Today I have three updates for you from previous millionaire interviews.

Today I have three updates for you from previous millionaire interviews.

I’m letting three years pass from the initial interviews to the updates, so if you’ve been interviewed, I’ll be in touch. 😉

These updates were submitted in June.

As usual, my questions are in bold italics and their responses follow…

OVERVIEW

How old are you?

I will turn 55 years old this summer.

My wife will turn 54 this summer.

We will be married 25 years in October.

Do you have kids?

Yes. We have a 21 year old daughter.

She will be a Senior in college this year. She is majoring in Nursing.

After she graduates, she plans to work in ICU or Critical Care for a period of time and then go to school to become a CRNA.

What area of the country do you live in (and urban or rural)?

We live in rural Northeastern part of the country.

What was your original Millionaire Interview on ESI Money?

I was Millionaire Interview 38.

Is there anything else we should know about you?

I have continued to be a 50% owner of my business and my wife is still teaching high school Calculus.

NET WORTH

What is your current net worth and how is that different than your original interview?

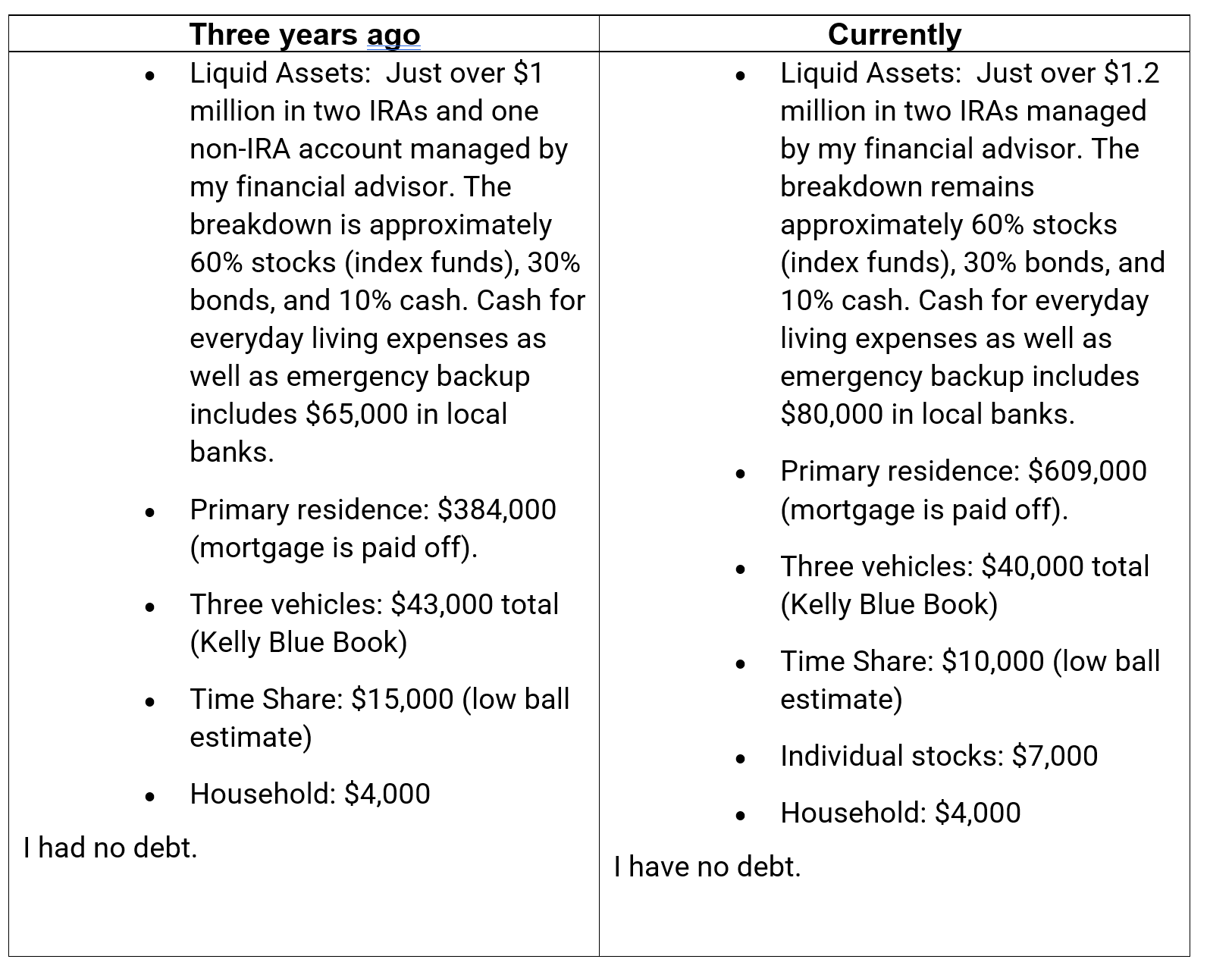

Our current net worth is now $6.5M.

When we did the interview three years ago, it was $4.5M.

We have been blessed to have our net worth grow by $2M in the last few years.

What happened along the way to make these changes?

We have continued to stay the course.

Even when the market has been volatile, we have stayed the course and continued to save and invest.

What are you currently doing to maintain/grow your net worth?

See above. Stay the course.

I am a proponent of being persistent and consistent.

Have a goal(s), make a strategic gameplan, stay committed and focused, execute said gameplan.

Don’t be distracted by elevator music, talking heads, or negativity.

Believe in yourself and your goals.

When things get rocky or volatile, that’s when you have to be more focused, disciplined and have faith in what you want to accomplish.

Never take your eye off the prize.

EARN

What is your job?

I am a 50% owner (CFO) of a small Company that deals with building controls/HVAC.

What is your annual income?

$143,000.

My wife earns $90,000.

How has this changed since your last interview?

My income has increased slightly from my last interview.

The company has had some better years and we have been able to increase our compensation.

My wife, not so much. Her contract has had minimal increases the last few years.

Have you added, grown, or lost any additional sources of income besides your career?

Both of us do a few side hustle jobs on the side, but nothing worth mentioning.

I do some personal taxes on the side and she teaches some cycling classes at a local gym.

SAVE

What is your annual spending and how has it changed since your interview?

Our annual spending has remained consistent.

I track this yearly and in the past five years we consistently spend between $80-89K per year.

What happened along the way to make these changes?

We live below our means. We certainly do NOT live like millionaires nor do we act like it.

It has been our mindset and lifestyle since we were married almost 25 years ago. We stay debt free and continue to invest at an aggressive pace.

INVEST

What are your current investments and how have they changed over the years?

My current investments are the same as they have always been.

The bulk of my investments are with Vanguard. I have some investments with Janney.

The rest is in individual stocks, 401K, IRA’s, 403B and cash in the bank.

Broken down as follows:

- $557K in cash (checking, savings)

- $14K in individual stocks

- $540K in 401K

- $492K in 403B

- $895K in IRA’s

- $4.029M in mutual funds

What happened along the way to make these changes?

Same as before. We have done nothing different.

We have remained consistent, disciplined and stayed the course.

We have continued to invest in the same funds.

We don’t take chances with our money and we only invest in things we are familiar with.

What are your plans for the future?

I am going to retire at age 59. We have already laid out our succession plan at the company.

My wife is taking it year to year. She will probably retire before I do, but we are not sure when that will be.

Health insurance remains our concern in retirement.

Given that you have a bit more wisdom and experience, what advice do you have these days for ESI Money readers?

Pretty much the same advice I gave in my first interview.

Old fashion hard work never goes out of style.

Educate yourself. Knowledge is power – the more you know….I preach this to my daughter constantly.

Pick your course and stay with it.

If you decide to get married, pick a partner with the same financial mindset and discipline as you.

Stay out of debt. Debt is your worst enemy. You can never truly be financially independent if you have debt hanging over you.

——————————————

OVERVIEW

How old are you?

I am a 71-year-old widower.

I was married for 41 years.

Do you have kids?

I have one daughter.

She is 42 years old, and lives in the Midwest.

What area of the country do you live in (and urban or rural)?

I live in a suburban area of a large city in the southwestern United States.

What was your original Millionaire Interview on ESI Money?

My original Millionaire Interview was #45 and was conducted three years ago.

Is there anything else we should know about you?

I also submitted Retirement Interview #9.

NET WORTH

What is your current net worth and how is that different than your original interview?

- Current net worth: $1.96M

- Previous net worth: $1.5M

What happened along the way to make these changes?

As indicated in my initial interview, I’ve been retired from my 9-to-5 job since 2015.

The basic positive changes from my initial interview of three years ago are primarily related to gains in the stock market, the increasing value of my residential property, my saving of additional funds, and increases in my income as I was asked to expand my online teaching to include the development of new courses.

I have also been spending quite a bit more during the past few years, primarily due to my efforts to maintain and improve my house. I currently have no plans to sell, but the house is now over 40 years of age and maintenance is getting more expensive. In addition, I am also involved in minor improvements.

What are you currently doing to maintain/grow your net worth?

I am satisfied with the growth of my net worth over the past three years. The gains have far outpaced the expenditures.

Going forward, my plans are to continue making minor adjustments in my investments, to continue the same amount of teaching that I have done in the past, and to maintain or slightly reduce my current spending patterns.

In addition to the teaching, I have one final course to develop, and that will probably be the end of the availability of course development assignments.

EARN

What is your job?

As mentioned, I retired from my regular job in 2015.

However, since 1998, I have been continuously involved in a side hustle that produced significant income for my family.

I have been teaching a variety of subjects online for 23 years. When I decided to retire from my regular job in 2015, I figured I would simply focus on part-time teaching online. Although I didn’t need the money, I definitely needed activities in retirement.

I originally thought I would simply do it until I was 70 years of age, but I enjoy it so much that I have continued. This type of work is an excellent side hustle as it can be done during spare time at home, or virtually from anywhere.

What is your annual income?

My annual income is comprised of three sources:

- My Social Security, which is $35,375 per year

- My income from teaching which ranges between $14,000 and approximately $20,000 per year

- A specific dollar amount ($22,200) that I arranged to be distributed from my individual retirement accounts.

How has this changed since your last interview?

This has changed somewhat from my last interview, as initially I was receiving approximately $33,000 from Social Security. In addition, my income from teaching was usually only $10-$12,000 per year.

As mentioned, during the last three years, the college where I teach had asked me to develop several new courses. I’m currently working on the fourth new course, and this activity has been conducted in addition to my normal teaching load.

Regarding the amount that I have distributed from my IRAs, I decided early on that I only needed $1,850 per month and I probably would not have to increase that annually in the foreseeable future. That has been the case.

Have you added, grown, or lost any additional sources of income besides your career?

There have been no additional sources of income, but the Social Security and teaching income has grown.

I estimate that the teaching has produced approximately $700,000 since it began in 1998.

SAVE

What is your annual spending and how has it changed since your interview?

My annual spending is approximately $68,000 per year. This is quite an increase from my original interview.

My spending in a typical month is as follows:

- Home and utilities: $1,585

- Transportation: $106

- Groceries: $400

- Health: $230

- Insurance: $545

- Restaurants: $475

- Shopping/Entertainment: $325

- Cash/Checks: $100

- Finance: $1,815

- Uncategorized: 130

What happened along the way to make these changes?

In the past three years, I have initiated additional payments to establish monthly maintenance activities for my yard and pool. In addition, there have been relatively high replacement costs for the home air conditioning unit, the pool pump and ancillary equipment, and a number of other items.

I also own three vehicles, and there have been several high repair bills during the past year.

On the positive side, my overall income has increased to the point where I continue to make quite a bit more than I spend. This is due to the increase in income from teaching, cost of living increases in Social Security, and the fact that the stock market has done so well.

INVEST

What are your current investments and how have they changed over the years?

All of my retirement investments are in the stock market.

When I retired six years ago, my 401(k) was rolled over into qualified IRAs. Since I was dealing entirely with retirement savings, the focus was on preservation with growth.

I am currently invested in Mutual Funds, ETPs, and Closed-End Funds (~97%), and in Cash and Cash Equivalents (~3%).

The portfolio includes:

- US Bal/Asset Alloc (11.14%)

- Int Long Hi Qual US Bond (9.17%)

- Large US Gro Eq (11.34%)

- Mid Cap US Val Eq (3.36%)

- Strategic Income (8.48%)

- Ultrashort Bond (3.41%)

- Cash and Cash Equiv (3.32%)

- Large US Bl Eq (33.74%)

- Mid Cap US Bl Eq (4.76%)

- Sector (2.48%)

- Short Int Hi Qual US Bond (8.8%)

Prior to retiring, the 401(k)s held by myself and my wife were both successful, however, they of course were limited by the stocks and bonds offered by the companies managing the 401(k)s. The changes that occurred at retirement, therefore, included expanded investment options.

This is the primary reason for my changes in investments over the years.

What happened along the way to make these changes?

For the most part, the nature of the portfolio has stayed the course.

During a few periods of volatility, minor buying and selling occurred with less risk. However, I have not been interested in much change, as I am in this for the long term.

MISCELLANEOUS

What other financial challenges or opportunities have you faced since your last interview?

In regard to opportunities, I accepted offers of developing three new courses at the college where I teach. However, I also became busier with family obligations and other activities, and I did turn down one course development opportunity.

The challenges that were presented included the aforementioned home maintenance and improvement, as well as automobile repairs. Everything was inevitable due to the passage of time and caused little concern, as I am still making more than I am spending.

Overall, what’s better and what’s worse since your last interview?

It’s been a very interesting three-year period. Improvements include major gains in the stock market, the value of my home, and higher amounts of income and Social Security.

If I had to choose something that was worse, it would be that I’m spending quite a bit more money. I still have the highest confidence in my future financial situation, however, as the retirement funds that are being distributed to me are still only $1,850 per month. This is approximately 1.8% of my retirement funds.

What are your plans for the future?

My primary plan for the future is to resume visits with my daughter, son-in-law and grandkids. We’re separated by several thousand miles, so it has been a very long time since I’ve seen them. As one of my most important bucket list goals was to spend as much time as possible with them, I’m certainly glad now that the pandemic restrictions have eased.

I also intend to continue teaching online for the foreseeable future, because it is a positive activity that keeps me focused. In addition, I will also continue to follow my stock portfolio at least weekly, exercise regularly by hiking and bike riding, continue to write, and continue my newfound hobby of photography, and plan other day trips to interesting destinations.

Given that you have a bit more wisdom and experience, what advice do you have these days for ESI Money readers?

One primary recommendation that I would have to make is for readers to evaluate their talents and expertise and work on establishing several different sources of income. I started my side hustle around 23 years ago, and I have never regretted it. If you can have a second job of any type, try to focus on minimizing the impact on your family.

Experience has shown me that once a person is interested in having a side hustle, he or she should continually evaluate any related opportunities. For example, one could offer services as a consultant, and when new technologies or other opportunities become apparent, one can often easily segue into new offerings. The trick is being able to identify needs that are not being met. When you can find these types of opportunities, then the fun starts.

The other two recommendations I would make would include minimizing or avoiding debt completely and taking advantage of 401(k)s if you possibly can. If 401(k)s are not available at the place where you work, it is essential to begin your own retirement funding.

Every day, we are all hit with an incredible number of advertisements. When it comes to major purchases, it is necessary to sit down with your significant other and draw up your own plan regarding what you really need and what you really want. Remember that everybody is selling something, and that we just need to determine whether we need it, want it, or that we simply can do without it.

As we all know, each family is remarkably different in their spending habits. The concept of “habits” is a fascinating subject. In our retirement planning, we need to look at the difference between obtaining goods and services now or having the mindset of accepting delayed gratification. “Do we really need that new car now, or can we get a few more years out of our Grand Turismo Hooptie?” We should include these discussions in our family meetings.

——————————————

OVERVIEW

How old are you?

41 now.

Wife almost 37.

Married 6 years.

Do you have kids?

1 year old kid now.

She already has ~22k in a 529k and $5k in a ROTH IRA.

We are planning on having one more kid.

What area of the country do you live in (and urban or rural)?

Suburbia.

What was your original Millionaire Interview on ESI Money?

NET WORTH

What is your current net worth and how is that different than your original interview?

Previous ~4.4 million.

Now ~7.0 million.

Breakdown is:

- 350k individual picked stocks

- 100k crypto

- 2.12 million in after tax funds

- 470k in simple IRAs

- Main house: 1 million

- Rental house: 1 million

- Beach house: 500k

- Cash in bank: 500k

- Business value: 1 million

What happened along the way to make these changes?

These gains occurred because of continued and prolonged investments into a well diversified portfolio of 85/15.

During the start of covid, after tax account dropped under 1 million. I wasn’t scared and invested as much as I could (a little cautious as there was no reference point for a pandemic). I bought the dip and the dip ramped me up from <1 to 2+ million within 1 year.

In the meantime, I also gambled with individual equities and hit a home run with TSLA. I also bought ~100k of crytpo which has been up and down. Bitcoin is a long term hold for me and I won’t worry about it until 10 years from now where I hope it will pad retirement by 500k-1 million per bitcoin.

I live in a city with massive appreciation and my main house has gone up 2+x. My rehabbed rental has 2x+ also. My beach house has 2x. I maintain rental income from rental house + beach house. Beach house is almost completely paid off and main house is next. Rental is 1/2 paid off.

I will cash out the rehabbed rental in 7-10 years to buy my wife a dream house if she wants. I expect it to run 1.2-1.5 million based on developments occurring 2 blocks away.

My original plan for this house was to flip, but I couldn’t get the price I wanted. I had a bad contractor and have fixed and replaced almost all the work done by them in the subsequent years so it’s been more of a loss (but offset by tax advantages). With appreciation, it will be a large gain once I sell.

What are you currently doing to maintain/grow your net worth?

Continue to pump in money into properly allocated portfolio. I have enough fun money in my individual stocks account and reached my goal of crypto. I allocated approx 5% into it as a hedge bet so I will not put in more.

I plan to retire at age 48 or massively cut back and/or do an entirely new field of work for fun/challenge.

Compounding growth works. Took me 8 years for first million saved. 2nd took 3 and I think 3rd took 2.

EARN

What is your job?

Medical profession/practitioner and educator.

What is your annual income?

My first interview was 471k. It jumped to 865 in 2019k. Due to covid shutdowns, it dropped back to 665k in 2020.

I NEVER EVER IN MY LIFE imagined that I would make 865k.

How has this changed since your last interview?

I am just more experienced and even better at my job.

My reputation has grown for my work.

Have you added, grown, or lost any additional sources of income besides your career?

As mentioned, I had a bad experience with my rehabbed rental and would have considered it a loss, but I got lucky with appreciation since the last interview.

Since then, I have added small amounts of commissioned incomes from affiliate programs within my profession.

SAVE

What is your annual spending and how has it changed since your interview?

Personally my expenses have dropped to very little. I buy nothing for myself now. I have too many material things and after a decade of accumulating things when I was younger, I just don’t care now.

I still have 2 European cars for myself and will continue to do so, but pretty much other purchases have dropped to 0.

I do still want a Patek Aquanaut though. 🙂

My wife spends most of the money and my personal allocation goes to my daughter now for savings and in the future, private school.

What happened along the way to make these changes?

Everyone is correct: kids are EXPENSIVE, but worth it!

As I said, I just don’t need material things too much now. I’d rather travel, fish or have fun with my friends/family.

INVEST

What are your current investments and how have they changed over the years?

Listed above. I will continue to grow my after tax dollars.

My flat fee financial advisor’s calculations says that I will have about 8 million NW by retirement time. I think that is wrong as I am about at 6 million.

My goal is 5 million minimum in liquid assets to retire. I think I will likely have 6+.

A 3% or 4% withdrawal rate at that time + any job and there is plenty to retire.

What happened along the way to make these changes?

Don’t be a fool and keep investing.

If you have funds, buy more when there are dips.

IMO it is not market timing if you still meet your minimum desired savings per month. It’s a bonus.

I am for at least 10k savings a month with after tax dollars. Pre tax, I think it is an additional 4.

MISCELLANEOUS

What other financial challenges or opportunities have you faced since your last interview?

Babies are expensive! Fertility treatments are expensive. I think I have spent 80k on them.

Could have bought myself a used AMG wagon.

Overall, what’s better and what’s worse since your last interview?

Personal life is better because we have a kid. I never thought that I would like being a dad as much as I do. I was opposed to things like private school, but now see value in them (plus the local district teaches common core math which I do not want my kid to learn; I want classical education).

I am earning more income than I ever imagined. The only person that really knows how much I have is my best friend. No one really knows how much I make and I’m cool with that. If my wife ever wants to know, I will tell her, but it works for us how we divvy up finances (no joint accounts and she has a nice monthly budget).

I want to retire young so that I can have more time/location independence and take my kid or kids to Europe for a month if I want to. I don’t mind working as long as I have a remote job.

What are your plans for the future?

To work towards retirement. I have personally conquered my profession in what I planned to do so I want to retire.

I say that now, but at that time my kid will be 7-8 years old. I may re-evaluate and perhaps just work a lot less and hire someone in to do my work.

Or I may quit completely and find a different career to work.

Given that you have a bit more wisdom and experience, what advice do you have these days for ESI Money readers?

Keep saving. Aim to save a certain amount even if it seems lofty and work towards it.

When I was young, I aimed for 10k a month savings, which seemed ridiculously absurd. But I worked at it and now it’s just an easy bill.

Beyond that, keep in mind that divorce is expensive and will delay your retirement. I say that b/c I have seen some friends with some terrible divorces where all parties lost. Put energy into your marriage.

Also don’t be afraid to hedge bet 1-3% into crypto; bitcoin isn’t going away anytime. Market cap is 1 trillion already. No way 1 trillion is going away.

“Market cap is 1 trillion already. No way 1 trillion is going away.” Uhh, in the dot com crash of 2000, over 1.7 trillion vanished almost overnight, and that’s not even adjusted for inflation. That was over 20 years ago, so it would be well over 2 trillion in todays dollars. Crypto is numbers in a computer somewhere with no intrinsic value. In my opinion, most or all of it could be determined worthless very quickly. It’s not for me. For me, for something to be an “investment,” it has to have something of fundamental underlying value. A business with revenue and profits that have been showing good growth for the last 20 years straight would be a good example.

There are limitless discussion about value and bitcoin worth. I’m not here to discuss or argue that. You are welcome to have your opinion and mine. For me, it is a hedge bet.

If my crypto and btc goes to 0, that sucks. But you know what, it has really very minimal to no impact on my retirement as my other investments are growing significantly.

The other spectrum has to do with the potential growth. We will know in 5-10 years and at that time, I am betting that btc is 500k to 1 million a coin. If so, then I am padding my retirement by quite a bit. If not, again, I am still retiring at likely age 48 with likely >6 million in liquid assets not counting real estate. If the stars align, I can retire at 48 with 8+ million.

At 4% withdrawal rate, I never have to work again. But I prob will do 1 day a week work in my profession somehow as long as it is a remote job.

Millionaire 58,

Your best friend knows your net worth and not your wife? No joint accounts and an allowance? Not really understanding why she is not asking. I know I am not your wife, but as a woman, wife and equal partner to my husband, boy does this rub me the wrong way. Hope it continues to work for you and that you will do the right thing and take care of your wife if for some reason your marriage dissolves in the future.

Im so grateful for your comment. I am a wife, married (25 years) to a man who refuses to share any financial information with me. He also does not share any money with me either. I bring in my own income and I struggle. He lets me pay for most things. He never helps me with anything financially related. When he does pay for things that we both use or need like the mortgage or food, he makes all the dicisions about those things. I have no idea what our retirement looks like because Im kept in the dark about things of that nature. I need to get a divorce. Its time!

This is not the proper forum for this type of discussion, but I feel I just need to respond. Wife in the Dark, my heart aches for your situation. Please seek the advice of a good divorce attorney who has access to a good forensic accountant before you confront your husband and take any other action. Your situation borders on abuse. Also, if financially feasible for you, start funding your own retirement.

I agree it’s time for a divorce. One recommendation that I have is to not only hire an attorney but also hire a Forensic Accountant. This will mitigate your soon to be ex hiding money and assets from you! This is extremely important as it’s easy to hide it in a relative’s name. A good friend of mine took this extra step and it prevented the ex from hiding over $1.4 million!

This is a very hard situation. I have lived it and am now living it post-divorce and now he’s passed away as of last June. When I asked, he wouldn’t tell me anything. Granted, I waited too long to ask. My attorney found he was trying to hide his pension during the divorce. Now we were very young during our divorce proceedings, but please take care of yourself during this process. I am a low-income earner, so no one understands why I read these, but I paid off my last credit card last Monday after 10 years. That’s why. Everyone praises my determination. When you read these blogs, of course you’re determined for a better life for yourself. I’ve had help as well. That more or less is how long it’s been since our divorce minus some details. Please take care of yourself again. Divorce is hard.

Everyone has a different relationship.

My wife is terrible with money and admits. When we were serious in our relationship, she told me that I was to be in charge of money. She knows that I am very good with it. In actuality, part of the reason for no joint accounts is none of us wanted to go to the bank and make a new account.

Why would we need to? I pay every single bill from my personal account because it’s just easier. She has a credit card that is for family and every month, I just pay it from my personal account b/c it’s just faster than transferring money to a joint account, paying from a joint account after logging into it, etc. My account is essentially a joint account.

She has an allowance because there are no bills or any costs that she needs to contribute to. She’s a stay at home mom now and that’s what we both want and we’d have it no other way as raising our kids is the most important part of our calling. We BOTH settled on what was easiest and fair. I have an autopay from my personal account to her personal account that she’s had her whole life. Her “allowance” is pure discretionary income. She likes to buy $600 shoes. OK go ahead, I don’t care since it’s her budget.

Not every marriage needs pure equality in every instance including financials. My wife asks me sometimes what we’ve saved and I tell her, but she never asks more because I guess she doesn’t want or care to know.

BTW this is the way my parents did it and turns out, the way HER parents did it too. There is nothing malicious, condescending, etc of our financial relationship. It’s just works and is way easier.

Millionaire #45. I was stuck by how your liquid assets have not risen as much as expected (for a 60/30/10 portfolio even after accounting for the 22K annual withdrawal) given the stock market is up more than 50% over the last 3 years. It makes me wonder how much of your return is being consumed by high fee funds and financial advisor fees. Might be worth getting a second opinion from a flat fee advisor. A rising market can obscure the impact of fee drag but it is there during both good and bad times.

I agree with flat fee. Flat fee is much more beneficial. During COVID shutdown (last March), I dumped as much as I could into market and was rewarded with huge gains.

At one point my after tax account dropped from 1.5 to 900k. I dumped more in and in the past year, it has jumped to 2+ million with continued addition.

Hi Millionaire 58, thanks for sharing your situation with the readers. I alway appreciate the opportunity to learn from what fellow millionaires share in the stories. I have question about Roth IRA that your 1 year old daughter has. It is my understanding that Roth IRA contribution has to be from the account owner’s earned income. I am not sure how to get around that rule (Unless your child has earned income as baby model).

Yes, she has earned income from being a model in my work’s advertisements. I have ads and paid bills to pay if I am ever questioned and audited.

This is a large advantage of owning a business. You can use the business to fund legitimate expenses (versus simply paying taxes).

For her 529, I made sure that I funded during the lowest of the lows of covid shutdown and she’s had a 42% gain in the past year with Vanguard total stock/equities funds.

That’s awesome. Thanks for the reply.

58, I also took advantage of this with 6K Roth’s/year/employed child. While you can’t directly deduct Roth contributions, the corporation allows for employment of the children (which is an expense against the corporate earnings), and of course the compounding benefits of a Roth over many decades means the funds will grow tax free and ultimately be available tax free upon withdrawal for the recipient. Many also don’t know that the Roth contribution does not have to be directly funded by the recipient’s earnings – it can be funded by a parent, grandparent, friend, etc. so long as there is earned income against the contribution.

Now that my oldest is starting college, there is a tuition assistance benefit that your corporation can expense up to $5250/year/beneficiary that is not taxed to the employee as income. I’m doing this as well.

Corporations are probably the single best advantage that the wealthy use to their advantage for multiple reasons, which does include tax advantages. An employee earns an income, pays taxes on that income annually, and whatever is left over is what can be spent (that’s why employee paycheck always seem so small relative to expectations!). A business earns income, then spends first (expenses), and then is taxed last on what’s left over, so often a much lower effective tax rate relative to revenues (income).

Add in real estate benefits including tax depreciation and tax deferred appreciation, real estate professional status, 1031 exchanges, cost basis upon estate transfer and you can see how the wealthy use tax laws to get ahead.

Then of course long term capital gains tax rates in taxable accounts may be better than 401k/IRA accounts that are ultimately taxed at personal income tax rates (especially for those well in the top income bracket as I am) and usually limit what you can invest in.

I encourage financial literacy in the areas of business ownership, real estate ownership, stock market capital gains benefits to anyone who asks me about how I do it.

To millionaire interview #58,

I’m with you on the Patek Auquanaut. I’ve been on my local authorized Patek dealer’s waiting list for two years. I bet I never get the phone call…🙁

I was in London 2 years ago. Went to Patek store and was ready to buy it for 15000 euros. But it was sold out everywhere!

I’ll have to buy it sometime. At the latest, I will reward myself with it for retirement. Hopefully earlier 🙂

Millionaire #38,

Congrats on your investment achievements. One question I had was regarding your concern with healthcare costs in retirement. While these costs are always a concern, I would think with your net worth it wouldn’t be a huge concern. The reason I ask is I am contemplating early retirement in a year or so with around 4.5 million in investments at age 57. My analysis says I should be fine with buying private health care coverage (family coverage) to bridge the gap until Medicare. Just wanting to see if I am not seeing this clearly. Thanks

Hi! Congratulations on your financial successes and early retirement! No, I don’t think you are missing anything with regard to health insurance. This has always been a personal wildcard with me since I see yearly how much the premiums increase. Our healthcare costs to insure our employees is outrageous. We will probably be okay, but it’s the one cost we can’t seem to get comfortable with. Thanks for the message.