As noted in My Third Experience at a Direct Mail Retirement Seminar, my wife and I accepted an invitation to meet with Dustin (financial planner) and Gregg (Chief Investment Officer) from Accelerated Wealth.

As noted in My Third Experience at a Direct Mail Retirement Seminar, my wife and I accepted an invitation to meet with Dustin (financial planner) and Gregg (Chief Investment Officer) from Accelerated Wealth.

They had done an impressive enough job at the presentation to convince us it was worth an hour, plus I had a few questions I wanted to run by them, so why not? In addition, my wife and I had each received a free 8-count nugget offer from Chick-fil-A and there was one near the Accelerated Wealth office, so it was cheap date night afterwards. 🙂

BTW, our neighbors four doors down (who we sat with at the event) made an appointment with them as well. It happened a couple hours before our appointment.

The next day I ran into the neighbor while he was headed out to his car (I was walking back from playing pickleball at the gym) and we chatted about our meetings. More on that at the end.

Arriving at Accelerated Wealth

Our meeting was on Wednesday, January 22 at 2:30 pm.

My wife was at church for meetings. Since the church is closer to the offices than our house, we agreed to meet there.

It was a 15-minute drive from our house and I arrived at 2:20 pm (I hate being late).

Their building is very swanky and in an affluent and growing area of town.

I walked in and was greeted by two nice ladies at the front desk. They offered me something to drink and I took coffee. Free coffee is a big plus IMO! Ha!

While I sat on the couch in their reception area waiting for my wife, one of the ladies brought over an information form and asked me to fill it out.

As she handed it to me I told her I would look it over, but if the information was more than I wanted to share, I might not fill it out.

Sure enough, they asked for all sorts of personal and financial information that I didn’t want to share in that format. I’m sure most people show up unprepared and the sheet/information gives the planners something to review.

But you know me — I was prepared. I had a detailed summary of our financial information assembled and ready to share.

I told her that at this point we were just getting to know them and would be deciding if we wanted to proceed or not. The information requested was for a later meeting if we wanted to proceed.

She said she understood and took the form back.

Soon after, Gregg came out and said hi to me. He said he’d be back out when my wife arrived. She arrived soon after that and we all headed to a back conference room.

Reviewing Our Information

The four of us got settled around a conference table and chitchatted a bit. I told them I had a handout that summarized our financial situation as well as had questions listed so we decided to begin there.

The handout contained information on it that I’ll soon publish here in my annual financial review, so I’ll just give you the highlights now so as not to spoil that post:

2019

- Me – retired from marketing career in August 2016; now 55

- Wife – works part-time at church; now 58

- Income: $204,721

- Expenses: $119,475

2020 Forecast

- Income: $130,090

- Expenses: $91,310

2020 Details

- Not counting dividends in income since we reinvest those.

- Lower website (sold one site) and rental income (banner year last year).

- Expenses are lower since both kids are now out of the house.

- Expenses include $18k of vacation/travel costs.

Net Worth: $4,502k

I broke out the key parts of net worth as well to give them insight into where our assets are.

Then I listed my questions as follows:

- What is the best time/strategy to take Social Security?

- Any thoughts on planning for RMDs?

- What is your perspective on LTC insurance?

- Is there any simple/effective way to turning investments into income generators?

We discussed the numbers for 20 minutes or so. They were very complimentary of the job we’d done managing our money.

We also talked about our background in financial coaching, writing, etc., so they knew we had a pretty good understanding of our finances and how money works.

Discussing the Questions

The heart of the meeting was going over our questions. What follows is a general paraphrase/sense of what occurred. I did take notes and am writing this post two days after the meeting, but I could have missed or misunderstood some things.

In other words, this isn’t a verbatim transcript ready to be accepted as sworn testimony in a court. It’s my recollection and perception, so reality could be a bit different.

What is the best time/strategy to take Social Security?

At the presentation it was mentioned that Dustin is one of only two people in Colorado Springs that’s a certified Social Security advisor, so I had the chance to hear from someone who really knows what he’s talking about.

We explained our work situations: my wife had a decade or so of work and then nothing after that. I paid the maximum to Social Security for most of my career.

He asked me what we thought we should do and I said:

- Have my wife take her Social Security at her full retirement age (which is 67).

- When I turn 67, I take my Social Security and she claims half my benefits.

We had some discussion around this but it’s basically what he said he would recommend.

BTW, he also said he’s fairly bullish on Social Security and doesn’t think it’s going away any time soon, especially for those 55 and older. Yes, there could be changes but probably not massive for the older crowd.

Finally! There’s an advantage of being older. 🙂

Any thoughts on planning for RMDs?

This was a big part of their presentation, so I knew they had something to share.

BTW, we’re sitting on a mountain of RMDs.

If you look at this PDF from Fidelity, you’ll see that at 72 (when we’d be forced to take RMDs), our life expectancies are 25.6 years.

If you take $2.5 million in assets we have in IRAs and divide them by 25.6 years, that means our RMDs will be close to $100k per year.

This of course assumes there’s NO asset growth in the next decade and a half when we turn 72.

Dustin reiterated that he’s paying as much taxes as he can now with the intention of not having to pay them at all in the future.

He discussed something they called “super Roths”. From what I could understand, it’s permanent insurance with high cash value and a low death benefit (designed to maximize cash value so it’s more of an investment and less of insurance) that allowed you to grow your wealth tax free.

That’s a very simplistic explanation, but we only had about five minutes to cover it, so that’s my level of understanding currently.

Of course at the mention of permanent insurance the warning alarm on my checkbook started to go off big time.

Dustin says he has three of these policies and uses them to shelter money/investments from future taxes.

They said it was a great way to pay taxes now and avoid them later.

We had the discussion about no one knowing if tax rates will actually be lower in the future, but that didn’t go far because…no one knows.

We then moved on to the next question…

What is your perspective on LTC insurance?

I’m working on a post (it will probably be a two-parter) on long-term care (LTC) insurance so I was pretty up to speed on the topic. That said, I wanted to know what they thought of it.

Dustin said “you can’t afford not to have it.” This is the answer I expected. Didn’t someone once say “never ask an insurance agent if you need insurance?” Ha!

I asked him about the prevailing guideline of people with net worth in the middle ranges needing LTC insurance — that those at lower net worths don’t need it because eventually the government takes care of them and people at higher net worths ($2 million+) are self-insured.

He said “you insure your home and your car though you might be self-insured, why not your long-term care?”

This is a good point in some respect. We don’t see people advocating cutting home and auto insurance and self-insuring, why would we think we’d do it for LTC?

After I thought about it, I came to this conclusion: I don’t really insure my home and car for the replacement costs of either because I am certainly able to absorb the hits if either of those needed replaced. The main value is the liability coverage for each (especially the car) in case I’d need it. I also tack on umbrella insurance for just this reason.

In addition, the various factors might make home and auto insurance a “better deal.” You need to look at cost of each, the odds of needing them, and what they cover if you do need them. I’ll sort that out for LTC insurance in the posts I’m working on.

That said, they recommend using the same (I believe) super Roth/permanent insurance as a way to cover your LTC costs. It is a better way in their opinions to handle the cost. It may be as LTC insurance is both pricey and some companies are pulling back on coverage. But if you own an asset that pays for LTC, you control it.

That said, I already own assets that could pay for LTC, so why do I need a new one?

Obviously I don’t understand everything at this point since we covered it quickly and it’s pretty complex, so maybe I misunderstood.

To round out my questions, we did talk about the income question a bit, but since 1) there’s no great way to generate safe income these days at the 6%-8% level and 2) I was asking it more just for curiosity sake as I don’t really need the income, we didn’t waste much time on it.

Considering Another Investment Option

After we made it through my questions, Gregg wanted to talk about investing.

By this time they had a great feel for who I was — that I favored passive funds, low cost, etc.

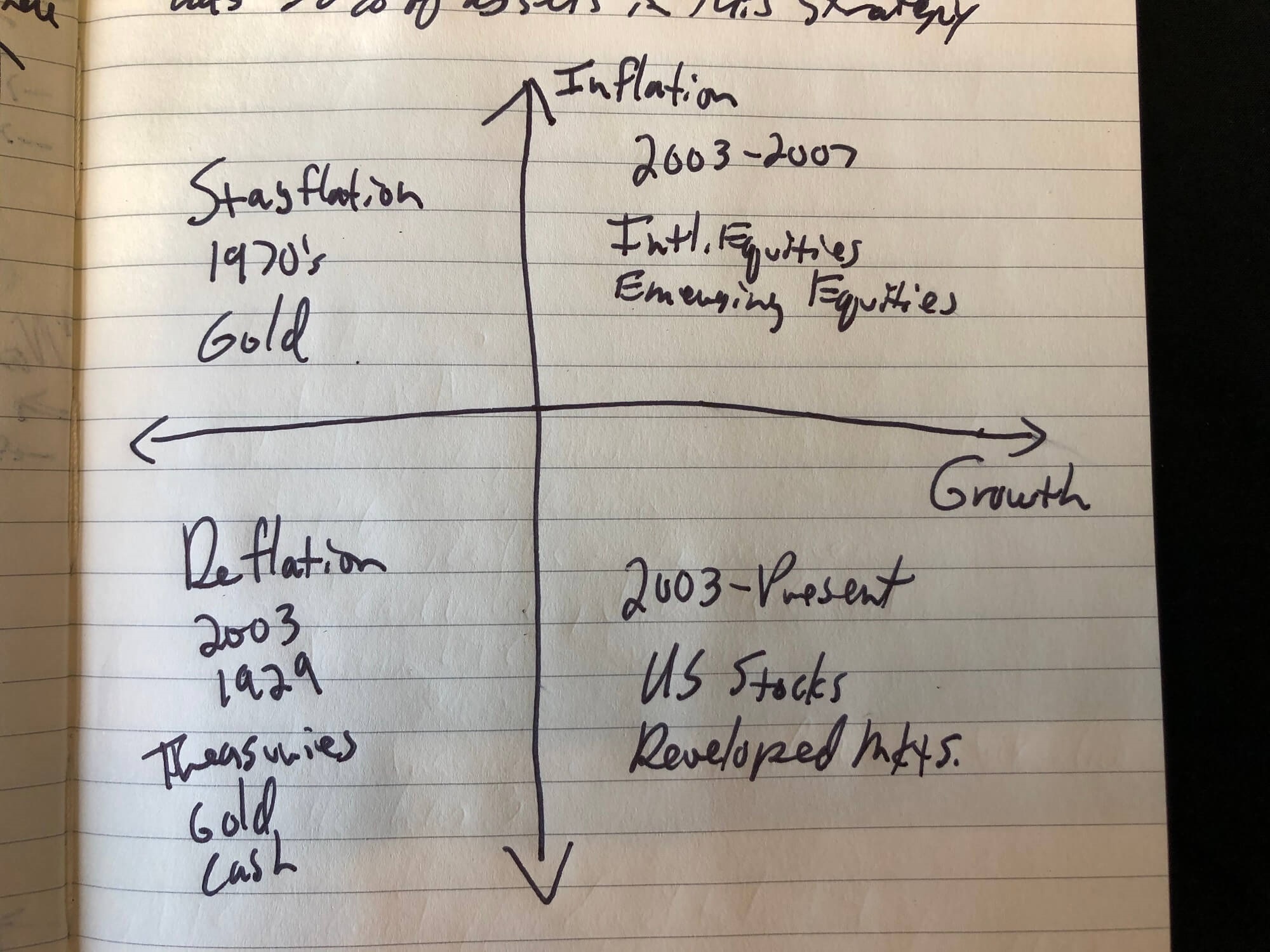

Gregg said he wanted to point something out and drew this picture…

My drawing isn’t the best but hopefully the meaning comes across.

He said that over the past decade our portfolio of all equities (U.S. and international) was tailor-made for what happened in the market (because life has been lived on the right side of the graph). It was almost the perfect set up for the rapid growth we’ve seen.

That said, while no one knows what the future will bring, it’s highly likely that the go-go days won’t last and the economy will move to the left side of the graph.

As such we might want to consider a managed fund that “pays for itself in spades” (I had told him I wasn’t excited about active management or their associated fees) to invest our money in a way that the market calls for.

He didn’t tell me what the fund was, but the idea is that the manager moves your money to the proper market sector based on the economy. This supposedly protects you in case of a downturn and still gets you most of the gains in good times. In other words he moves the asset allocation based on the market we’re in to cut losses and manage upside.

It’s a simple concept and sounds compelling, but can anyone really pull this off consistently?

Gregg’s suggestion was for us to carve off at least some of the $2.9 million we have in stock index funds (including taxable accounts) and put it into this fund for protection in case the market turns south. His words were something close to “a prudent move would be to diversify the investments you have.”

He said the guy’s methodology was “super impressive” and that he (Gregg) had “50% of his assets in this strategy.”

I got zero details other than that — not the name of the fund, the manager, anything on costs, etc. We didn’t have time for it.

As you might imagine, I have a gazillion thoughts on this. I’ll lay out the key ones and let you chime in with your take:

- It is true that my portfolio has been “the right thing at the right time.” So far, I’ve ridden a pretty good wave the last several years. Of course I had to bite my fingernails and hold fast in 2008 and 2009 when most others were jumping ship, so those gains came after a lot of second guessing myself but still holding the course.

- It is likely (though no one knows) that the market is in for some rough times in the next several years. This could be sped along by our upcoming presidential elections depending on who gets elected.

- I still have a long-term outlook. At the rate we are going now, I will NEVER need the funds we’re talking about. So why not let them sit and ride the market out for the next 20 or 30 years? Even if it tanks, it’s likely to come back up again.

- As I discussed with the guys, I’ve won the game so do I really need to keep playing? In some respects what they are recommending keeps me playing the game. But in other respects it’s basically holding with what I have and not playing (just trying for protection).

- Gregg said something like “these are the moves wealthy people make.” This could be true and it could be something we need to do as well. Perhaps this is an option above my current level of expertise because I’ve never been wealthy before. 🙂

- I’m guessing that the fund they use has very high expenses which isn’t my style at all. Liquidity might be an issue as well, but I don’t know.

- Can I do what they recommend myself? Do I want to?

We’ll get to your thoughts on all this in a moment.

Finishing Up

As the meeting started to wind down, they suggested a follow up meeting where we could get into details of the super Roth and the investment option.

I told them I’d consider it and get back to them.

I asked about any costs for the follow up and they said there would be none, so I’m leaning toward going. But I’ll let you help me decide that…

They then gave me a copy of a book titled “Retirement Confidence” written by Chris Abeyta, one of the company’s owners, as promised at the presentation. Gregg said he thought I probably wouldn’t get much out of it as it’s written for someone with a lower level of financial understanding. But you know how much I love to read, so I took it! 🙂

So what do you think — about the super Roth idea, what we should do (and why) with our investments, where the market is going, paying taxes now versus later, and, the big question, should we take another meeting with them (I’m thinking why not, but maybe there are reasons not to)?

A Few Follow-ups

Here are a couple things related to the topic that I wanted to be sure and cover:

- I asked them why they didn’t turn their radio show into a podcast. The short answer: it’s not a priority for them. They have more than enough business and don’t really need extra marketing. Of course they are still doing seminars so…

- My neighbor told me he has four additional meetings set up with them (all free). He doesn’t have as much leeway with his finances as we do and can’t afford to lose 50% of his investment value because he’s in the retirement red zone. My guess is that they pitched him the same fund they shared with me, but I’m not sure. We’ll probably compare notes if we proceed.

Comments?

An interesting read and on the short side, if you have “Won the Game”, why are you still playing? As to Long Term Care (LTC) several of my previous financial advice providers all pushed me to NOT take it , but to build my portfolio to provide a “safety net” in the event a need arises. Chances are, should the need arise for LTC, my chosen executor would draw down funding, as i would be incapacitated and not aware of reality. Each situation is certainly different from the other but i believe that LTC coverage is not a good thing, and that there are better solutions and strategies to help people get through their needs.

Thank you for doing this for us, we learn so much. I had to google Super Roth and this is what I learned…..Indexed universal life insurance is often known as a “Turbo ROTH” or a “Super ROTH” because it shares many of the characteristics of a ROTH 401k—after-tax money goes in and tax-free money comes out—yet there are no IRS contribution caps, so you can contribute as much as you want to your Super ROTH.

We have a term life insurance and a Universal (whole) life insurance policy, so I guess I could consider that my Super Roth or even my LTC insurance.

Thanks for taking the time to write on this subject! This was a particularly interesting article and very relevant to my situation since we are about the same age (I’m a bit younger, 51) with very similar net worths and exposure to the market. Additionally, we appear to have similar investing philosophies (low fees, index investing, minimal insurance except for liability, etc.) and we have similar questions about the future.

I look forward to reading more about the investment/insurance vehicle they are suggesting. From what you describe it feels like an annuity or something similar. I have avoided annuities due to bad press and my feelings on fees but maybe there is something I have missed in my analysis of these products.

LTC is an interesting one at this point in my life. We recently put my inlaws into a care facility, a tough decision but what we believe to be right in our situation, and the LTC insurance they bought when he retired is a godsend. We have been drawing on the benefits for less than a year and I believe it has already paid for itself. It takes a bit of work to jump the hoops to start drawing the benefits and monthly followthrough to keep the checks coming but it is better than having to deplete our inlaws modest estate to cover their LTC. That being said, I am not sure it is required for the wife and me since we have a larger estate and no children so self-insurance seems to be the right answer but we continue to look at the options.

Thanks for all you do, I look forward to following the rest of your retirement seminars and planner adventures. The only guarantees we have are the fact that none of us get out of this thing alive and we cannot take it with us.

Very interesting read.

Did they disclose how they get paid? Giving away free follow up meetings seems to suggest they either get compensated by AUM or are commission based which puts you in high front loaded funds.

I personally will self insure for LTC. Their argument about trying to compare it with home and auto doesn’t fly with me. LTC companies are at much higher risk of going out of business by the time you need it decades later. Plus a lot of companies realized how expensive it is now and have pulled back as you mentioned.

Did not disclose how they get paid. Haven’t gotten far enough to ask, though I would at some point for sure.

Did you review their ADV? It’s a bit of a red flag they don’t post this on their website where it would be easy to find. You can go to the SEC website to find it. I learned this from Abominable Snowman. They have to file these with the SEC and disclose their fees and compensation. https://www.adviserinfo.sec.gov/IAPD/Content/Common/crd_iapd_Brochure.aspx?BRCHR_VRSN_ID=569287

holy cow 2% AUM and the advisers also get commission from insurance sales. I think Nicole Boyson is currently studying these types of double-compensation kick-back type of firms. But anyway 2% is ludicrous.

With their current AUM, your account would represent over 2% of their business! Of course they would let you have a second meeting free of charge. The best part will be how they justify keeping you in 3-4% cash so they can collect their 2% fee safely without you having to notice or feel the pinch. Please take that second meeting and report back. Maybe see if they can have it over lunch. Just kidding.

I supposed I view things from a more simplistic angle. The Super Roth you said sounded like permanent insurance which for me is a hard no. I immediately think whoever sells it to someone gets the first year’s premium as their selling cash reward and then annually will receive part of the premium as income. Hard to be impartial when that much cash is coming towards the person selling it. I immediately see my checkbook behind all the vaults on the Get Smart tv show. Yeah, I’m your age range.

As for managed fund . . . even Warren Buffet can’t time the market and he is a pretty good picker. As you already said why continue to play the game if you have won.

Glad you are writing these up. I’ve had similar meetings but not to the level of products they are pitching you. Course I don’t have the asset level you do but have a good future nest egg for me.

Gregg said something like “these are the moves wealthy people make.” This could be true and it could be something we need to do as well. Perhaps this is an option above my current level of expertise because I’ve never been wealthy before.

My thought was that Buffet has stated that when he kicks off, his money goes to his wife in a simple 4 fund index portfolio. That seems to be the move that wealthy person makes, not active management.

This is what you get when you meet with a fee-based advisory firm… Bad advice all-around.

1) their argument on passive versus active management funds is ludicrous. This is an academic argument at this point, and believing their manager is the next Peter Lynch is both uneducated and assinine. The only real reason to recommend it is to make more money off of you.

2) permanent insurance is a joke unless you happen to be one of the few people who are going to in into estate tax issues, which is north of $11 million. Just make sure you have less than that when you die… Oh, and they earn 50-110% of the commission you pay in that first year, which is the real reason they mention it to you.

3). LTC for someone with a net worth north of 4.5 million. Again, offered and recommended because they make money from it.

The solution? Get your advice from a flat, fee-only advisor on the same questions. They will almost certainly provide the counter-arguments you are looking for.

Likely, the only good advice you received was on social security.

The financial industry isn’t your friend, which is why it is so important to limit conflicts of interest. This best done with a flat, fee-only fiduciary who has experience working with people like you.

Yeah, looking at their ADV to see how they are compensated, its easy to see why they would recommend all of these extra products. It doesn’t even seem like they have a tiered structure for their AUM fees, so you would essentially be writing them a check every year for $90,000. Well, you wouldn’t write them a check. If people had to actually write out a check to their advisers, very few would hire one. But they would skim it off your accounts. What a grift!

Here is my simple take for what it is worth – I do not care for any of their advice. 🙂

Even the answer on Social Security seems to make little sense to me despite this being their area of “expertise”. If you and your wife are healthy why would you not wait till age 70 to claim yours and likely your wife as well (there are some wrinkles in this in which maybe she should claim hers at 62 and switch to half of yours at age 70)? That would allow you to perhaps do some Roth conversions in lower tax brackets after your wife retires but before you have the added burden of Social Security income. Maybe ages 60+ to 70? At least some of the RMD burden could be alleviated? Just a thought.

Obviously I do not know as much about your full situation as needed and I do not consider myself an personal finance expert but my advice is run away….

Wife claiming at 62 has a pretty big downside. It means she would be limited to 32.5% of his draw not half. Given that she has so trading 5 extra years of an even smaller draw than if she drew at 67 and then being stuck with only 32.5% of a much larger draw would almost certainly be a large mathematical mistake.

Claiming at 67 is nearly an actuarial wash with claiming at 70. If you live to 90 then 70 is better. If you live to 80 then 67 is better. But neither is that much better than you might think. If you live to 84 or so its about a wash.

The person that needs to wait until 70 is the person who has no money and will depend on social security for nearly all of their retirement. If this person could possibly work until age 70 and then draw that person will change their retirement payouts in ways that will be very meaningful for their personal retirement situation. This person needs the higher payout and longevity protection that drawing at 70 provides. For someone who has a solid retirement, it will have very little meaningful impact so why not draw at 67 and start getting the benefit? Drawing at 67 also has some time value of money benefits that reduces the benefit of waiting until age 70 that very few comparisons take into account. They just show total dollar differences but when you draw at 67 you can spend less of your savings and those savings growing over time makes the benefit of waiting until age 70 even smaller. It is also the case that waiting until age 70 only helps the primary drawer, the spouse only gets 1/2 of the age 67 draw, not the age 70 draw. In addition since the wife will be drawing a much lower draw, she would have to wait another 3 years to be able to draw 50% of the spouses draw which will be a big hit. Actually as I type this in this particular situation waiting until age 70 might take beyond age 90 to pay off given the reduced spousal draw for another 3 years. Drawing at age 67 is almost certainly the far better solution here in almost every conceivable scenario.

All that is to say that I agree 100% with their social security advice. I think everything they said about social security was spot on including the fact that social security is rock solid and has zero chance of going away and very little chance of even being modified for those close to retirement (except to possibly see benefits increased for lower wage earners in the future). Younger high income earners could have benefits reduced in the future but that is the only real risk. I have been preaching the safety of social security for decades.

Their social security advice was great. Why? Because they have no financial incentive to give self serving advice that is wrong.

All their other advice was clouded by self-serving incentives that drastically distort their view of reality. The number one rule of sales is be careful what you incentivize because that is exactly what you will get, even the things you didn’t intend to incentivize. However in this case the company incentivized exactly what it wanted to and that is high cost products that will be very lucrative for both the company and their sales reps.

I will discuss each from bad to worse.

Bad:

Managed funds. These will have high fees for the company. The funds will need to out perform the market every year just to keep pace with the market. No research shows any fund company ever being able to do this over a sustained period. These guys must have found the secret. ooooooh, secret, everyone loves to be in on the secret.

Worse:

Permanent insurance as a super Roth. This is so dumb I hardly know where to start. This is the same as the whole “bank on yourself” trope that has been going around for decades. You pile large sums of money into a life insurance policy and then you pull funds out of that policy tax free later in life. But there is a catch. A huge catch. One they try to ignore or gloss over or explain away.

Here it is: IT’S NOT YOUR MONEY. IT’S THE INSURANCE COMPANY’S MONEY. IT’S JUST A LOAN. YOU HAVE TO PAY IT BACK. AT INTEREST, AND USUALLY A HIGHER RATE THAN WHAT THE CURRENT MARKET IS WHICH RIGHT NOW MEANS ABOUT 6% RATE OF INTEREST ON THE PAYBACK. YOU CAN NEVER TAKE A DIME FROM A LIFE INSURANCE POLICY UNTIL YOU ARE DEAD!!!

Oh but they will tell you that’s fine, you just never pay it back, you just roll the interest over (which means it compounds and you pay interest on the interest on the interest ad infinity) and you will have so much built up in there that you will never have to pay it back and then it just gets paid off by the death benefit when you die.

That is all good and fine if you don’t take out too much, if you don’t have it out too long and don’t live too long so that the compounding makes it grow to an amount that exceeds the death benefit.

And how much money do you have to put in and for how long do you have to pay and let the policy “grow” before there is enough in there to take any decent amount out? The answer is a lot and a long time. And then if you do take considerable loans out and they keep piling up interest at 6% or higher throughout the years you watch it eat your estate piece by piece and by the time you die your death benefit is gone to pay back the loans. If you live too long you may actually find yourself in a situation where you have to start paying it back because it became too large. It’s like a reverse mortgage where the bank eventually owns your house. You now have to pay the mortgage back or get out of your house. Except in the life insurance case there is no house to forfeit, you would have to forfeit the life insurance policy which they would make you do before the loan value even exceed the cash value of the policy let alone the death benefit. And if you have to surrender the policy to satisfy the loans then the value of the loans that exceed the value of the premiums you paid in (not the cash value just the premiums you paid) would all become taxable income in that year. Where is the money supposed to come from to pay that.

Life insurance is not your money until you are dead. Never ever forget that. It’s not a bank. It is not an investment account. Let me say that again. IT IS NOT AN INVESTMENT ACCOUNT!! You do not own any of that money.

So why do advisers push something so bad. Because the incentives are so mind warpingly distorting. My father-in-law was an insurance salesman. Permanent life insurance built his entire business. He told me the details. He made 110% commission on the first year premium and then a much smaller but still decent piece of every subsequent premium.

So are these advisers evil? No the company does an amazing job brain washing these people. My father-in-law owns tons of this stuff and bought a lot of it for all his kids too. Granted he got commissions on all of it but I have had many discussions with him about it and the best I can get him to admit is that people should probably have some term too since they probably can’t afford to buy nearly enough permanent insurance to cover their true insurance needs but he strongly believes in the investment portion of the policies. Plus he says he has sold to many people who blew all their other money and if they didn’t have these policies they would have nothing. So what he is saying is it is financial insurance for people who are terrible with their money.

So yes, please sign me up to buy something that is financial insurance for people who are terrible with their money.

WORST:

LTC as a permanent insurance policy. I am not a believer in LTC policies themselves because there are just too many unknowns and the industry keeps changing. I am not sure what I would need by the time I would need it and if a current policy would be the right fit. Plus it is very expensive. But at least it is what it is and pay what it pays for the need you bought it for.

Piling even more money into a life insurance policy so you can draw that out when you have Alzheimer to pay for care and run up big loans very quickly and then have no one there to really understand what is happening with that underlying policy before it eats itself up needs to get surrendered and your family now has to deal with not only the pain of watching what you are going through but the potential financial mess that will get sprung on them when everything starts to fall apart with the life insurance policy? This is financial malfeasance.

But they sales people don’t know any better.

They have been to dozens of company religious cult-like investment meetings where they were fed so much kool-aid that they don’t even know what non kool-aid tastes like anymore. Again my father-in-law has told me how they had multiple yearly meetings discussing how great and beneficial these products were for all their customers. It’s not kool-aid to the devoted, it’s the air they breathe.

I really don’t blame them. The kool-aid and the commissions are purposeful brain washing techniques. They cannot see the truth because they have been indoctrinated. But that makes them no less dangerous. Perhaps more dangerous. Religiously indoctrinated cult like followers have been shown to do a lot of damage. The uninformed need to stay away from these people. They are dangerous.

That is why the only advice they gave that was really good was on social security. No kool-aid, no warped commission structures, no cult meetings, thus no brain washing.

Not trying to debate but what I was perhaps suggesting was his wife taking her SS at age 62 and then switching to her spousal SS at age 70. I was not suggesting locking in at age 62.

Anyway, I find this calculator to be very valuable regarding SS claiming strategies:

https://opensocialsecurity.com/

Try it out!

Hi Crusher,

I think I did understand what you were suggesting. Most people do not understand the details of what happens to the spousal draw when a spouse draws prior to their own full retirement age.

I explained this in a different post here:

https://esimoney.com/my-experience-at-a-direct-mail-retirement-seminar/#comment-84100

but I will summarize it again:

In order to get a 50% spousal draw you cannot draw before your own full retirement age of 67. Every month that a spouse draws early reduces her spousal draw and if you draw the full 5 years early it reduces the spousal draw from 50% all the way down to 32.5%. So for instance if ESI had a FRA draw of $3000 (That’s probably a pretty good in the ball park estimate), then if his spouse draws at 62 when she switches to her spousal draw that draw would change from what would have been a $1,500 a month draw down to a $975 a month draw. It is almost impossible to devise a scenario under which this would not work out worse for her in the long run if she draws at 62.

Hmmm, I have to look into this further.

Thanks!

Hmmm….I need to look further also. I get the same recommendation from opensocialsecurity.com that I believe Crusher is getting. That site (which I’ve believed to be reputable) suggests my spouse drawing at 62 then moving to spousal benefit (albeit reduced) 4 years later when I’ve turned 70 provides the highest expected NPV benefit. I understand the NPV’s could shift based on life expectancy, but I also thought the site dealt with that thru their survivor benefit modeling. I’ll have to study further. Fortunately spouse’s 62nd birthday is 5 years off.

Well geez….that was helpful (to me). I did look further at opensocialsecurity.com (OSS) while my earlier comment was still “under moderator review”. I now realize OSS defaults to use SSA’s “standard mortality”, but gives options to adjust to use either more pessimistic or optimistic mortality assumptions. When I switch to “super preferred” (we both live the longest “option”), the highest NPV does come very close to spouse drawing at FRA and me still at 70.

I guess that’s the beauty of these financial blog sites. They force me to learn from the community. It takes a village….

If I understand you correctly, then I have to disagree. I started taking SS 4 months ago at age 63 (reduced rate of course). My FRA is 66 and 4 months. My wife also started collecting on my SS 4 months ago (she has no earnings record). She collects 50% of my FRA benefit.

Great. Different perspectives are always interesting to hear. What specifically is it that you disagree with that caused you to draw early?

I think I missed that your point was that your spouse was still getting 50% even though you filed early. I didn’t say anything about the primary filing early. Only the spouse filing early. How old is your wife? If she is older she may already be at her FRA, which is why her benefit is not reduced. There are other things that can affect it like if she is caring for a qualifying child etc. I don’t know all the details of your situation. However whatever your situation is I am only pointing out what the US Govt says its policy is. So somewhere here there is a disconnect with the facts, because the SSA is pretty clear on what happens as stated in the article from the SSA website that I referenced in the previous post. If the spouse draws before their own FRA, their spousal benefit is reduced unless there are other extenuating circumstances.

Ah that makes sense. My wife is older, past her FRA, so it’s not reduced, as you explained. Thanks for the clarification!

Thanks, Apex! That was a good read.

Thanks Diogenes,

I apologize for how long it was. I was just typing away and after I posted it and saw its size I thought good God, no one is going to read all that. 🙂 I could have benefited from a good editor on that post I think. I am glad at least one person did read it though.

On the contrary, I found it fascinating and I am a much smaller fish who likes learning for all y’all sharks.

MY LTC story: this was pitched to my mom and stepfather in the 1990s. The takeaway was that the cost of the insurance and their pot of money would converge eventually. However, the stepfather got recurrent cancer and never needed it. My mom, at just 90, has home health and other bits and bits so that, although she can walk with a walker, stays in her home and does not need LTC.

Refugee, you should check your mom’s LTC policy. My mom’s policy pays 50% for in-home care and suspends premium payments when she is on in-home care.

I was waiting for your comment since I knew it would be EPIC! You didn’t disappoint.

What are your thoughts (or anyone else’s) on what people like my neighbor should do with his investments now? Go to cash (at least in part)? Something else?

TL;DR – if you just want the investment advice and not the long prelude skip to the section below the ************

Before I give my opinion on this let me just address the scary 800lb gorrilla these guys brought into the room. Namely that this market has been riding a cocaine high for the past 10 years and the future looks dim. This was a purposeful scare tactic. The data makes it look plausible and of course anything is possible. After all the metaphorical doomsday clock has been at 2 minutes to midnight for the past 2 years and they just moved it closer last week to only 100 seconds to midnight. The world could end at any moment, so eat, drink, and be worried. That seems to be the general state the media is always telling us to live in.

I see it differently and thusly:

1. Yes we have had the longest expansion in post WWII history, but it came after the sharpest recession and pullback in post WWII history. That fact is rarely part of the narrative but it’s a critical ommision. We didn’t shoot off on a rocket from the top of the empire state building. We have been floating up in an air balloon from deep within an abyss. Everything is relative and our relative altitude is not as high as some stats can be made to appear.

2. Yes our PE ratios are historically higher than average, but they are not at levels that the previous two crashes had and there other differences that decrease risk.

(a) PE are above average, but not at crash levels. historical PE chart: https://www.macrotrends.net/2577/sp-500-pe-ratio-price-to-earnings-chart.

(b) Interest rates are considerably lower than the 2000 and 2008 crashes. Interest rates are the competing market for stocks. When there are no alternatives for yield, the demand for stocks tends to stay strong.

(c) Both 2000 and 2008 had massive pressure building from excesses in the market. I am aware of no such pressure or excesses in the market today that are remotely on par with what was building in the market in those two crashes. 2000 was the dot com explosion where the nasdaq went up over 100% in 1999. People took out loans on their houses to buy stocks. Which stock? Any stock, because stocks just go up. There were jokes about brokers promoting certain stocks and the client asking what do they do? Answer? Go up! That is likely just a story but it is representative of how mom and pop investor had gotten sucked into the mania. 2008 was the housing bubble where people bought houses with no income, on documentation, and no plans to even use the house. They just sat on it for 6 months and sold it for a 15% profit. When those loans began to default it was so pervasive across the financial sector that it brought down huge institutions and nearly the entire financial sector all because of rampant speculation. That is a key ingredient to a bubble. Speculative mania which is not present in a meaningful form in the current market.

(i) Side note: Housing prices have fully recovered since the crash and become hot in some areas. Housing is no longer cheap, but it is not a bubble either. House price strength is currently driven by pent up demand, low supply, and low interest rates, not speculative demand. There is no current bubble in housing. NO CURRENT BUBBLE IN HOUSING. Could housing stagnate or go down. Yes it could. Could it crash like 2008. No way. The buyers and holders of houses today are 10 times stronger than the sub-prime mess, credit default swap, AAA rated mortgage backed security fraud that precipitated 2008.

(ii) side note 2. I am not saying this just with hindsight. You have no way of knowing what I really thought but in 1998 I already saw excess in the stock market. I had predicted to many people that the mania had to end. I didn’t actually pull out any money so I don’t know what that meant about my conviction but I did believe it would end. I was two years early and more than doubled my money before it actually did end so it was still better to stay in. Plus I was young so I didn’t have much to gain or lose anyway. Oddly enough in March of 2000 I finally lost heart and threw up my hands and said I guess I am wrong, to infinity and beyond is possible. It crashed about a week later. So my fortitude gave out just a little too early, but it is a perfect example of another phrase I have heard often about the market. “The market can stay irrational longer than you can stay solvent.” Don’t try to bet against the market. In 2006 I told my brother that housing had peaked. I didn’t expect housing to go up anymore after that year. It had become too detached from reality. From a housing sales number stand point that appears to have been about the peak, but housing prices did still climb for another year and it was another 2 years again before the stock market crashed. So in both those crashes I felt there were strong pressures from excessive mania in the markets. My assessments appeared to be a couple years early before any consequences hit the market. And of course anything can happen and we don’t have to follow old patterns. The Coronavirus could kill us all and crash the entire economy. But I don’t currently see the types of things that caused the last two crashes.

So that all being said, do I think we can keep getting these kinds of returns for the next 20 years? No. Returns have been too high. There will probably eventually be some reversion to the mean but with interest rates this low that mean might be higher than it historically has been. And of course the pull back could be after the market goes up considerably from here.

Who knows. Not me and not these advisers. However the idea of 0% over the next 20 years seems very implausible. Even 3% seems unlikely to me. So I think one needs exposure to equities to provide any meaningful growth in their retirement portfolio.

*********** INVESTMENT ADVICE STARTS HERE ************

My preference for retirement is to have growth assets like real estate and dividend paying stocks which throw off enough income that I never have to touch any principal yet the underlying asset tends to increases in value with the market as a hedge against inflation so that future income streams also increase. That is why bonds are not listed as one of these assets because they only throw off income but have no growth potential. I believe this to be the gold standard for retirement.

But other than the types of people who read sites like this, the number of people who are in a position to do this is negligible.

So what to do for the masses.

For those with less than $1 million of retirement assets, I would do the following:

1. A few years before needing to draw on the assets, 3-5 years worth of income requirements (calculated needs after social security, pensions, and any other income sources) should be put in cash equivalents. Laddered CDs, medium term bonds, corporate bonds of very safe companies, etc.

2. The rest should be invested in various index funds. Most in broad funds like an SP500 fund or even a balanced type fund such as Vanguard Wellington if portfolio variation is strong concern. (Side note: I am not personally a fan of target date funds, but for some people they might make things feel safer.)

3. Needs for new funds should come from the stock portfolio when the market is doing well or is flat.

4. When the market is down more than a small amount, lets say greater than 5 or 10%, then needs for funds should draw from the cash funds. Once the market recovers then stocks can be sold to replenish the cash funds for the next downturn.

5. The 3-5 year cash supply is to withstand large draw-downs instead of short corrections. In that sense 5 years is best if one can afford to have that much of their portfolio in cash equivalents and still generate enough return to fund their retirement.

The goal of this plan is to remove sequence risk where withdrawals from stocks at the wrong time have a devastating affect on the size of a portfolio making it nearly impossible to maintain the life style that it was previously affording.

Wow! Another great response!!!

Great information Apex. SS information you provided in previous comment is particularly good. It can be confusing understanding difference in benefits between spousal/survivorship and you nailed it. For maximum spousal benefits from a higher earning spouse, lower earning spouse is best to wait to file at FRA. Higher earning spouse is better to wait until 70 to file so that lower earning spouse can have higher survivor benefits. I also agree with keeping 3 to 5 years in cash equivalents if one can afford it. Excellent information!

Great advice Apex! I am fortunate to have enough of a nest egg to live off dividends. And, although I intellectually understand that money is fungible, my animal brain feels safer when I don’t need to touch the principal.

Spot on about the permanent insurance Apex! Bravo! Keep preaching…

Thank-you for your insight. This helped me rethink when I take by social security.

Thank you very much, ESI! This is very helpful. Very much looking forward to your LTC insurance post.

Go to the next meeting and post what more you learn about the snake oil they’re selling, just out of curiosity.

My thoughts on pretty much everything they told you:

“Act as if every broker, insurance salesman, mutual fund salesperson, and financial advisor you encounter is a hardened criminal, and stick to low-cost index funds, and you’ll do just fine.”

William J. Bernstein, “If You Can: How Millennials Can Get Rich Slowly” (FREE BOOK) – July 16, 2014

http://tuttle.merc.iastate.edu/Bernstein_If_You_Can.pdf

I would be inclined to agree with this comment the most. A few simple truths: 1. Nobody cares about your money as much as you do. If you educate yourself, and really care about the moves you are making, you will do just as good (or better) of a job than the vast majority of “professionals.” 2. All this “free” stuff and time they are giving away is not “free” in the end. Someone is paying for it. It’s like that old saying in a card game, if you look around the room and don’t know who the sucker is, it’s you. They are not doing all these free meetings and seminars and giving away books because they are altruistic people and wake up every day super excited to spread the gospel of financial freedom for others.

I loved reading about your experience. I got the impression they were trying to make money on you, via commissions and/or fund fees.

Thank you for sharing the Social Security information. We are nearing the age where we could start to collect but my husband is still working (enjoying his job, though less so over time). I suspect we will start collecting around the time we reach full retirement age, as the advisor suggested.

My parents had/have LTC insurance. My dad paid premiums for at least twenty years and then collected for less than eight months before he passed away. My mom has been paying premiums for at least twenty five years and has not yet been covered for her expenses, even though she has been in assisted living the past 2-1/2 years. Additionally, the maximum payment is $100/day, which is far from great coverage. Luckily they/she have good income, savings, and secondary medical insurance. I don’t think LTC insurance makes sense for our generation, though I wish that was not the case.

My math says that since you don’t need Social Security, you should draw it as soon as possible and put every dime in the market. The growth rate on you money in the market over the 5 years should be sufficient to match any loss of benefit from drawing early.

Whenever I see people promoting taking SS early and investing it I have to wonder.

For the average person, you have to live on something. So, when you hit age 62 and draw SS, you are either living on work earnings or living off of other investments.

If you are living off of work earnings and taking SS before your full retirement age (FRA), you run afoul of the earnings limit if you have earned income above $18,240 in 2020. That means they take away $1 for each $2 earned above the limit. So if someone is working a job and earning something above $40K a year you aren’t likely to be getting very much from SS to invest. Additionally, you start paying taxes on what Social Security you do get when you have adjusted earned income (e.g. after tax deductions) over $30-40K a year depending on tax status, further likely reducing what you have to invest.

Now, if you are living off investments, there may be ways of maneuvering things to your advantage so taking SS to invest may be good for an individual (e.g. I could see someone with multiple rental properties finding ways to maneuver earnings and taxes to get SS and be able to invest it). But for the average person you are either taking money from your investment accounts to live on or from your social security to live on, effectively making your SS money an investment “wash”. So as general advice I don’t buy the “take it and invest”. Most folks aren’t likely to better 7-8% a year on investments until they hit FRA. So I think this is more about concern over not getting it or what if scenarios than actual finances.

So while there may be various reasons for taking SS early, I’m not seeing taking it early to invest as one of them for most folks.

Thanks for sharing. If you are familiar with the bogleheads forum, you should post your 4 questions to see what the collective wisdom of the group recommends to compare/contrast to the financial planners.

For your first question – see what https://opensocialsecurity.com/ recommends.

Other than the social security question, the financial planners recommendations for the 3 other questions all had their best interest at heart vs. your own.

It would be a big no thank you for me (free coffee or not & I do like free things).

Thanks for meeting with the financial advisor!

A couple of thoughts.

Ran a broker check and found this little gem https://www.colorado.gov/pacific/dora/asi-wealth-agrees-to-sanctions-for-securities

It’s always a good idea to run a google search of an advisor and the firm using the key words FINRA and SEC. For large firms, it is common to see numerous complaints. Ie Merrill Lynch.

Another place to search is the SEC if someone holds themselves out as a financial advisor or advisor representative.

Here is the disclosure form that is required to be given to clients.

https://www.adviserinfo.sec.gov/IAPD/Content/Common/crd_iapd_Brochure.aspx?BRCHR_VRSN_ID=569287

The ”financial planners” in quotes since I don’t know their full legal names, would need to be vetted on these sites as well. Too many insurance agents call themselves financial planners with no background in finance.

Looks like Mr. ESI could call himself a financial planner!

Last place to check is with the insurance commissioner’s site.

The following is my opinion and should not be construed financial advice. Consider these comments as pure banter while chatting over coffee.

You don’t need long term care insurance. Either your rental income or the RMD’s would cover the cost of stay. Comparing LTC insurance to auto and home insurance is a classic scare tactic by insurance agents.

Average stay in a long term care facility is 2.4 years. https://www.morningstar.com/articles/564139/40-must-know-statistics-about-long-term-care

I’d like to see a post on their tactical/timing/ worlds greatest money manager. I’m dying to know who they use or if it’s their own “in house” proprietary model. Either way, here are the potential fees per the SEC disclosure.

1% to firm

1% to advisor who would handle your account.

? fund fees and expenses plus a potential platform fee with the custodian.

They can discount this a bit if you have over 1 million. In my experience, total all in fees with many financial planners runs 2-2.5%. Even outfits like Ric Edelman charge a lot.

Why take social security early? Wait to age 70 since you don’t need it. This acts as longevity/LTC insurance if you live past 80. Plus, your 90 year old self or wife will thank you for the 8% of guaranteed returns on your SS benefit that keeps up with inflation.

As usual, another great post.

I just want to comment on your Social Security plan. I’m pretty much you, just older. Similar assets, wife paid into Social Security only about ten years. I paid the max in for 38 of the 38 years I worked, which is three more than matter. That means like me, you’ll get a big check and your wife will get a small one until she switches to half of yours. I’d suggest you consider modifying your plan from both of you taking Social Security when reaching 67 to her taking hers at 67 and you waiting until 70. You’ll get three more years of 8% that way and if she outlives you, which is likely, she will get that extra 25% or so the rest of her life. My wife is very healthy, she’s training for a full marathon right now and she is 65, unless a truck runs over her I’d guess she’ll outlive me by ten years. I’m a runner too but there are way more silver bullets out there taking out men my age(and yours) than there are for women. My wife is only one year older than me, not three years like yours, but the math is pretty solid for me waiting until 70 to get her the biggest check possible after I’m gone. I would think it would probably still hold for you as well. But I’d guess you’ve run the numbers so maybe I’m wrong. I had my Vanguard advisor run them as well and it favored our plan.

Agree fully with Steveark’s SS plan. Exactly what spouse and I plan to do. I am higher earner. Spouse is 1.5 years younger.

“Gregg said something like “these are the moves wealthy people make.” This could be true and it could be something we need to do as well. Perhaps this is an option above my current level of expertise because I’ve never been wealthy before.”

This is exactly what a salesman would say. If you wanted to do what “everyone else is doing”, you could go back to work, take out a mortgage on your house, carry a balance on your credit cards and buy a new car with a loan! It seems that you are doing just fine even if you don’t make “moves wealthy people make.”

Don’t waste anymore time with these guys, they obviously just want to get their hands in your pockets.

I’m tempted to go just to get the details on what they are proposing…aren’t you curious? 😉

I’m chuckling at all the concern as if you are a minnow swimming among sharks…I doubt Mr. ESI is going to be bamboozled by their slick presentation. And I have no doubt you’ll head back for more the eye-opening content 😉

LOL!

This post has more than average comments (reader interest?), so yes, please go back and get more details. I’m really enjoying this post and comments.

I also agree with most of the comments in this post.

Yes, I’m curious to hear their plans. Confident that you can handle yourself! Try to get another free dinner too.

I chuckled a bit reading the post and comments. At one time I wrote up a list questions for financial planners. A quick summary was:

What services do they provide other than portfolio mgmt?

Explain in detail how they get paid?

Are you a fiduciary and how do you define that term?

Ask them to outline their recs on asset allocation, asset diversification, and asset location and why? It’s ultimately my decision, but I what to understand their thought process.

Do they feel they can offer “better than net index returns”. If they say yes, and they usually do, ask them if they would:

1) guarantee the index (including dividends) annually.

2) take the next 1% better than index returns for themselves.

3) split the remainder better than index returns with me.

Their answer to the above will show how confident they are in their ability to perform.

This would be a little more difficult to reconcile in non-retirement account due to taxes.

I must admit, I haven’t done this yet, but I will if I meet with an advisor again.

It’s a simple, “Mr. Advisor, put your money where your mouth is”.

I’m sure no advisor would agree. And, I wouldn’t accept this unless it was in writing and from a large brokerage firm.

Robert – I think you’re questions are spot on. Although I wouldn’t suggest actually using your payment structure – you’re incentivizing them to take huge risks. If they take the risks and it works out they get paid and they’re a genius, if not, oh well they’re not going to get paid anyway and now they just lost a bunch of your money. This is why it’s best to get a fiduciary and pay them directly as opposed to paying them based on AUM or some amount of gains.

The repeated high quality content in this blog series is extremely impressive and I have read the last few hundred blogs so consider myself an expert on the topic 🙂 Kudos ESI

Few points

1. I have often thought I need to get smarter on LTI insurance (and looking forward to the blog series) but today was the first time I realized it is probably something I don’t actually need. Funny on the house insurance as 7 years I decided I was not going to renew it as had a very high deductible (10K) and due to area I live in it was $4000 to $5000 a year (on a 400K home) with my thought being if some catastrophic happened I could afford to buy a new house. I was a little uneasy about it most because it is not normal but made sense and now have 28K to 35K I can use if I need a new roof or something that more likely would occur. I did spend some $ on some new fire alarms all around the house 🙂 I kept the car insurance that was required by the state I am in and have full coverage on two cars but once they get under 10K in value (have 1 older one) I remove it. No real logic behind it.

Funny about the “All the wealthy people” and “we have 50% of our $ in it”. I would ask for an account statement to see if they are telling the truth (doubtful) as went through this first hand many years ago when I started interviewing financial advisors (lots of low quality and have to really work/research/interview) to find someone good (and you have to know what to ask). I personally am not a fan of fancy offices and lots of staff and fancy marketing as you know who pays for that (their customers). Really great article from Josh Brown on this that I would recommend

https://thereformedbroker.com/2017/07/17/the-butcher-of-park-avenue/

and a few more

https://thereformedbroker.com/2018/06/25/three-uncelebrated-edges-2/

https://www.zerohedge.com/news/2018-03-20/study-reveals-95-finance-professionals-cant-beat-market

All the above I bookmarked and read about once a year.

Millionaire 73

https://esimoney.com/millionaire-interview-73/

ESI: thank you for writing the summary. Also thank you to the many comments written. My mother had LTD bought when rates and coverage were more favorable than nowadays. But she also had sufficient funds to be self insured but she wanted to protect inheritance for her children (my brother and I). Unfortunately she was diagnosed with ALS and her life changed dramatically and she went to heaven before LTD could even pay a bill. But the LTD gave her peace of mind during the illness. My husband and I are self insured with no children to worry about for inheritance. Fidelity agreed with our assessment.

Umbrella insurance was a good topic you mentioned. I hope more people research the value of umbrella insurance as they increase their net worth and potential for lawsuits.

My husband and I went to a seminar where the topic included paying taxes now on Roth conversions due to low tax rate and buy insurance products. Of course the word insurance product wasn’t used by the presenters rather special offers to increase wealth and protect money for heirs. It is scary how many financial advisors are offering insurance products but disguising the actual financial vehicle.

I was actually pretty surprised when you said the first and the third of the dinners were a tie or close. To me – this is exactly what I would have expected after I read about the third dinner experience. I was intrigued by the low key approach of the first dinner though. Thought their responses were more thoughtful too. Are you considering giving them a visit to compare and contrast?

As an aside, I am in business development (fancier name for selling). I personally prefer the low key approach and have been reasonably successful. But I am so surprised when I see a lot of people fall for a lot of jazz and no substance in my business (and the buyers are supposed to be fairly sophisticated). Feels to me that folks with no substance compensate with jazz. But of course that’s a self serving explanation 🙂

Passion still sells. People want a little sizzle with the steak!

You need a lot of sizzle when the steak is Salisbury.

Hey, I like Salisbury steak 😉

Thank you for posting this. The timing is perfect. I was considering seeing an adviser I found on WCI. Not because I need someone to tell me how to invest (decent/good offense here), but more to address the questions you teed up: to get LTC insurance or not; RMD ramifications; and best way to invest going forward “once you’ve won the game”. Based on what you shared, I have decided to hold off another few years. When all is said and done, these guys need to hustle for a living and make a buck. “Fiduciary” be damned. Thank you ESI.

I do like that they did not use scare tactics on the future of social security. Many financial planning web sites (and presumably live planners) don’t include social security in retirement income estimates, which really ups the savings pressure for people. Survey results show large percentages of people believing social security will go away, but that reflects their lack of information, rather than reality.The reality is that in 2035 when the trust fund is exhausted, SS will only be able to pay 80% of benefits with current SS tax receipts. That means that they could pay full benefits by increasing SS payroll tax by 25% from 6.2% to about 7.75% (employee and employer). So, make a wild guess about whether voters would prefer 20% benefits cuts or a 1.55% increase in the payroll tax? Benefits will not be decreased in that scenario. You can count on that.

Why not start converting IRA money to roth now? At a predicted RMD of ~$100k that would put you in the 22% tax bracket if tax brackets stay the same as they are today. The 22% bracket is up to $171,050 and the 24% is up to $326,600. You will most likely be paying a 22% rate at a minimum as things now stand. Why not cap out to the current 24% bracket now (not that much more than the 22%) by converting some money to roth and locking in future tax free growth? I think tax rates will be higher in the future. I realize this ignores the time value of money and misses out on the growth that 24% spent on taxes now would make if it stayed invested, however, tax free growth is attractive if tax rates are higher in the future. It might be possible to reduce future RMD amounts enough to put the withdraws into the 12% tax bracket.

This is the strategy I’ve been doing for last couple of years when I realized that if I don’t make any changes, I’m going to get slammed with taxes when I have to start taking RMDs. I’m a 56 year old working drone and have been paying the tax on my conversions with paycheck money, not IRA money. The “problem” I’m having is I can’t convert enough money each year, staying within the 22% bracket, to keep up with the growth in the IRA. When I quit work I’ll be able to take bigger bites but I’ll do it at the 12% tax rate. It will take me about 20 years to convert it all using a 12% tax rate, not counting future growth, but I don’t need to convert it all. I just need to convert enough to keep the future IRA RMDs in the 12% tax bracket.

Hi Kek,

MD on FI/RE (signs GASEM) has good examples of how he is doing this in real time (now 68 working to finish by 70 (when SS Pension starts) or 72 when RMDs starts. Here is a link to one of his many posts on the subject http://mdonfire.com/2019/12/30/roth-to-the-rescue/

By the way, shooting for $500 K in IRA at age 72 is a pretty good goal per his calculations which seem reasonable to me to keep in the 12% bracket.

Another good source is Big ERN blog: https://earlyretirementnow.com/2019/11/20/how-much-can-we-earn-in-retirement-without-paying-federal-income-taxes/

This link is to the 3rd in a series of articles on a case study where he solves for how much to do in RMD conversions before age 72, and how much to do after age 72 in this particular case. The good thing is that he has 2 or 3 very good calculators on his site (and some good links) that lets you Do It Yourself.

Both are highly recommended to you and other readers. ESI knows Big ERN also and has written highly of him.

“pays for itself in spades”

That phrase alone – although I’m not entirely sure what it means – scares me. Sounds like the advisor thinks it’s a “guaranteed investment” that gets better-than-average returns and never loses money. Something that doesn’t exist in reality.

This firm and it’s founders have been sanctioned and fined for selling unlicensed securities. They are not true, 100 percent, all the time, fiduciaries. They receive commissions and give poor financial advice. You may even be pitched annuities. Run away quickly to a fee-only, 100% fiduciary who will sign a written agreement with you that they will ALWAYS do what’s in your best interest. This company will not do that for you. The honest truth is they have no right to call themselves financial advisers when they are just commissioned salespeople.

seriously? Where did you find this

One of many links on the subject below. Also, feel free to contract FINRA directly. I will also add that this firm has pitched equity-indexed annuities to numerous individuals, and profited immensely, despite FINRA issuing a warning against these insurance products, and the individuals/firms that hawk them.

https://www.colorado.gov/colorado-springs-investment-firm-agrees-sanctions-related-unlicensed-securities-sales