As regular readers know, I’m a big fan of real estate investing.

As regular readers know, I’m a big fan of real estate investing.

For those who don’t know, you can get caught up by reading why I got started in real estate, how my real estate investing plan came into being, and the results I’ve had from real estate investing.

The summary: It’s been awesome and I wish I had bought more when I had the chance!

I’ve been thinking about ways I could share my knowledge of real estate with ESI Money readers — either adding a real estate option to my selection of free email courses or perhaps even creating a real estate product/class that I could sell.

But as I thought of ideas, I realized my real estate investing experience is both limited (to a specific type of investing) and narrow (I have one given approach and don’t deviate from it). So my experience is not the best to share with an audience that may want a wide variety of real estate investing options and ideas.

Thankfully, I knew someone who could help me out. Chad “Coach” Carson has purchased and managed hundreds of properties as a full-time real estate investor for 17+ years, so he know what he’s talking about. Better yet, I know Chad personally and trust him. He’s the real deal — just the sort of person I’d want to introduce to ESI Money readers.

So I asked him to write this post detailing how real estate could help people get to retirement. For those of you who want a good overview of the options, this post will be a great way to begin considering your real estate investing options.

With that said, let me turn this over to Coach Chad Carson…

——————————————–

Reaching retirement is a lot like an ultra-marathon. The distance from beginning to end is so long that you can’t even see the finish line when you begin! And actually finishing the race can be grueling as you run into obstacles, both internal and external.

So, this article is about finishing that ultra-retirement race. And more specifically, it’s about doing that with real estate investing, one of the most powerful retirement vehicles available to you.

I have personally used real estate investing to “retire” when I turned 37 (I put retire in quotes because I still choose to stay active with work-style projects that fulfill me). And I also studied 25 other real estate early retirees in my book Retire Early With Real Estate![]() .

.

Plus as you may know, ESI Money also used real estate as an important part of his push to the finish line of an early retirement. So, what I’m going to share with you has worked well for me and many others.

Now let’s get started learning ways to finish the retirement race using real estate investing!

Define the Finish Line (aka Financial Independence)

Before we figure out how to get there, let’s begin by defining what we actually mean by finish line.

Although retirement is the topic of this article, I don’t actually like to use that term to define a financial goal. For me, it’s too fuzzy and has too many different definitions.

Instead, I prefer to use the term financial independence. And my favorite definition of financial independence happens to come from the owner of this blog – ESI. Here is his definition:

“Having wealth to cover expenses indefinitely.”

There are three key words in that simple definition:

- Wealth

- Expenses

- Indefinitely

The race you are running is to build wealth. And you must build enough wealth to cover your personal expenses. For how long? For an indefinite period of time so that you don’t run out of money before you run out of life!

Simple concept, right?

But turning the concept into an actual number gets a little more complicated. So, let me briefly talk about something called the 4% rule of thumb.

Approximate Retirement Finish Line – The 4% Rule of Thumb

In the FIRE (financial independence, retire early) community, a common retirement milestone is the 4% rule of thumb (or some variation).

The rule of thumb gives you a wealth building target. It says that you need to build enough wealth so that 4% of your net worth will cover your personal expenses each year. Once you reach that milestone, your chances of not running out of money during a “normal” retirement time frame are good.

Or looked at another way, you need to build wealth of 25 times your personal expenses (1 ÷ 4%). For example, if you want wealth to cover $100,000 per year of personal expenses, you’d need to build a net worth of $2.5 million ($100,000 x 25).

The 4% rule of thumb is a good rough approximation for a retirement finish line. And if you want to be even more conservative, just use a 3.5% or 3% rule (28.5 or 33 times your expenses) to make your chances of never running out of money even better.

But the 4% rule of thumb does have some tricky assumptions and problems if you rely on it too rigidly. You can explore those issues in-depth with fellow blogger, early retiree, and economics Ph.D Karsten from the blog EarlyRetirementNow.com in the retirement withdrawal rate series.

But luckily for you if you plan to use real estate investing to cross the retirement finish line, the math and assumptions get a LOT easier.

Let’s look at how much wealth you need to retire using real estate.

How Much Wealth Do You Need to Retire With Real Estate?

Retirement calculators are helpful in situations where most of your retirement wealth comes from stocks, bonds, and pensions. You must balance your future personal expenses against dividends, growth rates, withdrawal rates, withdrawal timing, and more.

[Note: ESI Money has some great calculators if you are interested.]

But luckily, the real estate retirement math is a lot simpler. In fact, it’s so simple you could do it on the back of a napkin. It basically has 3 variables:

- Your expenses in early retirement (E)

- Your wealth invested in real estate (W)

- The conservative income yield or cash-on-cash return on that equity (r)

The basic formula with these 3 variables is this:

For example, let’s assume you need a minimum of $70,000 per year of ongoing investment income to cover your expenses (i.e. your financial independence number). Let’s also assume you can find properties with a 10% cash-on-cash yield. This means you need to invest equity of $700,000 into real estate.

If that math doesn’t work for your situation, you can change each of those three variables as needed. For example, if your financial independence number is $100,000 per year, you may need to invest $1 million instead of $700,000.

Or, if your financial independence number is $100,000 but you want to be more conservative with your cash-on-cash yield, you may need to build more wealth. For example, if you only receive a 6% yield you’d need to invest $1,666,667.

So, to calculate how much wealth you need in order to retire early using real estate, you start with your personal expenses (E in the formula). Next, you plug in an assumption for the cash-on-cash return that you can expect for your real estate investments (r in the formula). I often use 6%, although it’s certainly possible to get higher yields in real estate. Others may want to use a lower return than 6% to be more conservative.

The result of the simple equation (W) is the amount of wealth you need to invest (if you already have the money) or to accumulate (if you’re growing your portfolio).

And did you notice that even at the more conservative yield of 6%, the wealth you need to accumulate to produce $100,000/year is much less than the 4% rule ($1,667,667 vs $2,500,000)?

One of the major benefits of real estate investing is its ability to produce income at a much higher rate than more traditional investments like stocks and bonds. And this allows you to retire much sooner and more predictably.

And just as importantly for the “indefinitely” part of our financial independence equation, a real estate plan does not eat into the principal of your net worth. You live off of rental income while keeping all of your wealth invested in those same properties.

It’s sort of hard to run out of money when you don’t spend it!

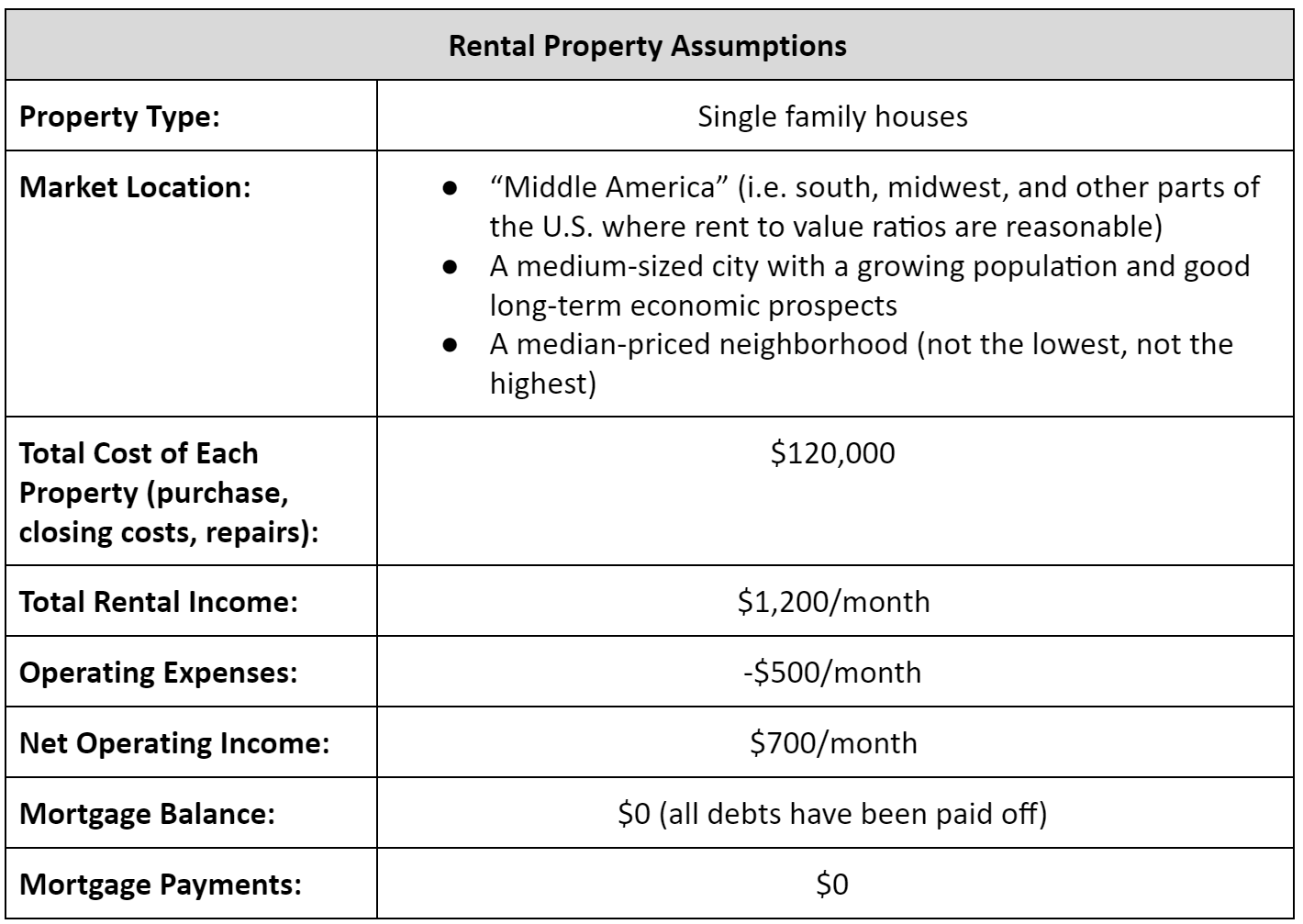

Now let’s look at an example of this real estate retirement income translated to real life. This example assumes you own 10 free-and-clear (no debt) rental properties.

10 Debt-Free Properties & a Comfortable Early Retirement

In this scenario, you own 10 rental properties and use them to retire early. But every example has assumptions. And you need to understand those assumptions so that you can apply the principles and adapt them to your own unique situation.

The assumptions for the rental properties in this example are as follows:

Now, another big assumption is that this is the end of a period of wealth building or growth. You did not begin with this portfolio of debt-free, income producing properties. You had to build it over time.

Later in this article I promise I’ll get to 7 strategies you can use to build a portfolio of free and clear properties and finish the race. But for now let’s look at the income this 10-property portfolio could produce.

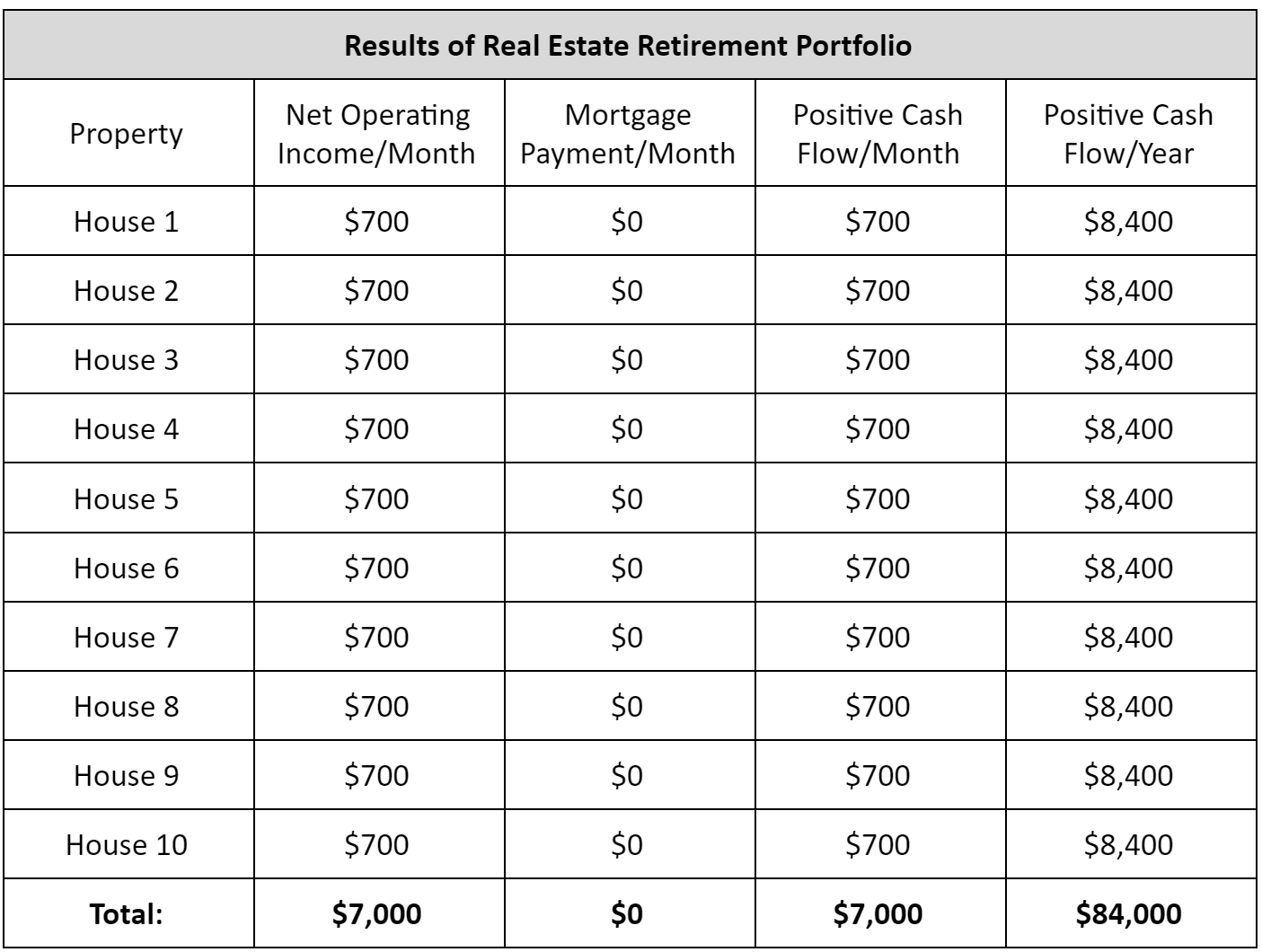

Living Beautifully on $84,000 Per Year

Here are the financial results your real estate portfolio using the assumptions above.

What have you done as an investor in this example? You’ve basically created your own early retirement pension plan.

By investing $1,200,000 over time (10 houses x $120,000), you will receive a consistent stream of rental income indefinitely into the future! And if you bought in the right locations, the rental income will likely keep up with inflation over time so that you can still pay for the same lifestyle in the future.

[Editor’s note: This example matches perfectly with my idea of buying one house per year for 20 years.]

This type of simple portfolio fits ESI Money’s definition of financial independence VERY nicely!

And another takeaway from the example is the simplicity and the power of a real estate-based early retirement portfolio. Managing 10 properties, especially with a property manager, is a VERY part-time project. I personally spend less than an hour or two per week on many more than that.

Yet, the income of $84,000 per year is life-changing. And with solid rentals in quality locations, both the income and the equity in these properties will likely be sustained or go up over time.

So, if one to two hours per week allows for $84,000/year in income, what will you do with the rest of your time? It’s an exciting question that I’ll let YOU figure out in your own retirement.

But now, let’s transition to the 7 practical ways you can use real estate to finish the retirement race.

7 Ways to Use Real Estate to Cross the Retirement Finish Line

You’ve now seen why real estate is a great retirement vehicle. And you also have a specific idea of the type of wealth and income you need to retire using real estate.

So, now it’s time to share some ideas on how you can go from where you are now to crossing the retirement finish line.

I’m going to assume you’ve at least begun the wealth building journey. If you’re brand new, get started with some of the Earn-Save-Invest principles you’ll find on this site.

These 7 strategies aren’t given in any particular order. So, pick the ideas you like and leave out the rest!

1. Rental Debt Snowball

The Rental Debt Snowball is a strategy you can use to pay off your rental properties much quicker than normal. The strategy basically works like this:

- Save cash for down payments

- Purchase several income properties using conservative, low-interest loans.

- Save 100% of the real estate income plus extra savings from a job.

- Use all savings to apply towards one of the loans each month until one loan is paid early.

- Use all savings + new free & clear income to apply towards another loan until paid early.

- Repeat until all loans are paid off.

- The key to the strategy is concentrated debt payoff. Instead of spreading out your extra cash over many loans, you attack one loan at a time and let the cash flow “snowball” or accelerate.

The process is very practical for building wealth and crossing the retirement finish line. Unlike the roller coaster ups and downs of public stock markets or even real estate prices, you control the variables of the plan – how much you save and how much you pay off.

And the process is also very emotionally satisfying as you feel yourself getting closer and closer to the finish line. Like dominoes falling, you get to watch one property after another become income generating machines for life!

2. The All-Cash Plan

The Rental Debt Snowball Plan starts with debt. But perhaps you already have a large chunk of capital to invest. Or maybe you don’t like the idea of using debt leverage in real estate.

In either case, the All-Cash Plan is a variation that could work well for you. And if you use it, you won’t be alone. It’s my understanding that ESI used all cash to buy his own rental properties. [Editor’s note: Yep, this is correct!]

My version of a simple, conservative All-Cash Plan basically works like this:

- Save enough cash to buy one income property (or more than one if you have enough money)

- Save 100% of the rental income plus extra savings from a job

- Buy another income property

- Repeat until your goal for free & clear properties is met

Like the Rental Debt Snowball Plan, this plan is all about snowballing your rental income. But in this case, you’re just saving the cash flow for another cash purchase instead of paying off debt.

So if you’re using this plan to build wealth, the name of the game is patience. You simply find good deals, buy them, save your money, and buy more good deals to grow and compound.

Or some of you might use this All-Cash Plan just to diversify away from other asset classes like stocks. In your case, wealth building may not be the primary need. Instead, you’re looking to reduce overall risk (through diversification) and increase your overall income for retirement.

This plan can work in any market. But it works best in markets where your rental properties produce reasonable cash flow. Some of you, however, may invest in higher-priced markets where cash flow is not as good. In that case, the next plan may be interesting to you.

3. The Buy 3, Sell 2, Keep 1 Plan

With both the All-Cash Plan and Rental Debt Snowball Plan, you need strong rental income to make the plan work. But not all real estate markets or real estate investments produce strong income.

What if instead, you can find deals below their full value (i.e. you purchase equity), but the cash flow may be close to break even. This often happens in high-priced markets like California and in big cities.

If that reality fits your situation, you may want to use something I call the Buy 3, Sell 2, Keep 1 Plan.

The plan works like this:

- Buy three income properties (or some multiple of three)

- Use small down payments plus loans for purchases (if needed)

- Rent for a short period of time (1-5 years)

- Sell two of the three properties, but keep the third.

- Use the net sales proceeds from the two sales to pay off debt on the third keeper property.

The primary goal of this plan is this: buy quality properties at a discount.

The quality properties ensure that you can sell someday, hopefully at an appreciated price. The discount on your purchase gives you a better chance of earning a profit when you sell.

And that profit when you resell is the key. After you pay taxes on that profit, you can plow back the proceeds to pay off the debt on your remaining property that you’ll keep as a long-term rental.

For example, let’s say you earn net profits of $75,000 on each of the two properties you sell. Then together that $150,000 could be used to pay off a debt of $150,000 on the third property.

Essentially you’re using your skills as a negotiator and deal finder on the front end to give your wealth building a boost across the finish line on the back end!

My business partner and I used this strategy to accelerate our own wealth building with real estate early in our careers. And we’ve also used the strategy lately to prune off less-than-desirable rentals and continue to reduce our mortgage debt.

The next strategy also takes advantage of reselling properties for profits. But in this case, you make a lot more after-tax profit by living in the property.

4. Live-In Flips

A Live-In Flip is a strategy for those willing to move into a great real estate deal and sell it for a tax-free profit. If you do this enough times, you can build a large chunk of wealth relatively quickly that can help you cross the retirement finish line sooner.

The key to this strategy is a U.S. tax law that says if you buy and then live in a home for at least 2 out of the last 5 years, you can earn a tax-free profit up to $250,000 as an individual or $500,000 as a couple filing jointly.

My friends Carl and Mindy Jensen from 1500 Days did Live-In Flips several times early in their careers, and that nest egg later grew into a $2 million+ net worth that allowed them to retire early in their 40s.

You will know this strategy is right for you if you have the time and energy to find good real estate deals and/or you’re willing to do repair work. Doing repair work is not a requirement, but it will increase the profit margin of your deals.

The next strategy is also related to the home you live in. But instead of flipping, it involves turning your home into a rental.

5. House Hacking

House hacking is one of my favorite strategies for those getting started in real estate investing. But you can also use it to cross the retirement finish line sooner.

House hacking just means that you live in a residence that can also produce rental income. And the way you produce that income can vary.

The classic house hack is when you live in a duplex, triplex, or 4-plex to generate income from the extra units. But many people are also buying houses that have a basement or garage apartment that can be rented long-term or short-term on Airbnb.

This strategy has a triple-benefit for those willing to try it.

First, you reduce your overall housing cost right now. This allows you to save more money to invest, payoff debt, or whatever your financial priority might be.

Second, if you continue the house hack long-term, it reduces the amount of money you need to save for retirement and cuts the time until your retirement date.

Why is this? Remember the 4% rule or the financial independence number I wrote about earlier? The lower your personal expenses, the less wealth you need to build.

Third, if you choose to move out of the house hack you now have a long-term rental property that can produce income for you over the long-term.

Now let’s look at one more strategy that uses your home to help you cross the retirement finish line earlier.

6. Downsize Your Home

As much as I love turning your home into an investment (see House Hacking and Live-In-Flips above), most people’s homes are NOT a good investment.

Why not?

Because once you’ve owned it for a while, the price appreciates and you build a lot of equity (i.e. the difference between what the house is worth and what you owe). Any typically, this equity is sitting dormant and not being invested optimally.

So if you are willing to capture that equity by moving and downsizing, you can invest the equity to help you cross the retirement finish line sooner.

For example, let’s say you own a home worth $500,000 that has no debt. And let’s say you could be happy with a smaller home worth $200,000.

If you invested that difference of $300,000 into income-producing real estate with a 6% income yield, you’d earn an extra $1,500/month! For many of you, that’s as much as you’d earn from social security. And it could be the difference-maker to help you cross the finish line.

And beyond the financial benefits, you might also find that simplifying your life by downsizing your home frees up your mental energy to explore and enjoy your new found free-time in retirement.

The final strategy is more of a side-hustle than an investment, but it may be beneficial for some of you.

7. Start a Part-Time Real Estate Business/Career

I look at real estate as a hybrid between a start-up company and a pure investment. If you want to be a completely passive investor, you can. But if you want to earn active income, even part time, you can do that too.

Here are a few ways that you could make a side hustle career out of real estate:

- Property management – both your own units and units of others

- Real estate sales – getting your real estate license can be a fun and profitable way to earn money when you’re already involved in the real estate market anyway

- Flipping houses – the business of finding, fixing, and quickly reselling houses can be a profitable venture – either part-time or full-time. If you choose to flip houses, I recommend studying my friend J Scott’s The Book on Flipping Houses

.

. - Wholesaling – if you’re good at finding real estate deals, you can buy low and sell quickly at a marked-up price to other flippers and landlords

- Project Management/Contracting – if you love rehabs, you could manage remodel projects for others for a fee. You’ll likely need a contractor license with your local state

Now you might be saying “THIS isn’t retiring if you’re still working!”

This is true. But the point of retirement for me isn’t to not work. It’s to spend your time doing what you love!

And transitioning to a semi-retirement arrangement like this can often get you out of a career or job you feel stuck in.

If you can earn just an extra $30,000 per year, that’s the equivalent of $750,000 you don’t have to save using the 4% rule of thumb (i.e. 25 x $30,000 = $750,000).

That relatively small side-hustle income essentially buys you freedom to make a move. And that can be a big deal if you want to retire early and not wait decades to access retirement funds in a 401k or IRA. [Editor’s note: This is the same principle I talked about when I wrote how a side hustle can get you to financial independence in 10 years. In this case, your side hustle is real estate!]

Conclusion

You’ve now learned how to use real estate investing to get across the retirement finish line.

We started with defining financial independence and identifying how much wealth you actually need to retire.

I then shared an example of a simple portfolio with 10 properties that could produce $84,000 per year in retirement income.

Then we went through seven strategies that can help you build wealth in order to close the gap between where you are now and your retirement goal.

I hope these ideas have given you some practical insights and some inspiration if real estate is part of your retirement plans. I’d love to hear from you in the comments below if you have questions or thoughts for me.

And for those of you who want a short video summary of these principles, your wish is my command!

Great tips on real estate. The key factoid you metnioned that got me started in real estate a few years ago is that once the system is set up, you don’t need to dip into the principal. With stocks the SWR 4% rule has you selling some each year to make up the difference between the yield and SWR. So eventually your capital diminishes. With real estate, if things go well (and of course that is a big IF) you theoretically can live off the positive cash flow from rental income.

The things that can derail you with real estate can be planned for with a sunk cost fund (HVACs, roofs, etc will eventually need to be replaced). People get in trouble when they assume every dollar they collect in rent can be spent without setting aside some for these big ticket items.

“a sunk cost fund (HVACs, roofs, etc will eventually need to be replaced)” Good point. Sounds like a Reserve Fund. Smart HOAs have one.

https://www.investopedia.com/terms/r/reservefund.asp

Your point about planning for those big costs is right on. I think one of the biggest mistakes new investors make is not running the numbers correctly. Just to make a deal seem like it’ll work, people conveniently ignore future replacement of roof, HVAC, driveway, etc. But if you build those costs into your cash flow model and set money aside, the ride becomes much smoother.

I’m curious if anyone has been able to generate similar returns on homes in vacation areas with shorter seasons. Or, what the economics need to be to make it work.

Thanks-

Hi, thank you for the very good detailed post. I live in Asia and have been thinking of getting in to real estate to make the retirement goal faster. Can you use these same techniques with lands instead of rental properties?

If not, is there a different technique/formula that you would recommend?

Thank you once again!

Fantastic article, this is what I love about real estate. It’s simple and easy to understand. Your numbers and examples are fairly representative of what you can find in my market. I like how you illustrated you don’t need 50 or 100 units to be comfortable, nothing wrong with that but you don’t have to go that big if you don’t want to.

Im looking to form a similar RE portfolio but instead more passive with a combo of RE Syndications and Note investing Funds that gives off “Passive income”. Slightly less upside but more hands off.

Duke