Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

Today we have Andy from Marriage Kids and Money.

This interview took place in June.

My questions are in bold italics and his responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I’m 38 years old and my wife is too.

We’ve been married for 10 years.

Do you have kids/family (if so, how old are they)?

Yes, we have two children. My son is 6 and my daughter is 8.

What area of the country do you live in (and urban or rural)?

We’re a suburban family living in metro Detroit, MI.

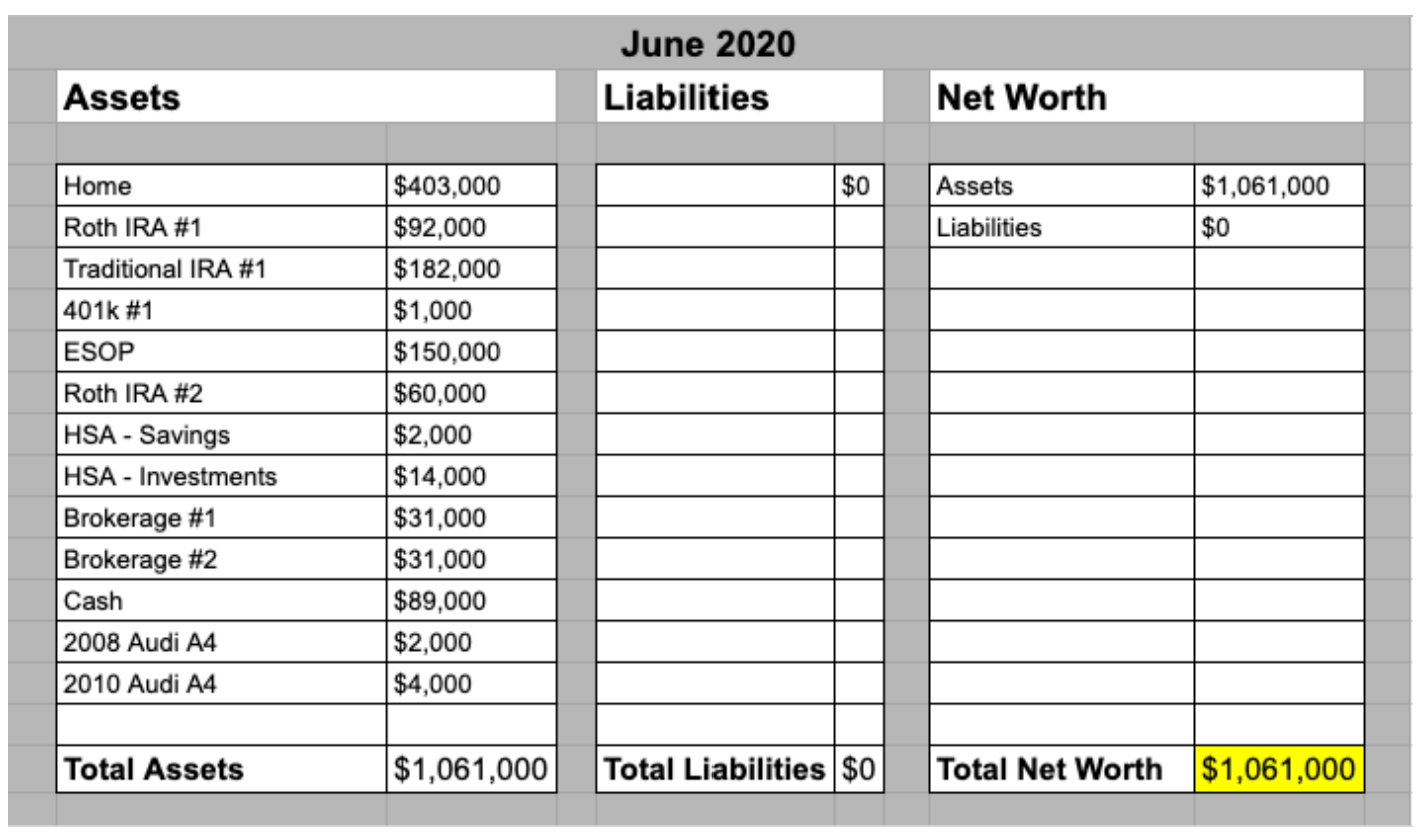

What is your current net worth?

$1,061,000

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

Our home is worth around $400,000 and we own it outright.

We have retirement accounts totaling $350,000.

The rest of our assets are in cash, my previous employer’s ESOP (Employee Stock Ownership Program), taxable brokerage accounts and a couple of 10-year old cars.

We do not have any debt.

Here’s a net worth chart for reference below:

EARN

What is your job?

Up until about 6 months ago, I was a full-time corporate event marketing sales professional. I was in this industry for 15 years and climbed the corporate ladder earning a generous salary along the way.

I decided to make the leap into the world of entrepreneurship earlier this year after my passion for corporate event marketing faded.

Today, I own a small media company with the goal of helping young families build wealth and thrive. Some of my current revenue sources include advertising, sponsorships, coaching, freelance writing, content production and speaking.

Now, I absolutely love going to work every day!

What is your annual income?

Over the past 10 years, our average annual household income was $190,000.

This year, we project our annual household income to be around $125,000. My new business will hopefully grow over time and our income along with it.

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

My salary for my very first full-time job out of college was $38,000. I worked as an “Event Coordinator” traveling around the United States and Canada showcasing luxury cars to luxury clientele. It was an incredible job for a 21 year old!

After a while, I got tired of being on the road. My time off usually fell on a random Tuesday because I was always working on the weekend. Our events usually happened on the weekend so I was always working on Saturday and Sunday. Hanging out with friends and family became very difficult.

I decided it was time for a change out of the events industry.

Advertising was my next industry choice. But to get myself off the road and into a more 9-to-5 kind of lifestyle, I had to take a $10,000 pay cut! Looking back, this was not a smart move on my part. My new income was so tight that I could barely make my mortgage payments or pay my bills.

This was around the time I started to use my HELOC (Home Equity Line of Credit) as my personal ATM. When I didn’t have enough money to go to the bar with my friends, I’d borrow a little bit from the HELOC. If there was a vacation or concert I wanted to go on, the HELOC became my go-to.

Over time, I decided that the only way for me to make more money was to go back to school and get my MBA. Surely, the MBA would help me grow my income!

5 years and $30,000 of debt later, my salary had finally started to grow (honestly, I think it had little to do with me getting an MBA). I rejoined the events industry and took a stressful, demanding and complicated position working for another luxury automotive company.

At this point in my career, I was making around $70,000 and my new wife was making $60,000. This double income no kids (DINK) portion of our life allowed us to do some amazing things financially for our family’s future.

After having children, I felt the pressure and desire to continue to grow my income as high as possible. I was in a commissioned sales job and the sky was the limit as long as I put in the hours. In our second year of marriage, my wife and I made $280,000 combined!

The income was fantastic, but my life felt out of balance working so many hours and being away from my wife and my newborn daughter.

Once again, I decided to make a career change to another event marketing company that provided incredible benefits and a salary of $160,000 that would allow my wife to stay at home with our daughter and our yet-to-be-born son.

The year I left my corporate event marketing career behind I grew my income to around $180,000.

Today, with my small business, I hope to earn an income of around $75,000. It’s a major pay decrease but I absolutely love the work that I’m doing.

What tips do you have for others who want to grow their career-related income?

There was a pivotal moment in my career when I went from that 5-figure income to a 6-figure income. Nearly a decade went by when I was making over $100,000 and that dramatically helped our ability to become young millionaires.

Depending on your situation, background and experience, here are a few ways I feel others could do the same:

- Establish credibility. Be someone that your colleagues, clients and supervisors can rely on. When you say you’re going to do something, do it on time and go above and beyond with the request. This way, when new opportunities arise, you’ll be the first person they consider.

- Express your interests and speak up. If there is a job opening that you want, make it loud and clear that you’re interested. Perhaps you feel that you should be paid more for the work you’re doing. If you’ve been accomplishing your goals consistently and it’s been a while since you’ve been promoted or been given a raise, it’s time to speak up. Start the conversation politely yet confidently. Over time, these tough conversations meant hundreds of thousands of dollars for our family.

- Grow your network (and your net worth). It’s fun to track your net worth, but your network can be even more important in growing your wealth. I made it a point to connect with and grow relationships with as many people as possible during my time in corporate event marketing. Being polite, smiling and genuinely being interested in conversations can go a long way in creating connections that last decades. And those connections can help you with new career opportunities or even small business ventures.

What’s your work-life balance look like?

In corporate event marketing, you’re busiest when the events are happening. And given that my last employer was a global events company, we would travel for sales opportunities, presentations and events quite a bit.

Today my work-life balance looks a lot better than it used to.

My typical work-week lately has been Monday through Thursday, 10am-6pm. I take Fridays off to be with my kids and roll into the weekend.

For the past year, I have been pretty good at “turning it off” when I’m not working too. Friday through Sunday, I don’t check social media which helps me focus on my family.

Do I stick to this plan all of the time? No, but the fact that it’s part of my routine and schedule makes it happen 90% of the time. And that’s a lot better than where I used to be.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

At this time, our income sources are as follows (approximately):

- My small business: $75,000

- My wife’s job: $50,000

Together, we’ve found a couple of good 30+ hour per week gigs that give us a decent income and allow us to still be together, not work weekends and spend time with our kids.

In the future, I’m interested in developing passive income streams from dividend investing, but I honestly don’t know enough about it yet. The learning continues!

SAVE

What is your annual spending?

Around $70,000 per year.

What are the main categories (expenses) this spending breaks into?

- Housing = $17,000

- Transportation = $6,000

- Food = $10,000

- Entertainment = $12,000

- Kids = $6,000

- Donations/Gifts = $10,000

- Other = $9,000

Do you have a budget? If so, how do you implement it?

Yes, we have a budget. Around 2011-ish, we started using Mint and it’s helped us stay on target for our big financial goals.

Originally, I brought up the idea of managing our household finances with a budget early on in our relationship. My wife appreciates how organized we are with regard to our finances and always reminds me to have a little fun along the way…that’s why I love her!

Our monthly budget meeting is called the “Budget Party”. My wife wasn’t keen on the idea of budgeting in the beginning so I thought if I came up with a slick name that she might show up. It worked! Maybe it was the pizza and booze I brought to the “party” too that helped…who knows?!

What percentage of your gross income do you save and how has that changed over time?

Over the 10 years of our marriage, we saved around 50% of our income. This helped us to achieve our big goals like becoming debt free, paying off our mortgage early and becoming young millionaires in our 30’s.

Now, we’re taking our foot off the gas so that we can enjoy more life today by working less. With less income coming in, we’ll save less. But for the first time in my life, I’m not worried about it so much!

It remains to be seen how much we’ll exactly save this year, but I’d venture to guess around 20% instead of 50%.

What is your favorite thing to spend money on/your secret splurge?

I am a sucker for new tech gadgets.

We just got a brand 70” TV in our basement for watching movies together.

I bought an electric scooter (like the Birds or Limes you see on the street) for my wife because she wanted one. But, I’ve ridden it 10 times more than her because it’s so much fun!

We have two Amazon Alexas – the kids love them too!

Also, I love going on family vacations. Michigan is a beautiful state, but come winter time, we need to feel the sun! Some of our favorite destinations are Florida, California and Mexico.

INVEST

What is your investment philosophy/plan?

I’m a fan of low-cost index funds.

They are simple, easy-to-understand, low barrier to entry and incredibly effective.

Retirement

Right now, our investment portfolio for our retirement breaks down as follows (keep in mind we’re both 38):

- US Large Cap: 60%

- US Mid/Small Cap: 10%

- Int’l Equities: 10%

- REITs: 10%

- Bonds: 10%

The goal is not to touch these funds until we’re 65. At this point, if we let our investments grow without touching them until 65, we could potentially have over $3,000,000 in our retirement years (assuming a 7% interest rate).

At a 4% withdrawal rate, that would give us $120,000 per year to live on. Plenty!

Semi-Retirement

We’re already at our first level of semi-retirement right now. Working 30+ hours per week with jobs we enjoy.

The problem is that we HAVE to do this work. What about the time when we don’t want to?

That’s why I think it would be fun to add another level to our semi-retirement journey. Our second level would allow us the ability to work less than we already are or simply cover more fun expenses in our lives.

In order to fund that second level of semi-retirement, here’s how our current brokerage portfolio is laid out:

- US Large Cap: 50%

- REITs: 20%

- Bonds: 30%

Currently, we don’t have a lot in our taxable brokerage accounts. Between me and my wife, we have around $60,000 total.

I’d love to grow this to $1,000,000 over the next 10 years. That would give us the ability to safely withdraw $40,000 per year and have the balance continue on into our retirement years (where we’ll have a large amount of investments waiting for us anyway).

What has been your best investment?

I know a lot of people don’t consider your primary residence an investment, but I do.

We purchased our current home in 2013 for $350,000 with $150,000 down. My wife and I paid off the $200,000 mortgage in less than 5 years.

Now, we live in our $400,000 home free and clear. It’s an amazing feeling to live in a home without a mortgage!

What has been your worst investment?

My worst investment would be buying my first home.

In 2004, I bought a $200,000 home with maybe 10% down. I quickly learned how expensive homeownership can actually be.

I definitely did not factor in furnishing, repairing, updating, painting, decorating and paying utility bills. Quickly, my homeownership dream became a nightmare. I started to accumulate debt and started working on creative ways to make more money like house hacking and selling a lot of my possessions on eBay.

As time passed on, the housing market took a major turn and my home was valued around $110,000 instead of $200,000. The mortgage was still very high at around $170,000 and at the time I had a HELOC of around $10,000 as well.

When I finally sold the house in 2013, I was able to receive $225,000. I definitely spent WAY more on housing upkeep, repair, debt payments and heartache than was worth it.

This experience was a major reason that I set a goal of living mortgage free in the future.

What’s been your overall return?

We bought our home for $350,000 in 2013 and it is now valued at $400,000 in 2020.

After about $50,000 of updates (roof, kitchen, laundry room, closet, etc) between the time of purchase and today, our ROI is probably $0.

Still…the best investment I’ve ever made. I love our house.

How often do you monitor/review your portfolio?

Twice per year, I rebalance our portfolio to ensure we’re not overleveraged in certain areas.

Outside of rebalancing, I don’t really look at our investment accounts that much. I know that our portfolio is going to go up and down quite a bit over the next 25+ years until we retire. There’s not much I can do but keep riding the rollercoaster and rebalancing every once in a while.

NET WORTH

How did you accumulate your net worth?

Our net worth was accumulated through earning a high household income over a period of 10 years and then putting that money to work for us. During that 10 years, we had an average HHI of around $190,000.

With that money, we did the following to grow our net worth to over $1,000,000 in 10 years:

- Eliminated our $30,000 of student debt and $20,000 of car debt

- Saved $150,000 for a down payment on our new home

- Maxed out my 401k from 2013 to 2020 (and received 15% employer match)

- Maxed out Roth IRA contributions for a few years

- Started an HSA savings and investment account

- Paid off our $400,000 home in less than 5 years

- Saved $100,000 so I could have a runway for my first year of entrepreneurship. (Happy to report that we haven’t had to live on any of it yet!)

My wife did receive a small inheritance of $30,000 after her Mother passed away last year. We’re using that money to create an annual celebration that can live on year after year by using the quarterly dividends earned. Our first celebration will be this summer!

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

For the last 10 years, I would say that “Earning” has been our best wealth-building tool.

And for the next 10 years, I’m hopeful that “Investing” will be our next best wealth-building tool. If we don’t touch our money, continue contributing to our accounts over a few decades, then we should continue building wealth and creating a comfortable life for ourselves and our kids.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

My wife and I had more than few arguments about money during our 10 years of marriage. These arguments stemmed from our differing views on money, saving and enjoying life today.

Through time, 18 months of marriage counseling and both of us truly empathizing with each other’s backgrounds, we found that our differences were actually martial advantages. She helped me understand why she wants to enjoy life more today and I helped her understand why prioritizing saving and investing early was important for me and our family.

By empathizing with each other, we had the ability to benefit from both viewpoints. I now see the value in enjoying each of our days more fully. And now she sees the benefit of planning for tomorrow.

In short, we’re finding a way to “buy the hot tub” AND “retire early”!

What are you currently doing to maintain/grow your net worth?

This year, our income is going to take a big hit. We made close to $200,000 last year and this year we’ll be closer to $125,000.

With that, we won’t be saving nearly as much as we have in the past. We’re happy to make this income trade for more time doing work we enjoy.

Hopefully, over time, we’ll grow our income doing the work we love. If not, we’re not too worried because we enjoy our current lifestyle a lot.

We’re hopeful that our investment balances will continue to grow over the next 10 years while we focus on enjoying our family lives. With two kids under 10, these years matter a lot to us.

Do you have a target net worth you are trying to attain?

Not anymore. $1,000,000 before 40 years old was my big stretch goal and we did it.

For now, I’m happy to relax more and let the power of compound interest do it’s work.

If we don’t contribute another dime to current investment portfolio, earn a conservative 7% interest rate and our other assets hold around the same value, we’ll hit a $2,000,000 net worth before our 50th birthdays approximately.

Given that, I’ll set a new goal today that we’ll go for a $2,000,000 net worth in the next 10 years (by 2030)!

Setting goals is fun. I’m game ESI family!

How old were you when you made your first million and have you had any significant behavior shifts since then?

38 years old.

I’m not as income-focused now. For the next decade, I’m focused on doing work that I love for 30 hours a week.

With a little luck, I’ll make a solid income and grow our net worth even more.

If we don’t, that’s totally fine. It’s just a number.

What’s more important is that I’ll be there for my wife and my kids during a crucial decade during their adolescent years.

What money mistakes have you made along the way that others can learn from?

Here are the top three money mistakes I’ve made during my wealth-building journey:

Buying a Home I Couldn’t Afford

As I mentioned above, my first home quickly became a nightmare when I realized the true cost of homeownership. The hard times were compounded when the metro Detroit housing market had a huge hit during the Great Recession.

Purchasing My Wife’s Engagement Ring with my Student Loans

In 2009, I was SO in love with my girlfriend (now wife) that I wanted to get married to her as quickly as possible. The only problem was I didn’t have enough money for the ring.

I decided to borrow from my student loans to buy it.

It was a pretty great “investment”, but I wish that I would have saved up for it with my own money and been a bit more patient.

Having Blind Faith in my Investment Broker

In 2012, we had saved up over $100,000 and we were looking for a short term (less than 24 months) place to hold our money. We asked our “investment broker” for his advice and he suggested putting it in bond funds.

I didn’t understand what a front load fee was until that day.

A few months later, we were down by around $7,000 and we just felt swindled. Shortly after that, we broke off our relationship with him and I’ve been managing our investments ever since.

What advice do you have for ESI Money readers on how to become wealthy?

If you want to become wealthy, study and read up on others who have done it. ESI Money and the Millionaire Interview series is a fantastic place to start.

Also, seek out specific stories, blogs and podcasts that inspire you and your specific path. There is no one right way to become wealthy. Find your very own special way and pursue it.

FUTURE

What are your plans for the future regarding lifestyle?

The next 10 years: Our short-term goal is to work 30 hours per week doing work we enjoy.

10 Years from now: Our long-term goal would be to have the option to work less. We would do this through making $40,000 per year of passive income.

What are your retirement plans?

By age 40, we want to have the ability to work 30 hours per week doing work we enjoy. At this point, we will more than likely stop saving for our traditional retirement (401k, IRA, etc) because we should have plenty waiting for us at 65.

By age 50, we want to have the ability to work 20 hours per week doing work we enjoy.

By age 60, we want to have the ability to work 10 hours per week doing work we enjoy.

By age 65, we want the ability to choose whether or not we want to work at all.

When money isn’t an issue anymore, we’ll do more of what we love. Travel, spend time with family and give back.

Are there any issues in retirement that concern you? If so, how are you planning to address them?

I’m concerned about how much we’ll be taxed in retirement with our pre-tax retirement funds because I have no idea how much money we’ll be making in our 60’s.

We’ve decided to diversify our tax advantaged accounts to help with that. We have a good amount of funds in both pre-tax (traditional IRA) and post-tax (Roth IRA) retirement accounts.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

I’ve been interested in saving money to hit financial goals since I was a kid, but it didn’t “click” until I learned I was going to be a father at the age of 29.

The idea of fatherhood jolted me into wanting to take better care of our financial situation. I wanted to give my kids the best life possible.

Who inspired you to excel in life? Who are your heroes?

I’m very grateful for discovering the magical world of “personal finance” in my late 20’s. Folks like Suze Orman and Dave Ramsey were my gateways to a world of possibilities. They emphasized the importance of controlling your money to create the life you’ve always wanted.

Scott Alan Turner helped me understand the importance and simplicity of index fund investing.

My father showed me the importance of dedicating yourself to a goal and seeing it through to the end.

My mother demonstrated the importance of frugality and the power of saving. She helped me open my first savings account in 3rd grade.

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

- The Total Money Makeover

by Dave Ramsey: This book opened my eyes to the simplicity of personal finance. You don’t need to know all the jargon or be a PHD to control your money.

by Dave Ramsey: This book opened my eyes to the simplicity of personal finance. You don’t need to know all the jargon or be a PHD to control your money. - The Simple Path to Wealth by JL Collins: JL Collins’ book that is all about simplicity when it comes to investing. While Scott Alan Turner’s book 99 Minute Millionaire opened my eyes to index fund investing, JL Collins’ book broke it down and made it easy to comprehend.

- The Slight Edge by Jeff Olson: The Slight Edge demonstrates how simple daily actions compounded over time can lead to tremendous results.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

Yes, our family gives to charity.

In 2017, we gave around 1% of our after-tax income. When we finally calculated that, we decided we could and should give more.

In 2018, we laddered up to 3%. In 2019, we did 5%.

This year, we’re aiming to give our own version of “10% giving”.

- 5% to charities

- 4% to family

- 1% randomly (random acts of kindness and big tips during the holidays)

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

Right now, our estate plans are to give everything to our kids. They are young and we want them to have a great life if we were both to pass away early.

If we’re able to live full lives, we’re not quite sure what we’ll do. I like the idea of leaving the world a better place than we found it. That may be best directed by our children or it may be best directed by our favorite charities. We’ll see as time rolls on.

This Warren Buffett quote always sticks with us though …

“Leave your children enough money so they can do anything, but not enough that they don’t have to do anything.”

Great story! Thanks for sharing.

So glad to see a millionaire giving money away and having the desire to increase that giving instead of most of these interviews where wealthy people give little or nothing. As Winston Churchill is reported to have said, “We make a living by what we get, but we make a life by what we give.”

I love that quote!

Nice work! I think it’s great you are choosing a path of being able to spend more time with your family and a healthy work/life balance. Also it’s refreshing to hear that you are not solely focused on “retirement” and actually enjoy your work and plan on it being a part of your life past the point of being financially independent.

Great interview!!

So appreciate all you shared and offered within each question! Interesting and informative!

Sounds to me that you’ve found your way and you’re on the right path.

Keep your focus on your wife and children, as you’re clearly doing.

Trust me, 65 will be here before you know it. As the country songs says, “Don’t Blink.”

Thank you! I’m very excited for this next chapter of my life.

I still have a lot to learn about small business ownership and how to grow a business. That’s going to be a fun journey!

Great story. Congrats. At 38 you are well ahead of the pack. It’s also great to hear how counseling helped you. I wish my wife and I had done the same, it would have helped us further accelerate our journey to FI.

Thank you! Counseling was huge for us. It helped me truly empathize with wife and learn how to communicate more effectively.

I’m not sure about Andy’s target. He says he will have $3million when he retires at 65. That’s 27 years from now and the safe withdrawal rate of $120,000 in the first year sounds like plenty, except the buying power will be the same as $54,000 in today’s dollars. Again that might be plenty but it is less than half of what it sounds like. On the other hand he was only talking about retirement accounts, by age 65 he will have a lot of taxable investments as well and probably will be looking at additional funds available to withdraw safely. In fact he mentioned hoping to be able to pull $40,000 from those accounts even before retirement. I think he is in great shape to live a rich life now and in retirement because he will have more than enough invested to offset inflation.

It’s a great point on “future dollars” vs. “today’s dollars”.

I’m hoping my small business will continue to grow and that will help us put away more for taxable brokerage, HSA and other recurring digital passive income streams.

Great share and congrats on the milestone.

Based on what you’ve shared , It would seem that you would factor the equity if your business into your retirement plan. You mentioned that you enjoy what you do – and that being self employed was a goal. You didn’t seem to reference the aspects of self employment that put you ahead in so many ways. It’s would seem that this would be your greatest accomplishment yet – to become self employed and create a cashflow stream. That’s no small matter.

Also – great job with paying off the mortgage. With money as cheap as it is to borrow ; have you considered a 30 year note so that you can accelerate your business ? Your top book is a Dave Ramsey book so maybe not. Just curious.

Congrats on all you’ve done. I’m interested in the entrepreneurial aspects of you though over all of the rest. Self employment is usually the key to true security and wealth.

Great job !

Your point on money being cheap right now is well-taken. Rates are crazy low!

For me, I like keeping our expenses lower (no mortgage) – it helps me sleep better at night. So to borrow from my home for the business doesn’t sit well with me. You’re right on a top book being Dave Ramsey (I like the anti-debt message) – it’s not right for everyone and I definitely see the upsides of having low interest rate debt in your life. It’s just not for me.

I’m excited about growing that small business though!

Thanks for sharing! I see a lot of similarities in your story and situation with my own. I love your alternative concept of the 10% giving – that is something I’d really thing about implementing as well! As a follow up question, what are your thoughts on college savings / 529 for the kids?

Thanks! Yes, we’re digging the alternative 10% because it allows us to be more generous with friends, family and neighbors today.

As for the 529, we’ve been saving in accounts for our kids since they were born. We have around $80k invested right now (kids are 6 & 8). How college will look in 10 years is a big mystery though!

I think we’re going to slow down our 529 savings so we don’t have too much. I believe John has experience with this!

Good story. I am about 10 years ahead of you and see a lot of similarities in our approaches. Good luck. Also good for you not looking to frequently. It has been some turbulent times recently, and likely more to come. Much easier to stomach it if you are not looking. Enjoy those kids. They grow faster than you can imagine.

Thank you! I’m enjoying the time with them while they are young (also tearing my hair out at times too – haha)

This isn’t easy. But it’s also worth mentioning that whoever is able to balance both personal and financial life.. turns out to be the most happiest person.. Sending you lots of good wishes and more success and happiness in life…

Thank you Riya!

It’s a delicate balance and I’m working on it daily. I hope I’m able to figure it out. It’ll be a fun ride either way.

I think once you get more in equities then you will feel much more secure than you do now and sleep just as well.

I followed the DR plan for 6 years until I realized it wouldnt help me reach my goals.

Sure, I would have financial “peace”, but not financial “independence”, and still have to work for 40 years whether I loved the work or not.

I like that you call out the possibility of not wanting to do the work but still have to. Keep your investing rate high and the 2nd level you are seeking will come soon enough.

That’s the best quote! Really good interview & great job with your finances!