Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in December.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

We are 57 and 52.

We’ve been together since 1994, married since 1996.

Do you have kids/family (if so, how old are they)?

We do not have kids, but we have nieces and nephews who we treat like grandkids.

We have people say to us, “You don’t have kids so it is easy for you.” That is not true and if we have had kids yes we would have needed to work longer but people use their kids as an excuse when it comes to wealth building.

I know people who have done both, well.

What area of the country do you live in (and urban or rural)?

Urban and moving to urban/rural when we retire in 2022.

What is your current net worth?

$1.6 million plus a lifetime pension of about $42K per year for the next seven years, $37K for the five after that and then $32k each year after that (once each of us reaches Medicare age we get a reduction in HC portion of benefits.)

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

- Company Stock – 7%

- Mid/Small Index Funds – 15%

- Growth Stock Mutual Funds – 10%

- S & P 500 Large Cap Index Fund – 25%

- International – 15%

- Bonds/Cash – 8%

- House (paid for) – 20%

- No debt

EARN

What is your job?

I am a Project Management Professional, Senior Manager, run a Project Management Office in US for a large US Based Company. I have been doing logistics and project management since 1983 counting my time in the Navy.

Wife is Assistant Development Director for a non-profit and has worked mainly around Healthcare & Healthcare Insurance before her current role. She has a bachelors degree in communications.

What is your annual income?

Currently at $230k per year combined.

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

Post Military, $25k first year, 747% growth since then.

My wife has always earned between $30k and $50k per year except the two years she took off to finish her college degree.

To earn more I just kept educating myself about leadership, kept my head down and did a good job. I became a solid leader and that leadership and learning carried my career along.

For my wife she is a worker, always there, always on time, always will to do more and that led her to financial success.

What tips do you have for others who want to grow their career-related income?

Find something you like to do is the most important. If you do not like what you do or you are not passionate about it will be hard to be successful.

Once you are doing that you need a budget and have 6 to 8 months of expenses in the bank.

Once you control your money and you and your spouse are on the same page about money your focus shifts to growing your career which will grow your income.

Continuous education is important, and you must do things to ensure you are a great communicator, understand how to manage your time, manage flow of information (there is no merit badge for having the highest number of unread emails) and become a leader who is not afraid to lead and understand how to utilize conflict to your advantage.

Do not shy away from looking at the military as a starting point. Many people are shocked when they find out how many successful people over the years started with service. There are many great training opportunities that translate to the public sector. I was a logistics specialist and that was one of the catapults of my career.

What’s your work-life balance look like?

We exercise, play golf, attend sporting events, like the arts and spending time with friends and family and we have done that throughout our careers.

One must schedule this time also because committing to these things and planning for these things forces you in a way to follow through and these are the things that help keep you motivated.

I love to cook and we like to go out to eat but we only do that normally about three times a week.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

My wife and I served as City Commissioners, she for 6 years and me for 4 years. We did not do it for the money, we only drew about $1000 a year after taxes, but the experience was so valuable.

We also get dividends from my company stock and those had become quite large over the years of holding those assets and we chose since that was not really a retirement account since it was outside of 401k and IRAs, we used that money as a reward for our efforts.

SAVE

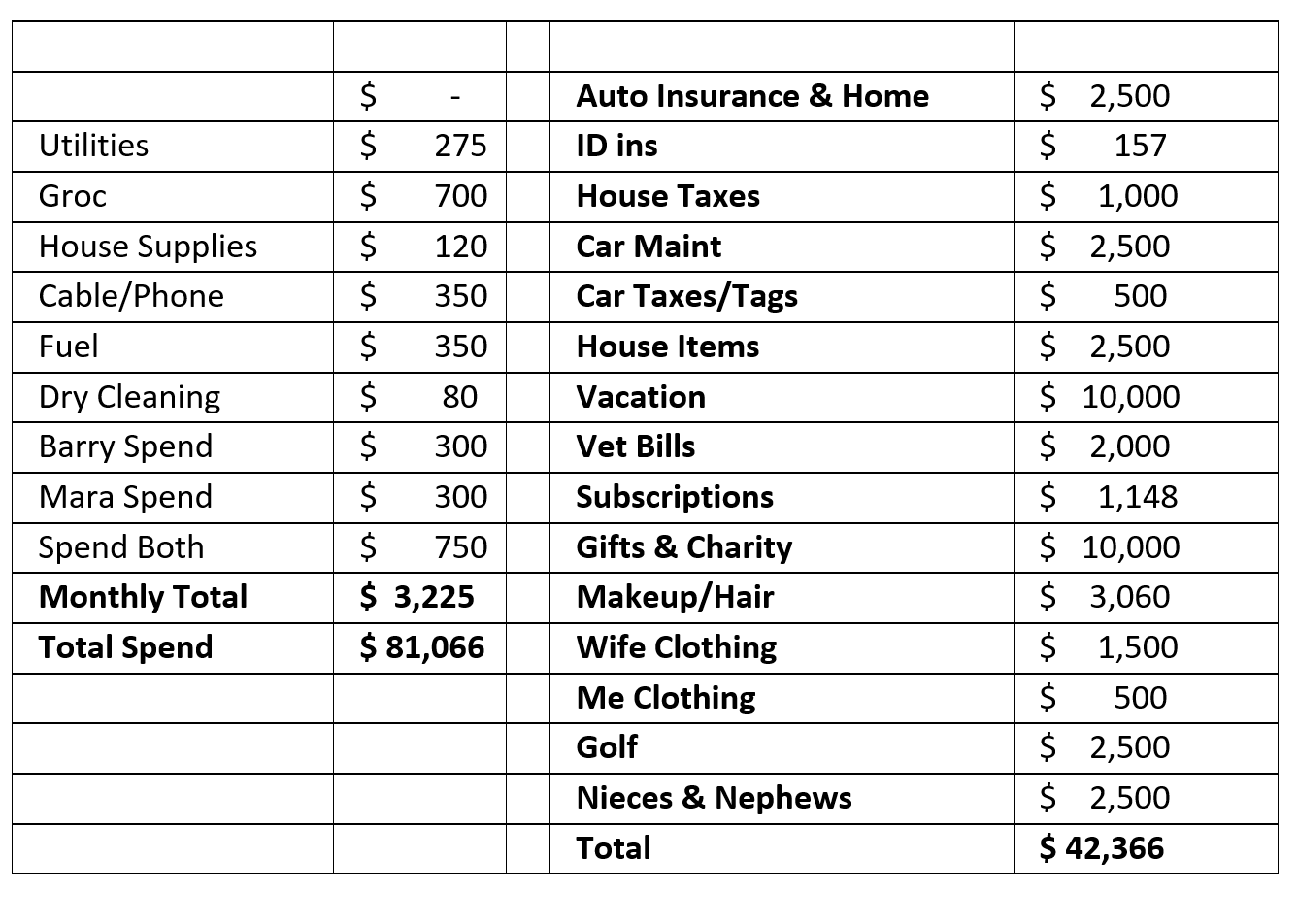

What is your annual spending?

$85k per year now.

We have our retirement expenses planned through the age of 105 for me and for my wife 100 and we will never run out of money.

I think it is a myth that people spend less in retirement, as we plan to spend more each year up until I am in my 80’s and then spending does wind down a bit.

What are the main categories (expenses) this spending breaks into?

Do you have a budget? If so, how do you implement it?

Yes, as listed above, we track revenue in and expenses out, just like a Profit and Loss Statement, and expenses are post investment expense and since 1994 we have always put at least 15% of our gross income into retirement accounts.

The budget or tracking of expenses to me is the most important, as you have to know where it is going and why. I do all the admin work on the budget/expense tracking, and we meet monthly when the expense is compiled for the month.

Also, even though I am the primary bread winner we both get the same amount of spend money each month on ourselves, aka “blow money”. I know working married couples who do what I call “halfsies” on the bills, even after both are putting money in retirement, the primary bread winner has more to spend. To me those people are roommates not partners and the partnership is the best approach to wealth.

What percentage of your gross income do you save and how has that changed over time?

Since 1994 we have always put a minimum of 15% in retirement and we always ensure we have a 1-year emergency fund in place.

We have had years where we have put 32% of our gross income in retirement, cash accounts or company stock as our income has gone up much faster than our expenses.

What’s your best tip for saving (accumulating) money?

You must put 15% away for retirement first then you budget from there.

We do not have debt, and to me house is only acceptable debt.

I do think however if you are putting 15% in retirement, and you have fully funded emergency fund vehicle debt is acceptable to me, but I do not have any and never plan to.

What’s your best tip for spending less money?

Budget or tracking expenses.

If you do not know where it is going how can you ever spend less?

What is your favorite thing to spend money on/your secret splurge?

No secrets, we plan every expense and we do not make a purchase of more than $100 without discussion with each other.

We know when we will need to purchase next vehicle and have plans in place for things like AC/Furnace, Roof, Water Heater.

If we decide we want something, TV, new phones, etc. we plan for those expenses as needed.

INVEST

What is your investment philosophy/plan?

I like what Warren Buffett says, put money in index funds, they are the best for the average investor.

I like Dave Ramsey’s 25/25/25/25 plan also, both are proven to work.

I do not trade individual stocks, but I do have company stock because it is part of my bonus structure.

My returns since 1994 have average 9.2% and all I need in retirement is to get an average return of 4.25% and I will never run out of money.

What has been your best investment?

Turned out to be my company stock.

In 2021 it made it to over $200 and most of the shares I owned were awarded at $90 or less.

Also investment in ourselves with continuous education either through our employers or even paid for on our own.

What has been your worst investment?

I bought Starbucks stock, held it for two years and it showed almost no growth during that time.

What’s been your overall return?

8.2%

How often do you monitor/review your portfolio?

Once a month and that is my recommendation for anyone.

The trigger for me is the first Monday after I get paid, paid once a month.

I do an update on all our holdings and I chart that information on a monthly basis.

By having this information and tracking as we have done, we know that our projected rate of return in retirement is safe.

NET WORTH

How did you accumulate your net worth?

When I reached age 52, we had secured our fist million.

We did this through working hard, having a financial plan and tracking expenses. It is all about goal setting and tracking to those goals and that is exactly what we did.

You know what, it was hard. None of this is easy and that is why I think people often give up or just fly by the seat of their pants.

One of the big keys was once we did not worry about money anymore then our lives opened in so many ways as did our careers and that is the big key to all of this, take control so it does not control you.

We inherited about $35k but not all at once and at some point later on we are likely to see another $40k which we will just give to our nieces and nephews.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

I told two young men I played golf with one day, who just graduated college, had their first jobs so they were just starting out.

I said to them, guys, I do not give advice, but I will tell you the most important thing about finances is “compound interest” so invest first then do everything else.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

When my wife decided she wanted to finish her degree we had to press pause on a few things.

Before that pause those we laid some ground rules, and one was we had to save enough money to pay for her school with no loans and where she did not have to work.

She was an hourly employee at the time and had access to unlimited overtime and she worked her tail off for a year and we saved enough for her to finish school debt free and not have to work.

What are you currently doing to maintain/grow your net worth?

I would not say I have my investments on auto pilot, but I am happy with my mix, and I will just adjust as needed as we go.

We are looking at turning some portion of our retirement money over to be professional managed at some point.

Do you have a target net worth you are trying to attain?

With pension numbers and my other investments, including cash and house we are at roughly 2.7 million.

With retirement on the horizon that will deplete versus grow but there is still growth planned and we will leave behind legacy money.

How old were you when you made your first million and have you had any significant behavior shifts since then?

52 and I would say I have more confidence than I have ever had and that continues to grow.

What money mistakes have you made along the way that others can learn from?

There is not a get rich quick scheme. Sure some people do that but in general slow and steady wins the race.

I chased a few individual stocks along the way and mostly made some money off of them, but I would have been just as good leaving that money in my index funds or mutual funds.

My biggest mistake was not starting to understand or invest until I was age 30.

What advice do you have for ESI Money readers on how to become wealthy?

You cannot “wish” your way to wealth, it is hard work to get there.

As Dave Ramsey says, “Live like no one else so later you can live and give like no one else” and that is a great philosophy. You have to go against the grain and not be “normal”. Don’t be intimidated by what other people say or do about money, stick to your plan.

I will use my sister-in-law and brother-in-laws as examples. They made fun of us for a long time because we lived off a budget, but I can tell you they are not making fun of us now because they realize they are going to be working until they die, no retirement in sight.

FUTURE

What are your plans for the future regarding lifestyle?

Well, I am retiring at 58, my wife is 53. She is taking a year off then going to work 6 or 7 more years.

I plan to do some part time work, like at a golf course for the next 7 years and then when I am 65 and she is 60 we will be fully retired.

We have already purchased our retirement home and we bought it for $70k less than the proceeds of our other house and we spent about half that money to make it the way we want it.

What are your retirement plans?

We will be playing a lot of golf, exercise, attend concerts, plays, sporting events and travel.

We are going to spend time in England, Ireland, Scotland and Wales and we plan to visit continental Europe making our way through France, Spain, Portugal and Italy. We will do an Asia trip and we will also visit South America.

We also plan to spend January on the Southern coast of the US every year.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

Healthcare is always a concern, so we are over budgeted in that area based on what the experts say. Outside of that no major concerns.

You better have a plan for long-term care.

We have chosen to budget for assisted living for both of us and we have researched the cost and estimated how much it will be for us when we get there.

We have opted not to purchase long term care insurance.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

I always had part time jobs, starting at age 13 so I understood money but basically what I understood was to spend it you have to make it.

I really did not learn about saving until I was in the military, and I become a good saver but did not understand investing.

At age 30 is when it clicked for me.

Who inspired you to excel in life? Who are your heroes?

Both sets of my grandparents, born in between 1912 and 1917. Both enjoyed very nice retirements and they were nothing but just working people who scraped and scrapped along the way, and they were inspiring to me.

I worked at a hotel my junior and senior year of high school, and it was a place where a lot was going on. I learned a lot from people who worked there and people who came there, it was really cool because I always listened to things they had to say about life and allot of it I did not understand but it is amazing now how many things they said that I understand now are so true, those people are heroes to me. Several of my school teachers also, they took time to teach me about life not just academics.

I learned a lot from my parents of what not to do but my mom in the end did end up having a nice retirement but she worked until she was 75.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

I am a magazine and sports column reader in general.

I did read the Millionaire Next Door, One up on Wall Street and Dave Ramsey’s Financial Peace and all three help us in our journey.

I still listen to Dave’s radio program.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

Yes, we do. We believe that that this money comes back to us over time.

We are not stuck on a percentage, we just give when we can, or if we get “extra” money.

We also do things like the month of December we tip our servers the cost of the meal in cash when we go out to eat. We also do things for our dry cleaner, the local police and fire at Christmas, the people who directly or indirectly take care of us.

We also are very generous with our nieces and nephews for birthdays and Christmas, and we also take them shopping when the visit for clothes, shoes, etc.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

We are going to set up a trust and the plan right now is it will be to take care a cemetery and also to put flowers on the gravesites of our parents and some other family members at other sites.

We also plan to leave half of our assets to be split up by nieces and nephews.

This interview has an update which you can read at Millionaire Interview Update 70.

Well done and congrats on your upcoming retirement! I completely agree with you that it’s easy for others to say you got this far because you don’t have children. We do not have children either, but regardless as you mentioned, it still takes a great amount of discipline to continue to save/invest and not inflate your lifestyle. Wishing you all the best!

Thank you! Best of luck to you also.

We have three kids and were a single income family. But your story is much like ours. Kids/no kids what works is the same. I agree on married finances, my wife and I own everything jointly. It’s our 44 th anniversary today! You’ve done great, thanks for your service, and I mean that. My dad lost some body parts in WW2 so I take military service seriously. You’ve helped keep world peace, such as it is, for one of the longest periods in human history. Way to go! You have a bright future.

Steve-O, happy anniversary to you and your bride!

Thank you and salute to your dad! Congrats on 44 years.