and for us it’s about income as much as it is about assets.

- I know that everyone – from Bogle to the ESI millionaires say to hold a few ETFs, broad-market low-cost index funds and to stay away from individual stocks, and for the most part I agree. I would tell people, “do as I say, not as I do”. But I bought many of these stocks – just about all are blue-chip, known names across sectors that pay dividends consistently and at a good yield. Many I bought low, bought more when the market dipped and they’ve appreciated significantly, which is a blessing and a curse since selling means generating a taxable event. For now, I’m happy with the income. And, I’ve got a balanced portfolio with a good mix across the major categories: Individual stocks, ETFs, broad-market and some specialty mutual funds, Munis, Bonds and cash.

Who helped you develop this plan?

My financial planner played a significant role, but by educating myself through magazines, newsletters etc…: Kiplinger’s, Money, Morningstar, Consumer Reports Retirement newsletter (now defunct), NY Times, NewRetirement, Ric Edelman. They all had things to say and while their advice wasn’t always for me, I’m able to ask informed questions of him.

Some things our planner helped with:

1) He recommended taking a Line of Credit against our assets to build the house. The interest rate was low and deductible against investment earnings/interest. Next he recommended we convert to a mortgage vs. paying off. Our money is working, the mortgage interest is deductible and we got a great interest rate.

2) About 10 years ago I started to ‘hammer’ him on fund expenses (much to his chagrin) but given how much we have with him, we’ve brought this down significantly. Way back when, I didn’t know expenses were a ’thing’ since these tended to be buried in the prospectus but now it’s a decision-point for me when it comes to investing. When I have excess cash that I’d like to invest I as often bring ideas to him as he does to me.

What plans did you make in advance to leave your job?

Well, since the decision to leave wasn’t ours, we didn’t do any specific planning.

That said, even had I had more time I was/am comfortable with our plan.

The expense projections are realistic with enough of a cushion, we have some assets that are liquid (i.e. cash) that we can access if needed and, most importantly our investments provide enough of an income stream and when we start tapping our Social Security and Pensions we can think about reinvesting.

What were your pre-retirement concerns (financial or non-financial)?

After all I had read about the newly retired needing a purpose, having their identities so tied to their jobs and feeling lost or bored, I was very concerned that I would experience these same feelings and would start to ‘climb the walls’ after a month or so.

I also anticipated trying to find a new job and experience one disappointment after another: the unspoken age discrimination, not having the skills companies are looking for, a rigorous interview process or having my resume fall into a black hole.

Financially, though my models tell me otherwise, I was, of course worried about running out of money, an unexpected major expense that would significantly deplete my savings or expenses much higher that planned.

How did you handle deciding on and paying for healthcare?

Fortunately, I qualified for retiree healthcare benefits for my wife and I, and I made it just ‘under the wire’.

While not subsidized, which I would have qualified for had I been there until age 55, I had enough years with the company that entitled me to pay the group rate with the same coverage that I had as an employee, which includes dental and vision.

The health coverage, fortunately is terrific including free prescription coverage.

When I or my wife turn 65 we enroll in the company-sponsored Medicare Advantage plan.

We consider ourselves blessed that we’re in this plan as this gives us tremendous peace of mind. While the coverage is not inexpensive, I know on the open market we’d likely be paying more for less.

How did you tell your family and friends of your plans?

I told everyone I retired.

I’ve never been ‘let go’ and while many go through it in their careers, it was tremendously embarrassing and humiliating.

I feel as though my career has ended in failure and that is something that I just would prefer to keep to myself — except my wife, of course!

It’s great, in a weird way that I have someone that also went through this.

My boss, by and large was supportive and understanding, and he and I crafted the ‘retirement’ story and that was how it was announced internally.

I told my team as well though, in all honesty they likely know the truth. Of course, after I left, the truth came out. Unfortunate but understandable. People just talk.

THE ACT OF RETIRING

How did you ultimately retire?

For me, I was given a choice: leave that day, leave end of year, leave end of February.

I chose end of February as I would accumulate time with the company, earn, still invest in my 401(k) and qualify for my bonus.

Since it was positioned as ‘Retirement’ it was a long goodbye, getting work things in order for my successor, managing my team and projects etc… So, business as usual up until the end.

I didn’t want a lunch or a party as these tend to be uncomfortable so my departure was quiet.

My wife and I went out to a nice dinner that evening.

But, I am above all a professional and I took a lot of pride in what I built there and wanted to leave with my head held high.

My wife’s ‘retirement’ was a bit more sudden, along the lines of a classic firing: mystery meeting set up, HR and her boss in a meeting room, her boss read a script, she was handed a packet and was escorted out after collecting her things. It was an unceremonious, humiliating end to a long and successful career.

What went well?

Once we decided that working full-time was no longer in the cards, settling into the retirement mindset was easier than I thought and the boredom etc…that I expected to experience didn’t really happen.

Our finances and our plan (knock wood!) has held up so we’ve not had to struggle nor significantly curtailed our lifestyle.

We were never extravagant spenders anyway so there really was no change.

What didn’t go so well?

For me, since leaving my company was unplanned my first thought was to find another job so I started the process of job-hunting:

- I updated my resume, and I took advantage of the outplacement services offered to me as part of my separation. I found this to be particularly disappointing but I accept responsibility for that as well since I had higher expectations. I found this to be very formulaic i.e. “today we’re going to work on your elevator pitch” or the best way to answer why I left my last job. That said, these are critical skills for job-hunters and for most these exercises are invaluable but for me, my heart wasn’t in in it.

- I networked, reached out to former colleagues etc…and got some bites but many roles like the one I left were either highly technical — if I were recruiting for my job I’d want more technical too — or just not for me.

- I thought about doing something completely different and there were some positive aspects to this but we were in the midst of building our house so we’d be away for several weeks at a time.

I look back on my career and have my share of regrets: I should’ve done this, I shouldn’t have said that, I should’ve taken on this job or project etc…

I don’t think there is a person who ever worked that didn’t share these regrets with varying degrees.

While I don’t necessarily block these out, over time I put these in perspective.

But, I still see, out of the corner of my eye colleagues that have done well, landed a great job or got a great promotion and wondered if that could’ve been me if only…I know these thoughts will diminish over time but I imagine the newly retired go through this process.

How did you ultimately find the courage to do it?

I guess this question could be re-worded as, “how did you decide to retire vs. finding another job”?

For me, this was a rude awakening. That is, to find a comparable job in the same or similar industry would have been very difficult.

Companies want younger and more technical: while I would consider myself tech-savvy, many companies want player-coaches. Sure, soft-skills are great but getting through the first hurdle — demonstrating the hard skills — is very difficult.

I tested the waters early but realized that I would have had to invest considerable time upgrading my skills in order to more effectively compete. Interviewing is now a different ball game now — by video vs. in-person which I found to be somewhat jarring.

I know that it’s something that with practice one becomes more comfortable with but for me I found it to be frustrating to talk into a monitor vs. interacting live.

I did a lot of soul-searching about what I wanted my next job to be:

- Another large company? Sure, but I know what that brings. While compensation and benefits, and the trappings that may come with the job may be attractive, I also know that there is a drudgery aspect — meetings, politics, good co-workers and bad, competitiveness and honestly, the work itself.

- A smaller company or startup? Maybe, but those are harder to find, and they tend to be frenetic, chaotic work environments. Challenging and exhilarating too, but for me a younger person’s game.

- Consulting? I did a bit of that for a consulting firm after I left my job and while the engagement was unsuccessful (client mismanagement), it wasn’t for me. I realized that if I were to go it alone I would need to completely immerse and re-educate myself in this fast-changing world so my technical skills are top-notch and more importantly, have a great network of folks that would want to hire you!

- Changing industries or doing something I enjoy: I’m still contemplating that and keep one eye open.

I don’t need to tell you that job-hunting is difficult! Networking, developing a ‘pitch’, a tight resume, sending out countless letters, applying on-line, dealing with recruiters is exhausting and frustrating.

For me, I kept asking myself: do I really want to go through all this, for maybe another couple of years? I know many colleagues are fortunate, and smart enough to have a broad network where they walk out one door, and through another in a matter of days into a job that is as good or better as the one I left. I realized I should have worked much harder at building a strong network.

I got to the point where I weighed the ’three F’s – Freedom, Flexibility and Fun’ with work. I enjoyed the Freedom of not having to answer to anyone, the Flexibility to go where I want and when, and the Fun of being able to go to the beach in the middle of the day, take a trip or go to a museum.

I also think that in the end, I just gave up trying to find a full-time job. I didn’t have the fortitude to go through the process.

I know I am fortunate and for many folks who lose their jobs, there is a much more positive spin on above, especially in a profession that one truly loves. I understand and appreciate that many folks find better jobs, whether through good fortune and a good network or a lot of hard work.

In some ways I envy these folks — to have a passion for what they do, to have done all the right things re building and maintaining relationships, being active and pro-active in being visible in their profession and being able to seamless move from one role to another.

I also understand that many folks need to keep working — financial obligations or because they enjoy what they do. For me, I count my blessings that I planned and saved enough that I don’t need to go back to work. That said, if I had, or found that passion it wouldn’t be work, right?

RETIREMENT LIFE

How was the adjustment, especially the first few months after retirement?

The adjustment was surprisingly easy.

My fears of boredom, inadequacy, the need to go back to work etc…never really kicked in.

At first, I admit it was a bit strange doing things during the day that I would normally save for the weekend or on a day off but that quickly wore off.

How is retirement life now? What do you like about it and what do you dislike?

Retirement life is good!

We enjoy spending time together, and while I wouldn’t call our days busy, they fly by.

What I don’t like is the nagging feeling that I should be working and in all honesty there are days I’m just bored.

My wife is the opposite — she loves not working and has no interest in going back.

What do you do with your time? What does an average day look like?

I think to the outsider, our typical day may seem boring, and they would say “you need to find something meaningful to do with your time!”.

Most days are a combination of going to the gym, running errands etc…

Once or twice a week we plan something: go to the movies, go to a museum or shopping, and go to a restaurant we like or want to try.

In nicer weather we may go for a walk on the beach or do some other outdoor activity i.e. play golf.

We’ll get together with friends for dinner or drinks once or twice a week and on weekends we’ll do activities as a group.

Every 4-6 weeks we’ll visit our Southwest home. We’ll shop for the house, explore the area, and get together with our Southwest friends.

Looking back, what would you have done differently?

I would have stayed ahead of the curve with my technical skills and made myself more of a thought leader in my industry.

I would have developed and maintained a much, much stronger network so I had options, whether moving to a similar role or a comparable one in a different industry.

I think if I had these options, It would have been easier to find my next endeavor.

I also would’ve cultivated a passion and developed a way to build upon that so I would’ve had the option to move in that direction.

I know there’s time for that and it is something I may still do.

Was there any emotional impact from leaving the workforce?

Yes. For me, I had never been fired so it was humiliating. I was ashamed, and I thought I need another job to demonstrate to myself that I still had ‘game’ and could find a job as good as, or better than the one I left.

I wasn’t afraid of the financial impact but more the emotional one: sadness, missing the social aspects and honestly some of the fun, boredom etc…and the inevitable frustration that job-hunting brings.

For my wife, she reveled. She couldn’t wait to retire and though she did some consulting for about 8 months or so, she didn’t truly enjoy it and was happy when the engagement ended.

What surprises (financial or non-financial, good or bad) have you had since retiring and how have you handled them?

I’m surprised at how easily we both were able to ‘let go’ and enjoy the freedom. There aren’t many days where I say to myself “I wish I were working”.

I know my wife never says this!

Fortunately, we’ve not had any financial surprises that we’ve not been able to handle. Thank goodness I planned for the unexpected.

What are your future plans?

We will eventually move to our Southwest home, though the timing is TBD. My plan has 5 years but that may change.

I’m keeping one eye open for a passion pursuit — it may be food-related (I have a culinary degree), or involve writing.

My wife loves retirement so as long as we’re healthy (we are!), we’ll continue to enjoy the Three F’s — Freedom, Flexibility and Fun.

RETIREMENT FINANCES

How has your financial plan performed compared to what you had estimated before retirement?

Our plan has held up well. The income our portfolio produces, coupled with the cash reserves and other portfolio moves have enabled us to both cover expenses without having to curtail our lifestyle.

I set a line-item budget at the beginning of each year and for the most part we’ve stayed on track. While I admit that I had no idea how much it would cost to maintain the Southwest home before it was built, we’ve been able to establish enough of a baseline so we can better plan.

When we were working we didn’t pay much attention to how much income our portfolio generated — dividends were reinvested, any cash buildups were also invested. Now, it is our primary source of income so naturally we monitor obsessively and I can better plan our cash flow. We’ve also done some other things to make the most of this:

Since my wife is 61, we’ve directed any dividends/cap gains etc… generated in her IRA to our checking accounts. Prior to 59 1/2 these were reinvested. Fortunately we’ve not had to sell any of these assets (yet) though we might start to draw down at some point, since RMDs will be an issue in 9 years.

In our taxable accounts, we’ve also taken the dividends/cap gains and interest, vs. reinvesting.

How are you handling Social Security, required minimum distributions, tax issues and the like?

Since we’re both a couple of years away from claiming Social Security, we’re still formulating a strategy.

I’ve run every combination (one or both claiming at 62, full retirement age etc…) and determined what my portfolio and cash flow would be at various future ages i.e. age 70, 75, 80 and beyond.

Personal Capital’s Retirement Planner is a great tool for this exercise once you determine your individual Social Security payments from their site as it enables one to create multiple plans based on different claiming ages or other events.

For us, we’re not concerned about how much we’ll have at age 90; age 70 we’re relatively young, hopefully healthy and can fully enjoy things.

My advice — it’s not about how much you’ll have at the end — you probably won’t be able to enjoy it. With Social Security, ‘you can’t take it with you’.

As for RMDs, we’re a ways off from having to take these and I’m weighing the tax implications of converting some of our traditional and rollover IRAs to Roth.

While we each have a Roth, I’m mindful that someday there may be a change to the tax laws that lead to taxing these as well.

We’re already taking the income my wife’s IRA generates, and I will do the same when I turn 59 1/2.

Since our investments are our primary income source, our tax rate is fairly low, and that’s just how we like it!

Did you return to paid work? Why or why not?

After a brief consulting stint I did not return to paid work.

I started to enjoy the freedom, we were/are financially in a good place and the longer I wasn’t working, the harder it would have been to get back into the work mindset. And to even get to that point I would need to actually get a job!

That said, I still keep one eye open for something that may interest me outside of my profession and I may pursue one day but for now I’m not actively looking.

My wife is officially retired and she does not see herself going back. But like me, she keeps one eye open for something that she may find fulfilling i.e. volunteering.

Did you find it hard going from being a saver to a spender?

For us, this was not as difficult as I thought.

We’ve set up our portfolio in such a way that we’re able to pay ourselves each month without having to sell assets for living expenses.

We can anticipate dividend and interest from our investments so we know what our monthly ‘paycheck’ is.

This provides something akin to the predictability of ‘payday’ when we worked.

While I look at our portfolio daily, despite market variations, dividends and Interest, our primary sources of income are fairly stable.

Looking back, what do you wish you knew in advance?

Well, I most certainly would have liked to have known it was coming!

I would’ve liked to get another year in, and there are things I would’ve done differently at work in order to leave on my terms, not theirs.

I think my wife would say the same thing.

What advice do you have for those wanting to retire?

For those seriously considering retirement, keeping in mind everyone’s mindset is a bit different:

1) Educate yourself.

Read books, newsletters, magazines and blogs that are retirement-focused.

This helped me know what I didn’t know and learn from others like me or faced with similar challenges i.e. Social Security, pensions (monthly payout vs. lump-sum, for example), paying for healthcare, taxes.

Had I not become an educated financial consumer I’d have been caught flat-footed.

2) Assume retirement will come earlier than you think, and not necessarily in the way you envision especially if you’re 50+.

The days of the gold watch, nice send-off with balloons and a cake are long gone.

More than likely, your boss, who’s probably younger than you, with Human Resources will be the one to tell you and you may not see it coming.

Or worse, you’ll start to see the signs and it’ll be ‘death by a thousand cuts’. If you’re prepared for the worst you’ll be ahead of the game.

It’ll still be jarring but at least you’ll have some measure of comfort that you’re ok.

3) Know your financial situation.

In particular, spending and future income.

Assume you’ll spend more than you plan for and have a line-item in your plan for the unexpected.

Leverage the various online tools — use more than one. I find Mint and Personal Capital to be invaluable to help with planning.

4) It’s easy to romanticize your job and towards the end, or even when you walk out the door you think about the good times, and how the bad times weren’t so bad after all.

That’s natural, but over time you’ll put these things in perspective.

If the good times were truly good (and for all of you I hope they were), you’ll have fond memories to share and reflect upon.

It’s easy to focus just on the good times and if you have the luxury of staying ‘one more year’ (absent financial circumstances), to do so.

I know it’s a time-worn saying but no one ever said, on their deathbed “If only I had spent more time at the office”.

5) Once you’ve developed and are comfortable with your plan, try not to compare yourselves to others.

Many folks like yourself have more, have less or have a different mindset than you.

The ESI Millionaire interviews are insightful — use these to learn, not necessarily to see if you measure up (or down) to people that may, on the surface be like you.

When you’re comfortable, ask yourself whether having x more money would significantly change your situation.

For me, sure I’d love to have more money — who wouldn’t — but I’m not sure I would do anything different. I wouldn’t live in a different house, drive a nicer car nor buy more expensive jewelry.

Plan to have enough to live the life you want and have enough of a cushion to take you through the rough patches.

Thank you ——

So insightful, honest and real ——. It seems to me that you learned the most important life lesson and acquired the skills you needed the most ——- 1. How to take care of yourself and how to keep the focus on understanding personal finance —- 2. And , you learned how to share your thoughts and ideas with others —— maybe you should start a retirement blog ?!? ?

Good luck and I hope all continues to go well. About 20 more months for my wife and me plan to join you and all the other happy retirees —-can’t wait.

Thank you so much for the feedback.

As for the retirement blog, thank you for the compliment! Not sure my life lessons are unique – there are lots of folks out there with stories to tell – but if this can help one person then that’s a good thing.

Good luck to you and your wife. Retirement is another step in life’s journey.

After reading all of the comments about you and your story —— are you sure you don’t want to rethink the “retirement blog” idea ——— message me , if interested, and I’ll do it with you —— who knows, it could be fun and a way to continue helping all of the younger savers ——

You always have a forum here to write about retirement! 😉

I love this new series. Thanks for the in depth look into your story. Seems to me you should start thinking about taking some distributions now from the retirement accounts with RMD issues on the not to distant horizon with pension + SS coming into play with 3+ million between you

I have heard others say they feared Roth tax changes. The only scenario that makes sense to me is similar to adding back Tax Exempt Interest. I do see that as possible, but in your scenario I think I would start making sure you got to the top of whatever target tax bracket you are aiming for to do some conversions. You didn’t really mention your expenses too much so its tough to guess. Perhaps I dwell on taxes too much in my own planning, but curious to hear your plan since you were so forthcoming with your other details.

Enjoy sounds like a very well earned retirement to me

Hi, thanks so much for the feedback, it was fun to reflect and to share.

Regarding taxes, I’m mindful of the tax impact of RMDs so I plan to determine the max amount to convert with the minimal tax hit. I’ve got a few years and with the proposed changes, a couple of more years as the age will raise from 70 1/2 to 72.

I love this new series, too. I get something out of each retirement post. Thanks so much for sharing your story.

Thank you!

This series is a great addition to the site and a very nice transition point from the millionaire series.

I felt the honesty in this interview. An eye opener to what is really going on. I do not like to network either. (Even though I am an out-performer at my job. )

I have been overloading my cash position this year as I get closer to 50. I hate not having cash invested. But at the same time I feel I need to have a bigger cushion so I am not forced to sell stocks out of necessity.

Thank you again for being part of this series.

The one thing I wished you talked about is your expenses, living in the midwest, even with another house in the southwest. You talk about strategies for when to take Social Security, but why? You’ll never even need it. Same thing with the annuity. I’m curious as to why you thought you needed it. With a net worth of over $6M, you’ll never run out of money if you both live to 150!

With no children to live it to, you also didn’t mention legacy or charitable giving. You describe a very modest lifestyle (no trips around the world, etc).

It just seems to me that you’ve saved a lot more than you could ever spend in a lifetime.

I am also interested in R4’s expenses and spend-down plans. What are the expenses by category (even if it’s just ballpark) and how well does it balance out with asset allocation, growth and risk?

ESI,

Any chance we can get this as a standard question? Perhaps something like “What are your expenses and spending plan as you progress through your retirement years?” I’d suspect different folks will have different plans (e.g. travel, charity, legacy, passion projects, etc.). Would love to see how different folks enjoy the fruits of their labor and how they thought through their ability to support these expenses. This is one of my biggest interest areas in this retirement interview series.

I have added this as a question going forward, but already have 10 or so in the can without it, so you’ll have to be patient for now. 😉

Y’all have done great for yourselves. A $7M net worth and you don’t have a desk, a commute or a boss. Dude, you didn’t get fired. You won!!!!

Thank you! I consider myself blessed. It didn’t end the way I had it scripted but (knock-wood) it will work out.

M24. I love this comment.

Retirement 4- you seem like a really good person. I just wanted you to know that.

Thank you much, you are too kind! This comment made my day!

Razorback summed it up very nicely…. “So insightful, honest and real”.

I’ll be honest, I’m approaching your age and have MUCH anxiety about my future. I “feel” young in many ways.. but I realize that is not the case. I’m in professional sales so there is always the risk of unexpected “changes”. I really appreciate your candor and feelings associated with your surprise “exit” from the work force. The idea of networking more is something I will work harder at… just in case!

But I’m more anxious about what it will be like not having work everyday. There is only so much tennis, gym and entertaining I can do. I just feel the need to be productive in some way and without work I fear the lack of structure will hurt me. Good thing for you and your wife is you’re in a great financial position so you have plenty of options!

Great story and thanks for sharing.

Hi, thank you for the feedback.

I can understand your anxiety, I can recall being surrounded by folks that were younger, in higher leadership roles etc… and wondering where the time went. Being in Sales is, fortunately one of the more ageism-resistant fields. There’s always a need for folks with good relationship-building skills and this is something you should leverage to expand your network.

As for anxiety around not working there are lots of avenues to channel that energy and if you’re in a good place financially, you can relax and be choosy about your next endeavor.

Good luck!

RI-4, this was a great interview, largely because of your humility and honesty. Don’t beat yourself up to bad about how things ended in your career. You are part of a large club of people who have experienced exactly the same treatment, including yours truly. I was bounced out of the corporate world at 57, a little over 4 years ago. Fortunately, like you, we were financially independent at that point so the scars were more emotional than financial.

I helped found a startup with some former colleagues but I’m kind of phasing out of the day-to-day. It just doesn’t excite me like it used to. I’ve looked at a few opportunities recently but, like you, I’ve also experienced age discrimination and hate the whole interview process and fakeness that goes along with it. I’ve been a “runnerup” for two opportunities but neither went my way. I thought what I was after was more the challenge of another role, since we don’t really need the income, but I’m starting to just let go of that idea as well.

Fortunately, my wife has a VP level job that she really enjoys. Her salary and bonus + my pension cover our expenses and our benefits and she talks like she wants to work at least another 5 years so I’m fine with that as long as she is happy. It is a bit of a challenge when one spouse is effectively retired while the other is in full-blown career mode but I’m sure I can adjust accordingly. She is about 4 years younger than me, very fit and attractive, high energy, ridiculous work ethic and the best at what she does so I think the odds of her getting moved out any time soon are pretty low.

One thing I have learned, which you also point out, is the importance of achieving FI at least by your 40s. Once you hit 50, all bets are off and it really is a crap shoot as to how much longer you have control of your own work destiny.

In summary, enjoy the fruits of your labor. You won! You achieved FI and now get to live life on your terms. Your former friends and colleagues should be so lucky!

Thank you for the thoughtful comments, greatly appreciated. I’m sorry to hear that your corporate career didn’t end the way you would have liked, but like me, it sounds like you’ve got a great partner, and she is blessed that she’s doing something that she loves and is well compensated for it with a few years to go. Unlike us, it sounds like she can leave them, not the other way around!

Ageism is tough and I hear ya re the interview process. It’s a slog, especially for us elder statesman that are competing against younger and faster.

You’re in a great place. Enjoy the ride!

THANK YOU for sharing your story.

I too, as a fiftysomething, LOVE this series, and am learning something from each retiree. From their perspective on being retired, as to how they came to be retired. Our HH income has never been as high some have shared; but we have done a good job overall saving, and have NO debt. Healthcare is our primary concern.

Healthcare seems to be the #1 issue, as I gleaned from all the retirement interviews and on other blogs. It’s understandable as these can be daunting. Having no debt, in your instance should no doubt soften the blow.

Good luck!

It’s certainly the #1 retirement concern from millionaires I interview!

Enjoyed your interview and will be rereading it for ideas. My spouse is a few years older than you, and your difficulties echoed things I’ve heard from him. But you and your wife have done a fantastic job of landing on your feet. Also, it’s great that you have a small pension and retiree medical benefits–my husband’s company doesn’t offer those. I wish you and your wife all the best. I think you have a lot to share with others in whatever capacity you choose–maybe as a teacher or a volunteer. Perhaps you could volunteer at a local non-profit to teach struggling families how to budget and save? Or volunteer in the schools teaching personal finance and investing?

Hi Sharon,

Thank you for the kind words. Yes, I think I still may have a ‘song to sing’ and perhaps teaching would be a good avenue. I enjoyed that aspect of my job so it may be something I’ll pursue.

Good luck!

This was a really honest interview and fun to read! I’d be shouting and screaming from the rooftops if I ever reach 7M net-worth but your humility is something to learn from. Difficult to why you consistently beat yourself over the firing, it’s an everyday occurrence in corporate America. As someone previously commented, You Won the Game! Time to start a new journey!

As someone in their early 30’s, I’d pay anything to sit with someone like you for a flat fee and take your advice on how to structure finances, financial goals, and advice on mutual funds and tax strategy. Traditional Financial advisors are out of favor among most of friends and colleagues.

Congratulations on your success!

Thank you Feisty FIRE!

I appreciate the kind words and I’m flattered that you’d think of me as someone to learn from! I think the best advice I can give you is to keep reading. It’s easy to name lots of books but I found the best way to learn was through publications like Morningstar, Money magazine and Kiplingers and of course, ESI Money! They are quick reads and have many great ideas for structuring a portfolio.

As mentioned, Mint and Personal Capital are two terrific tools for keeping you on track.

You have a ways to go, and the fact that you’re even reading Retirement stories speaks volumes – it’s great that you’re laying the groundwork now and that will serve you well as you approach retirement.

Best of luck to you,

Thank you for taking the considerable time to answer so honestly and openly – this makes the content so much more meaningful. I just came through the same thing you went through in 2015 – at the same age and with the same target retirement date – but I was able to find something within my current company just before my termination date. But it was not a “win” for me – I am still at the job though my heart is not in it, slogging through the days for the next 102 weeks until I hit 55 (it seems to go faster when you count down in weeks LOL). So don’t be too hard on yourself, I think you dodged a bullet 🙂

I have no doubt I will not have any problem transitioning to retirement (many hobbies, interests, and future goals), but I’m still anxious about the same issues as everyone else – will we have enough money to last our lifetimes, what will happen with healthcare, will our budget work according to plan, etc – so it give me hope to see another’s success. It’s great to see all your planning is paying off – revel in it!

And ESI – I LOVE this new series! I’m learning so much, and it’s reassuring to see how those with the same anxieties before retirement are doing so well, and are so happy in retirement!

Hi MI14:

Thank you for the feedback, greatly appreciated. The 102 weeks will go quickly, perhaps too quickly – summer, holidays, vacations whittle that number down and you’ll walk out with your head held high knowing you made it to the finish line.

Retirement, with proper planning can be fun and rewarding in its own way. The key is to not think of it as an afterthought but to plan, play what-if, imagine best and worst case to give yourself peace of mind. I think it was George Washington that said, “if I’m going to cut down a tree I’m going to spend hours sharpening the axe”. I’m sure I butchered the quote but hopefully you get my point!

Good luck!

I too really enjoy this new “Retirement” series. With respect to this interview you could have been writing my story (the exit, how I felt about my career ending the way that it did and how I felt about looking for a new job) …except that I was the breadwinner of the family and I had not done the pre-retirement financial planning that you did nor did I have any idea what our cost of living in retirement would be. Consequently I “retired” in late 2015 (at age 58) with a great deal of anxiety about our finances. While we had no debt, the last of our three children had graduated from university in 2015 (the year that I was laid off) and I had always saved, I had no idea whether I had saved enough. I had no idea what our annual retirement cost of living would be. I had no idea what our current annual expenses were. This was a period of my life that I would not like to relive. Once I gathered my wits about me…which took longer than I care to admit…I too started to voraciously read financial blogs as well as books on decumulation of assets. I have learned a lot and while I could/should have saved more I believe that we will be fine and I embrace the challenge of adjusting to the financial curveballs that may come our way. I also share what I have learned about retirement planning with my children…probably ad nauseum from their perspective. My hope is that I can teach them what I have learned about financing retirement so that they may be spared what I went through. Hope springs eternal:)

Pam

I’m glad that my story resonated with yours, I’m in very good company.

It’s good that you’re giving more thought to the future and are educating yourself on what will be most critical to a comfortable future, financially and that you will be paying it forward through your children. No doubt they will, if not now, down the road appreciate your wisdom regarding retirement planning.

Good luck!

You did so well with your investments from 2015 to 2019 precisely because you went “against the grain”. I know this, you know this – but the majority of millionaires here don’t get this based on the comments I’ve seen. You have to be your own person, or you’ll be herded by the Bogle mentality that provides mediocre returns and makes it so much more difficult to achieve any upward mobility. And that’s fine if you want to be safe, but you won’t see great returns tracking the indexes.

Case and point, the low cost index fund craze. I own 12 mutual funds, only one is an index fund and it’s up a little bit over 16% YTD (3 1/2 months). Not very shabby at all. I have owned most of my funds for several years now. Of Fidelity’s 3,741 offerings, I own 4 of their top 25, with returns of 29.90-49.90 YTD as of today! I doubled the value of our IRA’s in the past 3 years (including contributions) and plan to keep this up until full retirement age in 21 years.

My most coveted fund is up over 30x since it’s low in 2009. leveraged to the Nasdaq (40.66% annualized 10 year return!). Wanting to commit $2M after the next major market correction – consider that math. Very powerful stuff if you take the bombardment of “safe” advice with a grain of salt and use common sense to get ahead.

Good for you for doing your own thing in all your financial aspects, this takes great courage that I don’t see often, but applaud very much when I see this rare, humble wisdom.

MI-119

Sounds like you did well in the market and you’ve invested wisely. There’s risk-taking, and then there’s outright gambling. I’m thoughtful about the former, completely averse to the latter.

My individual stock holdings are a ‘greatest hits’ – names we all know with a long history of paying dividends. Not necessarily the most exciting but I’m glad they are a part of my portfolio and it’s all about the income now.

Good luck to you, I wish you continued success in the market.

Thanks Retirement4. I’m not smart enough to predict which companies will become the next greatest hits. Coupled with the increased risks associated with picking individual companies, I don’t think I have the knowledge, talent or experience to do this as well as you do.

I stick to mutual funds because the much more qualified fund managers (than I) decide when to enter and exit positions. I have found the funds I picked stay on top of the pack over the long term. I do not plan to introduce the $2M until after the next major correction, to minimize risk. Keep in mind this amount is only about 15% of my NW and about 2 years of income, a much smaller position than many take in the markets. If you read my interview, I am very aggressive about spreading risk between different investment vehicles outside of the markets. As a matter of fact, I currently have nearly $2M in CD’s and high yield savings, at no risk to principal. To me, adding significant positions at this stage of a bull market after the yield curve inverts is akin to gambling, but many will do this because the big fund companies tell them to continue dollar cost averaging into lofty market and thru bear markets, without independence of thought – it’s the grain. That’s okay, it will get people average returns with standard index funds. Just not enough for me at my current age.

M119-

Would you mind sharing what Fidelity mutual funds you are referencing? I would be interested to look the funds up. I have most of my money with fidelity. Thanks!

I see your link below. But what is your coveted fund? What is your top 4 out of 25? I would like to look at these closer.

My favorite fund, which I have owned for several years now is Direxion 2x Nasdaq (DXQLX). $1M invested a decade ago would be worth about $30M today. Per Fidelity, number 1 in terms of 10 year annualized return of 40.66%/year.

https://fundresearch.fidelity.com/mutual-funds/summary/254939200

The other 3 out of the top 25 (in terms of YTD returns) that I own are:

https://fundresearch.fidelity.com/mutual-funds/summary/316390863

https://fundresearch.fidelity.com/mutual-funds/summary/74318W846

(This one is quite volatile as the Chinese stock market is volatile).

https://fundresearch.fidelity.com/mutual-funds/summary/743185357

I personally would not buy them now that the yield curve has inverted, but I would seriously look at the most qualified sectors after the next major correction.

Those returns are insane! Need to do some reading…

MI-119- please share the names of these funds? I’m very curious as I’m switching out of some weak American funds my old FP was helping with. I’ve always been a bit of a Bogle admirer as I hadn’t had much luck on my own… I think I’m ready to step up my efforts in research.

This should help, I include leveraged funds in my research:

https://www.fidelity.com/fund-screener/evaluator.shtml#!&ntf=Y&levInvind=Y&sortBy=FUND_PRFM_DLY_NLD_RTN_YTD_PCT

I do not intend to introduce any significant new positions until after the next major correction as the yield curve has inverted and we’re in a very mature bull cycle.

Short term performance is important, but long term performance (>10 year) is critical for me as I intend to hold stellar funds for the long term. Also, the numbers mean absolutely nothing if your timing of purchase is not well chosen. The best time to take a position is when there is blood on the streets, and to practice restraint is when you see euphoria.

I mentioned in my interview my preferred sectors, that has not yet changed since.

Wish you well.

Very interesting… I’m waiting for the bloody streets!

Thanks… I’ll read up on these.

Thank you so much for providing such an open and detailed account of your transition to retirement.

This was an immensely useful read for me. I am in close proximity to your age and NW, but still slogging it out in a high-stakes MegaCorp career. I fully expect that if I continued on current trajectory, that somewhere in the next 2-3 years I would meet my career end in a similar fashion to yours, so having some perspective on how it usually goes down and the emotional content of the situation is truly helpful.

Perhaps a bit differently than your mindset at the time you were let go, I realize that I am pretty much FI – which provides peace of mind and allows me to not stress so much about it. My employer knows I’m FI too, which gives me a bit of leverage for the moment, as in “don’t screw around with me or I’m gone in 60 seconds”, but this will probably become a liability once my successor is seasoned and ready. I’d rather they canned me (for the nicer severance package) than me canning them, but we’ll see. Much of my pay is incentive comp, so really all they have to do is stiff me on the next bonus to send the message that its time – I would not put it past them, its a ruthless game.

In any event, I know that however and whenever it happens, I will be in shock and disoriented for awhile. My career progression has been decent, and I’ve had some great years and extraordinary experiences in my go-go days, but I never quite reached the level I would have liked, and so it’s not really going feel like an ending on a high note. I’ll be missed for a little while, I’ve mentored many and developed great relationships, but the machine will keep chugging along and will not miss a beat. That’s just the way it is.

I wonder what will be next. There is most certainly much ageism out there – and as a rampant form of discrimination it does not get the attention it should. Both wife and I feel a great need to be productive and useful, but we also want flexibility and work/life balance, which neither of us has had much of the past 30 years. I don’t think I’d take to full retirement well, but we’ll see.

At any rate, it is valuable to see how others are managing the transition. Don’t beat yourself up so much about the way you exited – many folks have had the same experience and if you ask me, sounds like you had a great run and made out quite well.

As M24 said and I shall echo: “Dude, you didn’t get fired. You won!!!!”

Hi, thank you for the feedback and comments.

While it sounds like you’re in a good place, your comment “don’t screw with me or I’m gone in 60 seconds”. I certainly felt that way at certain points, and it never worked out well. No one is indispensable. I’ve often heard it said, “better for a company to leave you, than to you leave them” but again, they have the control over how much of a send-off they give you, financially so my advice is to be humble, dedicated and a good employee, friend to all.

If and when the time comes to move on – either by your choice or theirs – take a deep breath, spend some time playing hooky, doing those things you never had the chance to do during the week and enjoy the sunshine. Your next endeavor will be there, no need to rush things.

Good luck!

Thanks, I completely understand where your perspective is coming from, and I’ve seen many people overplay their hand as you warned. But, I’m the sort of situation where “humble” (strictly from a professional, not personal perspective) does not get you very far. Dedicated and hard-working absolutely, yes, that is a minimum expectation. But as I have often tell my spouse, I am always one major error from the unemployment line (and at my level of responsibility all my decisions are major ones). It’s just the way it works in my realm – I have to be among the best at what I do simply to keep my job. So, I’m only as good as my last decision. To some extent, survival for +25 years in these shark-filled waters is a feat unto itself. I’m reminded every day that no one is indispensable and when I start to slip and my efforts cease to add to bottom line profits, I trust that the ax will come swiftly. Until then, I leverage whatever I can to be compensated at a level that makes it worthwhile.

Thank you for sharing so many insightful and honest comments. Your comments make me feel much better about our retirement and financial situation.

I can understand your comment about retiring a bit early but you handled the “retirement” gracefully with planning with your manager. I was discussing retirement with my husband and age 55 was the magic number due to the retired healthcare group health, similar to yours. My manager offered me a new position, pay increase and couldn’t understand why I kept saying no thank you to the added work. After 2 months of pressure to change jobs, I told him about my early retirement and was able to work until age 55, so that worked out well. My husband retired a few months after I did.

I haven’t found a financial planner yet, but do want assistance with a review of withdrawal plans for our 401k, ROTH IRA, etc. Similar to you, we live off dividends, interest and haven’t touched any of our principal. I have a small pension which pays for our retired group medical plan. Expensive, but I am happy to have the option to buy. Does your financial planner provide assistance on tax advantages? I’m not sure what type of person I need to interview and hire (CPA, Financial Planner, etc). I have a sizable 401K and thinking about converting to a ROTH due to tax advantages during the next 3 years. But we don’t have children, so not sure if there is benefit in paying taxes now and having reduced taxes during the RMD years. Taxes normally go up in the future but paying early now might not help us much.

Your comments about social security is helpful. We keep playing with the numbers too and perhaps will utilize the tools you mentioned. CDs are great, I feel a bit old fashion having cash and CDs but there is safety with liquid money. We are updating our investments to only have individual, mutual funds, ETFs that give us our retirement paycheck.

You didn’t mention wills or trusts. Would you be able to share? We set up a trust in case there were issues between the inheritors attempting to probate. Seems like people can change when money is involved, so we wanted to prevent that from occurring.

Your new lives sound perfect. Being with your wife, running errands when others are working, eating out with friends and enjoying life. My husband and I still reflect to each other, “we are out in the afternoon and others are working”. Never apologize for being happy and relaxed. Sometimes it is hard to find friends that can understand your new life, but be happy and do what makes you and your wife smile.

Loved reading this. A bit where I am. CPG, insight and analytics director, after yeArs of solid performance, feel like the company would like me gone. I’m not quite ready to be done though. Waiting to see how it all works out.

Thank you for the tips!

I’m always surprised that the wills and trusts issue/question doesn’t come up more often or isn’t a part of the interview. In the “Findings from 100 Millionaires” post, ESI found that most did not have an estate plan. And even those who said they had talked/thought about the issue often did not have a formal plan.

So I’m also wondering if the retirees will follow a similar pattern — would love to see the question added.

I’ve witnessed the process of settling a couple of ~$1mm estates, so can only imagine what can happen in a multi-million dollar estate. The sharp daggers come out in surprising ways and from unexpected corners. Nothing can fracture and destroy a family faster than the infighting that can occur towards end of life and after death of a parent and/or a strong family patriarch or matriarch. Sometimes its not just about the money, it’s also assets with nostalgic value. Probate can be somewhat of an emotional battlefield when you think about issues of selling a family home or splitting up (or selling off) artwork, jewelry, photos, etc.

Trusts can be part of the solution, but really IMO, what I’ve seen is that you need three things:

1) A really really experienced attorney, preferably one that specializes in estates. The general practitioners are good at small estates, but often lack quite a bit of technical knowledge when it comes to designing and actually settling a complex estate. What I saw was that the generalists somewhat outsourced the settlement process to para-legal contractors who were not especially competent. Having seen the problems this created, we went with an estate specialist at one of the big law firms because not only is he renown in the field, but his firm would be capable of providing plenty of back-up resources and support to the surviving spouse or (in case we both perish in an accident) our executor. Yes, he’s very expensive, but over time we’ve found the quality of advice and peace of mind that brings to be well worth it.

2) Choose your executor carefully. I know this sounds like stating the obvious, but being an effective executor for a complex estate and/or complex family situation will require a host of different skills. Clearly it has to be someone you trust, but also someone with some business and financial skills, who is comfortable dealing with legal matters, who knows your family situation well enough, who understands your wishes (as you can’t anticipate everything and they will have to use their judgement), who has enough backbone to keep everybody from tearing each other apart, and who has enough empathy to understand their grieving process.

3) A well-crafted, clear estate plan. Needless to say, finding the strong attorney is key to this one. I believe the more clear one can be about their wishes and intents, the easier for everyone.

Even the best laid plans can go awry and it is difficult to predict the circumstances of our own demise. I find that we need to update our plan every 2-3 years – for sure it is not a set it and forget it sort of thing.

One should also consider the possible circumstances leading up to death – healthcare representatives, power of attorneys, these things need to be in place BEFORE you need them. A lot of assets go missing before you even get to probate – this happens more often than you would think.

In part the plan is not just about taking care of us, it’s about easing the burden on our families and loved ones too.

P.S. my comment was meant to reply to CB’s

MMiguel: you listed some very good reasons why an estate plan with a trust is important. I was the executor for my mother’s estate and she had several trusts. Over the years, I met her attorney, understood my mother’s wishes and had her living close to me so following her plans went well. My spouse didn’t understand the value of an estate plan since he never experienced the complex documents and potential situations. After his mother passed with a simple will and inheritors began fighting, he agreed quickly to creating our estate plan. Money no matter how much can change people.

CB: Sounds like your mother really knew what she was doing, or at least had some very good advice. Plus, if a recall correctly from prior posts, your business background would have contributed to things going smoothly.

Parents of wife and I are all deceased now. We had similar experiences to yours – on my side there were not a lot of assets, but the will was probably 30 years old and practically unintelligible. There was no power of attorney or healthcare proxy either to deal with illness before death – that added a lot of stress to an already stressful situation.

On wife’s side, we nudged her parents into getting everything in order, and when the the last to die became unable to care for themselves, we were able to step in at just the right time, and take care of them and their affairs, before and after death. Having a clear and decisive decision-maker was critical to being able to provide appropriate care in the latter stages of illness.

I cannot emphasize enough, and I’m sure you get it, that the plan needs to consider not only death, but all the potential issues that can arise before that. Absent an accident and stroke, for the elderly, there is usually a slow decline, and a “grey” zone where physical and cognitive abilities are diminished to the point where they cannot make decisions for themselves. It’s a tricky dance because the nature of cognitive decline makes it difficult for the affected individual to recognize their own condition.

If there is not a clear plan, responsible party, and legal docs to back it up, that power vacuum tends to attract all kinds of unsavory types, ranging from sketchy family members with financial agendas and/or emotional issues to outright scammers and grifters.

I know it sounds over the top, but there is a proliferation of multi-million dollar scams out there targeting the elderly. Everything from fake charities to medicare fraud. It’s pretty bad, and we had to spend an enormous amount of effort just protecting our parents assets from all this. I hate to be such a downer, but I’ve seen all this up close – maybe too close. Goes without saying that millionaires are going to be bigger targets.

Ok, I’m starting a new policy — no one can suggest a question be added unless they suggest which one is deleted! LOL!

I know it would be great to add about 10 different questions, but these people already answer so many (most of the posts are 3k to 4k words) that we’re at the breaking point of who will even volunteer.

As I said when we put the questions out there for suggestion…there’s no way we can include every one we’d all like to see. 😉

LOL, ok I get it. Not exactly the most upbeat and inspiring question to be asking.