I’ve been to several direct mail retirement seminars (here’s the summary for the first, second, and third seminars) as well as a retirement workshop.

I’ve been to several direct mail retirement seminars (here’s the summary for the first, second, and third seminars) as well as a retirement workshop.

All of these were used by financial planners to solicit new clients.

I was aware of that when I went to them (of course) and expected that a “pitch” or “offer” of some sort would be made.

But little did I suspect that similar strategies were being used by planners online until I stumbled into one.

Here’s the story of how that happened…

Looking for Retirement Books

Over the past few months I’ve been reading a ton of retirement books.

I’m trying to assemble a broad range of knowledge so I can offer others the best thoughts on creating a great retirement.

I also want to read all the “top” retirement books so I can then recommend the ones I think are best.

Not too long ago I got on Amazon, searched for “top retirement books”, then contacted either publishers or authors directly (many were self-published) asking if they provided copies for media reviews (most publishers offer books for media outlets since the publicity can drive sales and the cost of printing and shipping a book is so low.)

I received several affirmative answers and you have been reading the fruits of these efforts here on ESI Money.

One book I wanted to read was Safety-First Retirement Planning: An Integrated Approach for a Worry-Free Retirement![]() . It’s written by Wade Pfau a well-known academic retirement “expert”.

. It’s written by Wade Pfau a well-known academic retirement “expert”.

Alas Wade didn’t have a publisher. The book was self-published by Retirement Researcher Media, a group of three guys (one of whom is Wade and, BTW, none of whom appears to be retired) who “help guide you along the path to a successful and sustainable retirement by providing modern, sound academic research, in the manner that helps you learn best.”

Between the three of them, two are PhDs and two are CFAs (Pfau has both degrees). So I wasn’t sure if this was an academic group or a planning company.

Their contact form was less than user friendly as they didn’t allow me to simply send a message asking for a copy of the book. No, in late-1990’s fashion, I had to first sign up for their site’s newsletter and THEN I could send a message.

As you can probably tell, I was a bit annoyed at this, but I persisted. I signed up and asked my question.

That was a few months ago and I have yet to receive a response about the book. The only thing more annoying than a forced sign-up at a poorly designed site (they really need to hire someone to update the look) is no response once you jump through all the hoops.

Soon after I signed up they sent me an introductory email. In it they listed several resources they have available, some of which are pretty interesting.

But behind many of them is a refrain I recall from the meetings noted above: “Have a Question? Want to have a Consultation?”

Yes, they were using the site to generate “consultations” which I then assume they used to turn people into clients.

Here’s the legalese at the end of each of their articles:

Retirement Researcher is a SEC registered investment adviser. The content of this publication reflects the views of Retirement Researcher (RR) and sources deemed by RR to be reliable. There are many different interpretations of investment statistics and many different ideas about how to best use them. Past performance is not indicative of future performance. The information provided is for educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy or sell securities. There are no warranties, expressed or implied, as to accuracy, completeness, or results obtained from any information on this presentation. Indexes are not available for direct investment. All investments involve risk.

The information throughout this presentation, whether stock quotes, charts, articles, or any other statements regarding market or other financial information, is obtained from sources which we, and our suppliers believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Neither our information providers nor we shall be liable for any errors or inaccuracies, regardless of cause, or the lack of timeliness of, or for any delay or interruption in the transmission there of to the user. RR only transacts business in states where it is properly registered, or excluded or exempted from registration requirements. It does not provide tax, legal, or accounting advice. The information contained in this presentation does not take into account your particular investment objectives, financial situation, or needs, and you should, in considering this material, discuss your individual circumstances with professionals in those areas before making any decisions.

Obviously, there’s nothing wrong with this — they are a business and trying to gain clients by giving away free information, very similar to what the seminar and workshop planners were doing. I just found it interesting that they were doing something I was familiar with, but doing it in a different fashion.

Anyway, I thought I’d share some of their resources with you as well as my thoughts on them.

Does The 4% Rule Work In Today’s Markets?

Here’s an interesting post that might be on everyone’s mind.

The question is “Does the 4% rule work in today’s markets?”

The short answer: No.

The longer answer:

The low interest rate environment creates additional stresses for the 4% rule that were not apparent in Monte Carlo simulations calibrated to historical data with higher bond-yield assumptions than are available today. For a 50/50 asset allocation to stocks and bonds, these simulations indicate that the 4% rule has a 69% chance of success instead of a 94% chance. The 4% rule may work for today’s retirees, but it is far from a sure bet or a “safe” spending strategy.

With lower stock allocations, the 4% rule is less likely to work because it is placing demands on spending above what today’s interest rate environment can easily support. It is magical thinking to believe that bonds can earn higher rates of return than implied by today’s low-interest-rate environment.

Returning to the issue of sequence of returns risk for retirees, the early returns matter disproportionately in determining sustainable spending outcomes. Success is also less for higher stock allocations because of the assumption that the historical equity premium is maintained on top of a lower bond yield for the early part of retirement.

This suggests that in a lower interest rate world, a 3% withdrawal rate reflects something closer to a chance of success than a 4% withdrawal rate historically provided over the broad range of historical market environments. With higher withdrawal rates, failure rates increase accordingly.

Doesn’t that just sound like an academic? Hahahaha!

Here’s the translation for the rest of us:

- The 4% “rule” that so many are relying on for planning their retirement withdrawals is more like the 3% rule now.

- As you know, I prefer a margin of safety in retirement planning so there’s NO WAY I’d use 4% if I was counting on my assets to meet retirement expenses.

That said, in The Top Five Money Secrets of the Happiest Retirees, Part 2 I noted how the book You Can Retire Sooner Than You Think![]() claimed that the 4% rule was more like the 5% rule (the author argued for higher withdrawal rates) by saying the following:

claimed that the 4% rule was more like the 5% rule (the author argued for higher withdrawal rates) by saying the following:

Assume you have your retirement reservoir sitting in cash and yielding almost nothing (let’s assume 0 percent per year). Just taking 5 percent at a 0 percent interest rate, the funds will still last you 20 years. A level 5 percent withdrawal per year x 20 years = 100 percent of your funds withdrawn, and then the money is gone. This gives you two decades of using 5 percent of your overall portfolio as an income sources—not bad.

A 4 percent yield plus 1, 2, or 3 percent in growth over time suggests that you can take out 5 percent almost indefinitely.

So, if you have a portfolio that’s generating a full 4 percent in income, this is where the rubber meets the road. If you’re generating 4 percent per year (based on your principal), you are technically dipping into your nest egg little by little each year. In this scenario how long will your money last? The answer is more than 40 years. For someone retiring at age 60, this takes you beyond age 100!

Now if you increase your 5 percent withdrawal rate each year for inflation (using 2 percent inflation) your money lasts closer to 30 years. That’s still a very long time. However, in real life retirees adjust their spending over time, typically moderating expenditures to counteract inflation and naturally spending less into their 70s and 80s. Hence, using this rather conservative scenario sets you up for a very high probability of not running out of money.

I’m wondering if they are sticking with this or are they now using 4%?

I’m so confused…hahaha!

IMO, the lower the rate you can use, the better. I would personally use 3% or maybe even 3.5%, but I think 4% is too high for me.

Of course, YMMV. Everything needs to be weighed in relation to your specific goals, plan, resources, etc.

How Much Income Do I Need in Retirement?

Here’s another post I found interesting.

It asks “How much income do I need in retirement?”

The best answer is “at least enough to cover retirement spending”, but as they note, many aren’t the best at predicting retirement expenses:

Most people are focused on saving for retirement so they’ll have the money they need to fund their income in retirement. However, ask most people how much they’re going to spend in retirement and they have no idea. To plan for retirement effectively, you need to have some sense of what your spending needs are actually going to be.

True. Most have “no idea”.

It’s disappointing but simply another sad reality of American financial ability (or lack thereof).

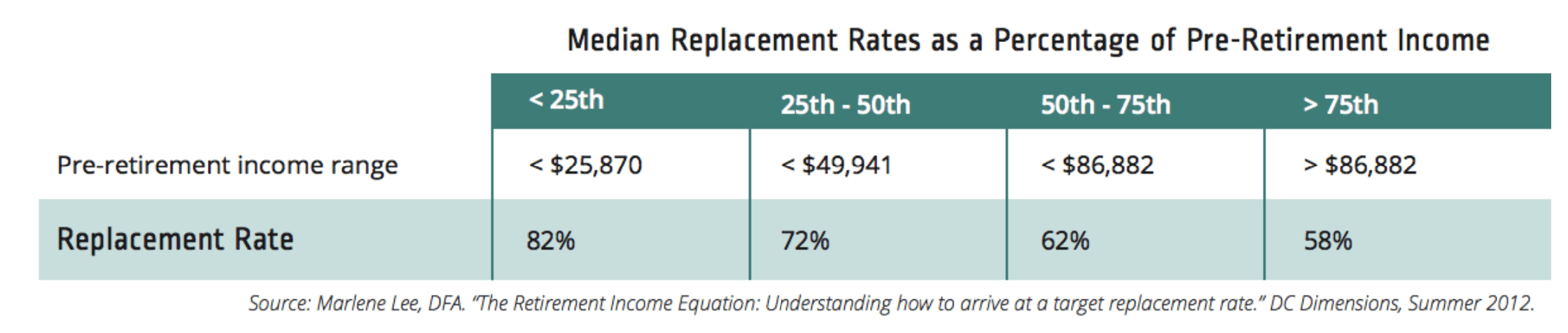

The interesting part is that they introduce the “replacement ratio” as a way to estimate retirement expenses.

Their thoughts:

One common approach is to find your “replacement ratio.” This is found by taking the income you made immediately prior to retirement and figuring out what percent of that income you think you’ll spend every year. The amount you’ll spend is the amount you’ll need to replace every year in one way or another.

Most people end up needing less income in retirement than they did while working, because, among other smaller reasons:

- You don’t need to save for retirement anymore.

- You don’t have job-related expenses anymore (commuting, clothes for work, eating out for lunch).

- You aren’t paying as many taxes since your income is lower.

While a lot of expenses will go down, you’ll also want to consider expenses that tend to go up in retirement, such as travel or other leisure activities you’ll have more time for. Depending on what you enjoy doing, this can end up being a significant portion of your budget in retirement.

Empirically, your replacement ratio is inversely related to your pre-retirement income. The higher your income before retirement, the lower your replacement ratio. Essentially, people with higher paying jobs had proportionally more of their income going to retirement, job-related expenses and taxes before retirement, rather than necessities.

This is very good information IMO. I haven’t seen anything like it previously though the chart I share below says it was created in 2012.

I knew that our spending had gone down (or could have gone down — we’ve bumped up travel spending a ton and keep earning a good amount so taxes are high — but without those unusual expenses we’d be down big-time) and now there’s evidence that this is common.

But it gets even better.

They share this chart:

How cool is this?

You can see how those with higher working incomes require much less spending (as a percent of pre-retirement income) than those with lower working incomes.

Of course, as they note, these are just estimates. They represent a good place to begin planning, but it’s best if you know your numbers specifically, especially if you plan to make any lifestyle changes in retirement (like we have with more travel).

I recommend people start tracking expenses closely at least five years ahead of retirement to see what they actually spend (my experience has shown there’s almost always a big difference between what people think they spend and what they actually spend). Then they have time to adjust if needed (which usually results in the need to save more) so they meet their planned retirement spending goals.

Four Retirement Ebooks

The email they sent also shared links to four (free) retirement ebooks they offer.

The ebooks are “fine” but they appear to be more teaser material than anything.

And they address issues that most ESI Money readers will be familiar with.

At the end of each they offer a consultation, but they don’t say if it’s free or not. I’m assuming it is, but if it is, why not say so?

More on this in a moment. For now, here are the ebooks along with some summary points and my thoughts…

Why Investing During Retirement is Different:

If you’ve been saving and accumulating, the question remains about what to do with your accumulated assets when you retire. Without the relative stability provided by employment earnings, you must now find a way to convert your financial resources into a stream of income that will last for the rest of your life. This is not an easy task.

Unfortunately, the investment industry as a whole is still far behind. Most are still focused on investing the same way they did as they prepared for retirement, despite the different challenges they now face IN retirement. In retirement, you experience a reduced capacity to bear financial market risk. Your standard of living becomes more vulnerable to enduring permanent harm as a result of financial market downturns.

In this ebook they go on to cover sequence risk and longevity risk.

They mostly introduce them, not really recommend any solutions (it’s only seven pages).

Transitioning Your Portfolio For Retirement Income:

As a general rule, advisors do not spend nearly enough time working with clients on the aspirational and emotional aspects of their framework for retirement. We are more comfortable talking about what is an appropriate amount to draw from a portfolio, or what is the “right” asset allocation. Nevertheless, the first question for someone about five years from retirement is what do you want to do in retirement and why?

I like that they’re addressing the non-financial issues associated with retirement, but I would have liked to see more content dedicated to this — like we did at our first retirement seminar.

5 Ways You’re Sabotaging Your Retirement Income Plan:

1. Jumping in Without a Plan

2. Saving “Something”

3. Risking Too Much – Or Too Little

4. Being Too Generous with Uncle Sam

5. Getting Investment Advice from the Wrong Places

This list is “ok” but nothing great IMO.

For the less educated, it’s probably a complete revelation, so perhaps it’s perfectly on target for the people they are hoping to attract.

Personally I’d prefer a list like The Top 10 Factors to Consider Before Retiring.

7 Risks of Retirement Planning:

1. Reduced earnings capacity

2. Visible spending constraint

3. Heightened investment risk

4. Unknown longevity

5. Spending shocks

6. Compounding inflation

7. Declining cognitive abilities

Again, “ok” by nothing revolutionary.

The Online Consultation

They also offer an online consultation — of sorts.

It’s called the Retirement Income Optimization Map.

You complete some information and it spits out a variety of facts/recommendations.

Here’s an overview of the service:

When you sign up for a RIO Map™ you’ll get:

- A 60-minute working session with your advisor to discuss your RIO Map™ and any questions you may have

- An overall Retirement Risks Assessment to help identify any areas of your retirement plan that may leave you particularly vulnerable, and

- A Funded Ratio plan where we’ll compare your liabilities and assets to determine how compatible your goals are with your economic reality.

It also includes these benefits:

The Funded Ratio will help you answer the following questions:

- Do you have enough to accomplish your future objectives?

- Are you overfunded or underfunded relative to these objectives?

- How much investment risk should you add or remove from your investments and earmark into other strategies?

From what I could tell, the only way to get this information is to complete it online and then set up a consultation so they could walk you through it. I was tempted to take one for the team and complete it, but I’ll leave that to you instead. I’ve done enough of these “experiments” lately. Ha!

One thing that’s missing (again) is the cost. It doesn’t say that there’s one but it also doesn’t say that it’s free.

If there is a cost, it needs to be spelled out clearly.

If there is no cost, someone needs to tell these guys that “free” is the most powerful marketing word ever and they need to be using it all over their site.

Anyway, I got some useful information (like the replacement ratio and thoughts on the 4% rule) but not so much that it made any difference in my planning or thinking.

I guess it’s really similar to the retirement seminars in that way — it’s a win if I can come out of them with one or two new tidbits to consider. I don’t have high hopes for much more than that.

What do you think of their conclusions? Have you ever completed an online tool like theirs and had a follow up call with a planner?

I think there’s a real opportunity for you to host some virtual retirement seminars and people would trust and value you because you’re not selling anything. I for one, would be willing to pay and sign up. Make it happen, Mr. ESI!

I’m with Jules —

Making it happen — that’s the key.

I’d be all in.

I actually have a retirement course I’ve been thinking about creating since I haven’t found anything else I really like.

It will be the next thing on my list — but working on something else now.

Look for an announcement in mid-September. 😉

Great news —- thank you.

I’ll be looking for something in mid-September!

I always find discussions around safe withdrawal rate to be interesting, though I’m not convinced that it’s now 3%.

Here’s Bill Bengen, who led the Trinity Study (which gave us the 4% SWR), talking about the numbers a couple years ago on Reddit:

“The “4% rule” is actually the “4.5% rule”- I modified it some years ago on the basis of new research. The 4.5% is the percentage you could “safely” withdraw from a tax-advantaged portfolio (like an IRA, Roth IRA, or 401(k)) the first year of retirement, with the expectation you would live for 30 years in retirement. After the first year, you “throw away” the 4.5% rule and just increase the dollar amount of your withdrawals each year by the prior year’s inflation rate. Example: $100,000 in an IRA at retirement. First year withdrawal $4,500. Inflation first year is 10%, so second-year withdrawal would be $4,950. Now, on to your specific question. I find that the state of the “economy” had little bearing on safe withdrawal rates. Two things count: if you encounter a major bear market early in retirement, and/or if you experience high inflation during retirement. Both factors drive the safe withdrawal rate down. My research is based on data about investments and inflation going back to 1926. I test the withdrawal rates for retirement dates beginning on the first day of each quarter, beginning with January 1, 1926. The average safe withdrawal rate for all those 200+ retirees is, believe it or not, 7%! However, if you experience a major bear market early in retirement, as in 1937 or 2000, that drops to 5.25%. Add in heavy inflation, as occurred in the 1970’s, and it takes you down to 4.5%. So far, I have not seen any indication that the 4.5% rule will be violated. Both the 2000 and 2007 retirees, who experienced big bear markets early in retirement, appear to be doing OK with 4.5%. However, if we were to encounter a decade or more of high inflation, that might change things. In my opinion, inflation is the retiree’s worst enemy. As your “time horizon” increases beyond 30 years, as you might expect, the safe withdrawal rate decreases. For example for 35 years, I calculated 4.3%; for 40 years, 4.2%; and for 45 years, 4.1%. I have a chart listing all these in a book I wrote in 2006, but I know Reddit frowns on self-promotion, so that is the last I will have to say about that. If you plan to live forever, 4% should do it.”

https://www.reddit.com/r/financialindependence/comments/6vazih/im_bill_bengen_and_i_first_proposed_the_4_safe/dlz1l6r/

Much of what’s published on retirement focuses on money. It’s important and it’s easily quantified, so it attracts authors. A lot of folks struggle with money, so financial writing fills a very real need. The “how much is enough“ question can be frustrating and often unknowable. Thank-you for helping to clarify it. But once you’ve acquired enough, there are other issues.

After years of reading, my favorite retirement book remains “How to Retire Happy, Wild, and Free: Retirement Wisdom That You Won’t Get from Your Financial Advisor“ by Ernie J. Zelinski. It deals with retirement life and only touches briefly on money. After a lifetime on the hamster wheel, it can be tough to step out and live freely. Old habits and mindsets put down deep roots. The door to our cage swings open at last and we don’t know how to respond. Zelinski’s book Inspires and encourages us to be free again. I’d be interested in your thoughts on his work sometime too.

Thanks for the reviews. The 4% withdrawal guideline is just that. Some years it’s higher, some lower. I would bet that with COVID withdrawals are quite low given cancelled trips and staying local. The one theory that really resonated with me recently is the concept of “mobile retirement years.” In other words the years in which one is most active. The concept states we have about 20 of these years. As an early retiree at 54 (3 years in now) I think this is a great way to withdraw plan and estimate cash flow requirements vs a constant and annual rate of say 4%. This is the withdrawal strategy we have decided to embrace. I’m just sayin.

Hi, thanks for reviewing Retirement Researcher. I’m Wade, and I see about your request to receive a free copy of Safety-First Retirement Planning. I do have vague recollections of receiving a request like this that I didn’t reply to. I apologize if that was you. I’ll reach out to the email address in your contact page and will be happy to send you an e-book or print version. At 350+ pages, it does obviously go into much greater depth than the brief overview articles you are reviewing here.

Thanks. I’ll reply to your email.

I found JL Collins’ discussion of the 4% rule in “The Simple Path to Wealth” very useful. Pragmatic but still thorough and showed how it’s not really a full blown “rule.”

I bought another of Wade Pfau’s book last year (How Much Can I spend in Retirement). A good introduction to the basic principles of portfolio analysis and the role of Monte Carlo simulations. But a bit repetitive and wordy. And I was disappointed to find in later chapters that the book was an overt advertisement for the author’s professional services.

The question about a safe withdrawal rate is all about risk. A Monte Carlo simulation can provide a dataset that can be used to set a risk threshold for a given portfolio withdrawal rate. I personally use a risk threshold of the bottom 25 % of results in a simulation with ~1000 runs over a ~30-year retirement. Each portfolio mix and other assumptions will produce unique results. For my own portfolio, I am very comfortable with a 4 % withdrawal rate over 30 years and can certainly see how a more risk tolerant retiree could look for more than 4 %.

Thanks for the feedback, Don, as was also shared in many Amazon reviews. Indeed, I learned my lesson that is the only book edition I’ll ever write which included as much description about how our paid tools work. For instance, none of that is in the Safety-First book.

This is directly from the website……Retirement Income Optimization Map 1 $495.00

Couldn’t find it when I looked — and I looked all over.

Note I wrote this post a few months ago and it’s just posting now, so it could have been changed.

I’ll get the book sent over. Our webpage hasn’t been updated in a while, and I will also note that there is a “Contact” button right at the top of the page that would allow you to contact us without having to sign up for the email list.

If you really want to know, you can use wayback machine to find out when a website changed it’s content. It archives and tracks changes of all websites. Just input the url and it will when the changes occured by date.

A couple thoughts:

1. I have read Wade’s work and usually find it useful and thoughtful (and I have read a lot of retirement books both from the $ side and the softer side

2. I’m about to early retire in my early 50s and stuggle a bit with SWRs given current low yield environment (seems govt bonds very very highly valued) as well as high CAPE (above 30) for US stocks. What are other alternatives to stocks/bonds????

3. Are business development companies (BDCs) a potential way to get some yield? Many yield over 10% such as Owl Rock Capital and Goldman Sachs BDC. There are a number of other traded BDCs as well.

4. Is it prudent to put 10% of retirement portfolio or so into a few publicly traded BDCs to get some yield?? This would lower the overall withdrawal rate of the portfolio vs relying on equity dividend and bond interest. Would 10% in BDCs lower the overall risk profile eventhough BDCs share price can be volatile?

Please share your thoughts…..

Wade was recently a guest on episode 271 – “Retirement Planning in 2020” of the Afford Anything podcast. It’s a great podcast and this episode, as the title suggests, is timely. You may not agree with everything he says but it will make you think about some things from a different perspective and I particularly found the discussion on sequence of returns risk very interesting.