It’s been two and a half years since I retired! Where has the time gone?

It’s been two and a half years since I retired! Where has the time gone?

I’ll tell you where it’s gone — into fun, relaxation, and enjoyment! LOL!!!

For those of you who are sticklers, yes, it’s actually been two years, six months, and five days. But who’s counting? 😉

Since my retirement day I’ve given an update every six months just to let everyone know how it’s going.

Today we’ll do the 2.5-year anniversary version with details of what’s happened since my last update in August and the mini-update over Thanksgiving.

To make this summary easier to read, I’ve put my thoughts into categories.

Here we go…

Life

- Things have remained very busy in retirement, though I have a wide open time of little activity for the foreseeable future (I do have a trip to FinCon set for September). If past history serves, that opening will soon be filled up with some to-dos, travel, a guest visit or two, and something totally unexpected. It remains a fun busy though (for the most part) and I still wish I had jumped into this lifestyle a decade earlier (which I could have since I was FI then.)

- It took a couple years, but the retirement life seems normal now. I no longer have that “Christmas morning” feeling every time I wake up, so I guess that’s the most visible sign. I’ve even been sleeping in more normally until 6 am or even 6:30 am on some days rather than getting up at 5:30 am or before like I did the first two years. Gasp! I’m losing my edge and becoming a bum! 😉

- Anyway, I do love the mornings as they are nice and quiet.

- I still have my Christmas tree set up year around. It’s on a timer so it’s lit when I come down each morning. So cheery! I did take down the Christmas lights on the stairs since leaving them up would be more than my wife could take.

- Like last year, we went back to Grand Cayman last month and had a blast (again). It was a bittersweet trip as it might be the last we do for a while (or ever) with both my kids and parents. My parents are going to start their RV life in the spring and at least one of the kids (if not both) will be working full-time. It’s the circle of life, I guess.

- The Colorado winter has been brutal so far — much colder and snowier than our other three winters here. But living in Michigan was good training and we can handle both cold and snow.

- Christmas was spent with just my immediate family. In the past my parents would have joined us, but since we were going to spend 10 days in Grand Cayman with them a couple weeks later, a trip for Christmas wasn’t in the cards. It was a nice, quiet Christmas. I’d love to take a Christmas cruise BTW, but not sure I can convince everyone else to do so. Anyone ever done that? If so, how was it?

- I wanted to start giving in different ways this year so in addition to my larger gifts through our donor advised fund, I started some small giving as well. This manifested itself in a few ways. First, I started leaving 30% tips when we ate out in November/December with a “Merry Christmas!” on the receipt. Second, I bought a pack of $10 Amazon gift cards and gave them out to people at the gym (friends and workers there). Everyone was quite surprised and acted as if I had given them $100,000. It was heartwarming to see their reaction. Third, we sent larger e-gift cards from Amazon to a neighbor, our pastors, my real estate management team, our CPA, and a few others (though we’ve done this for many years — it wasn’t new.)

- We did give some surprise larger gifts too. The backstory is that we’ve been working on our estate plans and talking about where our money goes when we pass. As we chatted about it, we decided to give some of our money away now at Christmas. So we sent $1,000 to each of my wife’s four siblings, to my dad (not my mom as we were taking her and my step dad to Grand Cayman), and a small church in Iowa that my parents attend. As you might imagine, the responses were “interesting”. Most wondered why we would do it and when we explained we just wanted to bless them, they seemed to accept that. I’m not sure how they each spent the money or if we’ll do it again, but it seemed right for this year.

Retirement Explanation

I keep playing with how to tell someone I’m “retired.” The main problem is that I look much younger than I am, so saying “I’m retired” makes people’s heads spin and then leads into details, a longer chat than I want, and so forth.

So I’ve dabbled with a few options like:

- “I’m financially independent.” — It’s true, but sounds pompous IMO, especially when I do it in a Thurston Howell III voice. 😉

- “I live off my investments/real estate.” — Also true (at least in part) and a bit less pompous. But still doesn’t get to the heart of the matter.

- “I run a few websites.” — Also true but gives the impression that I’m still at work 40+ hours a week, only run the sites for profit, and am not retired in any sense — all of which are far from the truth.

So I mostly go with “I’m retired.”

This leads to “How could that be?” (like it’s some sort of impossibility). I do have a decent answer for this. I usually say, “I earned a good amount, saved a ton of it, and invested wisely.” (Wow, someone should start a website based on that!) 😉

They generally nod at this point and the conversation then spins into, “What do you do with your time?” My mood at the moment mostly determines how I answer this but my favorite response is from a friend’s friend who is retired, “Whatever I want.” Ha!

BTW, I often get the reply, “Were you military?” when saying I’m retired since we have an Army base and the Air Force Academy in town. Plus I have short hair, so I look like I fit the mold.

Family and Friends

- My wife is still working 15 hours a week at our church as it gives her something enjoyable to do and she’s awesome at it. She’s also taking some classes online about teaching kids so she’s quite busy.

- My son now has two jobs. He’s selling phones at Costco (and did quite well over Christmas) but since they don’t seem interested in giving him full-time hours, he also found a job at the indoor electric go-cart place near our house. They may open up a full-time slot for him, but if not we’ll be looking at options this month. He needs (and wants) to work full-time as it’s his first step on the move-out plan.

- My daughter graduated college in December and plans to move in with a friend this month. I’ll be posting on the college process and how my daughter did it all, but for now let’s just say between the college incentive and the car incentive, she ended up with over $40k cash, no debt, and title to the $10 car we got from my uncle. Not bad at all.

- She’s looking for a full-time job but is also helping me at Rockstar Finance which covers a good amount of her expenses, so she’s not in too much of a hurry.

- BTW, if you recall, we drove her car out to Virginia in August so she could have it for her final semester. Since we didn’t want her to drive all the way back alone, I flew to Louisville on December 5. She picked me up at the airport around 5 pm (she had already driven several hours by that time) and we drove a few more hours into Illinois. We stayed overnight in a hotel, then drove 12 hours the next day to get home. It was a long trip but glad we did it in two days.

- We found out a good friend of ours has brain cancer. It’s not clear what will happen, but it’s another reminder that life is short. It makes me glad I retired when I did. Nothing in life is guaranteed.

Health

- I am still working out and even upped it a bit the past few months. I do weights and cardio each three days a week, but I also added some extra cardio-focused calisthenics to my weight days to get my heart moving every day.

- I also walked a ton this past year, averaging just under 17,000 steps a day for those who like specifics, here are the numbers from my phone’s app (note: these are the numbers from when I had my phone with me — there were times, of course, when I did not have it): 6.1 million steps, 4,226 flights, and 2,250 miles. When I look at this it seems that I might have walked more miles than I drove in my car if you take out the really long trips and just count “around town” driving. Most weeks I only drive my car to church and back and maybe a meeting (if it’s a rare week I have one). Otherwise, I walk to the gym, walk to the grocery store, etc. We do take my car to the airport and on trips where there are several people as it’s larger (Toyota Highlander.)

- I had a physical late last year and received a set of to-dos from my doctor. I completed most of them and will be going back next month for a follow up. My cholesterol remains borderline (it’s been around 200 for years) and we’re discussing options for how to handle it. The good news is that I have managed my diet better and am down five pounds from my doctor’s visit. He wants me down five more, so we’ll see.

- I also have a six-month dermatologist appointment in March to check me again after having basal cell carcinoma a year or so ago.

- One area of fitness I think about is keeping my mind strong. I think writing and running a couple sites helps, but as a supplement I do three chess puzzles every day. Anyone else think about this? Any tips for how to keep your mind at peak performance?

Entertainment

- We’ve cut back a bit on movies in theaters (more of a reflection of busy lives and not great movies than anything else) and spent most of our screen time watching Hallmark movies. We recorded all of the Christmas ones this year (of the 475 new ones they had out — or at least it seemed like that many!) and we’re still watching them. We also watch Gotham (last season!), America’s Got Talent (new to the winter), When Calls the Heart, Shark Tank, and a host of island-focused house-hunting shows. We record everything and skip the commercials and we always have a lot to choose from.

- I played a TON of video games this past fall — something I certainly would not have done if I had not been retired. In my Thanksgiving update I noted I had played Spider-Man

for 56 hours the first time, then about 20 hours the second time before I moved on to Assassin’s Creed Odyssey. I played that one 115 hours before I maxed out my character the first time and am now 53 hours into the second game with about 25% left to max out. I enjoyed both games a lot (as you might guess) and may even play one or both of them again one day.

for 56 hours the first time, then about 20 hours the second time before I moved on to Assassin’s Creed Odyssey. I played that one 115 hours before I maxed out my character the first time and am now 53 hours into the second game with about 25% left to max out. I enjoyed both games a lot (as you might guess) and may even play one or both of them again one day. - I have been “reading” a lot — and by reading I mean listening to Audible. In particular I listened to a 24-hour series on the Civil War (American Civil War — this is the course on DVD — I listened to the audio version). I have been a student of the Civil War on and off for a few decades and this was BY FAR the best thing I’ve heard/read on the subject. It had so many details and insights that added a whole new level to my understanding.

- In addition to listening I’ve read some really great money books lately including The Next Millionaire Next Door, Everyday Millionaires, and Financial Freedom: A Proven Path to All the Money You Will Ever Need. It’s been some time since there were this many new, great, money books.

- One area I’ve cut back on is podcasts. The ones I liked went off the rails in some way — didn’t tell me anything new, spent too much time on blah blah blah instead of getting to the content, got too political, etc. — and that’s when I moved to Audible. So far I haven’t gone back.

Market Meltdown

The biggest money news in the past six months has been the huge stock market drop in December (and the on-going drop before that). I have a few thoughts on this.

First of all, we took it on the chin financially. From the peak in August to the lowest day last year, our net worth was down $500k. Yep, half a mil.

Second, this did not phase me a bit. Why? A couple main reasons:

- We earn more than we spend. Our assets (like index funds) are just there growing (or in this case declining) and are ancillary to our finances. Sure, I’d rather be up $500k than down $500k, but no matter what the market does it does not impact me in the slightest.

- I have built in several margins of safety. The biggest one is we could probably cut our spending in half if we needed to and the rental income from our properties would cover that by themselves.

Third, you should have seen the chatter amongst FIRE bloggers during the drop. You would have thought the world was coming to an end! I suppose if you planned poorly and had your budget stretched to the max, then the world was coming to an end. But that’s the case whether you have a job or not. If everything has to go right for you to be “ok” financially, your house is built on sand.

I think many bloggers whined about the drop because IN THEORY they had all their ducks in a row, knew they would not panic, had it all covered, etc. but when the drop actually happened they crumbled like a house of cards. This, my friends, is the difference between theory and reality, between education and experience. If you plan for reality and base it on experience (or at least a solid theory you’re willing to stand behind), you shouldn’t have catastrophic problems.

The situation made me think of a couple quotes. First, here’s a classic from Mike Tyson:

Everyone has a plan until they get punched in the mouth.

Haha! So right.

And here’s one I found on the 1500 Days site:

Tyrion Lannister: l’m the captain of the ship, and if the ship goes down, l go with her.

Lord Varys: That is good to hear. Though l’m sure many captains say the same while their ship is afloat.

In other words, it’s easy to say one thing when all is well, but what do you say (and do) in times of trouble? Often that is quite different.

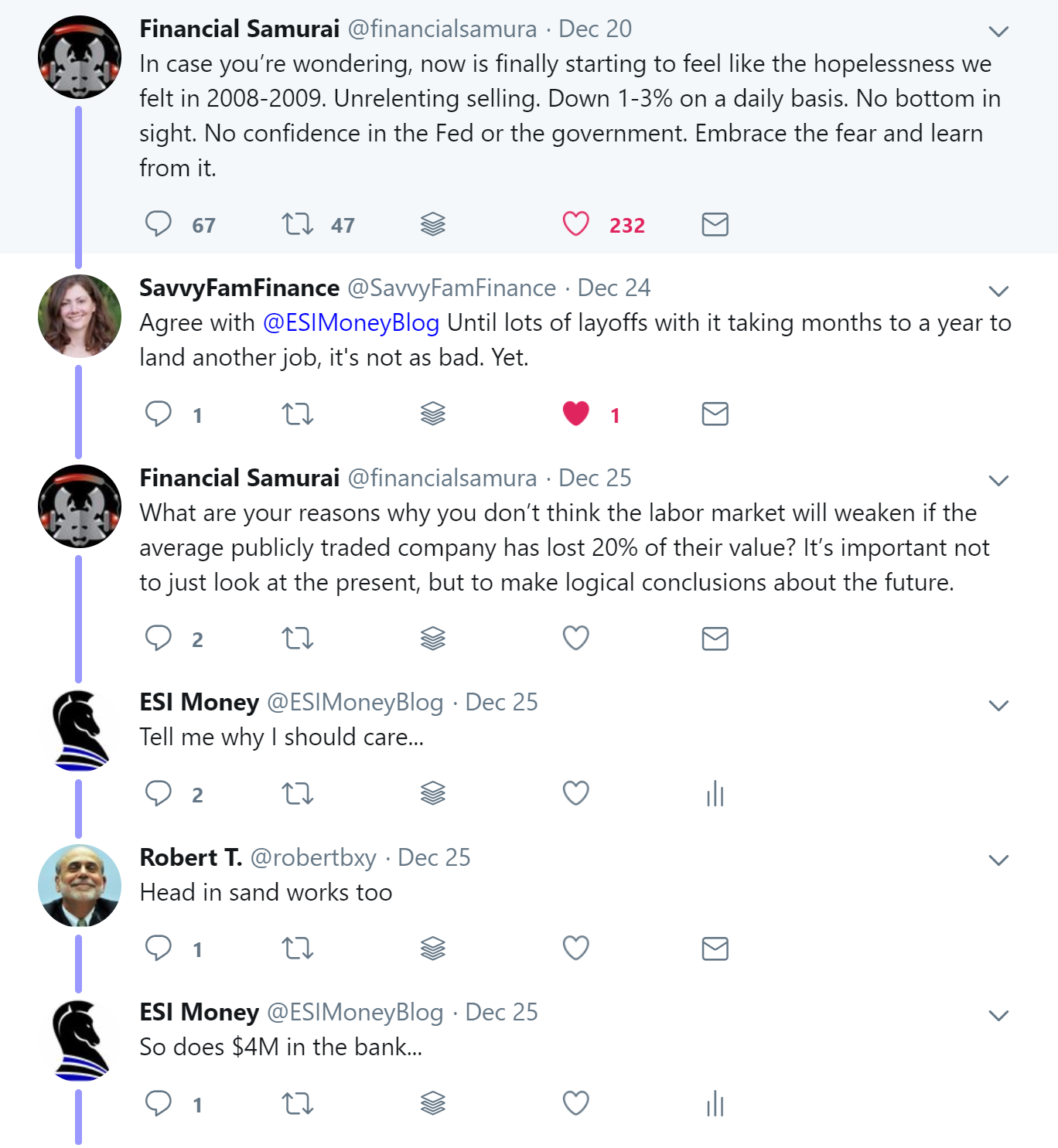

One of those who was the most “panicked” (I put that in quotes because you never know if he’s serious or joking as the combination of writing and his style makes it hard to tell true meaning — I think he does that on purpose, BTW) is Sam from Financial Samurai (which is to this day one of my favorite sites). I’m sure that he isn’t panicked personally because he’s loaded (he makes me look like a pauper), but he was sure stirring the pot (another one of his specialties — on purpose again) during the drop. Here’s one of our conversations during this time:

My points in this all (which are hard to get to on Twitter) were:

- It did not seem like 2008. I didn’t see big companies failing, politicians from both parties coming together (heaven forbid!) to figure out what to do, and real estate prices falling like crazy and foreclosures going up. None of that happened this time and all did in 2008-2009.

- Why should I care? See above. Income over expenses. Tons of assets to boot. Margins of safety. So why should I care?

- Robert T is a troll. Classic example — always critical with zero solutions.

IF (and this is a big if) it ever was like 2008 or ever gets like that, I’m actually ready to pounce. I have a ton of cash saved and would buy properties like crazy if they dropped off the face of the earth. So bring 2008 on and I’m ready to buy.

Again, if your finances are built on a house of sand, then you might have been worried. But if you do it right, you build them on solid rock — which would require a massive hit to make a dent. This is what I do, it’s what I recommend, and thus I sleep well at night.

All this to say watch out for those who play at finances, hold themselves out as experts, and then panic at the sight of some trouble.

Ok, that’s enough ranting. This is supposed to be an update!

Finances

- On the income front, things are going quite well with both ESI Money and Rockstar Finance (revenue has been higher than expected and costs have been lower). I’m in the midst of year-end numbers and taxes, so once I get things to a place where I can share specifics, I will. BTW, if you want to get an email every day with the best personal finance posts, you can subscribe to the Rockstar Finance newsletter. We’re running the Rockstar Rumble currently (you can read all the posts here) so there are lots of great articles from 2018 as well. And we’re also offering 30 Days to Great Finances in case you or someone you know is interested.

- We started an estate plan update in the fall and are now in the final stages of it. So many decisions to think through requiring lots of conversations to get everything right.

- I still update our retirement budget every month and I’m still pulling money out of Lending Club and Prosper. I’m down to about $20k with Lending Club and $10k with Prosper. I will keep withdrawing until nothing’s left.

- One interesting money-related medical event happened recently. My doctor recommended a colonoscopy (I know, the joy…) so I called to set up an appointment. I told them I was a cash-pay customer and wanted the price before I committed. She gave me the details and they added up to around $1,000. I asked her if I got a discount for paying in cash and she said, “Oh, yes. If you were using insurance the cost would be over $3,000.” How CRAZY is that?

- I’m still on Facebook and Twitter and have ramped up my Pinterest game as well. You can follow me on any of these if you like. If you want to follow Rockstar Finance you can find it on Twitter and Facebook.

So, that’s my retirement life lately.

Any thoughts or questions?

“$4M is nothing, it’s peanuts” – Suze Orman

🙂

Haha! I’m sure she would say so if she was a reader…

Good for you. Sounds like you have settled into retirement life nicely. From a professional standpoint, excellent with walking and strength training. Add stretching along with hydration and you will age well.

Weightloss: Yeah, I recently got that same talk from my MD. Have been reading the book Mini Habits for Weightloss. Might interest you. I found it workable to add just one more fruit and vegetable daily with the habit growing from there. Also added drinking more water through a fun app called Plant Nanny. The body really does feel better when fully hydrated on a regular basis.

I’ve lived through several market corrections. I definitely remember 2008 due to finally having invested a lot of money by then. My financial planner did his review of our plan in December and started with checking with me how I was doing emotionally with the drop. He quickly realized that I was as I had told him I would be just okay with it all. The market will come up and I feel blessed that I have enough money to lose that amount in the drop. I continue to put the same money away in the same diversified index funds and stick with the plan.

Agree about the financial podcasts. I’m basically down to two now and one of them I wade through the muck to just listen to one of the co-hosts when he is on. Still regularly listen to The Money Guy podcast.

Enjoyed your update and it helps me with my focus on retirement in the near future.

Thanks! I’ll check out the book.

That was a great tidbit of learning that you like to play video games, I would have never guessed 🙂 (I play occasional video games with my daughter, but it has been a decade or more since I was more into them).

The important thing you are doing is keeping your mind and body healthy in retirement. That is one of the factors that has shown to prolong longevity. There have been studies that came out that people who retire early actually die younger than those who work to more traditional ages and that was the underlying reason (lack of social activity, mental and physical deterioration).

I love reading these detailed posts, I love the reminder of “I should have done this earlier”. Its time to pull the plug. The form of charity is awesome, I will need to do something similar because I will miss my work expense account that I’ve been doing this on for people who’ve helped me around the office.

The market commentary was interesting too, I tossed money into the bear market with both index funds and banks and my personal finance coherts among others would tell me just how crazy the idea was.

Love the comments about video games, that’s near the top of my list to pickup again

I have a video game post coming up that gamers should love! 😉

Being in a similar position regarding outlook (and assets), when my spouse asks me a simple question like our options for dinner, I find myself giving a truncated folk song reply, “Jimmy crack corn.” Which is to state my feeling of indifference [“Jimmy crack corn, and I don’t care”]. It’s my same response regarding the current macroeconomic status. It’s why we built our asset “moat.”

[A reference to a folk song heard at campfires years ago as a child. Please don’t misinterpret.]

Regarding your cholesterol, I highly recommend watching forks over knives on Netflix and reading ‘The China Study’, best investment of time I ever spent helping me drop my cholesterol down to 110 without medication just through diet change.

Wow. I’ll check those out!

Great post! I look forward to your retirement updates.

Glad I am not the only one who plan logs a lot of hours on video games. ?

I agree that the dip was in now way as bad as 2008. I work in real estate (and am working on safe guards should it happen) and we just kept selling homes. No real difference.

Thanks for writing!

>> Any tips for how to keep your mind at peak performance?

Learn new skills (Mike Boyd on YouTube is a great example). Do things with your non-dominant hand (brush teeth, etc.). It’s amazing how learning some new skills really helps.

You got it! Left hand brushing for me from now on!

I enjoy reading these updates. They’re motivating. Your retirement sounds a lot like what we are planning, though we’re still several years out. I know I’ve mentioned it before – but I really appreciate your commitment to giving and I liked seeing the ways you are adding to that.

When you mention cutting your spending in half if necessary, would that primarily be travel expenses? How does the giving fit into that? Just curious as we’re still building all of our own margins of safety into the plan.

Thanks for these updates!

It’s everything. We don’t budget and I know we could cut almost every expense if we were forced to. We are nowhere close to tightening our belts.

But since we don’t need to, we don’t.

Nice update. I’ve recently made an “investment” in me (even though I’ve been a long time active cyclist for 25 years). I hired a nutritional coach and a cycling coach (mainly to polish up the nutritional end).

I hired a company called MetPro (MetPro.com). I have no financial interest in them. Check them out. Results have been fabulous. Weight loss, body shifting, muscle gain, etc etc.

Best “investment” I made in me. We all save butt loads of money, but if aren’t “optimally” healthy, doesn’t matter.

Thanks again for the update and glance in.

Ron

I will. Thanks!

Great post! At about 9 months into my “independence” (I’ve been playing around with alternatives to using the R word, too :-), I’m curious to see what others are doing, how their using their time, reacting to market ups/downs, and what they’re using for income streams. Property investment seems to be a theme – so maybe that’s something I should get up to speed on (never figured it out while I was working).

Brain games, keeping sharp:

1. Ken Ken – just do it! NYtimes publishes a couple of these in the Sunday Magazine each week; and there are other online sources. Best to play it on paper. Excellent brain sharpening tool.

2. Bridge (card game) – possibly the most intellectually demanding game I’ve ever played. And social, too, if you get involved in a bridge club and play duplicate. Lifelong game. Wish I had started playing in my 20s like my parents did. Find local source for lessons and go from there. http://Www.acbl.org

Thanks! Appreciate this!

Now, now. I said “starting to feel like.” Starting is a key word here! And it absolute did start to feel pretty dire with the daily 1-3% moves down with no explanation.

Thankfully, the markets are back up and we’re all rich again, WHOO HOO! Surely you make up at least $300K from the $500K loss?

Always keep hustling folks. Don’t regret not taking calculated risks.

And if you lose all your money, take solace knowing you can start all over and rebuild again. This is America.

Sam

Hahaha! I knew you’d have a loophole! It’s that ninja/judo wordplay you have mastered. 😉

Yes, up nicely since the bottom. And still hustling!

For keeping the mind in shape, I like language learning. My wife and I plan to travel, mostly to Spanish speaking countries, and I want to be able to communicate but also like the “badassity” of always learning something new.

I have thought about this as well. Spanish seems like the most useful language, but others appeal to me as well. I’ll think it over. 😉

This was a fun read. It seems like you are really enjoying your retirement. Handing out Amazon gift cards is a nice way to give back!

Financial Samurai is one of my favorite blogs as well. I believe most of what he writes has a sarcastic undertone to it, but he always has some unique perspective I love.

Yes, I think much of it is sarcastic. But he does it so well!

I enjoy your website. I discovered it a few months back and have read all of the interviews and most of the content. One of these days I will have to take the time to complete a millionaire interview.

Your Son should try to get on with Costco (not the phone kiosk). It is a great company, with great benefits and plenty of room for a growth career. FT sometimes takes awhile to achieve, but PT is guaranteed 25 hours a week at a good wage that increases based on hours worked.

He’s tried that but with no success so far. I’ve heard it is a great company and would love to have him work there.

So I mostly go with “I’m retired.”

This leads to “How could that be?”

What they are really asking is, ‘how can it be that I am not retired, and this guy standing in front of me is?” Same with the ‘were you in he military’? inquiry, they are asking if you have a pension. They are looking for an explanation for why they have to get up tomorrow morning and go to work. Am liking your attitude with the banter!:-) It must feel good to flex that ESI freedom!

I kind of enjoy it as well! 😉

Hey ESI

Really enjoy these updates so hopefully you can continue and interesting to hear some of the options for “I am retired” as well as good for you to stop the twitter troll in his tracks. I am getting mentally prepared and learning some of what to expect when I decide to join you in the RE part 🙂

Similar to you, I lost 568K in Oct/Nov/Dec and even although I was up 541K for the year prior to give it all back it still “hurt” but definitely did not feel like 2008 and my plan (even though I watch daily) is to stay the course and have a multi year horizon. That said the joy of gains is never equal to the pain of losses which is human nature but you can control your reaction and spur of the moment decisions are often not the best in retrospect. The stay the course worked will as was up 472K in Jan and back near my all time net-worth highs. On a side, as someone who 20 years was clipping coupons it is hard to mentally digest when the $ fluctuations get bigger as you are talking in terms of houses/cars ups and downs.

Some will find it interesting but in December in the midst of all the “paper” loses when some would be cutting back my wife and I agreed to do a bathroom remodel we had talked about for years. My thinking was it is small in the scheme of these big loses 🙂

Thanks again.

Millionaire 73

https://esimoney.com/millionaire-interview-73/

“I think many bloggers whined about the drop because IN THEORY they had all their ducks in a row, knew they would not panic, had it all covered, etc. but when the drop actually happened they crumbled like a house of cards. This, my friends, is the difference between theory and reality, between education and experience.”

Loved this quote. As you know, I’ve been saying this for a while now. I’ve written a couple of posts about it. In one of those posts, I said, “Buy low and sell high works. Until it doesn’t.” Many of the FIRE bloggers experienced real market drops for the first time. It was nothing like 2008.

But come on, man, as Dave @accidentalfire reminds us, Suze Orman says $4 million is nothing. Get to work, man.

I saw paper losses from peak of more than 2x annual household income (pre-tax) by Dec end. To me, it’s just another test of whether you’re willing to stick to your portfolio strategy and whether you have a sound plan to tolerate downturns. As for me, I hold sufficient assets in “safe” investments that I can use in market downturns that last 5+ years so I just let the market do what it does short-term. In fact, when the market dipped low enough for me in mid-December, I increased my position in stocks (mostly index ETFs) using some of that cash reserve since I’m still working and don’t even spend close to everything we earn.

Neurologist said to keep brain fit

“get good sleep, get physical activity, socialize with people, learn new things, drink coffee and take Vitamin B12.”

I enjoy reading your posts. They are very motivational and keeps me focused on my own retirement goals. My 2 cents on the cholesterol, my wife got me eating oatmeal + fruits for breakfast everyday, but my workout routine was the same, and that drastically lowered my cholesterol. Now I am tell all my friends to eat oatmeal! 🙂

I have been looking for tools to help me track net worth (from various banking and investment accounts) and see year over year progress. Besides, doing this in Quicken, Personal Capital or Excel, I haven’t come across any other solution. I am curious how others track their net-worth. Are there other options?

I use Quicken but I hear people love PC.

Why wouldn’t you use one of these?

I use Quicken, but I am not a fan of their new yearly subscription model. It now forces me to purchase every year, whereas before I could update when I wanted. With PC, I am weary of how they are selling my data for a “free” service. Plus if their system was ever to be hacked then all the financial accounts get compromised.

Do you know how many gamers you could educate and turn FI if you streamed and talked about FI at the same time? Hahaha!

About keeping your mind sharp. My wife does the NY Times Crossword app. It’s about $0.50 a month or year or something ridiculous. It keeps track of your streak and has every crossword in the archives. Many of them are clever. My wife had a streak of 280 days and then her phone got trashed so she lost it lol. But she keeps doing it! I am not good at them but if you like them, check it out!

Love the updates, keep em coming!

PS. I missed the Anthem demo. It had a demo weekend and I assumed I could play at at my liesure but missed it due to some side hustling haha. If it goes on sale sometime I might check it out, or if my PS Plus membership gives a discount.

For brain fitness, there are tons of free how-to’s on youtube. I started with how to play piano by ear, got side-tracked on lessons on chords, and I’m learning a lot that my basic piano lesson books never bothered to explain. I’m sure you could find lessons on absolutely anything.

There are also a lot of websites that have exercises and games for brain training, I think they’re fun and challenging. Since I am (was before I retired) a computer programmer, I’ve decided to start writing some of my own. It seems like a good way to keep contributing.

We retired about the same time. And both of us appear to be enjoying it. One difference is I consult a day a week which covers our family expenses and that also handles keeping my brain exercised since the consulting is on some very complex issues. But you are handling that in other ways. It sounds like you’ve got it all worked out except for two things….leaving the Christmas tree up all year? That’s just wrong. And admitting you watch Hallmark movies? You are going to miss having your man card when it is revoked!

Thanks, always enjoy these updates!! Its like a window to the retirement life we are working towards…

Would be interested in reading your detailed review and advice on the estate planning process.. as you say: many many questions to think and talk through… I cant be the only finding this daunting…

Would love to know if your estimated colonoscopy costs end up including all related costs. I have had the frustrating experience that the estimates I get for medical procedures only include the main procedure and not the other costs such as pathology, other Dr. who read results,etc. Even when I say I want all the these things at time of estimate I am not given them and later told that of course that wouldn’t have been in the estimate. Maybe it is because they know I am not cash payer but I need to watch impact of medical costs with deductible etc. The 3k does sound right with insurance though, assumming it doesn’t fall under federally mandated preventative coverage.

Thanks for your blog. The only thing keeping me from FIREing is the cost / risk of health care. We don’t have serious health issues, but stuff happens. If something serious happens, the cost could be bankrupting. You may have a post on how to mitigate the catastrophic risk (but I haven’t searched for it yet). If you haven’t posted and have the time and desire to write about it, it would be great to hear your thoughts.

I take issue that if you had insurance it would cost $3,000 for the service. They jack the price up so high, and then discount it so heavily. I have to get up off the couch to find my records, and don’t really want to do it, but I think that the actual cost the insurance discount was $750 (I could be wrong – it’s happened). Anyway, my thought was you should go back and press them for a higher discount. The other poster was correct, you need to make sure that is the all in price of $1,000.

Thanks!

Loved the post! I am so mentally there, but still have a few years to go financially.

Regarding your question about a Christmas cruise, we just took one in the Caribbean with the extended family (my family, my parents, and my brother and sister and their families–12 people in all). We actually were on the boat the week before Christmas (Dec. 15 to 22), which for us was the best of both worlds as we still got to have Christmas morning at home. It’s more expensive to go during this time, but it was really a lot of fun. The ship was decorated very nicely, lots of Christmas music, large gingerbread village in the dining room, etc. And a lot of the ports had decorations up in the harbor areas. We had a fantastic time–I think you’ll love it.