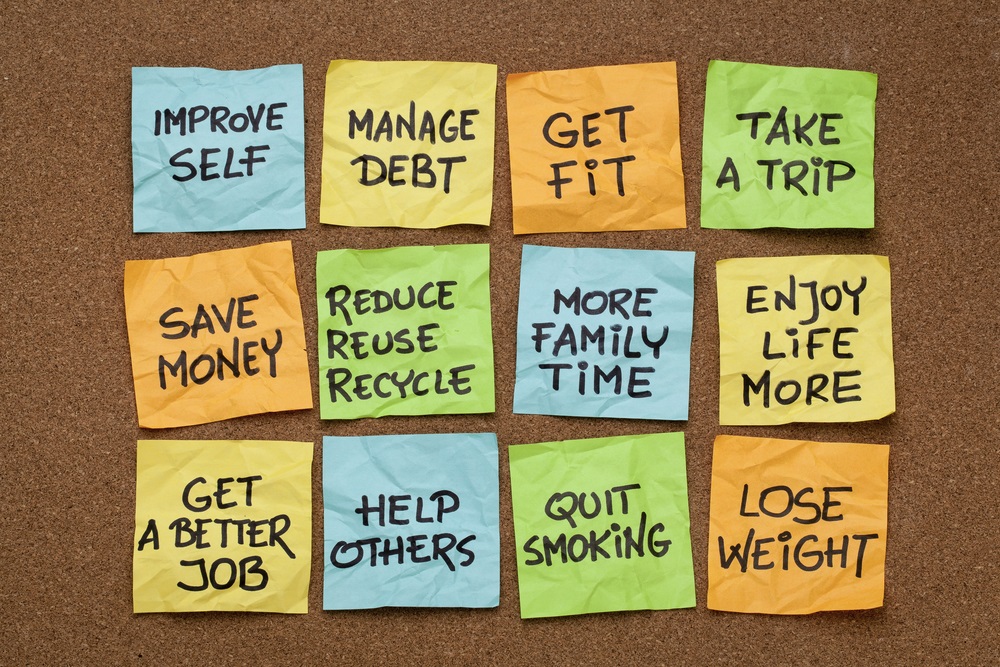

As regular readers know, I’m a New Year’s resolutions guy.

As regular readers know, I’m a New Year’s resolutions guy.

I set tons of resolutions each year, then develop steps to achieve them by the assigned timelines.

Then I track them all on a spreadsheet I review daily.

It’s a bit over-the-top, I know, but it keeps me accountable and on track. I want to be sure I’m regularly making progress on what matters most to me.

I don’t make all my goals but I do hit many more than I would without making them a priority.

Like mine, your resolutions (or goals, if you prefer) for 2018 will be specific to you, of course.

That said, there are some money resolutions that everyone should at least consider when making plans each new year.

I’ve divided them up by E, S, and I as well as “other” money categories.

Here goes…

Earn

Wouldn’t you like to make more money, retire earlier (if you want), and enjoy your job more?

That’s what this set of resolutions is about:

- Grow your career — Ha! You didn’t think I’d skip this one, did you? I think you all know my take on a career by now (it’s worth millions, can be made worth more with seven steps, and doing so will help you get to financial independence earlier). Even if it’s just a few simple steps — everyone should consider taking some action on their careers every year because of the huge impact it can have on your financial well-being.

- Create a side hustle — I love side hustles because they give you options — like being able to retire much earlier. There’s no better time to have started a side hustle than ten years ago, but the next best time is NOW. So either consider some of the side hustle ideas I’ve suggested or create your own and get to it. In ten years you’ll thank me! (BTW, if you’re having trouble coming up with an idea, check out Side Hustle: From Idea to Income in 27 Days

. It will not only help with the idea part, but in developing the business as well. Very good book IMO.)

. It will not only help with the idea part, but in developing the business as well. Very good book IMO.)

These are the two earn areas I think everyone should consider. Get them right and a lot of things naturally fall into place.

Save

Now let’s move on to saving. Here are a couple things to consider each year:

- Get a budget — You can call it a spending plan or cash flow plan if the word “budget” puts you off. But you must know where your money is going if you want to save it and the only way to really know is to track it. That’s what a budget does. For those of you who haven’t yet tried a budget I would say having one was in the top five activities that helped us grow our net worth. And BTW, controlling your spending is my #1 best money move anyone can make. That’s another reason this suggestion makes the list.

- Grow your savings rate — No matter what you’re saving today, you should at least consider saving a bit more. Once you have a budget, go over it with a fine-toothed comb to develop a list of savings opportunities. I’m not suggesting you go crazy, but my experience is that most people save way too little — that’s why this makes the list. As for what to cut and what to spend on, that’s your decision. Just be sure to spend intentionally where you really want to and cut the not-so-important spending.

If you’re looking for suggestions of where to save, review my series on the 52 best ways to save money.

Invest

Moving on to investing, here are a couple you’ll want to consider:

- Review investments — If not more frequently, you need to review your investment objectives and results annually. There’s a balance of how often you should look at them — too often and you’re prone to make stupid changes based on news events that often will torpedo results. Too infrequently and you lose a sense of how things are going. Personally, I “review” my investments (which is really just a quick look at this point) once per quarter. Maybe you will find that works for you as well, but annually is a minimum. This also gives you a chance to rebalance based on your goals.

- Consider alternative investments that support your objectives — For instance, it you’re going to retire in five years, you need to arrange your investments in specific ways which may include considering more income-producing options like real estate. I wish I had consider it earlier in my life and also wish I had bought more once I started. If nothing else, you should think about educating yourself on options (like house hacking, for instance).

That’s about it for investing. Otherwise, just let them sit and compound!

Other

Here are a few other resolutions that should be considered:

- Update estate plan — We are in the process of this since it’s been forever since we did ours. If it’s not something you’ve done recently, and especially if there have been major changes in your life, you should review your plan with an attorney.

- Check insurance — There are two things on this point: 1) review your insurance to be sure it does what you want it to and 2) bid out your insurance as it comes due to keep your company honest.

- Review credit reports — Now that Equifax has shared our data across the Internet we need to be diligent and check all our credit reports annually. This is true even if you’ve frozen your credit reports (as we have). You can’t be too careful these days!

- Create a disaster file — A disaster file goes along with a good estate plan — it helps those you leave behind deal with the financial issues.

- Develop a retirement budget — This is the first step in retiring early — knowing what you will need to spend when retired. If you’re decades away from retiring then doing this is a waste of time, but if you’re within 10 years of retiring (or plan on hitting FI early), you really need to do this. Plus, it’s a lot of fun as there’s dreaming involved. 🙂

So that’s my list of New Year’s resolutions everyone should at least consider.

I’m sure I missed some, so what would you add to the list?

Thoughts? Plans for 2018?

P.S. For those who prefer a video version of this post, see the ESI Money YouTube channel.

Since this will be my first year in semi-retirement I will not be growing my income – it will be cut in half!

However, I do hope to grow my side-hustles. I made around $1400 last year and hope to grow them much higher.

We usually set goals for r those in ESI categories but tend to forget about those in the Other category, thanks for the reminder 🙂

My resolutions for the year are

1. Blog posts frequently (Earn)

2. A dollar challenge (Save/Invest)

3. Trading /investing within my strategy circle (Earn/Invest)

4. Reading (Investing in self)

I have not set my goals very high. I have set them easily achievable for a person who begins baby steps for FIRE.

I didn’t classify my goals until I read this blog post, Thanks ESI 🙂

Something I read back a number of years ago was that new years resolutions should be made to change for the better. The premise was that if you make a resolution to loose weight and you don’t it is a failure. Where if you look at it from eating healthier and exercising more these are positive improvements.

You can apply this to your ESI scale and just about anything. I will be taking steps to improve many things in my life as major milestones have been achieved and major shifts will occur.

Both sons are now done with college and both have jobs. One has moved out and bought his own condo. They will be no longer my dependents but independent son’s.

My wife will be retiring from full time teaching after 31 years. She will explore the world of not having her life revolve around school and teaching.

Big changes in our house hold.

Worthy goals for those looking to be better next year!

Tracking my expenses!

It’s always been a scramble at tax time to get everything in order. Tracking expenses throughout the year would make this time a lot easier.

Fantastic list ESI. This should keep us all pretty busy. The only thing I’d add is the big picture thinking. What are your top 1-3 life goals. Set the rest of your ESI goals to meet those life goals. I missed this big picture thinking for a few years but I’m back on target now!

Great list! Like you said, I think reviewing insurance is really important. I used to work for the insurance industry, and can say that it’s critical to know what your policy covers and what it doesn’t, since finding out that an accident or disaster is not covered after the fact can be financially devastating.

For example, most homeowner’s policies do not cover flood damage. Also, the default, minimal liability coverage on an auto policy can be insufficient if you (or your teenagers!) cause a bad accident.

I also suggest an umbrella policy for everyone. A few hundred dollars can buy millions in coverage.

Agree on the umbrella insurance.

I’d add this to insurance in the Other category: Keep an inventory (list of items, costs, scanned receipts, and photos) of all possessions in your home. It’s a tedious process but it’s important for a home insurance claim, especially after a disaster. We began doing this room by room and dropped the ball.

Thanks for the advice and happy new year!

Good reminder on this. I heard about it before but then spaced off doing it. Certainly for any expensive items, I would think having pictures or receipts will help in getting the most from your claim. Things like a large OLED TV, musical instruments, tools etc. I know you are supposed to get an additional rider for things like jewelry or art, but I’m thinking if you have everything well documented, they might be more likely to bump up your claim a little more. I’ll probably give my insurance co. a call to get more details.

Great resolutions all around. I do periodically visit all of these. Reallocation of stocks occurs 2 x a year but the rest is annually. Having a back up plan for significant others if you are the main household finance person is key…nothing quite as daunting as all of those accounts if someone just lost a spouse and has no guidance.

Very good 2018 Resolutions. Some good ones added by other posters, as well! 2-3 of those are on my recurring list, that I follow each year, updating financial accounts, is included in my disaster plan; compiling net worth info sheet; is included in that document as well. Two goals of mine/ours for the first quarter of year, is estate planning and healthcare advanced directives — to get these document in order/signed! We have reached the age where this needs to be done. Even though my spouse thinks we can wait…I would rather have it done, just in case.

Its all about improvements and making progress. Tracking your spending is a good one. Its easy to get on autopilot and not realize how much you may be blowing in certain areas each year. It will get you to question your habits a little more. I spent how much at the bar last year??? Restaurants/ fast food? Chances are cutting back some is for the better. Spread out your indulgences a little more. Give up cable, satellite radio, or Amazon Prime for a month or 2. You’ll save some money and likely wont miss it that much either.

What a great post! I practically had to beg friends and family to write a will. I was shocked to find out many people do not have one or life insurance. I suggest at least enough insurance to replace 10-25 years of income, which is 10-25 times your annual salary.

Thanks,

Greenbacks Magnet