Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

Here’s our latest interview with a millionaire as we seek to learn from those who have grown their wealth to high heights.

If you’d like to be considered for an interview, drop me a note and we can chat about specifics.

This interview took place in August.

My questions are in bold italics and their responses follow in black.

Let’s get started…

OVERVIEW

How old are you (and spouse if applicable, plus how long you’ve been married)?

I am 39 years old; my wife is 41.

We have been married for 11 happy years.

Do you have kids/family (if so, how old are they)?

We have two kids, ages 5 and 3.

What area of the country do you live in (and urban or rural)?

We are blessed to live in a city of about 150,000 people in the great state of Idaho.

What is your current net worth?

We’ll do a deep dive into the value of our assets next month when rents are finalized, but I believe we are in the $2.7M range.

What are the main assets that make up your net worth (stocks, real estate, business, home, retirement accounts, etc.) and any debt that offsets part of these?

Assets

- Rental Properties (sole ownership): $1.97M

- Rental Properties (partnerships): $725k

- Primary Residence, no mortgage: $215k

- Stocks: $4k

- Land: $125k

- Cash: $140k

- Business Interest: Minimal saleable value

Total: $3.16M

Liabilities

- Rental Properties (total): $460k

We may be under-leveraged in our portfolio, but we like to be conservative and have worked on paying down mortgages over the last few years while investment properties have been expensive.

We are minority partners in a few small businesses that are related to our primary business.

EARN

What is your job?

The short answer that I usually give is that I’m a real estate investor. The longer and more fun (to me!) answer is that I’m a self-employed asset manager/entrepreneur, but that’s usually more than people want to hear. I retired from traditional work in 2014.

My wife works in our businesses as the accountant and does freelance bookkeeping for small business owners. She retired in 2019.

What is your annual income?

Annual income last year was $150k, which we anticipate growing about 20% this year.

Thankfully this comes from rental properties and is tax-advantaged, keeping our tax rate manageable.

Tell us about your income performance over time. What was the starting salary of your first job, how did it grow from there (and what you did to make it grow), and where are you now?

I worked in fast food at minimum wage in high school, which cemented my plans for going to college. My older coworkers showed me the difficult realities of being an adult working for near minimum wage, which was not the life I wanted. It was a very hard but necessary lesson to learn at 15, and one I think every teenager should learn.

After 3 years of working in fast food, I graduated to cleaning pools at $8.00/hour but less hours, leading to roughly the same income for less work. This was a revelation, and I got my first taste of entrepreneurship as my boss was a jack of all trades who set his own hours, which seemed cool to an 18-year-old. Both jobs as a teenager allowed me to build savings for college.

In college I worked as a math tutor during the year and took various jobs during the summer.

I discovered the value of commission-based income working as a security system installer at $100 per install and did that for two summers. I loved the reward of working hard and being paid proportionately rather than by the hour. Those two summers of hard work allowed me to graduate with very little debt since I attended a reasonably priced university.

The summer before my senior year I got an engineering internship paying $18/hr. and spent most of the summer very bored as it was 2008 and the economy was slowing and work for the company was drying up. It was great money for a college kid, but I found out I’m not meant to ride a desk looking busy.

I graduated with a degree in Mechanical Engineering in the depths of the Great Recession and it took about 8 months of unemployment (aside from starting a few of my own businesses) and another stint installing alarms before I got a job in engineering. This job started at $55k/year and was a lot easier than alarms, and every paycheck felt like winning the lottery since I was used to living on nothing while unemployed.

I turned out to be very good and very efficient at my job and was proactive in moving projects forward and seeking out work when I was bored. The company had no standard mechanism to review compensation, but I was proactive in seeking raises and responsibility and my bosses created several positions for me within my engineering group. Over the course of two years, I maxed out the income ($65k) for my career level and didn’t seek promotion because the next level meant a huge increase in hours and responsibilities without commensurate pay.

On the side of this, I met my wife and got married. Our dual incomes plus fledgling rental empire meant that in the first year of our marriage we were able to save a sizeable war chest. We had been given excellent advice to make the most of these early years of marriage, so we did by quitting our jobs to travel the world. We spent 6 months traveling Europe and Southeast Asia, and amazingly when we returned discovered that we were MORE employable than we had been before!

My wife received interest from several companies and eventually “settled” on a job she enjoyed more and got a roughly 40% pay increase to $50k. I approached my previous employer who welcomed me back as a contractor. This was ok news as it meant I had an income ($30/hr.), but turned into excellent news when I received an offer to contract with a different firm a few months later and leveraged that into a rate of $45/hr.

The end result of quitting our jobs and traveling was that our combined income went from $100k ($65k + $35k) to $140k ($90k + $50k) in one year!

Roughly a year after returning from traveling, we had rebuilt our savings to the point that I could quit my job and begin my real estate investing career in earnest. We were then living off a combination of my wife’s income, savings, and rental income from the 6 rental units we’d bought. We purchased 9 additional rental units the first year that I became self-employed and have continued to add to our portfolio and income.

Today our income is 90+% passive, 10% from our business ownership, and 0% from anything that approaches a traditional job.

Since I retired from traditional work, our income has been as follows (rounded):

- 2013: $150k (I retired)

- 2014: $80k

- 2015: $80k

- 2016: $90k

- 2017: $105k

- 2018: $130k

- 2019: $160k (wife retired end of 2019)

- 2020: $141k

- 2021: $150k

Switching to full-time real estate investing (buy and hold) caused our initial income to drop, but it was a strategic move that continues to pay dividends and compound with time. Additionally, our net worth has gone from ~$100k to $2.7M, so while we took a step back in income, there are other ways to measure financial success.

Hence the “S” and “I” in ESI!

What tips do you have for others who want to grow their career-related income?

- You must provide value in some way or form to your employer or marketplace. The more value you add, the more you can expect to be rewarded, but only if you…

- SHOW value to your company. There are a lot of very intelligent, hard-working people out there who are underpaid, because their superiors don’t know or chose to ignore the good work they do. If you do a great job, your projects succeed, and you make your boss look good, make sure your superiors know that you are part of the reason why. My grandma used to say, “If you don’t toot your own horn, your horn won’t get tooted!”

- You must believe in the value you bring, and once you know that you add value, don’t be afraid to ASK to be compensated like it. Your boss (or their boss) will not wake up tomorrow and think “(Your name here) does a great job, everyone likes her, and we are just not paying her enough. I’m giving her a raise!” It is up to YOU to ask for what you’re worth. Average people are a dime a dozen and won’t get raises. Good people are hard to find, and companies will do a lot to make them happy because it takes a lot of time and money to replace them. ROCK STARS (at all levels) get whatever they want because they are crucial to the company’s success. My wife was one of those and when she went to leave because work wasn’t fun anymore, her company threw 30% raises at her every 4 months to try and keep her and would have given her anything. Most of the gains in income between 2016 and 2019 were because her company couldn’t bear to see her go. Be the rock star!

- Keep your eyes open for opportunities with other companies. The conversations about potential raises were very different when I was just asking for one (5%-10% raises) than when I had proof of my value in the marketplace (40% raise). Less sales/negotiation is required when you can show what the competition will pay you. If you’re the gambling type and believe in your value, you can even bluff to get raises as long as you’re prepared for the consequences!

- Speaking of sales, learn to sell. I am not a natural salesman, but I’ve learned that we are all trying to make sales, all the time. You must sell yourself to a company to get a job, or sell your value to your boss to get a raise or be put on a desirable project. I’ve read and tried to apply principles of sales and negotiations, and I very much believe that even a basic understanding of sales would benefit anyone. Most people don’t know anything about sales and don’t want to, which puts you far ahead of your competitors just by reading a book or two. It is also super valuable to realize when sales tactics are being used to pressure you and how to neutralize them.

What’s your work-life balance look like?

Excellent! In the early days it was a lot of work as I worked my engineering job full-time and spent my nights and weekends learning about, looking at, analyzing, buying, and self-managing my rental properties. I believed I wouldn’t be doing that forever, and I now that I’m on the other end it’s great!

About five years ago I began training a friend of mine how to manage my properties, and now we own a property management company together. It has been a win/win as he gets to learn from my experience while making money, and I don’t have to deal with tenants.

FI/RE has been all that it’s cracked up to be, I work when it interests me and have plenty of time to spend as I choose. We can step away from work any time we like, and usually spend a sizeable (and growing!) amount of the year traveling. The very best part is that we can be there for all the important family events, both our own children’s and the extended family.

Do you have any sources of income besides your career? If so, can you list them, give us a feel for how much you earn with each, and offer some insight into how you developed them?

All my sources of income are now disconnected from a traditional career. We currently own 20+ rental units which produce ~$12k/month, some of which we developed while working in our careers, but most came after I made investing my full-time job.

I’ll get into the story of how I grew my portfolio in the “Investing” section.

SAVE

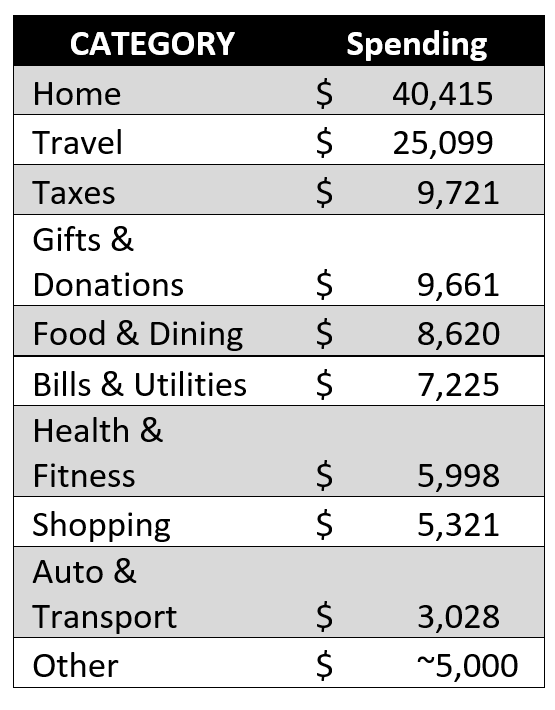

What is your annual spending?

We spent $120k last year, with a lot of discretionary spending.

What are the main categories (expenses) this spending breaks into?

Mint is not the most perfect form of accounting, but most categories are indicative of our normal spending habits.

Home is a broad category for the rentals as the payments have taxes and insurance baked in, but some rental-related expenses show up in Bills and Utilities.

Health and Fitness included some medical bills that (we hope) will not repeat.

Travel is exceptional because last year was our 10-year anniversary and we took an unforgettable trip to Hawaii with little regard for what anything cost. Worth every penny!

Do you have a budget? If so, how do you implement it?

When we were first married my wife and I were very budget-conscious (an accountant married an engineer – hello!!) and followed Dave Ramsey’s approach to money quite strictly.

As neither of us are natural spenders these days we have the budget standardized and review the previous month’s budget monthly, just to make sure nothing’s amiss.

We also do an annual review in January every year to make sure our spending matches our values.

What percentage of your gross income do you save and how has that changed over time?

We saved 19% of our gross income last year, which is (historically) a little low. Thanks to our naturally frugal natures, 20%-30% is more normal.

Looking at this statistic was a valuable exercise; I’ll be looking at this annually from now on!

What’s your best tip for saving (accumulating) money?

Having a purpose for savings is crucial, otherwise why bother? Whatever will motivate you enough to change your behavior is a good start.

When we set a goal to quit our jobs and travel the world, we knew we’d need to save up a nest egg. We budgeted, tracked, and charted our savings every month as a sanity check make sure we could actually do it. Nothing was more fun than updating our chart, because it meant once the “Savings” dot got above the “Quit Our Jobs” line, time to book the one-way ticket to Paris!

Learning to live on a budget was life-changing for us. Yes, it’s old-fashioned but there’s a reason that it’s been around for so long.

In order to meet your financial goals, you must first have goals and then know what’s happening with your money, otherwise it tends to disappear.

What’s your best tip for spending less money?

I think the single most important spending decision that will make many subsequent decisions easier or unnecessary is which house/neighborhood you choose to live in. If you max out your mortgage and buy an expensive house in a nice neighborhood, your 15 year old minivan will no longer cut it, time to get a $90k Tesla. You will feel compelled to add a $20k outdoor kitchen, a $30k pool, send your kids to a $50k/year private school, buy a $2k refrigerator instead of the $600 basic one, and on and on ad nausea. From this one decision springs unlimited spending and debt potential.

I’m experiencing the reverse of this currently. We live in an older neighborhood that is mainly renters and I’ve wanted to buy a Tesla model 3 since they came out. We sold one of our units last month and suddenly we can purchase my dream car, complete with full self-driving, in cash! Unfortunately, my Tesla would stand out like a sore thumb in our neighborhood, so we’re “stuck” with our perfectly functional 7 year old Honda, house with no mortgage, and cash in the bank to pounce on opportunities. Whenever Teslas DO become fully self-driving, all bets are off!

What is your favorite thing to spend money on/your secret splurge?

We love to travel!

We spend a month or two in the Caribbean every winter, and (Pre-Covid) travel internationally in the fall. Online school for the kids has been helpful for us.

INVEST

What is your investment philosophy/plan?

I am a real estate investor to the core. My plan was always to buy income-producing real estate, and I’ve rarely done anything else. Passive income is the most incredible thing in the world to me, and I have worked single-mindedly to obtain it.

I like to say that my first rent check changed me forever. I worked hard to find, analyze, and buy that one property, and I realized I’d receive a check every month, creating an income stream that stretches to eternity. Money that you don’t have to work for, what could be better!

In the beginning, my plan was to purchase just one property a year for the rest of my life. I still believe in that idea, but in the aftermath of the Great Financial Crisis opportunities abounded so I got more aggressive and bought as many as I could, as fast as I could. Eventually I started a company to purchase foreclosures at auction, gathered investors, and sunk our life savings into the first property. The recipe for our success has since been named the BRRRR Method, which stands for Buy, Rehab, Rent, Refinance, Repeat.

The key was to purchase at a price that would allow you to buy a property and fix it up and rent it out such that your total costs were less than you could refinance out of the property while making sure that the rent covered the mortgage. At the end of the process you owned a cash-flowing property with all your money pulled back out.

I was able to do that a lot when the housing market was terrible, and I acknowledge that I was both very lucky and a little bit good. The window of opportunity was open, and I took advantage, while still being conservative which is why I don’t own more. While there was risk in my approach, I made sure that I could financially survive any single project’s failure and always had engineering as a backup.

That will all sound like a fantasy to anyone trying to invest today and while the time for that strategy has passed (if you know where that still works, let me know!) I think there are lots of opportunities still out there in a different form. Personally, while I haven’t purchased any properties since 2018, I’m shifting to multifamily development which may have greater potential than anything I’ve done so far. According to the New York Times the United States has a housing shortage of 3.8 million units and I hope to have a tiny part in helping solve this crisis and make some money along the way.

Hopefully when a few years have passed and I do my Millionaire Update this thesis will have borne out. Stay tuned!

What has been your best investment?

My very first investment was a 4-unit apartment building that I purchased for $125k ($6k down, with homeowner financing) back in 2011. My wife and I lived in one of the units and rented out the other 3, which paid the mortgage and enabled us to live rent-free.

This year we anticipate grossing $39k on that same 4-unit property, for a yearly return of 31% unlevered (return on purchase price), and 650% levered (return on down payment). People may squabble about calculating IRR and equity growth, vacancy, maintenance, management, etc., but no matter how you slice it that’s going to be a good investment.

Many of the foreclosures we purchased using the BRRRR method technically have an infinite return due to my basis being $0. Since their cashflow is lower I count my “best” investment as the one that’s made the most difference financially. That first purchase was the springboard into being able to save the money to buy the rest.

What has been your worst investment?

Messing around with picking individual stocks, I have been burned to the tune of 20+% losses on a couple of occasions. I know the smarter approach is to stick with index funds but stocks bring out the speculator in me.

Observant readers will note that I still have some money in stocks, I guess I haven’t learned my lesson yet! Luckily I recognize my risky nature, and never invest any money I can’t afford to lose if things don’t work out.

What’s been your overall return?

Thanks to amazing appreciation AND rent growth of the last few years, the IRRs (internal rates of return) on my properties range from 15-30%.

I don’t focus on percentage returns much since I invest for cashflow, but I think IRR is the most appropriate for my situation. I’m not the accountant in the family!

How often do you monitor/review your portfolio?

We like to sit down and do a basic review of our portfolio and cashflow situation once in September after the bulk of the leases are renewed and rents are finalized, and again in January for a deeper dive.

NET WORTH

How did you accumulate your net worth?

Our net worth has been the result of a good choices, time, and some luck.

When we began investing, we envisioned buying rental properties over time until the income from the rentals was enough to replace our day jobs. As I gained experience and education (I’ve read A LOT of books about real estate and continue to read about one a month) we were able to instantly recognize good deals and snatch up properties quickly, which drastically sped up our plan.

The market during the recession was such that there were plenty of deals to be had if you were looking for them.

We hit our FI/RE number before we were aware of the acronym, but my wife continued working because (pro tip for FI/RE fans) banks over-scrutinize the self-employed and her W-2 allowed us to easily get financing and continue buying properties.

After purchasing the rentals we were satisfied with a good base of income and a decent net worth, but could never have predicted the wild real estate market we’ve experienced. I’d always read that real estate was the ultimate hedge against inflation but I understand that on a vastly different level now. I worry about the effects it has on the country as a whole and feel terrible for the people whose income, savings, and wealth are being destroyed through no fault of their own.

What would you say is your greatest strength in the ESI wealth-building model (Earn, Save or Invest) and why would you say it’s tops?

When working, I feel we were above average at earning (relative to our career level and peers), and good at investing, but I think the real strength was in the Save portion of the model. Had we not been able to manage our personal finances well early on, we never would have been able to invest at the level we have. Control of our finances was the basis of everything else, and we have friends whose incomes have always been multiples of our own but never seem to gain traction financially.

People see amazing, million-dollar opportunities pass them by because they don’t have the savings to take advantage of them, and I (and ESI readers) don’t want to be among them.

What road bumps did you face along the way to becoming a millionaire and how did you handle them?

Graduating when I did (2009) was certainly no blessing at the time, as unemployment for new college graduates was officially 25% but certainly much higher if you counted graduates working outside their specialties. For me personally unemployment was 100%!

Those were dark days as I watched my bank account dwindle into the low 3 digits with time passing, the economy sucking, and my grandparents losing almost a third of their retirement. I was able to start a few small businesses that kept me alive, but definitely not thriving. I called my father and he made it plain to me that I couldn’t move back home. Tough to hear but amazing parenting and the right decision. Fortunately I found a roommate situation where rent was only $185/month for a shared room. I’ll never forget the crushing feelings of being broke and nearly hopeless.

This situation eventually turned as I was able to get the job installing alarms and then the real job as an engineer. The 8 months of being unemployed after college were my Scarlett O’Hara “I’ll never go hungry again” turning point that taught me that I could survive on almost nothing and how to make every dollar count. I’d have preferred to learn those lesson a different way, but that’s not usually how life works.

We have also had difficulties arise with the rentals, and early on had a day where a fire knocked out our first apartment building and pipes froze at our other property on the same day, a 100% loss of our rental income in 24 hours. Thankfully we were in a conservative position with our debts, had a cash cushion for emergencies, and good insurance that eventually covered most of it, but it was still stressful. My dad taught me to allow for the possibility of the worst-case scenario and make sure you can recover if it happens, and it sure paid off that day.

What are you currently doing to maintain/grow your net worth?

We’ll likely never sell any of our rentals and if a housing crash occurs we’d take some paper losses, but thanks to our conservative position we’ll be fine even if values/rents somehow fell by 50%. We’re also in the early stages of becoming developers, which will allow us to grow both our net worth and passive income, depending on what we decide to do with the units.

I’ve also considered syndications but haven’t made the jump yet.

Do you have a target net worth you are trying to attain?

Net worth for us is a byproduct of investing for income but I think it would be cool to be a decamillionaire ($10M) someday!

How old were you when you made your first million and have you had any significant behavior shifts since then?

Surprisingly we achieved millionaire status only in 2019, then multimillionaire in 2021. If the housing market continues going gangbusters, we’ll be at $3M in the spring of 2023, which is wild. 30%+ property appreciation compounding yearly is crazy!

I would say our behavior hasn’t changed much; we do spend more on travel with less heartburn which is nice!

What money mistakes have you made along the way that others can learn from?

Risk management has been key to my success because like everyone I’ve made my share of mistakes and continue to do so, but I’ve made sure to never risk more than I can afford to lose.

When I was first starting out I got involved in options trading and unfortunately for me experienced a lot of success, tripling my (small) trading account from $3.5k to $10k one year, and then doubling the next to a high water mark of $20k. At that point I thought I was the best trader in the world and promptly proceeded to lose everything during a “Melt Up” of SHLD (I was holding “Put” options) in early 2012 and made it out with $1k, a 95% loss from the peak.

Though my “actual” losses were small they felt enormous. I imagine many crypto investors understand what I went through. It was a humbling, expensive, and necessary experience and since then I’ve tried to better recognize and mitigate risk.

If stocks are your thing don’t be a hero and don’t assume that you are special and different because you aren’t, and success is likely just fleeting luck. Learn and follow the classic rules of risk management, diversification, and when in doubt (which should be often) go for the old-fashioned long term buy and hold of low-cost index funds.

I no longer invest in stocks but do speculate on occasion with very small amounts. What I understand is real estate that produces cash flow, and now I try to stick to that.

What advice do you have for ESI Money readers on how to become wealthy?

- I cannot overstate the importance of being on the same page as your spouse, with finances as with everything. Wealth can be obtained by anyone but requires dedication, hard work, and sacrifices. The path is difficult if only one of you really wants to make that journey, and near impossible if the most important person in your life is actively working against you and/or begrudges the efforts you make to get there. For people who are not yet married I would suggest serious conversations about money and your vision for the future prior to marriage. For married people, do whatever it takes to decide on your financial priorities as a pair, because you and your spouse working towards the same goals is one of the most powerful things in life and can get you to wealth faster than you imagine. Divorce, however, is absolutely devastating in all regards, the number one destroyer of wealth, and something I wouldn’t wish on anyone.

- Financial education is of critical importance. Several studies of millionaires reveal that the vast majority came from average backgrounds, are self-made, received little, if any, inheritance, and yet achieved great wealth. What made them millionaires is how they think and view the world, which are skills that can be practiced and learned. Best of all is how many successful people have written books (and excellent interviews on ESI) explaining what they think, the decisions they faced along the way, the actions they’ve taken, and the wealth formula that worked for them, and you can learn from them. I’ve read hundreds of books and blogs about money and am always on the hunt for the next book that can change my thinking, and thus my life.

- Building wealth is more about what you keep and invest than what you earn. Yes, it is very helpful to have a high income and you should do whatever you can to maximize your earnings, but you can always outspend your income. My sister’s business partner has earned $500k+ per year for over a decade. She recently went through a divorce where it was revealed in court that her and her now ex-husband actually had a negative net worth by several hundred thousand dollars. The lesson: someone making $50k/year and spending $45k/year would be better off financially than a high-earner who spends it all. Additionally, if the lower-earning person invested that same $5k a year into a Roth IRA from age 25 to 65 and achieved a market-average 8% return, they would retire with $1.5M tax-free.

- Investing in real estate has worked well for me and I also appreciate it’s not for everyone. In my mind the formula is simple, no matter which path you take: buy assets, avoid liabilities. I have considered dividend stocks, syndications, storage units, and other forms of passive income and so far rental real estate is the best asset that I can come up with. I’m open to other ideas though!

FUTURE

What are your plans for the future regarding lifestyle?

Our lifestyle is fairly optimized already, but I’m of the opinion that more income is always better.

We have already “retired” early and are just going to keep the course. As our income grows, we may travel more but we also like where we live and are close to family, so it’s hard to envision big changes.

We will probably spend more time traveling or even buying a second home as we get older; winter seems to get less and less fun every year.

What are your retirement plans?

Retirement is a nebulous term for us since we currently work because it’s fun, not necessary, and can step away for any amount of time when we choose. Financially I imagine we will always try to take advantage of opportunities that interest us and grow our businesses.

We enjoy spending time together doing outdoor activities, and spend much of our summers camping, hiking, and kayaking. In the winter we love to ski (both cross-country and downhill), snowshoe, and stay active.

Personally, I enjoy racquetball, pickleball, and long-distance running, and am aiming for running a marathon next summer before I turn 40. I don’t know if distance running is sustainable long-term so I’m trying to do it while it’s possible. No time like the present!

Are there any issues in retirement that concern you? If so, how are you planning to address them?

Like many, the cost of health care is a concern but not a major one. My assumptions are that since we are fairly young and have low healthcare needs and our sources of income tend to match or exceed general inflation we should be ok.

Inflation is on my mind a lot these days but I don’t know how to combat that other than being invested in real estate.

MISCELLANEOUS

How did you learn about finances and at what age did it “click”?

I was raised by a very financially conservative father and a very financially liberal mother (they divorced when I was very young), and as such got to experience the extremes of the money spectrum. Though we grew up poor, from my father I gained an appreciation of the value of every dollar and from my mother I learned that life is about more than money and that it should be enjoyed. It’s been up to me to split the difference and I’m grateful to both for the examples they gave me. Interestingly it was my mother who gave me a copy of the book “Rich Dad, Poor Dad” early in college, which gave me the roadmap that I have followed since.

Whether it’s a product of nature or nurture I’ve always found it fairly easy to live on less than I make. I have augmented that by learning about money, business, and personal finance and will be a lifelong student of these subjects.

Who inspired you to excel in life? Who are your heroes?

My parents inspire me, because though they had a universe of differences, the one commonality that I never doubted was that they loved my siblings and me and tried to do what’s best for us. They both made unbelievable sacrifices to raise functional adults and I’ll always be grateful for that.

I had a teacher in the 7th grade who loved life, believed in the potential of her students, and taught with passion. She believed to her core that her group of 12-year-olds not only could accomplish anything but owed it to themselves and the world to do so. Her belief in me and the things she taught will be a part of me forever. Looking at the job educators have to do and how little resources they’re given to do so fills me with profound respect for anyone who can make it in that field.

My wife continues to inspire me to excel in life with her patience, support, and intelligence. I love being able to talk to her about my ideas and get wise and valuable feedback. I frequently tell family and friends that she’s better at business and real estate than I am, what a lucky guy!

Do you have any favorite money books you like/recommend? If so, can you share with us your top three and why you like them?

I’d love to break new ground here, but the classics are classics for a reason! I re-read all of these books yearly and recommend them frequently:

- Thomas Stanley’s “Millionaire Next Door.” This was the first book I read that took a quantitative, statistical approach to Millionaires and their behaviors. It was eye-opening to see what makes the average millionaire and it has informed my decision-making ever since. The greatest value was it made me believe that millionaires are like me and that if they could do it, I could too. It is fun to now be a millionaire next door!

- 2) Dave Ramsey’s “Total Money Makeover.” Dave has a simple system to help people get control over their money, proven out by millions of people over decades. What I find especially valuable is his grasp of people and psychology, and he understands that personal finance is about thinking and behaviors, not numbers. According to a recent article by CNBC which is consistent with other research, 58% of total Americans are living paycheck to paycheck, along with 30% of those that make more than $250k per year! Personal finance skills are crucial at any income level, and this is the best book I know of to provide those to people at square one, which is most people. While I believe there is such a thing as good debt and disagree with his approach to retirement, the fundamentals are indisputable, and I think everyone could benefit from something in this book.

- 3) Robert Kiyosaki’s “Rich Dad, Poor Dad.” I have a fondness in my heart for this book because it’s principles kick-started my financial journey. His ideas of assets vs liabilities, cash flow patterns, and passive income have come to define not just my thinking, but my approach to income and investing. This book is an amazing starting point into the world of money, but only one step on a long journey.

Do you give to charity? Why or why not? If you do, what percent of time/money do you give?

We try and donate 10% of our net income to our church to start, but also give time and further donations to causes we believe in. It is sometimes difficult to calculate what that 10% should be with an income derived from such a multi-variable source as rental income (should we tithe on debt reduction? Do we deduct taxes? Depreciation? etc.), but I’ve come to believe that the struggle to understand is part of the value of the tithe.

It is important to me to be able to give to demonstrate that wealth, while nice, is not the purpose of my existence and that I can let go. Generosity is healthy for the soul, and key to happiness.

Do you plan to leave an inheritance for your heirs (how do you plan to distribute your wealth at your death)? What are your reasons behind this plan?

We’ll probably do a basic split between the kids, but we’ve also talked about trying to spend most of it before we die to allow the kids to develop their own lives.

So far as I can tell there’s no perfect answer to this problem.

Great share here. You are doing it – the evidence is clear. Congrats on understanding that RE is the dominate asset class and systematically working toward an early retirement.

I chuckle when I see return between 15-25%. Absolutely ! Try that with equities.

Best of luck in the future. I predict that you’ll be a decamillionaire by 55.

Refreshing read for sure.

Thank you for the compliments from one RE guy to another!

Many people are scared away from active RE investing but it’s the best investment I know and the positive aspects (retiring ~30 years early, freedom to use my time mostly how I choose, accelerated NW growth) have massively outweighed the negatives (stress, hassle, risk). It’s been a journey but one I would do again every time vs the alternatives. 15-25% works for me!

Have you stuck with the investing plan you outlined in your interview? SFRs are hard to say no to but I’m curious if you’ve gotten into syndications or apartments.

to be fair to equities though, you can rock 10-12% with no vacancies, no chasing deadbeats for rent, no CDC-mandated rent moratoriums, etc….

Congratulations on your success at such a young age and taking advantage of the real estate market over the last 12 years. So many things were aligned to make it a great time to invest. Kudos that you were well read and prepared to recognize the opportunity.

You are very smart to take the time with your family while you are young, you will never regret that.

All the best to you and look forward to hearing how things work out for you in the future.

I too appreciate the simplicity of property investment. We got started after reading ‘Building Wealth Through Investment Property’ by Dolf de Roos & Jan Somers. That’s a how to guide. Then Dolf wrote Real Estate Riches as part of the Rich Dad series. That is more of a feel good book but it still has great advice. We lived in Hong Kong which is some of the most expensive real estate in the world but Roos simply suggested buy somewhere else with his ‘Yes but’ advice. Both good for your monthly book read.

Yes I have similar sentiments about my own market (South Africa – more of a scared of the economic trajectory) – do you think that one can do it elsewhere far away (not exactly close to any decent markets)? Or just invest into the US via RE private equity, instead of going direct?

Second question – is RE feasible with volatile floating rate mortgages or aim for fixed rates only to have cash flow certainty?

I’ll check them out, I’ve read Dolf’s Rich Dad book but not the other. I appreciate the recommendation and knowing that you can still invest in crazy expensive times and places, which seems to be everywhere now!

To be sure I certainly caught a couple of waves just about perfectly. I’m sure everyone feels the same but I wished I’d started a few years sooner!

As I mentioned I felt my plan would get me to where I am but never thought it would have happened so soon. Thank you for the words about preparation, I’m trying now to get in front of the next opportunity. It seems like we live in a time when more wealth is being created faster than ever.

Spending time with the family has been an amazing journey already and will continue to be so. That I did is the result of believing kindly offered words of people much smarter and more experienced than I. I myself am not that smart but fortunately I know how to listen to those that are!

hello , solid write up. You guys are on the path to a solid financial future. Slow and steady is going to get it done. Do u guys have any tax deferred funds? Any 401ks/IRA/Roths? sorry if I missed it…lots of wiggle room to use leverage to scale up, but I like ur take on being conservative. How did u finance ur properties? Keep going . I also see u reaching ur goal of $10M+. Wonderful

Nothing tax deferred yet, I own a ROTH but since RE is my investment vehicle, I don’t contribute regularly and haven’t seen a compelling way to make it work with RE. I have come across RE/ROTH ideas from time to time but they always seem too complicated. Do you know of a way to make ROTH work well with acrive RE investmen

As for financing, the BRRRR method described here (and better at Bigger Pockets) allowed me to snowball and reuse the funds I had.

Great interview! I live nearby to you in Joseph, Oregon. If you would like , we could meet sometime.

Well done! Nice to read about success after all of your experiences. I’m one who shy’s away from RE as I am not interested in managing it, but appreciate reading success stories for those who do.

I do plan to look at RE syndicates a bit closer.

Curious, you said you were expecting to hit the $3M mark in spring this year. How’s that goal looking for you?

Thanks for the kind words and keeping an open mind, I thinks it’s good to learn from everyone even if (or particularly if) their views don’t perfectly match yours. I don’t blame anyone for not wanting to manage properties, which is why I eventually started my own (hand-off) management company. That’s the biggest piece of the RE puzzle in my opinion.

$3M+ is on track, one of our projects is currently listed with a broker and when it sells will put us over the top. Fingers crossed!

How many millionaire interviews are there if you exclude landlords?

Not sure. I don’t track that.

But most millionaires (like me) would have reached that level without real estate. And most millionaires (like the ones in MMM) own more stocks than real estate.

Great job! Make sure you join the MMM forum (Millionaire Money Mentors) if you haven’t yet.

“We live in an older neighborhood that is mainly renters and I’ve wanted to buy a Tesla model 3 since they came out. We sold one of our units last month and suddenly we can purchase my dream car, complete with full self-driving, in cash! Unfortunately, my Tesla would stand out like a sore thumb in our neighborhood, so we’re “stuck” with our perfectly functional 7 year old Honda, house with no mortgage, and cash in the bank to pounce on opportunities.”

We call this stealth wealth … we don’t like to attract attention.

Had another RE investor buddy, who drove his 2-seater Mercedes to sketchy neighborhoods to pick up his rents. I thought he was loony. Hope he hasn’t been carjacked!

Well done! A few questions about your RE portfolio performance as you transitioned out of work.

It sounds like you had 6 properties when you quit your job, including the 4-unit apt building. Could you share the following numbers if you know them?

1. Your total rent roll when you quit your job.

2. Your net income per month after expenses, finances, and fully funding reserves when you quit.

3. The amount of $$$ in reserves per property when you quit.

We are closing on our fifth property soon and are building a timeline to retiring early or going semi-retired. Trying to figure out where we’ll feel safe doing so. Thanks!

PJTransport – Glad my story could be useful to you on your journey, congratulations on getting to 5 units. I’ve heard it said that almost no one has just one rental unit, they either try and quit or continue on to own many units. Seems like you’re on the latter path.

With the disclaimer that I’m just a random dude on the internet and am not qualified to speak to your personal financial situation, I can give a simplified answer to your question. When I quit my job my wife was still working and between her income and the rental’s income, we could cover our expenses and still save about $1k/month. We also had about $25k in the bank. It was a leap but not a crazy one, hopefully it came across in the interview that I’m a pretty conservative guy but will take risks occasionally when the payoff is high enough.

Your situation will of course vary, but seems like you’re on the right path, keep it up!

Also keep on eye out for my upcoming Retirement Interview, coming out on this sight in the next couple of months (May, if I remember correctly). That will cover your questions in greater detail.

Thanks, ApartmentGuy, your handle and your interview are both awesome! Haven’t joined the MMM yet but look for me in the next few days. Looking forward to getting to be a part of the community!

Mercedes to collect rent, wow, that’s one way to go! Stealth wealth certainly fits our lifestyle and personality, but to each their own!

Looking forward to seeing you in MMM. Awesome interview. Enjoyed this one a lot. I am interested in RE but a little ignorant and haven’t been bold enough yet. Kick myself for a few missed opportunities right after college when I had roommates that could pay my mortgage. Do you have RE specific books to start with? TIA.

Rob-

Thanks for the kind words, I tried to tell my story in such a way that it would inspire people like you. I remember trying to get started and feeling overwhelmed and not ready, and I still wasn’t when I got started. I will tell you that I learned more (deeply) in my first year of being a landlord/investor than from the books I read but the books also helped me get started and gave me something to turn to when I needed help.

There’s a few I really like for beginners:

1) Mike Summey’s Weekend Millionaire series – good system, really breaks down how to get started

2) Landlording on Autopilot by Mike Butler – a lot of the nuts and bolts – contracts, advertising, dealing with tenants, etc.

3) Rich Dad’s Guide to Investing – good theory, mindset, how to analyze and recognize deals

I’m still learning, and still read RE/business books all the time. There are a lot of great recommendations from ESI!

Thanks for sharing! We also do an annual review of our budget and spending to ensure they align with the calling of the Lord on our lives and values in line with it.

Not sure if you’re still reading comments related to this wonderful post, but would you be willing to share more about how you educate your kids while spending winters in the Caribbean? We want to do just that, but don’t know how to get started. We want the best for our 5yr old, but we really want to escape the harsh Midwest winters too! Thanks in advance.