Have you ever received a solicitation in the mail to attend a “retirement seminar”?

Have you ever received a solicitation in the mail to attend a “retirement seminar”?

We get them ALL THE TIME! They look like the sleaziest things you can imagine (if you read between the lines) — post cards offering a free meal at a local restaurant in exchange for hearing a presentation about a given retirement topic.

Most of them look like they are trying to sell either insurance or annuities, but I can’t be 100% sure. I believe they don’t want to be completely open about their intentions (I’m guessing that would put a damper on response rates), so they keep things kind of vague (similar to the ways a timeshare company operates).

But I’ve been curious about what these are really like so I’ve kept my eyes open for the right opportunity. I wanted to find one with a convenient time and location so I could attend and see for myself. Plus I figured no matter what happened it would make for a good blog post. 😉

After waiting for the right opportunity, we finally got a great option in October. This post will tell you what the offer was, give details of the event, share what we thought of it, and so forth, giving you a glimpse into what these sorts of events are about.

A couple notes before we get started:

- I’m going to break the review into two posts. This one will deal with the process of them soliciting us, us accepting, our attendance, and what they had to say about personal finances in a Q&A session at the end. The second will center on “how to have a great retirement”, the main idea of the presentation portion.

- You’re going to be surprised at my conclusions. I went in with one expectation and came away with a completely different outlook.

With that said, let’s get started…

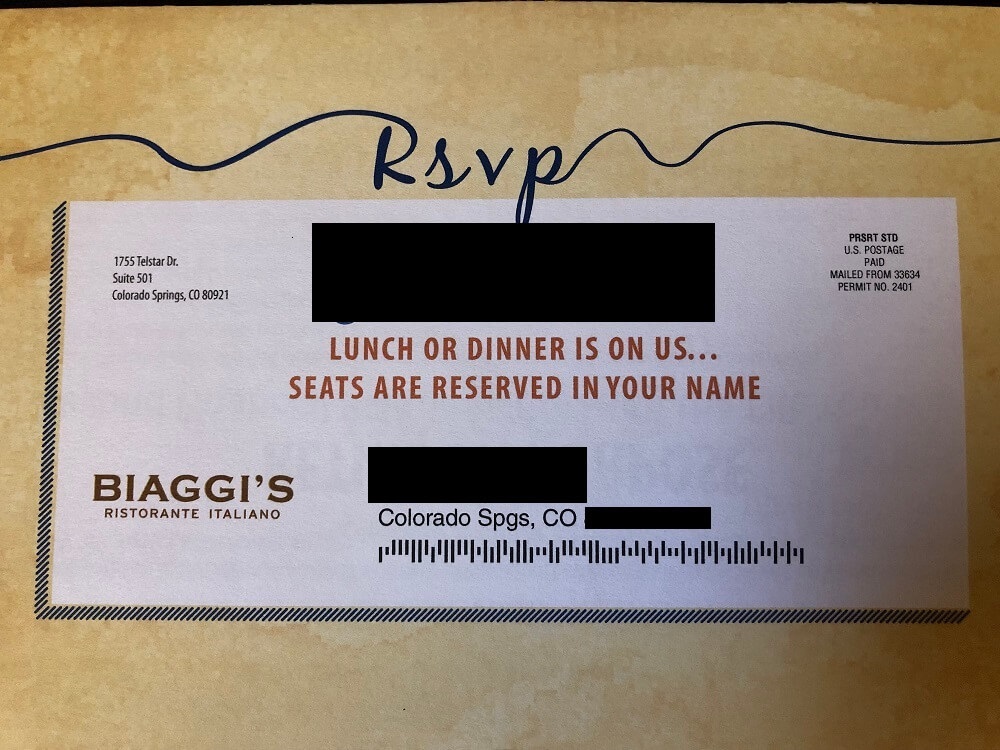

Retirement Seminar Mail Solicitation

As I said, we get offers to attend one retirement seminar or another almost every week. These come in the form of postcards sent to us via mail.

In early October we received one such piece and it looked like this:

Here’s the mailer we received. It was a tri-fold letter/postcard.

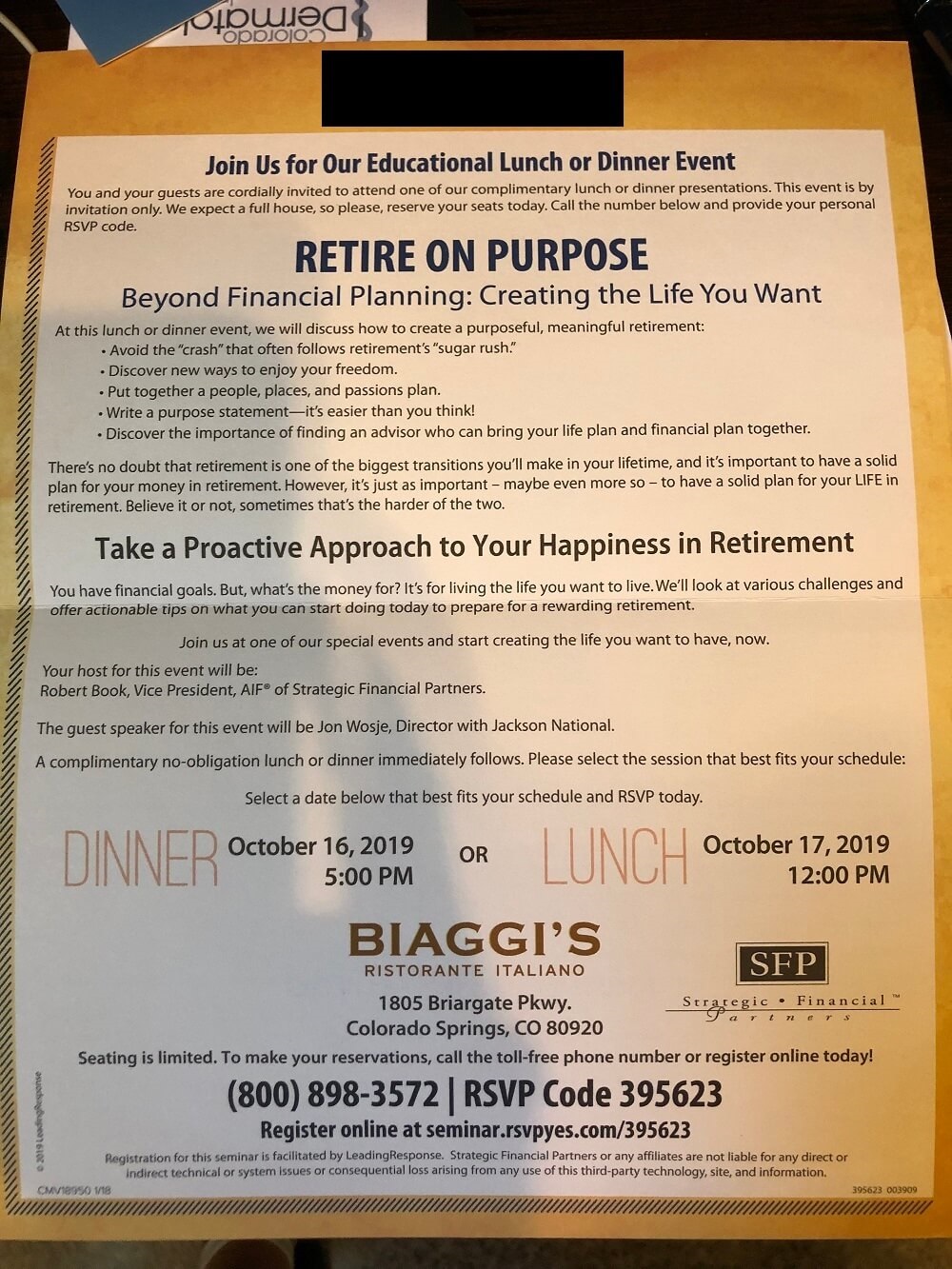

This is what was inside the tri-fold…

Here are our “tickets” — which we did not need. I suppose they are designed to make the event look more formal.

There were a few things that made this offer stand out from the others:

- It was at a restaurant we had been wanting to try — an upscale Italian place (I’d been there once before but my wife hadn’t).

- It was near our house. Very convenient.

- It offered a lunch option. Dinner is usually too late for us as we eat around 5 pm.

- The seminar looked at least somewhat interesting. I suspected there was going to be a sales pitch of some sort, but at least the presentation appeared to offer some value compared to “Learn How Annuities are Vital for Your Retirement”, which is the sort of offer we usually get.

I asked my wife and she was up for attending. So we selected the lunch option on Thursday, October 17.

I registered us online and received an email confirmation.

This was roughly two weeks in advance of the event. Over the next couple weeks we got at least one more email as well as a phone call reminder of the event. I had selected the “minimal contact” option when I registered, so I didn’t get placed on some sort of list (that I know of).

Attending the Seminar

On the day of the event we arrived a bit early (they asked us to) and were escorted to a small room (actually the wine room) where they had a table and screen. Here’s a view of the set-up:

Decent room, huh?

Over the next 15 minutes or so 7 or 8 other people showed up (I think it was three couples and one single guy) in addition to us, so there were 9 or 10 total. They noted that the night before they had a much larger turnout in a much bigger room.

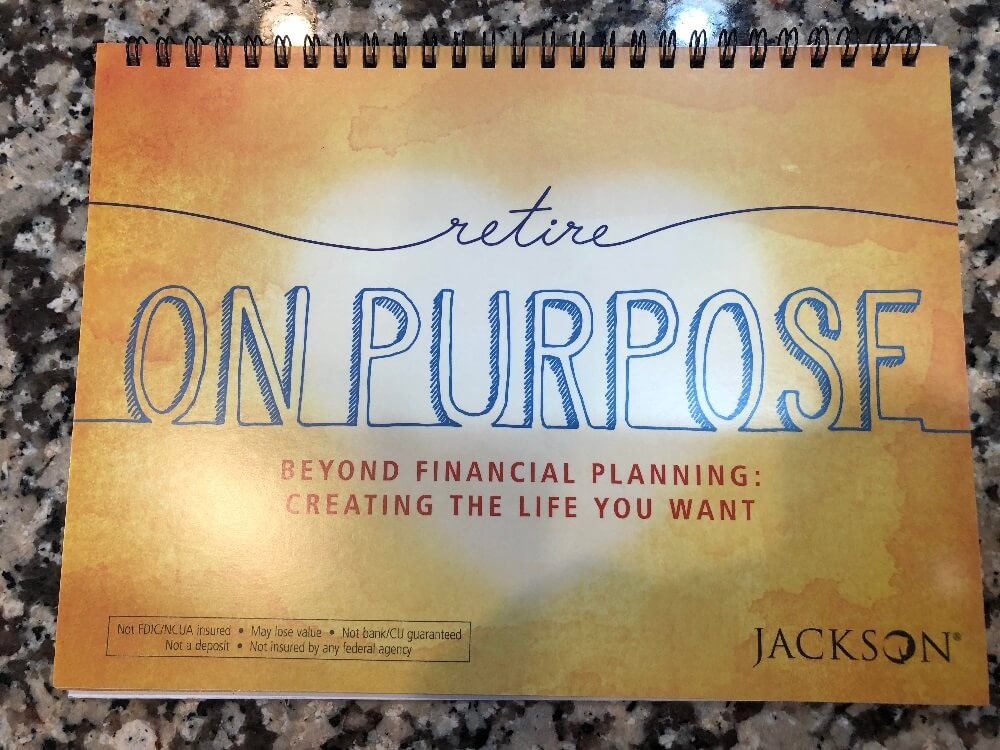

We sat around a bit and were served drinks and appetizers as well as placed our orders. I looked through the presentation materials which consisted of a spiral presentation:

I thought the presentation material was very well designed.

As well as this folder:

Professional presentation all the way around…

The folder had a workbook that went with the presentation plus a two-page survey about the seminar that we filled out at the end.

I read everything in between the time we got there and the time we ordered and had a good feel for it pretty quickly.

Once we had all ordered and started eating appetizers, the presentation began. A local financial planner got up, introduced himself, and welcomed us. He was the host and (I assume) the guy paying for the whole thing.

He introduced a man from Jackson National Life Insurance Company who would be our presenter. I’m not 100% sure what the relationship between these two was. My guesses are:

- The planner hired Jackson to do the presentation to help get clients.

- The planner does business with Jackson and as such Jackson offered the presentation as a way to get more clients.

Anyway, the presentation began and lasted about 30 minutes or so, during which time we got our food, started eating, and listened. I also took substantial notes and will cover the presentation in an upcoming post.

Just for reference, it centered on how to prepare for retirement from a non-financial standpoint. Basically how to not have a terrible retirement by thinking through issues and planning in advance.

End of Presentation Pitch and Questions

After the presentation was over, there wasn’t a pitch of any sort, which was a surprise to me.

The planner simply came up, said he hoped we enjoyed the presentation, asked us to fill out the survey (where we could leave our names and ask for a meeting if we wanted), and asked if anyone had any questions.

This is where the group opened up a bit, began to ask questions, and the planner responded.

I wrote down both the questions and responses and will share with you (along with my thoughts). Please realize these are paraphrased and summarized based on what I heard. I’m not attempting to create a transcript of exactly what was said as there’s no way I could have recorded it all.

Retirement Debt

Question: How important is it to go into retirement debt free?

Answer: It’s the most important thing. Retiring with no debt should be a primary objective.

My response: Can’t say I disagree, at least in principle. Having debt does make retirement harder. That said, I was surprised he said it should be a primary retirement objective. I would have had “having enough assets/income to cover retirement expenses” as the primary objective. Being debt free is a subset of that overall goal as it takes away a huge expense (your mortgage, which is usually the last debt to fall), thus making funding retirement much easier.

Long-Term Care

Question: What are your thoughts on long-term care insurance?

Answer: You may be self-insured if you have enough assets, but everyone else needs to consider how to address long-term care. The number one concern people have about retiring is running out of money — and having high long-term care costs is something that could significantly speed a person running out of money.

Not everyone needs long-term care insurance. We have four ways to address the issue so we tailor plans to a person’s specific situation.

But by age 50 you should at least be considering the issue and working on your plan for it.

There are some insurance policies that can also morph into LTC policies so those could be considered as well.

My response: I wish he had told us what the four ways of dealing with the issue were.

I haven’t spent enough time on this issue and need to think it through more. This was the first response that led me to consider setting up a meeting with this planner. More on that to come…

Taking Social Security

Question: When do you recommend taking Social Security?

Answer: How long do you plan to live? (Everyone laughed.)

The breakeven is roughly 80, so if you think you’ll live that long or longer, I’d recommend waiting until 70.

Even if you don’t think you’ll live that long, I would still recommend waiting at least until full retirement age (FRA) for almost everyone.

We look at models and advise people based on their needs. If they don’t need the income, then there’s usually no reason to take it early.

And, of course, there are many ways to take Social Security, especially if you’re married and both spouses have worked, so it can get complicated.

We have some clients who take it early because they think the system is broken and there will be changes that will lower their payouts. Our opinion is that there will probably be changes but they likely won’t hit most older adults as they’ll be left alone — the younger generation will get reduced benefits.

One exception could be means testing in which older, high-income adults do see their benefits reduced. So if you’re worried about this, you could justify taking it early.

My response: Here’s the second instance when I thought I might need to talk to this guy.

After thinking it over, my current plan is to have my wife take her Social Security when she turns 62. Then when I reach FRA (67), I’ll take my Social Security. She will be 70 and will convert to half of my benefit, which should be more.

But I need to chat with someone to be sure this is the best option for us.

Required Minimum Distributions

Question: How do you suggest thinking about required minimum distributions (RMDs) from IRAs?

Answer: Most people wait until the last possible moment to take RMDs because they assume their taxes will be lowest then. But we’re seeing many people have the same or higher tax rates at RMD time and thus being hit with large taxes since they have more to withdraw when they wait.

So we look at the person’s specific situation and oftentimes it’s best to withdraw earlier than the last minute to minimize taxes.

One way to avoid taxes is if you want to give you could send the RMD straight to a charity and thus have no tax liability.

My response: I assumed you could also send an RMD straight to a donor-advised fund and avoid taxes, which could have been a useable strategy for us.

But after checking into it, this is not allowed. Here are the details from Vanguard Charitable:

Up to $100,000 of your annual RMD from IRAs may be distributed directly to a 501(c)(3) public charity, enabling you to avoid paying income taxes on that amount. This option is known as a qualified charitable distribution (QCD).

The QCD applies to traditional, rollover and Roth IRAs. SEP and Simple IRAs also qualify (as long as you are no longer actively receiving employer contributions). Employer-sponsored plans do not allow for QCD treatment.

While we would love to offer our donors the ability to distribute their RMD tax-free to Vanguard Charitable, federal law does not allow donor-advised funds to accept QCDs. This is because the Pension Protection Act, which established QCDs in 2006, limited them to operating charities. For this reason, donor-advised funds, private non-operating foundations, and supporting organizations are ineligible to accept QCDs.

So we could give to a charity using our RMD, it would just need to be a gift straight to the organization, not through a DAF.

Reverse Mortgages

Question: What do you think about reverse mortgages?

Answer: They can work in limited situations but I generally do not recommend them. I’ve only had one client in 20 years use one.

I view reverse mortgages as a back-up to your back-up plan — only to be used if there are no other options.

Generally there are better options (like downsizing to a smaller house or even to a rental unit) than using a reverse mortgage.

My response: Yep. I can think of about 2,375 better options than taking a reverse mortgage.

And with that, he thanked us for coming and we left.

Overall Thoughts

That’s the blow-by-blow of what happened, but what did I think of it (FYI, I asked my wife to write down her thoughts too, but she’s too busy to write for such a small site as this — haha!)?

Here are my main takeaways:

1. It was much better than I thought it would be.

I had expected a sleezy sales pitch featuring annuities, whole life insurance, or some other combination of high-cost financial products from someone who knew less about financial planning than my cat.

But this was actually a worthwhile presentation, especially for those not yet retired. The meat of the time spent (the presentation on how to plan in advance for a useful retirement) was very good IMO and something 75%+ of potential retirees need help with. So there was really good value here.

In addition, the Q & A time was worthwhile and valuable as well. Though his answers were pretty superficial (they have to be when talking to a group since everyone’s situation is different), they still offered some good insights even for a more advanced retiree like me.

2. The planner represented himself well.

I’m not sure whether I’ll contact him or not, but his strong responses to the questions posed (plus the way he handled himself — professional but approachable) would certainly make me comfortable suggesting him to others who might ask me to recommend a local planner.

I wouldn’t be surprised to find out he picked up several clients between the dinner the night before and our lunch, making the event completely worth the cost to him.

3. The food was good but not worth a return visit.

We enjoyed our food, but it wasn’t anything we need to visit again. It was slightly above average and my guess is that the prices were steep.

But we got to try out a place we thought we might like and now we have (and can take it off our to-visit list).

Based on the successful outcome of this event, we’ve signed up for another one in November (which is about a week from when I’m writing this post). It’s at a very swanky restaurant so I’m going to have to get dressed up (a bummer), but we have wanted to try out the place but can’t see ourselves spending that kind of money on food. Now we don’t have to. 😉

Plus I’m kind of hoping it will be a train-wreck. It would make for such an interesting blog post.

Anyway, stay tuned…

Thanks so much for this. I always throw away those free meal / sales pitch invites so fast and never even consider going, maybe I will think more kindly of them. Past experience with free meals were never good….high pressure salesmen that won’t take a NO…they weren’t financial, it was time shares and fancy expensive fire alarms for your house. And, I didn’t get to order from the menu, it was a preselected generic meal.

Thank you, ESI! This is helpful. Looking forward to a post from you regarding Long Term Care: Buying insurance vs self insuring, how to prepare for when you and your wife can no longer manage your own finances, a plan to avoid scammers targeting elderly retirees, etc.

Regarding when each spouse should take Social Security, here is this calculator that was recommended elsewhere. I don’t know how accurate it is.

https://opensocialsecurity.com/

Question: I ran the social security calculator supplied above. I am 65 my husband will be 65 in February. (2020). Calculator indicates I should take it at 65 + 2 months (less than retirement age of 66), & my husband should take it at 70 + 3 months. We both work. I have a home based business and he works from home – traveling in spurts. We can retire but we are happy and making a decent income. IF we follow the calculator (I have not done more scenarios), my husband indicates we have income tax repercussions. Does anyone have thoughts on this? (Our financial adviser – whom I feel we should ditch – as he pushes packages with high commissions for himself – but has done very well for us), has always advised us to go with SS at 70 years each.

Hopefully one of our very intelligent and educated fellow readers can and will answer your question. I’m not qualified. I live in an old leaky barrel.

I am however more than qualified to suggest that you fire your financial advisor immediately. I’ll just leave this here:

“Act as if every broker, insurance salesman, mutual fund salesperson, and financial advisor you encounter is a hardened criminal, and stick to low-cost index funds, and you’ll do just fine.”

William J. Bernstein, “If You Can: How Millennials Can Get Rich Slowly” (FREE BOOK) – July 16, 2014

http://tuttle.merc.iastate.edu/Bernstein_If_You_Can.pdf

Since you did not provide your and your spouse’s PIA (primary insurance amount) from the calculator it is not possible to provide information specific to your situation.

However I can tell you 1 thing for sure and 1 thing that is a pretty safe bet.

1 thing for sure. It is always bad, wrong, mathematically challenged, & downright crazy to ever wait 1 day past age 70 to draw. Why? Because you get no increase in payments for waiting past age 70 so each month you wait is just that month’s money that you flushed down the toilet, with no increase to compensate for it in future payments. If this calculator actually suggested 70 years plus 3 months then its a bad calculator. I punched in some made up numbers that might mirror your situation and it suggested 65 + 9 months for you and 70 + 0 for your spouse. That makes a lot more sense.

1 fairly safe bet. If your spouse has a PIA that is at least double of yours and you expect at least 1 of you to live at least to life expectancy or beyond then it will usually maximize payments if you draw at FRA (full retirement age) and your spouse draws at 70, at which time you would then draw 50% of his PIA. It never makes sense for the person with a PIA of less than half the other spouse to wait beyond FRA to draw.

I’m curious, was the “plan in advance for a useful retirement” more around planning for various insurance, annuities, and other business like matters? Or was it about what to do with all of your free time? What to do with all of your free time is my biggest question about retirement.

What to do with your free time.

“…my current plan is to have my wife take her Social Security when she turns 62. Then when I reach FRA (67), I’ll take my Social Security. She will be 70 and will convert to half of my benefit, which should be more.”

ESI, This is also exactly my plan (and probably same for a lot of high earning readers), so when you find an answer to whether or not there could be a problem with your spouse converting to half of yours later if she takes hers early, please do let us know!

Have you considered using this calculator for additional Social Security guidance? It attempts to provide the best alternative for married couples.

http://opensocialsecurity.com/

There isn’t any confusion about what happens if your spouse takes social security prior to full retirement age. Her spousal benefit gets reduced for every month before her FRA (Full Retirement Age) that she starts her draw. For someone with an FRA of age 67 (which is probably getting to be most of us now) that will reduce her draw to 32.5% of the spousal draw instead of 50%. You would have to run the numbers to see which way it comes out better depending on the age and individual benefits for each spouse, but drawing before FRA definitely reduces the spousal benefit.

SSA describes it here:

https://www.ssa.gov/oact/quickcalc/spouse.html

The math for this is the following:

reduced 25/36 of a percent for 36 months = 25% reduction.

reduced a futher 5/12 of a percent for 24 months = 10% reduction for a total of a 35% reduction leaving 65% of the expected draw.

65% of 50% is 32.5% which is how much she would be able to draw as a spousal benefit if she starts her own draw at 62.

Thanks. This is good to know…

Double thanks! That link explains it all very clearly. So letting my wife take her S.S. early would reduce her spousal benefit, which would be a serious mistake (at least in my case).

I’m amazed (and slightly embarrassed) that with all the online research I tried to do, I could not come up with a solid answer to this question until now.

I have attended several of these on different topics (retirement planning, Social Security strategy, etc.) and my experience was similar. I always learned a few things so it was a worthwhile investment of my time. So far we have always had a good meal at an over-priced place where we would not go if I was paying. One difference is that we always got the meal after the presentation. The lunch option is nice if they have it. We went to one that started at 6pm and we did not get dinner until around 7;30…..but it was a good dinner.

In general the presenters goal was to get people to make an appointment for a 1 on 1 visit to review your financials or hire that firm as a financial adviser. I always declined and they did not press too hard as there were plenty of others signing up. One guy kept saying “you can’t do this on your own” but so far I am comfortable with my investments and strategy. Several of the presentations pressed the “fear factor” showing charts of how much people lost back in 2009. They never said whether their clients did any better than average however.

I did ask a presenter who was with a small financial planning firm how they could afford to pay for the high-priced meals and if it generated much new business. He said that the insurance company (I think it was NY Life in this case) paid for the dinners…..so that helps explain the process a bit and maybe why there is not as much sales pressure as you might expect.

My experience has mirrored Joe’s. I attended one “seminar” that was set as an education event over three weeks. They served drinks and light appetizers, you got a free book. They showed several real world examples of how they managed clients money.

The goal was to get you to a one on one. I went along fully expecting a hard sales push. They asked me about my plan and goals and asked that I provide as much financial information as I felt comfortable with sharing. The explained their methodology and exactly what I would be getting for my time invested.

One week later I met with them and the financial adviser told me I had a plan that had a 90+% chance of meeting my goals and that they would not suggest I change anything. They told me if I had any questions they would be happy to answer, no charge. They suggested I come back at age 62 to re evaluate. They did ask that I tell my friends and family about their service. A positive result for the time I invested.

I still get the ones with dinner at Ruth Chris and the local steak place. Those are the hard sell annuity and life insurance dinners.

I have a friend in another state that is an independent, flat fee financial adviser. He used to work for one of the major insurance companies and in adamant against going to these seminars. He does not meet with his clients for meals or drinks. I shared my experience and his thought was that the industry is changing and the advisers know the clients are becoming more knowledgeable. Coming across as a pushy insurance sales person will not get you the client base you want.

The area of the country I live in has many retirees so we get these invites on a regular basis, probably 2-3 per month. I have attended a half dozen or so and followed up with one on one meetings with 2 of them, but never did anything with them after that. One did a lot of software analysis on all of my investments, down to the mutual fund level, and then created a computer-generated plan of recommendations which essentially amounted to putting a bunch of money into their recommended annuity and converting my 401K and IRAs to Roths as a tax minimization plan to avoid future RMDs and then investing the rest in some of “their” highly recommended Mutual Funds. This seemed to me like a plan to maximize their commission dollars more than my portfolio but they did put forth quite a bit of analysis to come up with their story.

The other 1 on 1 was solely from someone that just sells annuities. His pitch several years ago was that the Dow was at an all-time high of 12,800 and we were in for a major beating so now was a great time to protect our hard-earned savings with a series of “his” highly recommended annuities, which he felt up to 70% of our portfolio should be in. This one was very easy to walk away from.

I did attend another seminar about a month ago that was very similar to the experience you just shared. I liked the presenter and felt he was very straightforward with his responses that also seemed to match many of my own opinions. I did not sign up for the one on one but might reconsider and give them a call down the road.

I’m always open to learning and picking up a new nugget or two to consider so I don’t mind investing a lunch or dinner on occasion if the general topic seems like something I’d like to know more about. I’m sure we will start getting inundated with seminars about the recent changes related to The SECURE Act which probably is something I will want to check out at some point.

Hey ESI – I’ve been working on a social security scenario calculator that allows me to play with different start and end (mortality) dates for my wife and I. It calculates the total of all payments for each scenario I try. Doing these a bunch of different ways (early/late, early/early, late late) and seeing how it affects our total payments allows me to evaluate the risk/reward tradeoffs.

For instance, is it worth giving up $100,000 on $1.8m in total payments in exchange for taking my social security early?

I find looking at it this way makes it easier for me to decide what tradeoff I’m willing to make, knowing that either one of us could die earlier than anticipated and thus leave a bunch of money on the table if we tried to wring every last cent out of the system by holding off claiming to max out the payment.

ESI,

Thanks for doing this and taking one for the team. I’ve always thoughts these seminars were cheap disguises for insurance salesmen. But sounds like this one had some good advice or at least got you thinking.

Couple thoughts:

*Retirement debt – we still hold a mortgage at 3.5% on ~$300k and feel one can do better in the stock market. No other debt is a good strategy. Plus no one wants to be house poor with a bunch of equity in your asset and no way to reach it unless through a HELOC. We’re comfortable with leveraging this debt.

*LTC insurance – these are expensive policies we chose to not buy and will self insure. An example to share – my father (81) just stopped payment on his to self insure at my urging. At $2500/yr it would have paid $188/month if executed. LTC care policies typically are activated <20% of the time and only for approximately one year. Rarely are the benefits exceeding the expenses. We will not do a LTC policy

*Taking SS – while there are many theories regarding this, my premise is based on the following: SS Trust fund is likely depleted 2035, meaning more going out than coming in to SS itself. While we retirees will get a payment, it is likely to be 78% of the total we earned. If the government comes up with a fix, means testing is also likely. Plus break even is 84 at my calculations. I’d rather have the dollar tomorrow than later because the total collected until 84 is the same. I get my money sooner and can enjoy it. And taxes are not going down from here.

*RMDs – with SECURE, the age moves to 72. This is a great thing for sure. But we are front loading our spending to enjoy it while we can and spend down some so our RMDs are not so big and we’re required to pull out more than we need and have to either give it away or buy stuff. Not our plan. With the 72(t) tax law for early retirees, we can take out a set amount now until I’m 59 1/2 and add it our current cash flow requirements and do our spend down strategy from my IRA.

*Reverse Mortgages – good for some who are House rich when cash is needed.

Just some thoughts on your topics and how they aligned to our early retirement strategy. Thanks again for your thought provoking blog.

Best,

Retirement Interviewee #19

I have a NEW take on Long Term Care: Due to aging parents (low 90’s both sides of family), I have had recent long talks with people who have gone “before” me handling parents who have lived long lives. The most alarming thing that I have taken away from Long Term Care Insurance: (especially if one has the best money can buy, – ) The facility has you captive. They keep you alive at any cost because you are their income. So my friend whose mother lived in a ritzy place at $12K/mo. and was deteriorating from dementia was fed her meds. and her long slow demise was and now remains a scar for the entire family. 1.5 years after being put in the facility she passed. A few months later her father was diagnosed with dementia. This time, they called in hospice for a consultation. Her father was taken off all his meds, and allowed to pass in dignity. He did live for 3 months in a long-term care facility, but closer to home and much less expensive. His passing will be remembered as being much more compassionate than her mothers. Does anyone think along these lines or am I the odd woman out? (That LTC – induces the facility to stretch out your life for the income?)

I would tend to agree — that facilities try to prolong life/payment and that I’d prefer the latter option.

This is 100% consistent with our experience. An expensive consultant we hired to help us make decisions for an aging/dying parent in a “high end” $12K/month facility told us we did not really need hospice at end of life – but what we figured out (on our own) was that unless we placed our parent under hospice care, the facility would completely ignore our instructions to take her off meds (which weren’t working anyhow) and only keep her comfortable and let her pass naturally. They are simply not oriented towards anything but keeping the patient alive, no matter what (though we often questioned the quality with which they carry out that mission). It wasn’t until we brought in hospice that we were able to manage the very end of life phase.

And our parent also coincidentally had LTC insurance, which after we ran the numbers, we figured out that she paid somewhat more in premiums than we ever got in benefits. Insurance companies aren’t stupid – there is enough fine print and red tape in those policies to “insure” that they are unlikely to pay out more than the premiums collected. I could write a book on all the little ways they managed to void claims. Fortunately, our parent was financially solid and not completely reliant on the policy.

My financial planner has all but given up pitching LTC insurance to us.

Thanks for sharing this (and braving the experience for all of us!). A couple items stand out – one in particular being debt in retirement. I am a financial services professional with a CFP designation among others, and nearing “re-wirement,” myself. My wife and I have begun the process of building a new home where we’ll move in about a year. We have a net worth of over $7M with $6.25M in liquid assets. When posed with the option of paying cash for our new home or taking out a 3.25% 15-year $750k mortgage to finance it (or a combination of these), I went for the mortgage it with zero hesitation. We will put the approx $550k proceeds from the sale of our current home into a low-cost balanced fund whose 10-year average return has hovered around 9.4% and whose return since inception (in 2000) is about 6.6%. Even if the fund underperforms slightly during our 15-year timeframe, the 2.5% rate arbitrage (6 percent earnings less the 3.5 percent mortgage rate) I project will cover just over 13 years (about 88%) of our monthly mortgage payments and allow us to maintain an enhanced level of liquidity. In other words, I could take the $550k proceeds, add $200k to it, and pay cash for the house, tying up $$ in bricks and mortar, or I could leave the $550k liquid, prudently-invested and liquid, and allow its proceeds to pay off the entire $750k obligation for me, with interest.

At a time when interest rates remain historically low, and retirees and near-retirees are looking for ways to leverage the equity in our homes by using tools like a HECM (essentially, a reverse mortgage), why would this planner – and others – be so averse to mortgage debt that essentially accomplishes liquidity in a different way, as long as it’s serviced intelligently?

I fully-appreciate the value of a debt-free retirement allowing one to “sleep soundly” but it’s not a uniformly-wise, mathematically-justified recommendation, and planners should stop treating it as such, particularly for those who’ve demonstrated an ability to leverage debt wisely, during their lifetimes.

Thanks again for braving the luncheon!

Great plan since the mortgage amounts to only about 10% of your net worth.

“why would this planner – and others – be so averse to mortgage debt that essentially accomplishes liquidity in a different way, as long as it’s serviced intelligently?”

Because 97% of the population is not as wealthy, financially experienced or as disciplined as you. Statistically speaking, the majority of Americans are woefully unprepared for retirement and will have to be very diligent in their spending, saving and investing to eke out a workless retirement. For most, eliminating debt before they retire will be a key component before they can exit the workforce, especially as pensions go away and the future of SS is uncertain.

Following are things I’ve worked out, comments welcome if I’m wrong on anything.

If your spouse’s health is questionable, there are special things to consider about SS and RMDs.

– If your spouse can only collect on your benefits, then see if both of you should start collecting SS early. This will let you get as much as possible if spouse’s life expectancy might not last until you reach your optimal age to start collecting. Otherwise, you’ll forfeit all the money that your spouse could have collected.

– Loss of spouse will force you to file taxes as single instead of married, thus likely throwing you into a higher tax bracket if you have taxable income. This is also a big factor if you’re planning to convert IRA funds to Roth. The usual plan is to convert the largest amount possible without it pushing you into the next higher tax bracket. Losing the married filing status makes it more expensive to convert because you’re probably already in a higher tax bracket.

You need to recheck that SS plan. If your wife takes her social security a day before her full retirement age, and you said she’d take it at 62, then when she migrates over to either half of your benefit or if you die, takes your benefit as hers, she will get less than if she had waited until she was at full retirement age. The only enception is if she takes hers at full retirement age and then switches to half of yours when you take yours at age 70 there is no loss of benefits. Talk that over with an expert because what you proposed will cost you as a couple.

Like they say, “There is no such thing as a free lunch!” I did go to a “free” dinner meeting hosted by Personal Capital for their clients with accounts exceeding seven figures. It was pretty interesting listening to some of their company leadership describe how they make decisions. I believe they hoped we would have brought guests, but we didn’t. And I think they’ve discontinued having those events. I was impressed with how young many of the other multimillionaire clients were. Most seemed to be medical doctors or oil and gas executives.

“I was impressed with how young many of the other multimillionaire clients were.”

May not necessarily have represented “earned” wealth. Years ago when I was on the board of a big city co-op apartment building, I got to see a lot of financial info on prospective apartment buyers (for the uninitiated co-op buyers have to submit a lot of income and wealth diligence info in order to be approved by the board before being allowed to buy an apt). What was quite a surprise for me was how much “support” most of the applicants received from parents, sometimes in the form of regular, substantial “gifts” that boosted their investment accounts early on. I have a couple of buddies doing exactly this for their adult kids as a tax-friendly means of transferring wealth. This explained how a lot of the younger creative/artsy professionals were able to live so nicely in one of the most expensive zip codes in the country. Hey, nice life if you can have it all, jus sayin.

I’ve seen a lot of those types too, but these at the Personal Capital thing seemed to be high earning docs and Corp execs, not spoiled brats. In not sure the brats invest that much, they mostly spend!

I live in your neighborhood so I get much of the same stuff. My wife and I were customers of SFP about 10-12 years ago, when we first sought out financial advice; the two men we worked with seemed conflicted when they pushed annuities at us and I challenged them on the appropriateness for us. They confessed to getting pressure to sell these lucrative insurance products. That was the beginning of the end for us and SFP. Since then we evolved to self management.

Two things I have done: my retirement plan includes $500k in self-funded memory care (Alzheimer’s is killing my dad), and my retirement budget covers a mortgage—I won’t pull money out of investments to pay a low-interest loan.

I celebrated my retirement with friends in that wine room thirteen months ago!

I’ve heard of these Direct Mail Retirement Seminar mailers, but have never gotten one. I would enjoy a free meal, and it sounds like it was somewhat enjoyable.

My wife and I once went to a timeshare presentation (although they insisted it wasn’t a timeshare). That was an awful experience. Plus it was for free tickets to a show – which they almost didn’t give us.