Today we continue our conversation with Scott A. Olson, co-owner of The LTC Shop.

Today we continue our conversation with Scott A. Olson, co-owner of The LTC Shop.

In case you missed part 1 of the series, you can find it here.

Scott and I had a chat via email and I’m posting those conversations.

My questions are in bold italic and preceded by “ESI:” while his responses begin with “Scott:”.

At the end of each topic I add an “ESI’s Thoughts” section that summarizes my take on the issue and what Scott has said about it.

Once that topic is completed and we’re ready to move to the next one, I’ll separate the sections with a series of dashes like this: “——————-“.

We now continue with Scott giving his responses to my original question…

ESI: Please review the two long-term care (LTC) insurance articles I sent you (Long-Term Care Insurance Overview and Who Needs Long-Term Care Insurance?). What did I (and the commenters) get right? What did we get wrong (or something that needs to be considered from a different way)?

Scott: Companies dropping out of the business.

You mentioned in your article that you’re concerned that “you get a policy and then your insurer decides to leave the business of offering LTC insurance policies. Not sure what the implications are for current policyholders when that happens, but they can’t be good.”

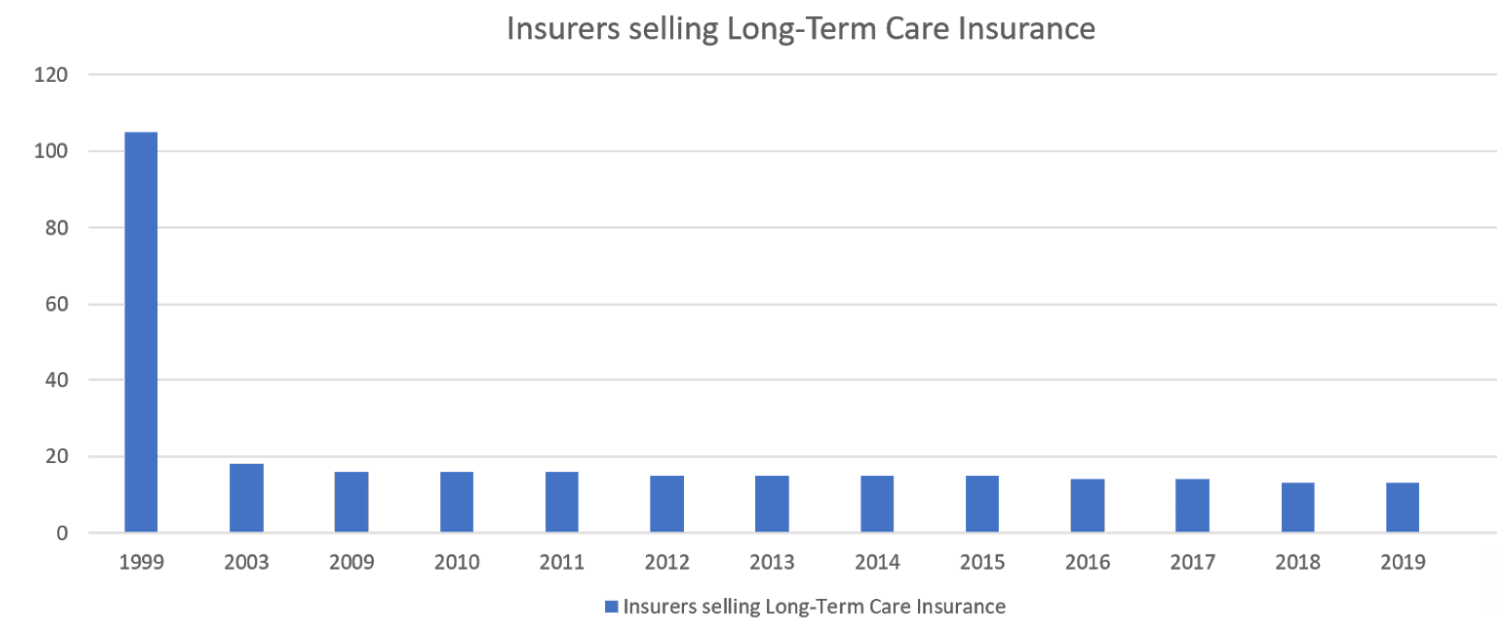

You also quoted NerdWallet, “The number of insurance companies selling long-term care insurance has plummeted since 2000. More than 100 insurers were selling policies in the late 1990s, according to a 2016 study published by the National Association of Insurance Commissioners. Less than a dozen are selling policies today.”

The truth is that over 173 companies sold long-term care insurance at some point. Today there are 13 companies selling long-term care insurance in most states.

The issue, however, is not how many companies sell long-term care insurance today, but how many companies are paying long-term care insurance claims. Fortunately, the long-term care insurance claims data is published every year. All 173 companies paid long-term care insurance claims in 2018 (the most recently published data). They don’t publish the data for all 173, but they do publish the data for the 100 largest. When combined, the 73 smallest companies account for less than 1% of the total number of LTCi policies in-force.

Here’s a link to the most recent report.

Long-term care insurance policies are guaranteed renewable. That means that the insurance company guarantees to renew your coverage every year, as long as you pay your premium on-time. If the insurance company stops selling new policies, they still must fulfill all of their legal (contractual) obligations for every policy they’ve ever sold. They cannot change the contract.

Most companies stopped selling long-term care insurance between 1999 and 2003. The number of companies selling long-term care insurance since 2003 has been relatively stable.

Most of the companies that stopped selling LTC insurance made that decision AFTER the Rate Stability Regulation was approved by the NAIC in December 2000. The Rate Stability Regulation is something that didn’t come up in your research, but I’m sure we’ll get to it during our discussions. The Rate Stability Regulation forces insurance companies to reduce their profits if they seek a rate increase. It removed the profit incentive from rate increases. That’s why you see such a huge drop from 1999 to 2003.

The NerdWallet article was wrong when it said, “The uncertain cost of paying future claims as well as low interest rates since the 2008 recession led to the mass exodus from the market. Low interest rates hurt because insurers invest the premiums their customers pay and rely on the returns to make money.”

The “mass exodus” happened several years before the 2008 recession and it had nothing to do with low interest rates. The “mass exodus” had everything to do with the new pricing regulations.

To add some perspective on the number of carriers selling long-term care insurance, in the 1980’s there were over 400 insurance companies that sold medical insurance. How many companies sell medical insurance today?

In most states, consumers have more companies to choose from for long-term care insurance than they do medical insurance. The same is true for disability insurance. More companies sell long-term care insurance than disability insurance, in most states.

ESI’s Thoughts

I thought this was very informative and did alleviate some concerns I had.

What do you think of his response?

———————————————

Scott: Who needs long-term care insurance?

As I mentioned above, your article does a good job of explaining why you’re able to self-fund. However, I suspect that most of your million-plus visitors every year are not in a financial position similar to yours. How can those readers decide if they should buy long-term care insurance or not?

Again, it’s important to point out that the decision should primarily be based upon income, not assets. Let’s look at a few examples. These cases are taken from real people I’ve worked with:

Couple #1:

This is a married couple in their mid-60’s. They just retired. Their home is paid off and worth almost $600,000. They have two CD’s of $100,000 each. They have no other savings or investments. They live comfortably on their social security checks and a small pension totaling about $2,000 per month for the husband and about $1,600 per month for the wife.

Even though this couple has a “net worth” of $800,000, they should NOT buy long-term care insurance. They could easily qualify for Medicaid by spending down just some of their savings. Also, if one spouse had to qualify for Medicaid, the spouse at home would be able to keep almost all of their combined monthly incomes.

Their residence is not at risk. Their income is not at risk. Only a little bit of their savings is at risk. They definitely should NOT own long-term care insurance.

Couple #2:

Here is another retired married couple in their mid-60’s. They live near their children, in a high-cost of living area. They do not own a home. They rent. They have worked in academia all their lives. Due to a bad divorce and some financial mistakes, they have only $150,000 in savings. The wife has a pension of $75,000 per year, with a COLA. The husband has a pension of $90,000 per year, also with a COLA. They both have children from prior marriages.

If one spouse needs care, in order for Medicaid to pay for the care, that spouse’s entire pension will have to go towards the cost of care. The at-home spouse would lose all of the income of the spouse who needs care. If this couple can qualify for a reasonably-priced long-term care policy, it would make sense for them to own it. (They did, by the way.)

Most people would say that Couple #1 with $800,000 of net worth should buy LTC insurance, but the couple with only $200,000 of net worth should not buy LTC insurance. “Net worth” is only part of the story and in both of these examples the household income is the more important factor in determining which couple should own long-term care insurance.

In summation: To determine if you should consider owning long-term care insurance, first determine what you’d have to lose in order for Medicaid to pay for your long-term care.

ESI’s Thoughts

First of all, I’m not sure he’s aware how many millionaires we have reading this site. 😉

I think many readers can certainly self-insure.

Second, we’ll get into Medicaid-related issues later on, so I’ll save my comments for then.

———————————————

Scott: Long-Term Care Partnership Programs

Unfortunately, your articles didn’t mention the Long-Term Care Partnership Programs which are in effect in 45 states. The first Partnership Programs were started in the early 90’s in California, Connecticut, Indiana and New York. The Deficit Reduction Act of 2005 opened the program up to all 50 states. Five states have chosen not to participate in the program: Alaska, Hawaii, Massachusetts, Mississippi, and Vermont.

To help reduce Medicaid’s expenditures on long-term care and preserve Medicaid for the truly needy, 45 states have created a “public-private” partnership to help the middle-class plan for long-term care. These “Long-Term Care Partnership Programs” encourage the middle-class to purchase an amount of long-term care insurance that is equal to their assets. If their long-term care insurance policy runs out of benefits they can apply for Medicaid to pay for their care and their assets would be protected from Medicaid “spend down” and Medicaid “estate recovery”. More specifically, for every dollar their long-term care partnership policy pays in benefits, they can protect a dollar from Medicaid.

Couple #3:

Married couple, husband age 61, wife age 58. They could retire now if they had to, but they both love what they do. He’s a former controller and does business consulting part-time. She works part-time for a local pre-school. Their net worth is about $1.8 million. Their house is worth about $600,000 with a small mortgage. Most of their investments (about $1.1 million) are in traditional IRA’s and 401k’s. They expect to live on roughly $85,000 per year once they fully retire.

He and his wife bought a long-term care partnership policy that starts off with $930,000 of shared benefits. The benefits grow every year by 3% compounding. By the time they are in their mid-80’s it will have over $1.9 million in benefits.

Protecting their assets for his wife and their two children is very important to him. He insisted on getting a long-term care partnership policy in order to protect their assets just in case they exhaust all the benefits in their policy and have to rely on Medicaid.

If, for example, the policy paid out $1.9 million in benefits, they could keep $1.9 million in additional assets if they ever have to apply for Medicaid.

Their annual premium is a little over $6,000 per year because they both had some health issues and were not able to qualify for the lowest rates. Fortunately, they are able to deduct most of the premium off the top of their income since he’s self-employed. After the federal income tax savings, the net cost for the policy each year is about $4,300.

Couple #4:

He’s 57. She’s 55. They emigrated to the U.S. from India in 2000. They used their life’s savings to make a down payment on an 800 square foot condo in which they still live. They have about $90,000 worth of equity in the condo. They have about $200,000 in savings. He’s a bus driver and she works in a grocery store. They are about ten years from being able to retire.

They bought two long-term care insurance policies where they share $150,000 in benefits. The benefits grow every year by 3% compounding. By the time they reach their late 70’s/early 80’s, their policies will have about $300,000 in total benefits. If they were to receive $300,000 in benefits from the policies, they could apply for Medicaid and they could protect $300,000 plus the roughly $125,000 Medicaid already allows the healthy spouse to keep.

Because the benefits are modest, their combined monthly premium is less than $160 (about $95 for the wife and $65 for the husband).

These “Long-Term Care Partnership Programs” encourage the middle-class to purchase affordable long-term care insurance coverage. They can target how much long-term care insurance they need based upon how much of their savings they want to protect from Medicaid.

If they want to protect more savings they can buy more benefits for a higher premium. If they have less savings they can buy less benefits for a lower premium. It’s an equitable and affordable solution for those who want to plan ahead.

ESI: Are there any sort of restrictions for any reason on Long-Term Care Partnership Programs?

Scott: To apply for a Long-Term Care Partnership policy there are no asset or income requirements.

To receive benefits from a Long-Term Care Partnership policy there are no asset or income requirements.

If, after using the benefits in a Long-Term Care Partnership policy, the policyholder applies for Medicaid, the policyholder must still meet the Medicaid eligibility requirements. However, the eligibility requirements are more lenient for someone who has used their Long-Term Care Partnership policy. For every dollar their Long-Term Care Partnership policy has paid in benefits they can protect one extra dollar from Medicaid.

ESI’s Thoughts

He’s right. I didn’t know anything about Long-Term Care Partnership Programs. None of the gazillion articles I read in doing my LTC research mentioned them.

FYI, Scott has a page dedicated to these that you can find here.

Just to add a bit more clarity (hopefully) to what these are, I found the following articles discussing them.

First, here’s what AARP says (FYI, this post is from 2006 — you think Google could find something more current for page 1 results):

The long-term care insurance (LTCI) partnership program was developed in the 1980s to encourage people who might otherwise turn to Medicaid to finance their long-term care (LTC) to purchase LTCI. If people who purchase qualifying policies deplete their insurance benefits, they may then retain a specified amount of assets and still qualify for Medicaid, provided they meet all other Medicaid eligibility criteria.

Although the partnership program was intended to attract lower- to middle-income Americans (the cohort most likely to spend down to Medicaid), state policyholder surveys indicate that most purchasers have substantial assets. The majority of purchasers in California, Connecticut, and Indiana had assets in excess of $350,000. In contrast, the average person age 55 or over has less than $50,000 in assets. The New York program, unique in that it allows unlimited asset protection for purchasers, has primarily attracted higher-income purchasers, because of this feature and its resulting higher premium costs.

Second, here are thoughts from Kiplinger (a 2008 article):

One of the most interesting new developments in long-term care is the expansion of the state long-term care partnership programs. In states that have passed these laws, people who have an approved long-term care insurance policy can qualify for Medicaid to help pay their long-term care bills after they’ve exhausted their coverage without having to spend almost all of their assets first.

If their long-term care policy provides $200,000 of benefits, for example, they’ll be able to protect $200,000 of their assets after using up their long-term care coverage and have Medicaid pay the bills.

Here are the specifics for what my state (Colorado) offers:

Colorado allowed insurers to sell qualified LTC Partnership policies beginning on January 1, 2008. For every dollar that a LTC Partnership insurance policy pays out in benefits, a dollar of personal assets can be protected (disregarded during the eligibility review and at estate recovery) if you choose to apply for Health First Colorado (Colorado’s Medicaid Program).

For example, LTC Partnership policy holders who apply for Health First Colorado coverage are able to maintain some level of assets (equal to the LTC insurance benefit paid) above the $2,000 Health First Colorado asset limit currently in place for eligibility purposes and a corresponding disregard during the estate recovery process at the individual’s death.

Partnership and non-Partnership policies are virtually the same except that Partnership polices have the added benefit of allowing policyholders to protect a portion of their assets if they choose to apply for Health First Colorado.

This is some important (and interesting) information that we don’t see covered much (as evidenced by how old these top-ranked articles are).

Discovering Long-Term Care Partnership Programs doesn’t change much for those who aren’t planning on the Medicaid option, but obviously does for those considering it.

Let’s move on…

———————————————

ESI: The examples are helpful, but they are very specific. Obviously personal finance is personal (i.e. unique to the individual’s situation), but I’m wondering if there are any rules of thumb people should consider when thinking about the subject of LTC.

Scott: There are only 2 rules:

1) If someone can easily qualify for Medicaid, then they don’t need any type of long-term care insurance.

2) Someone should self-fund their long-term care when the insurance options available to them are not a good value.

ESI: I’m not sure I’m clear on when you would recommend that people should self-insure. Is there any time that this is the answer? If so, what circumstances lead to that answer?

Scott: Someone should self-fund their long-term care when the insurance options available to them are not a good value.

ESI: How do you determine whether or not an insurance option available for someone is or isn’t a good value?

Scott: Math.

- P = Annual premium for $1,000,000 of long-term care insurance

- W = Net Worth

If P/W is less than .005 then it is probably a good value.

ESI’s Thoughts

I LOVE having this sort of information! A good rule-of-thumb is a great starting place for considering this topic IMO.

Let’s say I wanted $1 million of LTC insurance.

That means it would probably be a good value for me if the annual premium was $20,000 ($4 million net worth * .005) or less.

That makes it seem like a no-brainer.

But….

Is this a legitimate rule-of-thumb or one made up by insurance agents to get people to buy more policies? The skeptical side of me wonders.

Why do I need it anyway if I can afford to self-insure?

Your thoughts?

For more on this series, check out part 3.

Thank you, ESI, for another very helpful post. Question for Scott: For couple #1, you said they should opt for Medicaid instead of LTC, and that their residence is not at risk. Because of Medicaid Estate Recovery, wouldn’t the state own their residence and take possession of it after both spouses die? That means the couple couldn’t sell their home or move, and their children and grandchildren couldn’t inherit the home. Is that correct?

Great questions, Diogenes.

Diogenes: Because of Medicaid Estate Recovery, wouldn’t the state own their residence and take possession of it after both spouses die?

Scott: The state could put a lien on the home and the state could reimburse itself for the cost of their care after both spouses have passed away.

Diogenes: That means the couple couldn’t sell their home or move…

Scott: They could sell their home or move, as long as the lien is paid when the home is sold.

Diogenes: …and their children and grandchildren couldn’t inherit the home. Is that correct?

Scott: It depends upon how big the lien is. The state has the right to reimburse itself for the amount it paid for their care. When both parents have passed away, if the house is worth $600,000 and the state paid $400,000 for their care, then the children would be able to keep the difference of $200,000.

Scott’s Thoughts: This family (parents & grown children) could certainly benefit from a long-term care policy, especially a long-term care partnership policy. However, a well-designed long-term care policy for this couple (since they are in their mid-60’s) would take up too much of their modest monthly income. If this couple insisted on buying a long-term care insurance policy, I would encourage the children to buy it for their parents (or at least pay half of the premium).

Thanks very much, Scott!

I hadn’t heard of the agreement with states either. Very interesting.

Question: How are LTC policy decisions influenced when a Medicaid trust Has been formed to protect a person’s home and other assets?

Thank you, David, for your comment.

The Long-Term Care Partnership Programs are a perfect solution for the middle-class to plan for long-term care. Everyone can target how much long-term care insurance they need based upon how much of their assets they want to protect from Medicaid. If they want to protect more savings they can buy more benefits for a higher premium. If they have less savings they can buy less benefits for a lower, more affordable, premium. It’s an equitable and affordable solution for those who plan ahead.

Sadly, the programs suffer from anonymity. That’s why I wrote a book about it.

45 states have now enacted a Long-Term Care Partnership Program. Click on the map on this page to learn more about your state’s program:

https://www.ltcshop.com/long-term-care-insurance/partnership-program/

David’s Question: How are LTC policy decisions influenced when a Medicaid trust Has been formed to protect a person’s home and other assets?

Scott: That’s a very broad question and difficult to answer without more details. I’ll answer with a few important points and if you’d like further clarification, please respond.

1) The two largest assets most people have are their retirement account(s) and their primary residence. Retirement accounts canNOT be put into a “Medicaid Trust”. A primary residence can be put in a “Medicaid Trust” but you then lose all the tax advantages of a primary residence (e.g. capital gains tax exemptions, step-up in cost basis, etc…)

2) Many of the best facilities and many of the best home care agencies do NOT accept Medicaid (because Medicaid reimbursements are very low). Therefore, someone should only view Medicaid as a “payer of last resort”.

3) A “Medicaid Trust” can protect some assets, but it does NOT protect income. Therefore, qualifying for Medicaid could have an adverse effect on the healthy spouse’s lifestyle/income.

4) A “Medicaid Trust” only protects assets after they’ve been in the trust for 5 years. During that 5-year period the assets in the trust are not protected.

Let me know if you need additional clarification.

Thank you, Scott, for your answers.

Another question I had was about carrying your partnership policy (or any LTC policy) to another state. I have lived in many states and expect that I’ll move again one day. Are there any considerations with regard to moving other states?

Great question, David!

45 states have LTC Partnership Programs. The only states that don’t have LTC Partnership Programs are:

Alaska, Hawaii, Massachusetts, Mississippi, and Vermont.

44 of the 45 states that have LTC Partnership Programs honor all the other programs. Only one state does not honor the other states’ programs. That one state is California.

Therefore, if you buy a long-term care partnership policy, it will be honored, no matter what state you move to, as long as you don’t move to California (or one of the five states that does not have a program).

When is LTC a “good value”?

Scott: Math.

P = Annual premium for $1,000,000 of long-term care insurance

W = Net Worth

If P/W is less than .005 then it is probably a good value.

This is math, but unfortunately it is bad math.

Value can never be based on net worth. Need could be based on net worth but not value.

Value is based on the benefit you can get vs the cost you pay.

Consider purchasing anything else and doing a value calculation on it based on what you are worth. The more you are worth the better value everything is. That doesn’t make any sense at all. It would be true to say the more you are worth the less the cost of anything else affects you, but that has nothing to do with value.

This formula would imply the more you are worth the more it makes sense to get a LTC policy because the value will appear to be amazing. That, of course, is nonsense.

There may be good reasons to have an LTC policy, but this formula is no way to go about deciding.

I am also confused by the math. I would say that you should base the value of the policy based on the payout. So if you have a $1M policy, then you should calculate using 0.005*$1M = $5000. Which means if the premium is more than $5k/yr., it’s not a good deal. That on top of whether the 0.005 ratio is truly accurate.

Thanks, Apex, for your detailed reply. My first grade teacher, Mrs. Johnston, always told me that I was good at math. (My bubble has burst!)

I’ve had a long day today, but tomorrow morning I’ll sharpen my pencil and see if I can improve on my formula.

FYI, you and I do agree on most of the points you made here.

I’m interested in long term care partnership.

The long-term care partnership program is the perfect solution for the middle-class.

Thanks again for a great series. Thanks to Scott for being to open on this topic. I just have a few questions I’m hoping to get clarification on.

1. I totally get the math part (P/W). I’m a little confused as to why net worth is part of the calculation when early in the post the buy/no buy included the factor of income. I understand this is just a quick indicator, but

2. I’m a federal employee and we have an OPM sponsored program (https://www.ltcfeds.com/ ). Is there any benefit or concerns with buying through a plan like that verses one out on the general market?

I, too, am eligible for Federal LTC insurance and am interested in possible benefits and/or risks with the program.

Thank you, Paulz, for your great questions. I’ll answer question #1 later. Regarding the long-term care program for federal employees, it’s a good program. My mother-in-law bought her long-term care policy from them. It has changed a lot over the years, however.

Some important points about the program:

1) It does not qualify as a long-term care partnership program.

2) It is not regulated by the Rate Stability Regulation.

3) It does not have any preferred health discounts.

4) It does not have any marital discounts.

5) It does not allow spouses/partners to share benefits.

6) It has “unisex” rates. “Unisex” rates are good for women but not-so-good for men.

A healthy married couple is probably better off getting a policy on their own rather than buying a policy from LTCFeds (because of the marital discount and because of the ability to share benefits).

A healthy, single male is probably better off getting a policy on his own rather than buying a policy from LTCFeds (because individual long-term care insurance policies cost about 25% less for men, as compared to women.)

A healthy, single female who lives in Arizona, California, District of Columbia, Florida, Montana or New York is probably better off getting a policy on her own because “unisex” rates are still available in those jurisdictions.

A single female who does not live in those jurisdictions is probably better off buying her policy from LTCFeds because LTCFeds uses “unisex” rates.

Thank you for this reply. My biggest barrier to considering a LTC has been that I see the probability of either my spouse and I needing it and not both of us needing it, hence having to buy two policies versus a combined policy has put me off. I was going to “get serious” and make a decision one way or the other in the next year and this serious and your points have been very helpful.

Quick question if not already asked, is there a real reason the partnerships have not been better advertised. I’ve been reading up on LTC and this series is the first time I’ve seen it, and the first two classes (third was canceled due to COVID) of an Elder care and Finance class at a community college didn’t discuss this at all or even hint at it.

Thank you to the astute comments about value.

Based on my parents experience with long term care insurance (I realize it is anecdotal) I am reluctant to buy it. My mom needed moved into assisted living after not recovering completely from a serious illness. After the illness she had trouble with her balance so she was not able to cook, do laundry, and the like. She was in assisted living for just over 2-1/2 years but the only assistance towards daily living that she received was help with showering. LTC requires assistance with at least 2 of 6 activities (including dressing, eating, toileting, transfer, and something else). Her final two months in assisted living she required help with dressing as well but she still had a 90 days of paying her own way before benefits kicked in. She paid premiums for at least 20 years.

My dad was in assisted living for almost 8 months before he passed away. He had been getting bathing assistance at home before that which counted towards the 90 days of paying his own way before benefits kicked in. His LTC policy paid $100/day so he did collect a little bit but no where near the amount he paid in premiums over the years. I’m guessing he paid for about 15 years.

My parents had decent income and savings (my mom had just over seven figures in the bank when she passed away, 7-1/2 years after my dad). As my sister said, if the premiums had been invested instead there would have been a really nice pile of funds.

Kate, most of the LTCi policies that were for sale in the early 1990’s were terrible (compared to today’s policies). And most of the policies for sale in the 1980’s were not worth the paper they were written on because they had so many restrictions.

In the mid-90’s the insurance industry pushed for federal guidelines for long-term care insurance to help standardize benefit triggers.

Legislation was passed in 1996 and became effective in 1997. Most policies purchased since 1997 meet the federal guidelines for benefit triggers. In other words, if you compare 10 policies available for sale today, and all 10 are “federally-qualified” policies, the benefit triggers will be almost identical, word-for-word.

One of the major improvements to LTCi policies over the past 15+ years is adding “standby assistance” as a benefit trigger. My mother-in-law needs physical help to bathe/shower. However, she can dress herself, but, she needs someone within arm’s reach to steady her in case she loses her balance. That’s called “standby assistance”.

This “standby assistance” to help her dress, combined with needing help with bathing/showering meets the 2 of 6 ADL requirement. Her LTCi policy is covering the full cost of her assisted-living facility each month (over $6,000 each month). She’s already received about 5x what she paid in premiums and she has about half of her total lifetime benefit.

Does everyone who owns long-term care insurance receive more in benefits than they pay in premium? No. It would not be insurance if every one who bought a policy made a huge claim. Insurance is sharing risk between yourself, the insurance company and the rest of the policyholders.

Between myself, my wife, and our 4 sons, I’ve paid over $60,000 in auto insurance premiums in the past 10 years. We made two claims for minor accidents. Those claims equaled about $8,000 in benefits to us (after our $1,000 deductible). I’m thankful that we didn’t have any major claims. Some policyholders receive back more than they pay in premiums. Most policyholders receive back less than what they pay in premiums.

I’m sure my mother-in-law wishes she was fully independent and did not need to use her LTCi policy. But, she does need to use it. She was in perfect health when we encouraged her to buy the policy. I felt guilty encouraging it to buy it since she was in such good health.

Super-informative piece, thank you for creating and publishing this. And yes, I am among those sitting here reading this also saying: I never heard of these partnership policies.

Useful post. Finally, a clear answer to when to self-fund, with a simple formula.

I need to think through Apex’s comments. And do some modeling to see if the formula works as a decision-making tool across various scenarios. Particularly versus expected long-term asset appreciation rates. The cost is not just paid Premium but the lost future-value of that Premium from the policyholder’s asset base.

I still don’t like the fact that premium isn’t fixed, but subject to change. Making the “P” or premium in the formula a variable subject to change in the future. How do we account for that uncertainty in planning whether to self-fund versus using a Medicaid Partnership Policy? The purpose of insurance is to transfer risk that you can’t afford to bear if realized. The variability of premiums in the future (albeit with regulatory oversight for actuarial justification), means policyholders lose a key feature of insurance — predictability. It’s no longer a fixed expense.

Wow. It’s very rare nowadays to see for the first time information on this subject and the long term partnership program was news to me.

Sounds like an interesting option for sure but I guess it all depends on the state premiums.

I do not see the need to have the partnership program cover the entire net worth you have. I think that would be overkill for those with $2M or more as I doubt if you got a 2M policy you would use it all up and then overpaid for the extra unneeded coverage.

I would like to know what the typical cost of LTC would be for an above average benefit (good facilities and care) and the typical length that people require this (I have heard it usually is less than 3 yrs). If that is truly the case I would think $1M coverage would be more than adequate.